Bonds

How to construct a T-bill and SSB bond ladder to maximise your passive income

By Beansprout • 18 Oct 2022 • 0 min read

A bond ladder consisting of Singapore Savings Bonds (SSBs) or Treasury Bills (T-bills) can help you to earn a passive income while reducing exposure to interest rate fluctuations.

In this article

TL;DR

- A bond ladder is a portfolio of bonds with different maturities. This can consist of Singapore Savings Bonds (SSBs) or Treasury Bills (T-bills).

- A bond ladder can help you to earn a passive income while reducing exposure to interest rate fluctuations.

- For a bond ladder using SSBs, there might be limitations from the individual holding and allotment limits. However, SSBs offer flexibility as they can be redeemed anytime.

- We have not seen allotment limits for T-bills so far, and a bond ladder can help to overcome the uncertainty of not knowing the cut-off yield in advance as interest rates earned are averaged out over time.

What is a T-bill and SSB bond ladder?

One of the topics that the Beansprout community has been asking us to share is how to build a bond ladder.

After all, there is now more interest in T-bills and SSBs, but many are worried about making lump sum investments into these bonds with the significant interest rate volatility.

A bond ladder is a portfolio of bonds that have different maturities. This can consist of Singapore Savings Bonds (SSBs), Treasury Bills (T-bills) or even corporate bonds.

Instead of buying bonds that mature on the same date, you can purchase T-bills or SSBs that mature at staggered future dates.

This strategy is designed to reduce exposure to interest rate fluctuations while earning a passive income.

By spreading out the maturity dates, you can avoid timing the market and figuring out near term interest rates fluctuations.

Let’s explore how we can construct a bond ladder using T-bills and SSBs.

How to construct a SSB bond ladder?

First and foremost, we must understand how we can structure a bond ladder using Singapore Savings Bond (SSB).

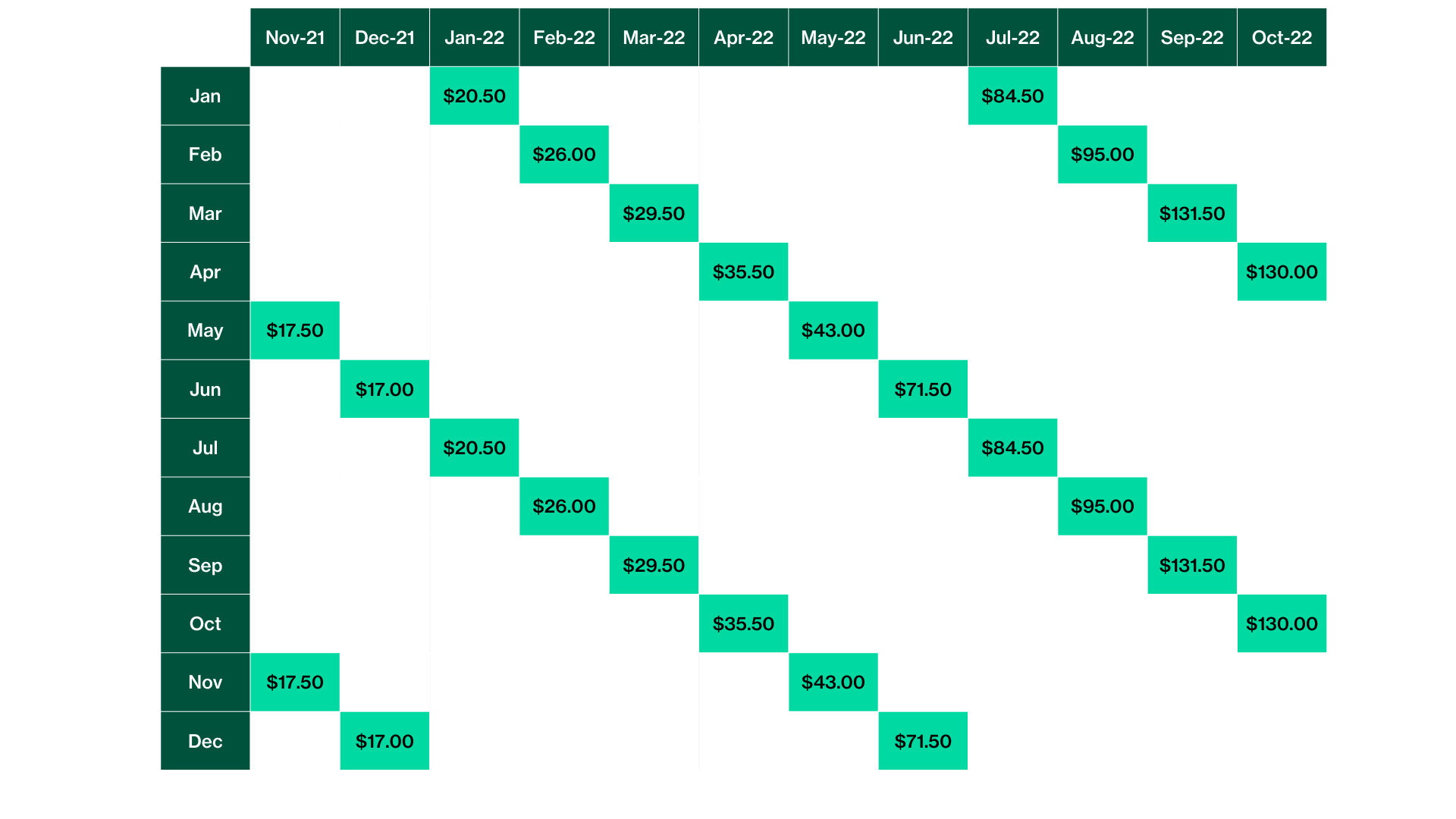

SSB pays a semi-annual interest and the bond ladder would allow us to receive monthly coupon payments.

A January issuance of SSB will be paying out interest in July this year and January next year, and a February issuance of SSB will be paying out interest in August this year and February next year next year.

Jan-22 | Feb-22 | Mar-22 | Apr-22 | May-22 | Jun-22 | |

|---|---|---|---|---|---|---|

| Jan | Interest | |||||

| Feb | Interest | |||||

| Mar | Interest | |||||

| Apr | Interest | |||||

| May | Interest | |||||

| Jun | Interest | |||||

| Jul | Interest | |||||

| Aug | Interest | |||||

| Sep | Interest | |||||

| Oct | Interest | |||||

| Nov | Interest | |||||

| Dec | Interest |

How much interest income would you earn with a SSB bond ladder?

For illustration purposes, we will be investing $10,000 into SSB on a monthly basis.

Over the past year, we would be able to get full allotment of S$10,000 in almost every month. The exception would be August 2022 where we would end up either with S$9,000 or S$9,500.

Let’s be optimistic and use $9,500 allotment in August 2022 for this example. A summary of our allotment amount, 1-year interest rate, and 10 year average interest rate is shown below.

Date | Amount | 1st year | 10-year average |

Oct-22 | $10,000 | 2.60% | 2.75% |

Sep-22 | $10,000 | 2.63% | 2.80% |

Aug-22 | $9,500 | 2.00% | 3.00% |

Jul-22 | $10,000 | 1.69% | 2.71% |

Jun-22 | $10,000 | 1.43% | 2.53% |

May-22 | $10,000 | 0.86% | 2.09% |

Apr-22 | $10,000 | 0.71% | 1.91% |

Mar-22 | $10,000 | 0.59% | 1.79% |

Feb-22 | $10,000 | 0.52% | 1.64% |

Jan-22 | $10,000 | 0.41% | 1.71% |

Dec-21 | $10,000 | 0.34% | 1.45% |

Nov-21 | $10,000 | 0.35% | 1.39% |

We will calculate the interest payment based on the first year interest rate.

The total interest we will receive in our first year of holding this SSB bond ladder will be $1,403, over a period of May 2022 to October 2023.

This would represent an average interest rate of 1.17% on our total investment of S$119,500.

By building a bond ladder, we get to blend the interest rates we are getting from our portfolio of SSBs.

While the interest rates received for the November 2021 tranche is low at just 0.35%, we would have received a higher interest rate on more recent issuances of SSBs.

The good thing about SSBs is that we can redeem the SSBs and re-invest them into the latest issuances of SSBs.

So we can redeem the November 2021 SSB and reinvest into the more recent issuances of SSBs.

How to construct a Singapore T-bill bond ladder?

Can we build a bond ladder using T-bills instead? We will show you using the illustrative example below.

Again, we can purchase S$10,000 for each 6-month T-bill from November 2021, and re-invest the money after the 6-month maturity period.

The initial investment is shown in the rows in orange below, while the amount reinvested is shown in the rows in green.

Issue | Maturity | Yield | Amount | Refund/Interest |

16-Nov-21 | 17-May-22 | 0.49% | $10,000 | $24.40 |

30-Nov-21 | 31-May-22 | 0.55% | $10,000 | $27.40 |

14-Dec-21 | 14-Jun-22 | 0.55% | $10,000 | $27.40 |

28-Dec-21 | 28-Jun-22 | 0.53% | $10,000 | $26.40 |

11-Jan-22 | 12-Jul-22 | 0.55% | $10,000 | $27.40 |

25-Jan-22 | 26-Jul-22 | 0.48% | $10,000 | $23.90 |

8-Feb-22 | 9-Aug-22 | 0.67% | $10,000 | $33.40 |

22-Feb-22 | 23-Aug-22 | 0.76% | $10,000 | $37.90 |

8-Mar-22 | 6-Sep-22 | 0.78% | $10,000 | $38.90 |

22-Mar-22 | 20-Sep-22 | 0.95% | $10,000 | $47.40 |

5-Apr-22 | 4-Oct-22 | 1.22% | $10,000 | $60.80 |

19-Apr-22 | 18-Oct-22 | 1.32% | $10,000 | $65.80 |

4-May-22 | 1-Nov-22 | 1.56% | $10,000 | $77.40 |

17-May-22 | 15-Nov-22 | 1.69% | $10,000 | $84.30 |

31-May-22 | 29-Nov-22 | 1.80% | $10,000 | $89.80 |

14-Jun-22 | 13-Dec-22 | 2.04% | $10,000 | $101.70 |

28-Jun-22 | 27-Dec-22 | 2.36% | $10,000 | $117.70 |

12-Jul-22 | 10-Jan-23 | 2.66% | $10,000 | $132.60 |

26-Jul-22 | 24-Jan-23 | 2.93% | $10,000 | $146.10 |

10-Aug-22 | 7-Feb-23 | 2.87% | $10,000 | $142.30 |

23-Aug-22 | 21-Feb-23 | 2.98% | $10,000 | $148.60 |

6-Sep-22 | 7-Mar-23 | 2.99% | $10,000 | $149.10 |

20-Sep-22 | 21-Mar-23 | 3.32% | $10,000 | $165.50 |

4-Oct-22 | 4-Apr-23 | 3.32% | $10,000 | $165.50 |

18-Oct-22 | 18-Apr-23 | 3.77% | $10,000 | $188.00 |

How much interest income would you earn with a T-bill bond ladder?

In this illustrative example, we would have received a total interest payment of about S$2149.70 over the 12 month period.

It’s worth pointing out that we would be able to receive an effective interest payment of $353.50 in April 2023 from our T-bill purchases on 4th October and 18th October this year.

This would be more than sufficient to cover our utility bills, phone bills and even allow us to enjoy a nice Haidilao meal!

Should you use a SSB or T-bill bond ladder?

Here are some additional factors we’d consider when deciding whether to build a SSB or T-bill bond ladder.

#1 – SSB may have allotment limits

It is worth noting that there is a maximum of S$200,000 of SSBs that any individual can hold.

Hence, if you have more than S$200,000 (lucky you!), then you’d need to include other bonds as part of your bond ladder strategy.

Next, we have seen allotment limits to SSBs in recent months as demand for SSBs has continued to grow with rising interest rates.

As we will not know what’s the allotment limit at the point of subscription, this makes it difficult to build a bond ladder based on our target amount of passive income.

Based on the SSB issuances in recent months, the maximum allotment per month can range from $9,500 to $42,500.

Once again, we may have to supplement our bond ladder strategy with T-bills if we are not able to get our target allocation of SSBs.

#2 – SSBs offer more flexibility

One benefit of SSB is that it is flexible. We can redeem the SSBs without any penalties, and still be able to earn the accrued interest.

This means that if interest rates move higher, you can redeem your SSB at any time and reinvest at higher rates.

On the flip side, if the rates fall, you’ll still have some bonds locked in for the longer term at higher yields.

What would Beansprout do?

One of the reasons why some investors are less keen on the T-bills is because there’s no certainty on the interest rate before the auction.

If you’re holding back from buying the T-bills because you’re uncertain of the yield, then a bond ladder offers a way for you to spread out your investment over several issuances.

Using this approach, you might feel less upset for making a lump-sum investment, if interest rates were to surge subsequently.

The other potential benefit of using a bond ladder is that you’d be able to receive regular interest payments to fund your passive income.

The good news is that the interest rates for both the T-bills and Singapore Savings Bonds have gone up recently. If you are looking at start on your bond ladder, you can read more about how to apply for the T-bill and SSBs.

This article was first published on 18 October 2022 .

Read also

Want to learn more? Discover more Bond-related insights here.

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments