REITs

It’s a lift off! What the US rate hike means for REITs

By Beansprout • 17 Mar 2022 • 0 min read

The US Federal Reserve has indicated that it could raise interest rates by seven times this year. We examine how this will impact Singapore REITs.

In this article

TL;DR

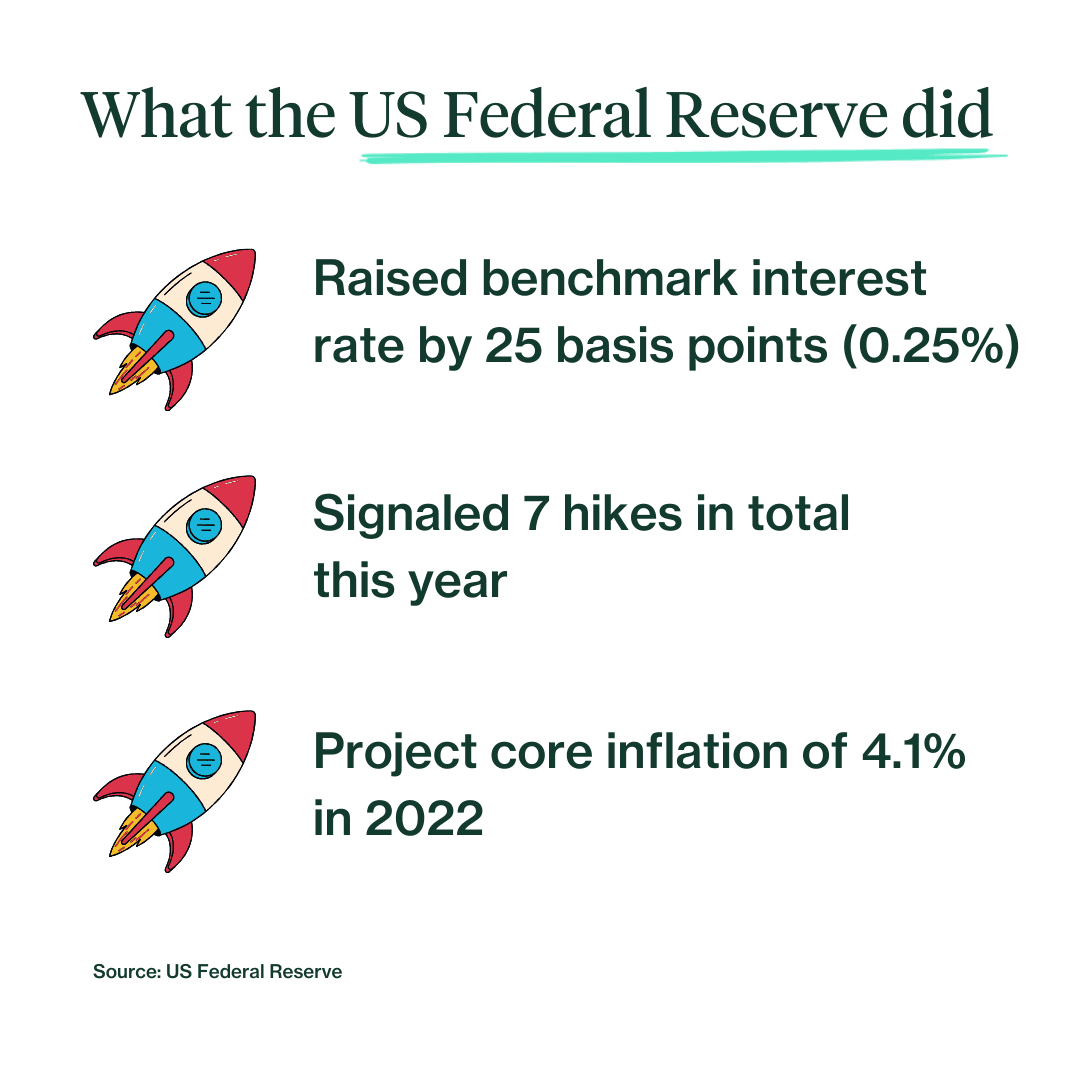

- The US Federal Reserve has hiked its benchmark interest rate by a quarter of a percentage point, and signaled 6 more hikes this year.

- Singapore REITs (S-REITs) have fixed close to 70% of their debt at fixed rates. This could help to cushion the impact of higher interest rates to borrowing costs.

- Following a sell-off in anticipation of the interest rate increase, the dividend yield offered S-REITs appears decent compared to government bonds and the Singapore index.

- In past episodes of rate increases, S-REITs have still been able to generate positive returns. Investors should look for REITs with low gearing, improving rental prospects, and attractive dividend yield.

What happened?

What has been widely anticipated has finally happened. The US Federal Reserve (Fed) has announced an increase in its benchmark interest rate by a quarter of a percentage point, or 25 basis points (bp). This also marks the first rate increase since 2018.

The rate increase has been closely watched given the impact it would have on the global economy. It probably explains why investors have been working so hard to track the level of inflation, as well as every word from US Federal Reserve officials.

In addition to the announced rate hike, the Fed also projected an addition of six more rate hikes in 2022, bringing the total number of hikes to seven this year. This comes against the backdrop of an “extremely tight labour market in high inflation”, as core inflation is expected to reach 4.1% this year.

As investors of real estate investment trusts (REITs), we would naturally wonder how the interest rate hike would affect their performance. After all, REITs are commonly seen to be sensitive to interest rate changes. And let’s face it, seven rate hikes in a year is a lot!

What does this mean?

- Higher borrowing costs for REITs

The higher US benchmark interest rates would likely translate into higher interest rates in Singapore as well. This is because of Singapore’s open economy which makes us exposed to global market movements, and dependence on the US as a trading partner.

REITs are dependent on borrowing to finance the purchase of assets managed by them. Hence, investors would definitely be concerned about how the higher interest rates would affect their borrowing costs and hence dividend distributions. Importantly, we do not want our dividend income from holding the REITs to be impacted by an increase in such expenses.

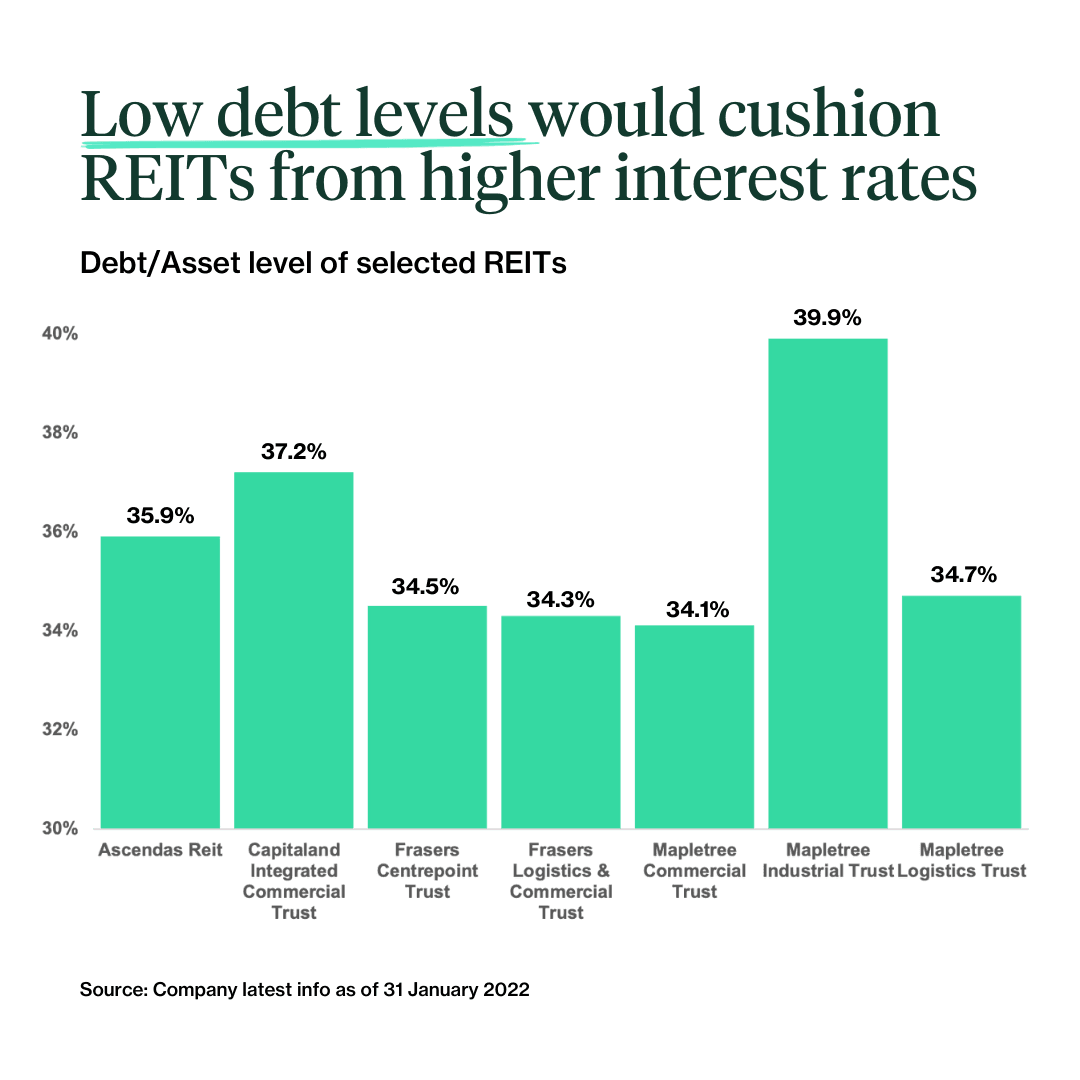

Thankfully, most Singapore REITs have low levels of borrowing, with total debt as a percentage of total assets typically ranging from 30-40%. Also, they have on average secured close to 70% of their borrowing at fixed rates. This would help to cushion the interest rate increases in the near term, as they will not have to pay higher interest for most of existing borrowing until the loan matures.

It has been estimated that a one percentage point (or 100 basis point) increase in interest rates could reduce dividend distributions this year by 3-4%. Hence, if we are looking at a total of seven rate hikes representing a 175 basis point increase, the potential impact to dividend distributions could be about 6%.

- Dividend yield for S-REITs appears decent compared to other assets

The other way that the performance of REITs could be impacted, is through how investors would value them into a rising interest rate environment. Some investors may perceive the dividend yield offered by the REITs to be less attractive compared to safer assets such as government bonds as the benchmark rate rises. This may lead to a sell-off in their holdings of the REITs.

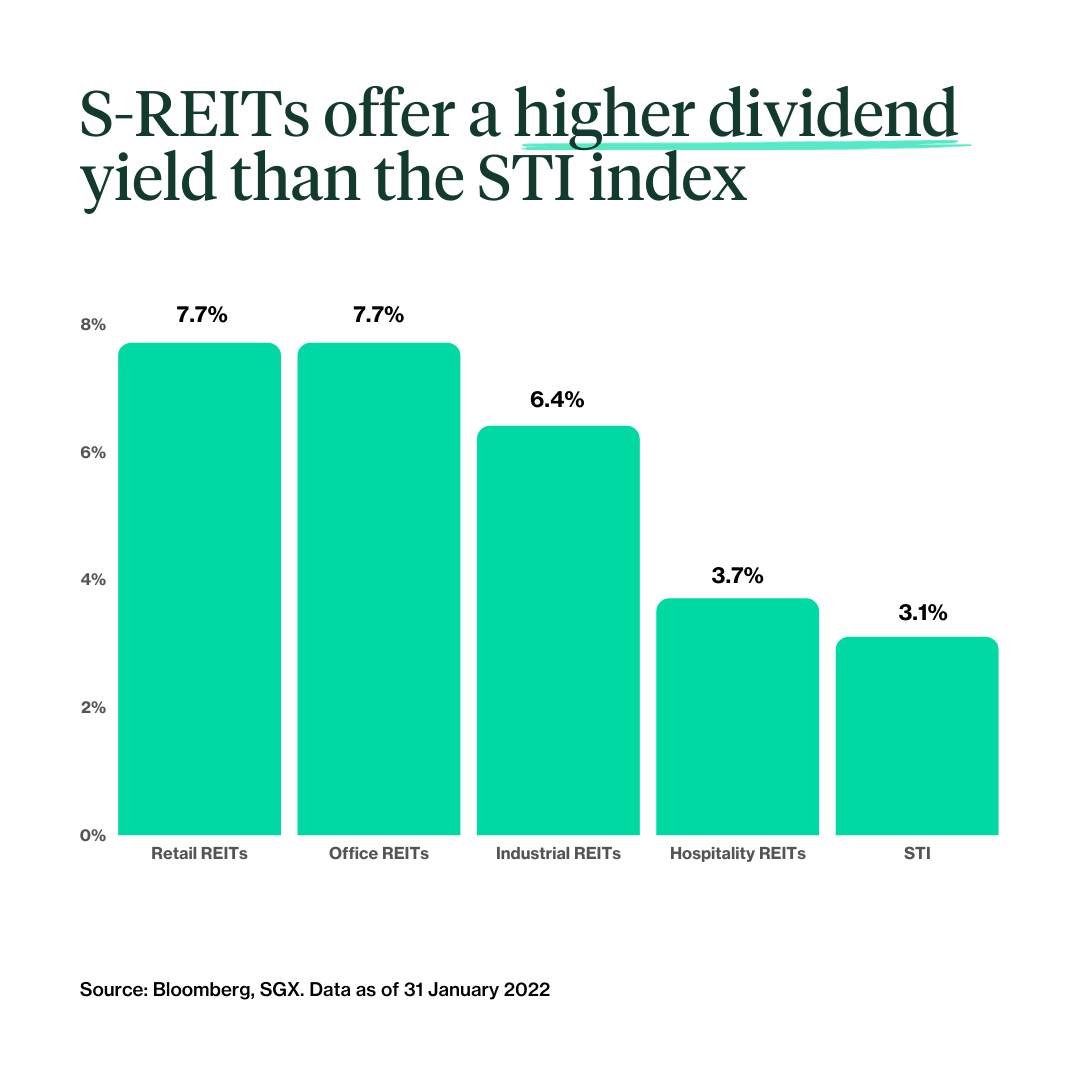

For illustration, the expected forward dividend yield for the Singapore S-REIT index was at about 6.0% as of 31 January. On the other hand, the yield for holding the Singapore government bond for 10 years is at about 1.9%. This means that someone holding on to a basket of Singapore REITs would earn a higher dividend yield of about 400 basis points compared to someone holding on to a safer asset like the Singapore government bond.

Of course, the faster the increase in the yield from holding the government bonds, the less attractive it would be on a relative basis holding on to the REITs. The saving grace here is that yield differential currently of about 400 basis points is already quite close to the historical average.

This means that investors might have already partly factored in the interest rate increases in how they value the REITs. This comes as an index of the REITs has fallen by 6% in January this year alone!

What would Beansprout do?

- What happened in previous episodes of Fed interest rate hikes

While the Fed rate hike is the first that we have seen in a few years, and comes in a very unique environment which Senior Minister Tharman Shanmugaratnam has described as a “perfect long storm”, we can still look back at previous episodes of interest rate increases to see how REITs performed back then.

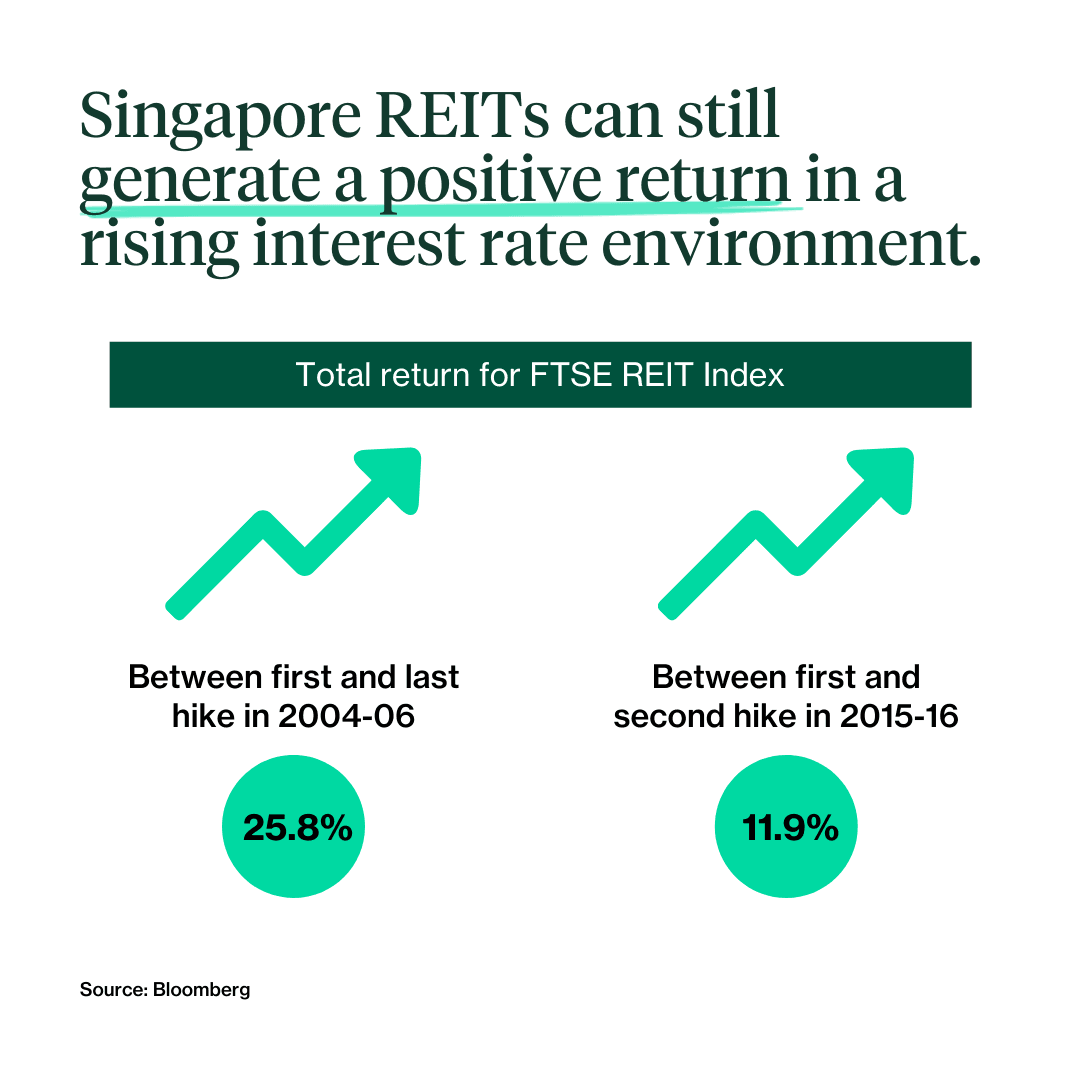

In the rate hike cycle in 2004, the FTSE REIT Index generated a total return of 25.8% between the first hike in June 2004 to the last hike in 2006.

In the 2015-18 rate hike cycle, the FTSE REIT index generated a total return of 11.9% between the first hike in December 2015 and the second hike in December 2016.

This would suggest that Singapore REITs can still generate a positive return in a rising interest rate environment.

Singapore REITs also offer a higher dividend yield compared to the Singapore market index measured by the STI. 2

- What to look out for in buying REITs

Given the environment we are in, we should be careful about which REITs we are holding on to. As we discussed in our framework of what to look out for in REITs in a rising interest rate environment, we would be looking out for the following in picking REITs:

a) Lowest gearing and higher proportion of debt fixed

b) Positive fundamentals to be able to drive higher rental reversions

c) Attractive dividend yield relative to the government bond yields

It might be worth looking through your portfolio to examine if the REITs you hold have the above characteristics to be able to withstand the higher interest rates.

To understand how we use this to screen for REITs, it might be worth checking out our article on 3 Singapore REITs to add to your watchlist.

This article was first published on 17 March 2022 .

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments