How to capture higher interest rates using a bond fund.

By Beansprout • 15 Nov 2022 • 0 min read

Our questions on the United Fixed Maturity Bond Fund 1 were answered by representatives from UOB Asset Management and Tiger Brokers at the seminar.

In this article

This post was created in partnership with Tiger Brokers (Singapore) Pte Ltd. All views and opinions expressed in this article are Beansprout's objective and professional opinions.

TL;DR

What happened?

We received many questions from the Beansprout community after our previous writeup on the United Fixed Maturity Bond Fund 1.

This did not come as a big surprise, since bond funds are relatively new to a lot of investors in Singapore.

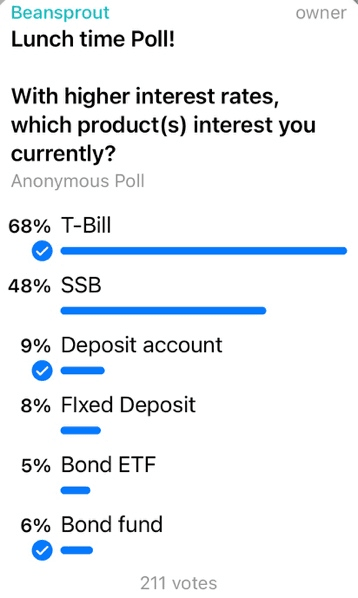

In fact, in a recent poll that we conducted in the Beansprout community, only 6% of respondents said that they are interested in bond funds with higher interest rates.

T-bills and SSBs drew the most interest within the community.

To find out the answers to the questions asked, we attended a seminar about the fund on 9th November.

We were glad to see that there were close to 200 others who were equally keen to learn more about the fund from representatives of UOB Asset Management and Tiger Brokers.

What we learnt at the United Fixed Maturity Bond Fund 1 seminar

The Q&A session at the seminar offered a chance for participants to ask their burning questions about the fund.

Here’s what we found out!

#1 – What is the USP of the fund?

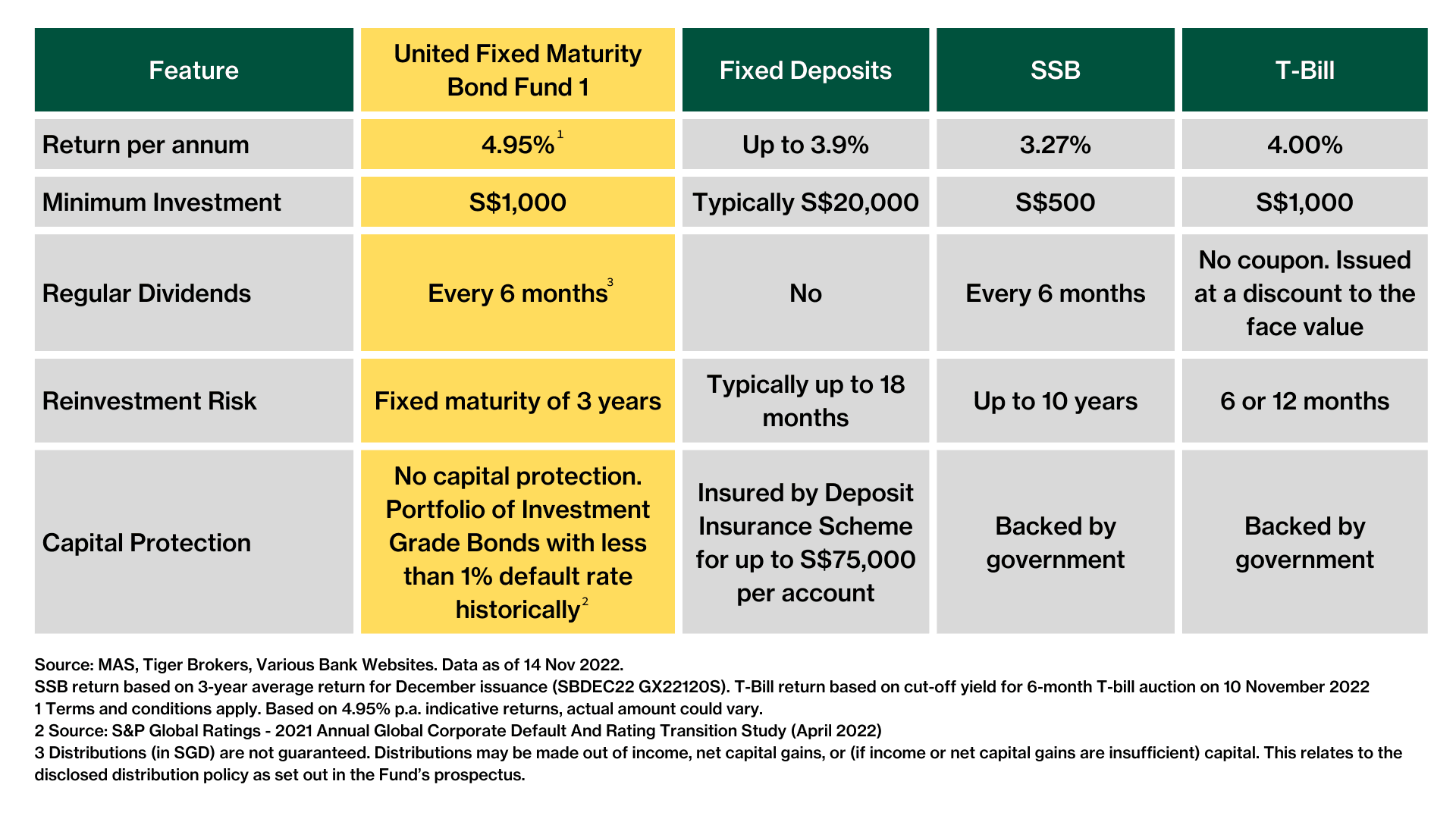

The fund invests in a portfolio of investment-grade bonds that matures within 3 years to generate an indicative return of 4.95% per annum1. This would allow investors to achieve the following:

Capture higher interest rates: The fund is positioned to take advantage of current high interest rates as yields on Asian investment grade bonds are now at a 13-year high.

Remove reinvestment risk of using shorter term instruments: The fund’s buy-and-hold strategy means you do not have to worry about getting lower interest rates when your current holding of shorter duration bonds mature over the course of the next one to two years.

Regular dividends every 6 months: The fund would allow you to receive semi-annual income distribution of about 3-4% p.a.2

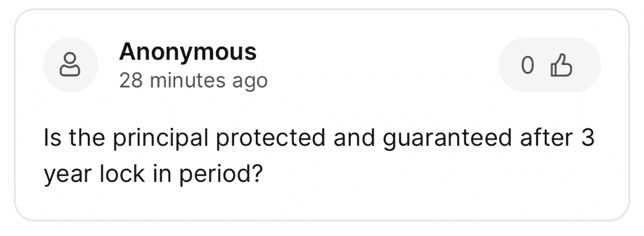

#2 – Is the principal protected and guaranteed after 3-year lock in?

Unfortunately, the fund is not principal protected as the fund will invest in a portfolio of investment-grade bonds. There will hence be various risks including risk of issuer defaulting.

However, as the fund invests in investment-grade bonds that mature within three years, the default risks are seen by rating agencies to be lower.

In fact, the historical default rate for such a portfolio of investment-grade bonds is less than 1%, according to a study by S&P Global Ratings.

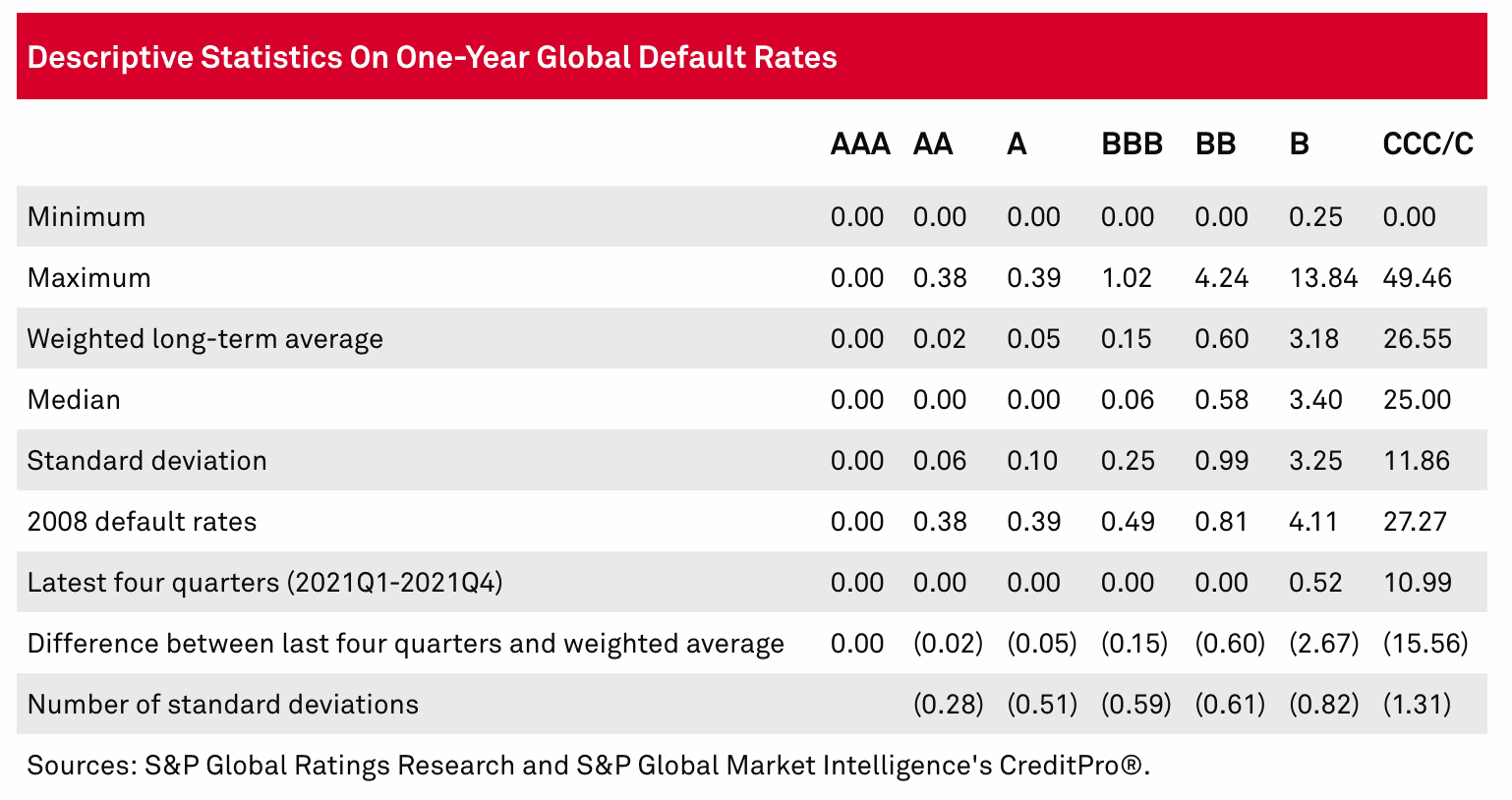

Based on S&P ratings, an investment grade bond is one that has been rated AAA, AA, A or BBB.

Using the lowest rating of BBB as an example, the median one-year global default rate is 0.15%. During the global financial crisis in 2008, the default rate was at 0.49%.

#3 – T Bills and SSB interest rate are also at least 3%. How does this fund compare with them?

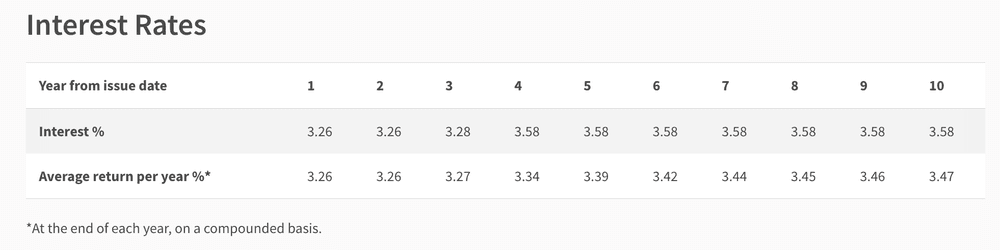

The good thing about the T-bill and SSB is that they are fully backed by the Singapore government.

However, the indicative return of the United Fixed Maturity Bond Fund 1 of 4.95% p.a.1 is higher than the yield on both the T-Bill and SSB.

We’ve also been sharing that we should consider the time period of the investment when assessing different options in the market.

For example, investors in the 6-month T-bill would face a reinvestment risk when we get back the money from the bonds that are maturing.

This means that if interest rates were to fall significantly, we might get a lower average return if we do not lock in the interest rates now.

#4 – Isn’t this almost like a fixed deposit already?

Fixed deposits are nice as that they are covered by the deposit insurance scheme for up to S$75,000 per account.

The best fixed deposit rate that we see now is at about 3.9%. The minimum deposit size to earn such rates is usually at least S$20,000.

However, you don’t have to be a millionaire to be able to enjoy such returns. The minimum subscription for the fund is just S$1,000.

You'd also need to think about re-investment risk when putting your money in shorter term instruments like a 12-month fixed deposit.

#5 – What are the fees that we will need to pay?

There will be no annual management fee charged for the fund. There will also be no subscription fee charged for the fund.

However, there will be an early redemption fee of 2%. This means that if you decide to take out your money before the 3-year maturity period is up, you will have to pay fees amounting to 2%.

Hence, you’d need to be prepared to leave your money in the fund for three years, or face the risk of earning a lower yield from the redemption charge incurred.

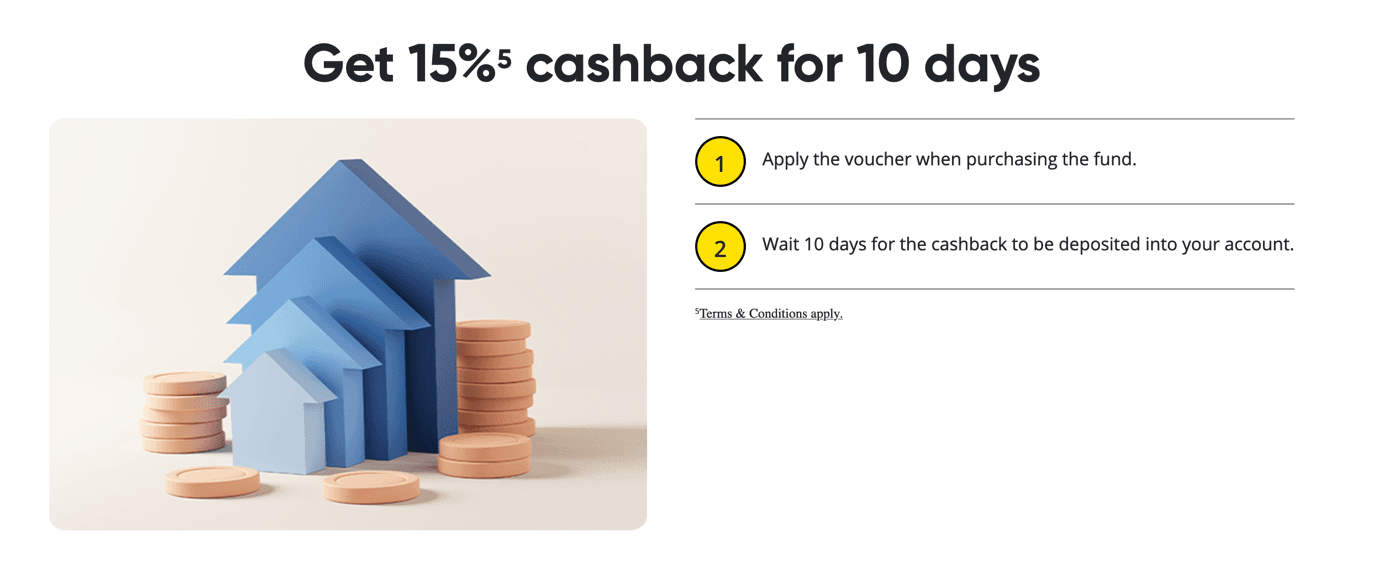

Tiger Brokers will also be throwing in some goodies to make the deal even better!

You’d get a 15% cashback for 10 days when you subscribe to the United Fixed Maturity Bond Fund through the Tiger Brokers platform.

This means that if you put $10,000 into the fund, you’d get a cashback amounting to about $41.

#6 – Is there a maximum amount we can put into the bond?

As there is a limit to the size of the fund, it will be available on a first come, first served basis.

However, as with all investments, we suggest that investors practise diversification to ensure that risks are well managed. In our simulated portfolio, we have a well-balanced mix of stocks and bonds.

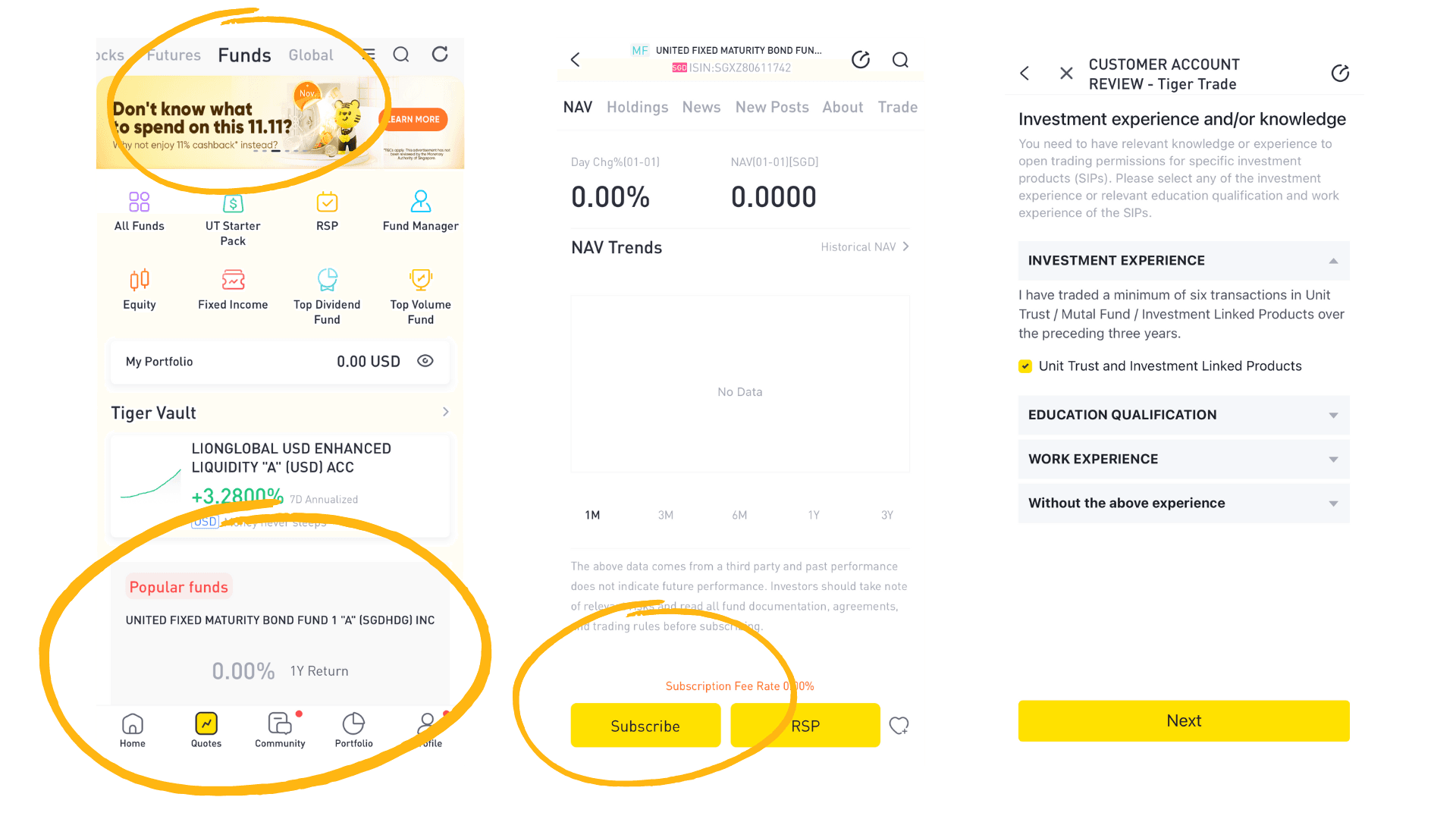

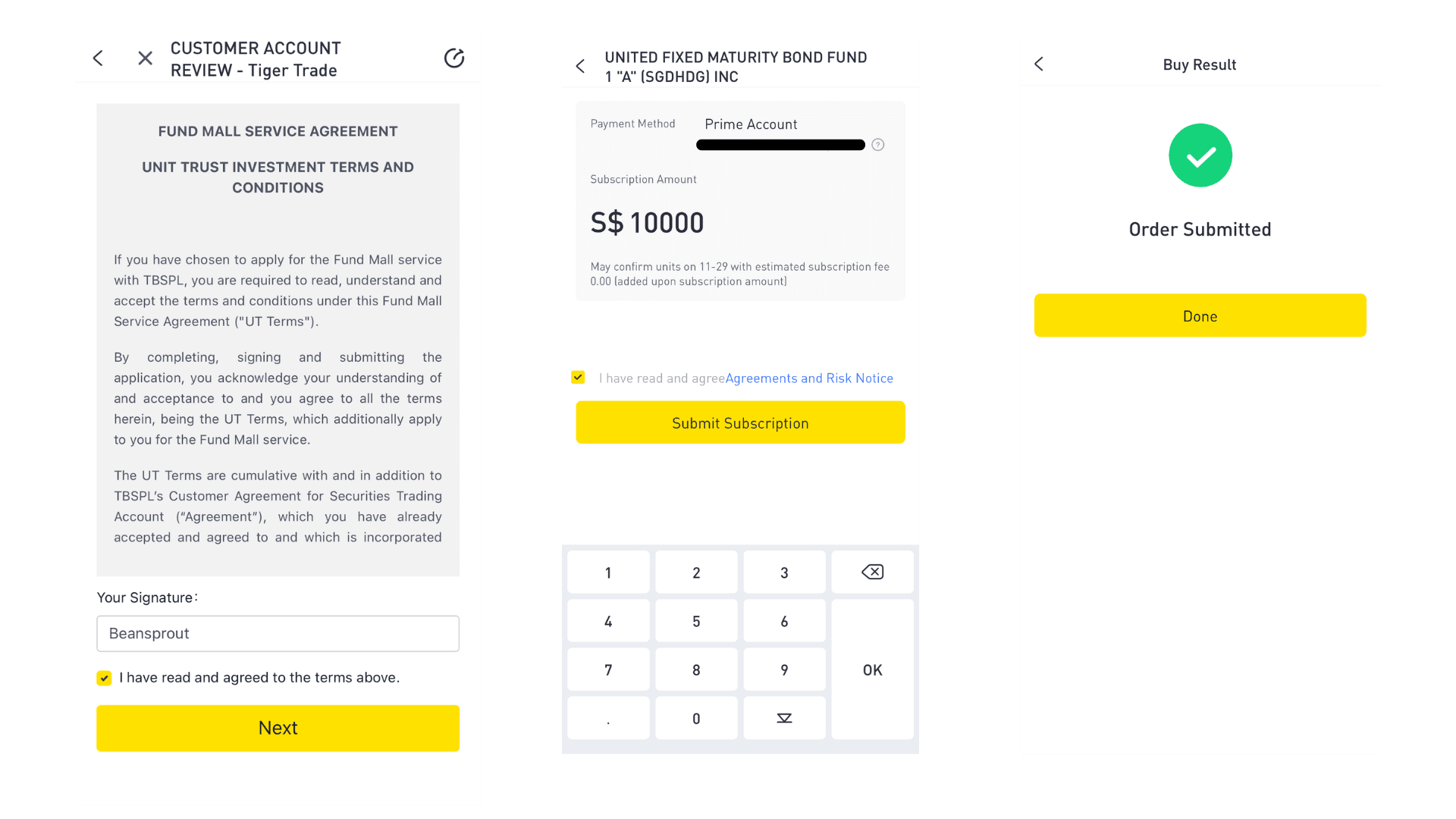

#7 - How to subscribe to the fund on the Tiger Brokers app?

If you're interested, here's a step-by-step guide on how to subscribe to the fund on the Tiger Brokers app.

1. Go to the Quotes tab and look for Funds at the top navigation bar. You'd see the United Fixed Maturity Bond Fund 1 under Popular Funds

2. Click on the Subscribe button

3. You'd be asked to fill in a Customer Account Review form if you have not previously invested in unit trust and investment linked products.

4. You'd be asked to sign after you've read and agreed to the terms and conditions of the unit trust investment.

5. Indicate the amount you'd like to invest in the fund

6. You'd receive a confirmation after you submit your subscription.

Do not be alarmed if you do not see much details on the fund in the subscription page on the app. You'd be able to get more details on the fund through the prospectus and product brochure.

What would Beansprout do?

We'd consider the United Fixed Maturity Bond Fund 1 if we're looking to capture higher interest rates, while not having to worry about re-investment risk from using shorter term instruments.

The United Fixed Maturity Bond Fund 1 is now exclusively available on Tiger Brokers, and subscription has gone live as of 14 November 2022! You can learn how to subscribe to the fund or register your interest through the link here.

If you have more questions, you still have an opportunity to ask the team from UOB Asset Management and Tiger Brokers at the upcoming webinar on 17th November

Sign up now for the free webinar on 17th November and learn more about the United Fixed Maturity Bond Fund 1.

1Terms and conditions apply. Based on 4.95% p.a. indicative returns, actual amount could vary.

2Distributions (In SGD) are not guaranteed. Distributions may be made out of income, net capital gains, or (if income or net capital gains are insufficient) capital. This relates to the disclosed distribution policy as set out in the Fund's prospectus.

Important information

A prospectus for the fund may be obtained from the Manager or any of its appointed distributors. Investors should read the prospectus before deciding whether to subscribe for or purchase units in the fund ("Units"). All applications for Units must be made on application forms accompanying the prospectus or otherwise as described in the prospectus. The value of Units and the income from them, if any, may fall as well as rise. Investments in Units involve risks, including the possible loss of the principal amount invested, and are not obligations of, deposits in, or guaranteed or insured by United Overseas Bank Limited (“UOB”), UOBAM, or any of their subsidiary, associate or affiliate (“UOB Group”) or distributors of the fund. The fund may use or invest in financial derivative instruments and you should be aware of the risks associated with investments in financial derivative instruments which are described in the Fund’s prospectus. The UOB Group may have interests in the Units and may also perform or seek to perform brokering and other investment or securities-related services for the Fund. Past performance of the Manager or other funds managed by the Manager and any prediction, projection or forecast on the economy or markets are not necessarily indicative of the future or likely performance of the fund or the Manager.

This advertisement is purely for informational purposes only with no consideration given to the specific investment objective, financial situation and particular needs of any specific person. It should not be relied upon as financial advice. Past performance or any prediction, projection or forecast is not indicative of future performance. Any funds mentioned herein are for illustration purposes only and should not be construed as a recommendation for investment. You should seek advice from a financial adviser before making any investment. In the event that you choose not to do so, you should consider whether the investment selected is suitable for you.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

This article was first published on 15 November 2022 .

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments