REITs

S-REITs hammered with rising interest rates. Are they worth buying now?

By Beansprout • 25 Oct 2022 • 0 min read

Rising interest rates can potentially affect REITs by driving weaker rental prospects, increasing borrowing costs, and making them less attractive investments.

In this article

TL;DR

- Rising interest rates can potentially affect REITs by driving weaker rental prospects, increasing borrowing costs, and making them less attractive as an asset class.

- Singapore REITs (S-REITs) with retail, office, industrial and hospitality assets in Singapore have seen rising rents in recent quarters.

- However, as lower risk assets such as government bonds now also offer decent interest rates, S-REITs may not offer the best risk-reward.

- We wouldn’t be in a hurry to pick the bottom in S-REITs due to risks of further interest rate hikes and a weakening economy.

What happened?

Many holders of S-REITs have reached out to ask what they should be doing now.

The S-REITs had a bruising few weeks, after a spike in interest rates triggered a sell-off.

This is especially so for the S-REITs with overseas assets.

Manulife US REIT has fallen by more than 50% so far this year, and Prime US REIT is down 45% so far this year (both as of 21 October 2022).

Another investor favourite, Keppel DC REIT, has fallen by more than 30%.

Even the blue chip REITs have not been spared.

Both CapitaLand Integrated Commercial Trust and Frasers Centrepoint Trust are down 12% in the past one month alone (as of 21 October 2022).

That’s not what many investors would have seen coming buying into REITs expecting a relatively safe return.

So the question that is at the back of many investors minds is – What should we do with REITs now? Are they a buy after the sharp decline?

Are REITs a buy after the recent decline?

Interest rates have moved sharply higher in recent months.

And the key reason why REITs have come down so sharply is because of the various ways they are impacted by higher interest rates.

This would include:

- Higher interest rates may cause a slowdown in the economy, leading to weaker rental prospects

- Higher interest rates may lead to higher borrowing costs and lower dividend distributions

- Higher interest rates may make REITs less attractive as an asset class compared to other assets

Let’s look at each of these factors individually to determine if investor worries are justified.

#1 – Will higher interest rates change REIT fundamentals?

Let’s face it – the economic outlook isn’t looking that great at the moment.

The concern that many investors have is whether high inflation and slower growth will affect the ability of REITs to earn a good rental income on their properties.

However, the weaker economic environment has not dented the strong operational performance of most sub-sectors as yet.

In retail, retail sales grew 13% in August compared to the previous year. CICT also noted that rents that they signed are on a positive trend in 3Q22.

In office, Grade A office rents rose 2.9% in 3Q22 compared to the previous quarter to reach a 14-year high, according to JLL.

In hospitality, average hotel room rates rose to $259 in July, the highest in nearly 10 years.

One area where we have seen some weakness is in overseas markets, particularly in US office.

The average physical occupancy for the top-10 cities remains low at 47% as of October 2022. Leasing volumes also slowed down in in the first half of the year.

#2 – Will higher interest rates affect distributions?

It’s quite clear that interest rates have gone up sharply in recent months.

As REITs rely on borrowing to acquire their portfolio of assets, this will lead to potentially higher interest expense and lower dividend distributions.

The extent to which interest expenses would be higher, depends on:

- The amount of debt the REIT has, as measured by its gearing level (total debt over total assets)

- The amount of debt that is maturing each year, which will have to be refinanced at a potentially higher interest rate

- The amount of existing borrowing that is locked in at fixed interest rates, shielding the REIT from interest rate increases.

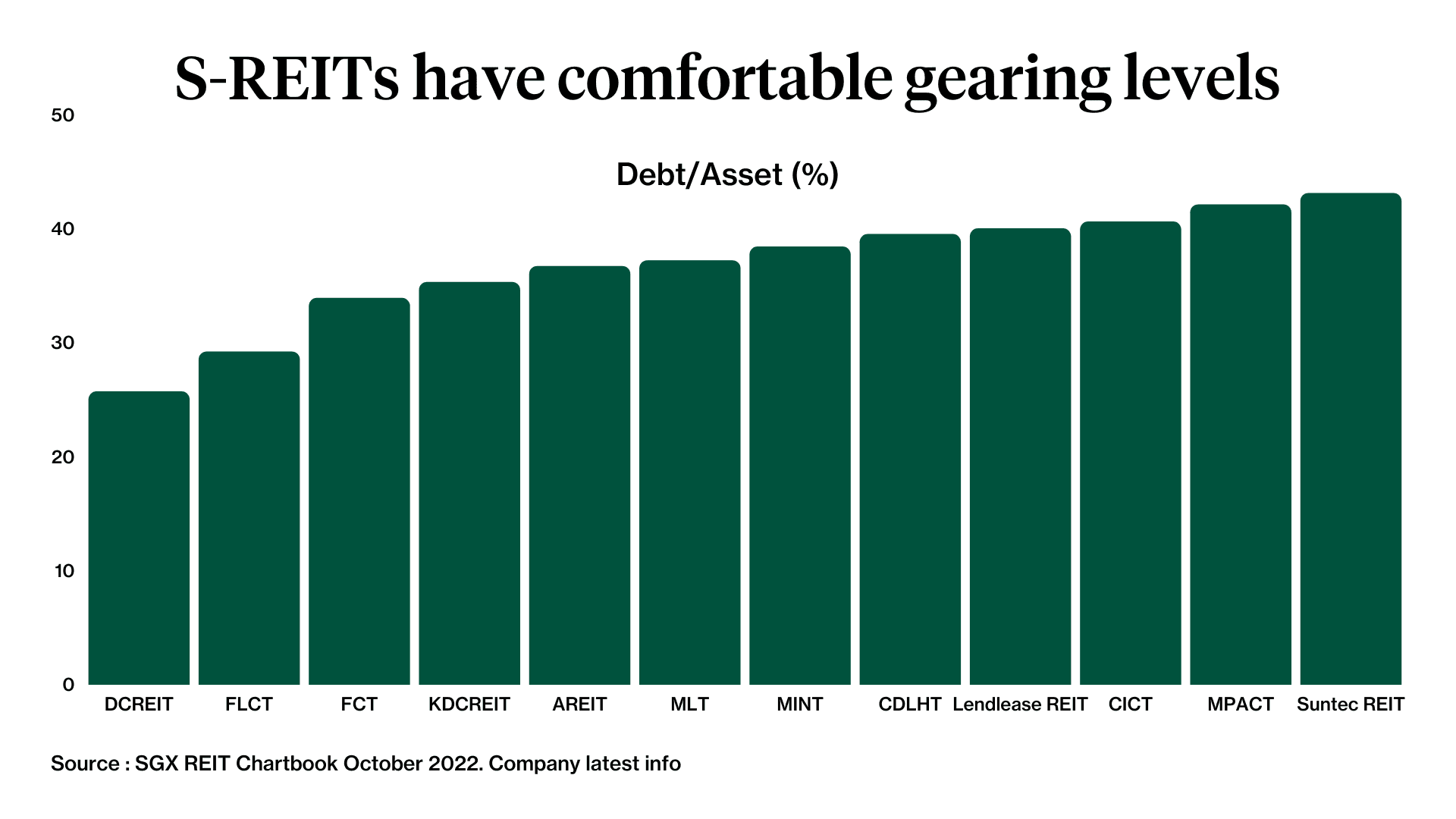

According to the latest quarter filings as of 30 September 2022, Singapore REITs have an average gearing ratio of 36.9%. This is comfortably within the regulatory limit of 50%.

However, there is a wide range of gearing levels amongst the REITs. For example, some REITs have kept their gearing low at close to 30%, including Frasers Logistics & Commercial Trust (29.2%) and SPH REIT (30.1%).

On the other hand, some REITs have gearing levels of above 40%, including Suntec REIT (43.1%), Mapletree Pan Asia Commercial Trust (42.1%), and CICT (40.6%).

The REITs also have different amount of debt that has been locked in at fixed rates.

For example, Digital Core REIT has only about 50% of its debt hedged as at 30 June 2022.

Putting these together, it is estimated that a 1 percentage point increase in interest rates, could lower their distributions per unit (DPU) by a range of 1-8%.

#3 – Will higher interest rates affect REIT valuation?

As interest rates go up, it makes lower-risk assets such as government bonds appear relatively more attractive compared to riskier assets such as REITs.

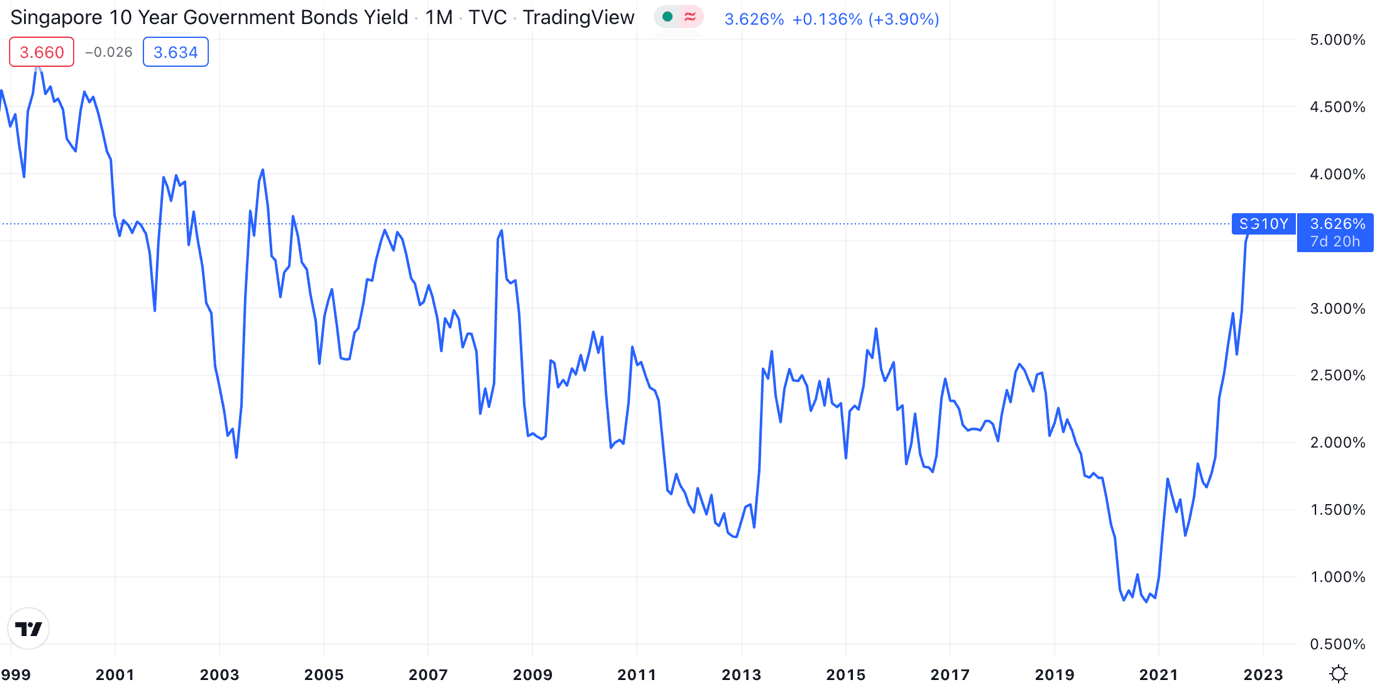

For example, the yield on the 10-year Singapore government bond has risen to 3.6% as of 21 October.

When you’re able to earn such a good yield on an effectively risk-free asset like the Singapore government bond, you’d naturally demand a higher yield for a relatively higher risk asset like REITs.

This is especially so with the greater economic uncertainty and potentially cuts to expected dividends.

In the past, investors have demanded a yield that was 3.85 percentage point (3.85%) above the 10-year government bond yield to compensate for the risks they are taking for holding REITs. This differential in yield is called the yield spread.

Adding 3.85% on top of the 10-year government bond yield of 3.6% would mean that yields on REITs need to be closer to 7.45% for them to be fairly-valued.

Based on the forward dividend yield of 6.2% as of 30 September 2022, it might seem like the REITs are not fully reflecting the higher interest rates as yet.

What would Beansprout do?

Singapore REITs have fallen sharply in the past few months, but it might be too early to say that the worst is over.

After all, interest rates could continue to climb as inflation remain persistent.

The fundamentals of S-REITs have been strong so far, but they could deteriorate with a worsening economic outlook.

#1 – Interest rates could move higher

One of the things that investors have underestimated is how quickly interest rates have moved up.

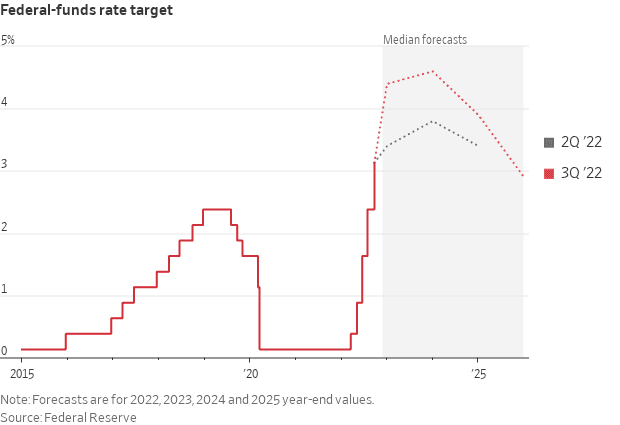

The US Fed is projecting that its benchmark interest rates could rise by another 1.5 percentage points (1.5%) to 4.6%.

However, if inflation remains more persistent like how it has been so far, there’s a chance that we’ll see even sharper increases in interest rates.

This would make REITs even less attractive compared to a lower risk asset like treasury bills or SSBs.

#2 – Prospects could worsen if economic slowdown persists

The property market in Singapore has held up well so far despite all the global economic headwinds.

And we’re not just talking about residential property, but also retail, office and industrial segments.

What we would need to be wary of is that the rental prospects could worsen if the economic slowdown becomes a full-fledged recession. Or even worse, a financial crisis.

In summary, we wouldn’t be in a hurry to pick the bottom in Singapore REITs.

If we want to be holding on to REITs, we would also be more selective to make sure that they are able to withstand the higher interest rates.

With the economic uncertainty out there, we think the risk-reward might still be better for short duration government bonds.

Find out more about how much we’d allocate to REITs in our simulated portfolio.

Access more expert insights on C38U, AREIT, MPACT and Keppel DC REIT.

This article was first published on 25 October 2022 .

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments