Bonds, Savings

Should you sell your T-bill and SSB to put into the OCBC 360 account? A lesson on re-investment risk.

By Beansprout • 05 Nov 2022 • 0 min read

Apart from comparing interest rates, we can also look at the time period of the investment when assessing different options in the market.

In this article

What happened?

In case you have not heard, OCBC has raised the interest rate on its flagship OCBC 360 account to up to 7.65% per annum.

As our guest writer shared, it will be difficult to get to the top tier interest rate of 7.65% of annum.

However, you can still earn 4.65% per annum on the first S$100,000 in your bank account by crediting at least S$1,800 a month, saving, as well as making charges to selected credit cards.

This created a lot of buzz in the Beansprout community, as many of you started asking if we would sell our Singapore Savings Bonds and T-bills to put money into the OCBC 360 account.

Comparing T-bill and SSB with OCBC 360

If you are new to investing in bonds, Beansprout is here to guide you along the journey.

Here’s one thing we can all learn today – Apart from comparing interest rates, we can also look at the time period of the investment when assessing different options in the market.

After all, we will potentially get back the money we invested in a bond at different periods, depending on when the bond matures.

For example, the Singapore T-bill has maturities of 6 months or one year. On the other hand, the Singapore Savings Bond allows you to invest for up to 10 years, while allowing you to exit your investment in any given month with no penalties.

What this means is that we need to choose the right product depending on how long we want to lock-in the expected interest rates for.

We can look at this using a simple illustrative example of two 6-month T-bills and the 1-year interest rate on the SSB.

In the November issuance of the SSB, the 1st year interest rate is at 3.08%.

If we put S$100,000 into the SSB, we would receive S$3,080 of interest in one year.

If we put S$100,000 into the 6-month T-bill based on the latest interest rate of 4.19% per annum, we would get about S$2,089 worth of interest over six months.

If the interest rate stays at 4.19% per annum in the auction 6 months later, we can reinvest our S$100,000 into the next 6 month T-bill and receive another S$2,089 of interest for another six months.

Over the 1-year period, we would have received about S$4,178 worth of interest, above the S$3,080 of interest received for the Singapore Savings Bond.

Why we should start thinking about re-investment risk

If interest rates stay the same or even go up from where they are currently, it’s good news for savers because we are able to earn more interest income over time.

The risk is that the interest rate is lower when we get back the money from the bonds that are maturing.

For example, if the yield on the 6-month T-bill falls to 1.00% per annum six months later, we would just be getting about S$500 worth of interest.

Adding this to the S$2,089 worth of interest received in the first six months, the total interest received would be about $2,589. This is below the S$3,080 worth of interest received for the SSBs over the first year.

Is there a risk that interest rates might go down?

The interest rates in Singapore follow the interest rates in the US closely, so it might be useful to track the direction of the US interest rates.

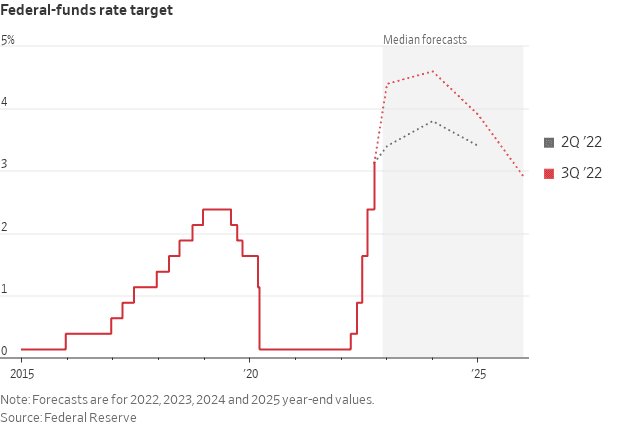

US Central bank officials have projected in September that interest rates will continue to rise further in 2023, before coming down in 2024.

What this means is that while we should take into consideration the higher interest rates when planning our finances, we should not assume that interest rates will keep going up when making our investment decisions.

How does OCBC 360 compare to SSB?

Having introduced the concept of time horizon when it comes to planning our finances, it should become clearer how we should think about the OCBC 360 vs the SSB.

First and foremost, the OCBC 360 is a deposit account. As a deposit account, it is generally used for short term cash needs as it is highly liquid.

It is also insured by the Singapore Deposit Insurance Corporation (SDIC) for up to S$75,000 per account.

However, there are some considerations we should bear in mind when using a deposit account for investment purposes with the high interest rates.

First and foremost, the interest rates offered by the banks can be changed anytime. Prior to the latest increase in interest rates on 1 November, OCBC just changed the interest rates previously in September.

What this means is that while interest rates may continue to go up, we cannot assume that they will stay high and not come down eventually.

Hence, if we want to capture the higher interest rates now, we can consider the SSB which gives certainty on the interest rates for the next 10 years.

The other advantage of the SSB is that we can choose to exit our investment in any given month, with no penalties.

How does OCBC 360 compare to T-bill?

What if I want to get a higher interest rate for just the next 6 months?

The yield on the 6-month T-bill rose to 4.19% per annum in the latest auction on 27 October.

On a headline level, you would be able to get a higher interest rate by putting your money into the OCBC 360 account compared to buying a 6-month T-bill.

The risks of interest rates coming down sharply in the next six months is also lower, based on Fed’s projections.

However, you’d need to be aware of the terms and conditions to get to the 4.65% interest rate with the OCBC 360 account, and make sure you are able to meet them.

Also, while we can put our CPF OA money into the T-bill, we can’t put our CPF OA money into the OCBC 360 account.

What would Beansprout do?

By now, we hope we have been able to share with you why it is important to consider our time horizon when planning our finances.

This is one of our considerations when deciding which product to invest in to benefit from the higher interest rates.

In summary, a deposit account like the OCBC 360 may allow us to earn a higher interest rate on our spare cash.

However, there is no certainty that the interest rates may stay where they are. As such, we would not view them the same way as investment products such as bonds.

The Singapore Savings Bond has the advantage of allowing us to capture high interest rates with certainty for up to 10 years, while providing the flexibility of redemption anytime.

The Treasury Bill has the advantage of potentially allowing us to help us earn a higher interest rate compared to the CPF OA account for a 6-month or 12-month period.

This article was first published on 05 November 2022 .

Read also

Want to learn more? Discover more Bond-related insights here.

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments