REITs

Digital Core REIT bounces sharply off lows. More upside ahead?

By Gerald Wong, CFA • 04 May 2024 • 0 min read

Digital Core REIT has been one of the best performing REITs in the past year. We find out if the REIT still looks attractive with a dividend yield of 5.9%.

In this article

What happened?

Some investors asked me about Digital Core REIT during our recent webinar on Singapore REITs.

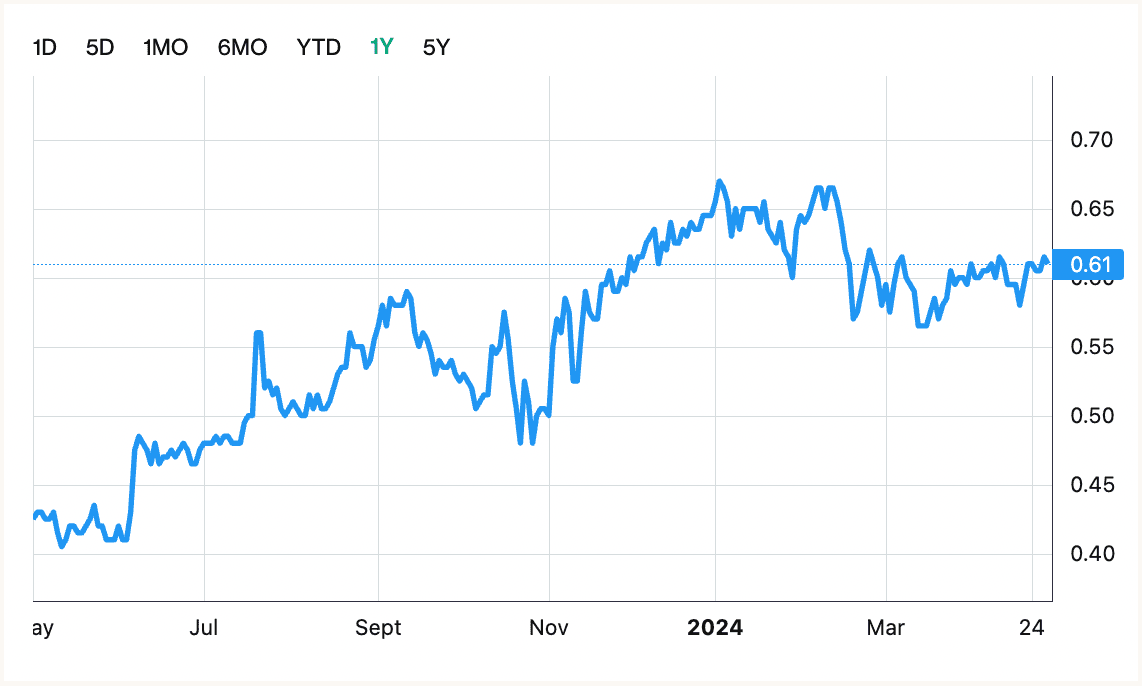

Digital Core REIT has been one of the best-performing REITs in the past year, with its share price rebounding from a low of US$0.37 to reach US$0.61 as of 30th April.

This is in contrast to another pure-play data centre REIT - Keppel DC REIT, which recently fell to reach a 1-year low after dividends were cut further.

Many investors were curious to find out how Digital Core REIT is performing after the data centre REIT reported that its second-largest tenant, Cyxtera Technologies, filed for bankruptcy.

Let us find out by looking at its recently announced its 2024 first quarter (1Q 2024) business update.

What you need to know about Digital Core REIT’s business update

#1 – Decline in net property income

Investors should note that Digital Core REIT only pays out distributions on a half-yearly basis.

The REIT does, however, provide its financial statements every quarter and we were encouraged to note that its financials were sturdy despite the lingering headwinds of high inflation and surging interest rates.

Revenue for 1Q 2024 fell by 8.2% year on year to US$24.6 million but property expenses dipped by just 5.7% year on year.

The result was Digital Core REIT’s net property income falling by 9.5% year on year to US$15.8 million.

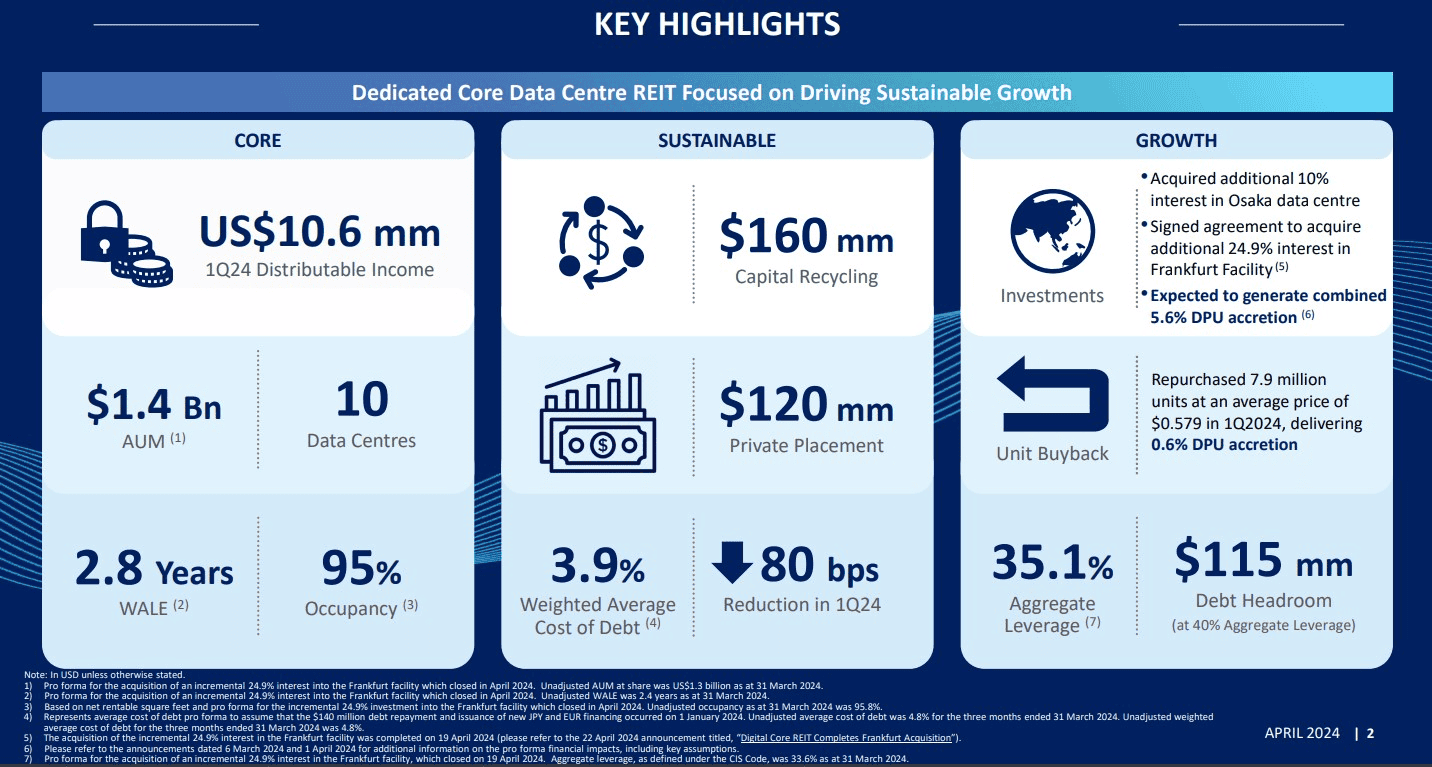

Adding back distribution adjustments, the REIT saw its distributable income slip by just 2.4% year on year to US$10.6 million (see below).

Digital Core REIT recently signed agreements to acquire a 10% interest in an Osaka data centre along with an additional 24.9% interest in a Frankfurt data centre.

These two transactions will generate a combined addition of 5.6% to distribution per unit (DPU).

Meanwhile, the REIT manager also initiated the purchase of 7.9 million units at an average price of US$0.579 in 1Q 2024 to deliver additional accretion of 0.6% to DPU.

#2 – Improved debt profile

Digital Core REIT’s manager has worked hard to improve the REIT’s debt profile and it’s showing in the numbers that the REIT disclosed.

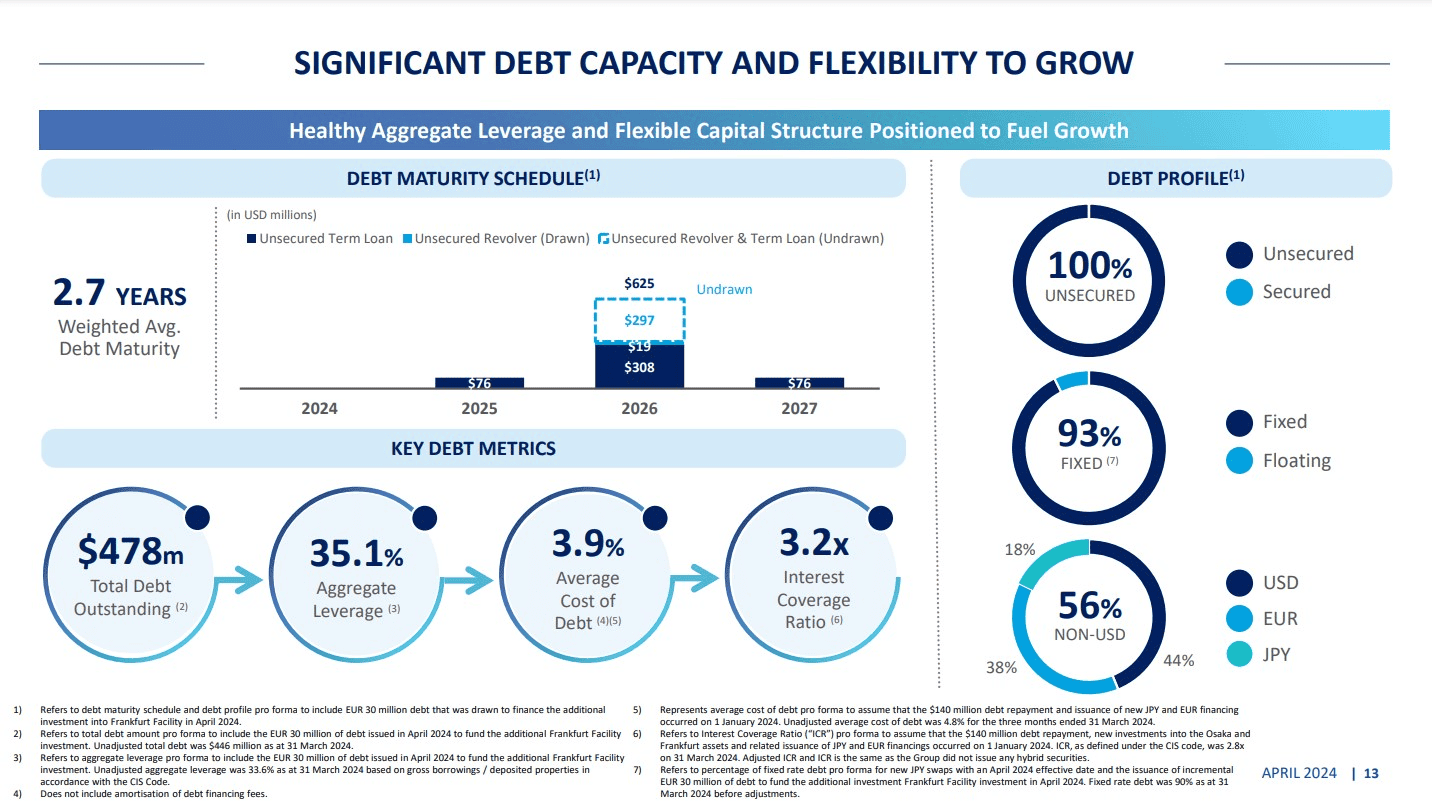

After the two acquisitions mentioned above along with Digital Core REIT’s asset sales and fundraising exercise, gearing stood at 35.1% for 1Q 2024, not far from the aggregate leverage of 33.5% as of 31 December 2023.

The REIT manager brought in Japanese bank Mizuho to arrange for a Japanese Yen-denominated term loan and to fix the rate for its four-year borrowings at just 1.5% per annum.

As a result of this action and the paying down of US$140 million of its US floating-rate debt at a 6.4% cost of debt, Digital Core REIT managed to lower its overall cost of debt to just 3.9% in 1Q 2024 from 4.7% at the end of 2023.

The interest coverage ratio has also gone up from 2.9x to 3.2x over the same period with 93% of the REIT’s debt pegged to fixed rates.

#3 – Customer concentration is still an issue

Back when Digital Core REIT proposed a series of transactions to resolve Cyxtera’s bankruptcy, one of the goals of the REIT manager was also to increase the regional diversification of the REIT and the number of customers it had.

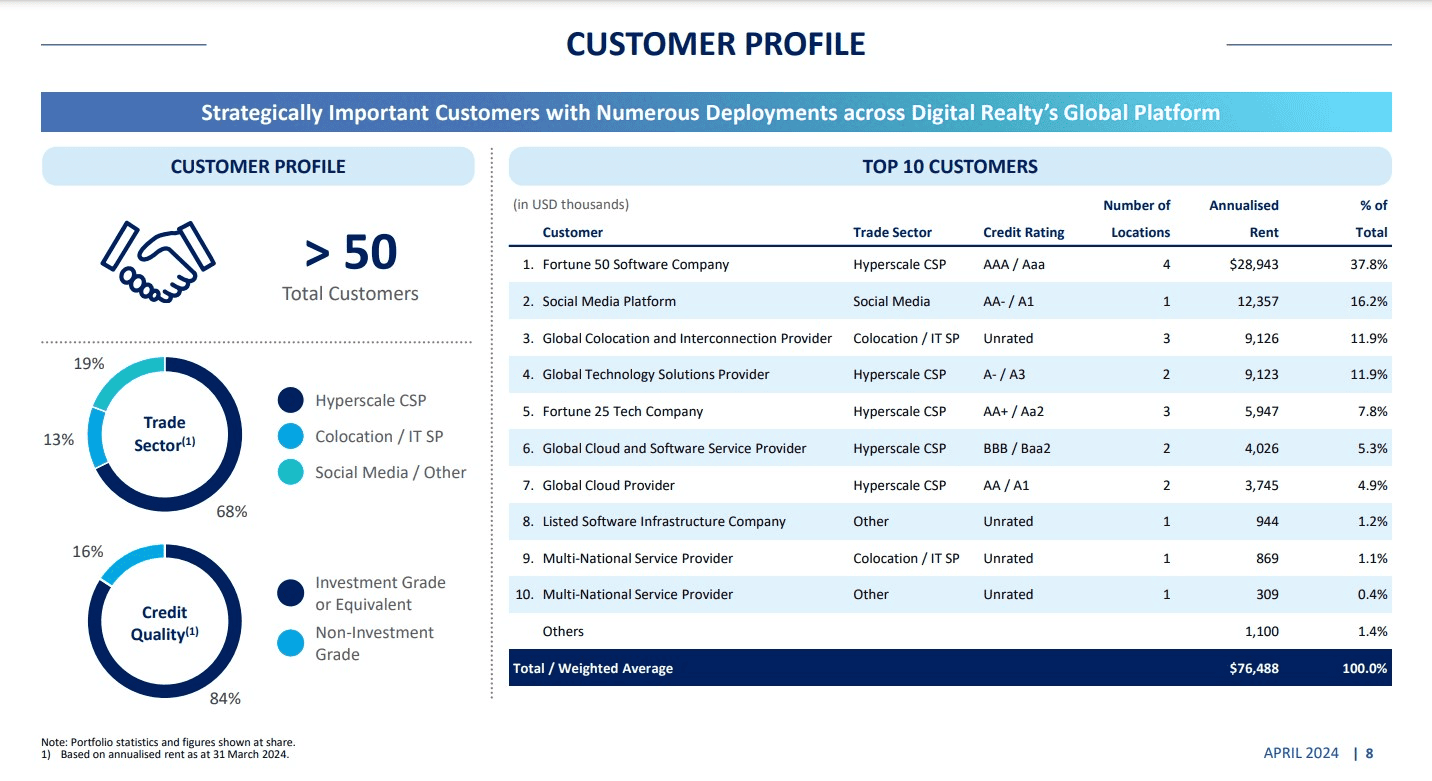

In November 2023, the REIT projected that the number of customers will increase from 26 to “more than 40”.

Fast forward to today, and Digital Core REIT now counts more than 50 customers as tenants within its portfolio of 10 data centres.

Around 84% of the portfolio belongs to investment-grade tenants and slightly more than two-thirds are from hyperscalers.

However, the problem of customer concentration remains with 37.8% of the REIT’s annualised rent coming from just one Fortune 500 software company.

Close to 65% of annualised rental income comes from the top three tenants.

Digital Core REIT could do better to diversify its exposure further to reduce reliance on these three customers, or it could face a similar situation to what happened with Cyxtera.

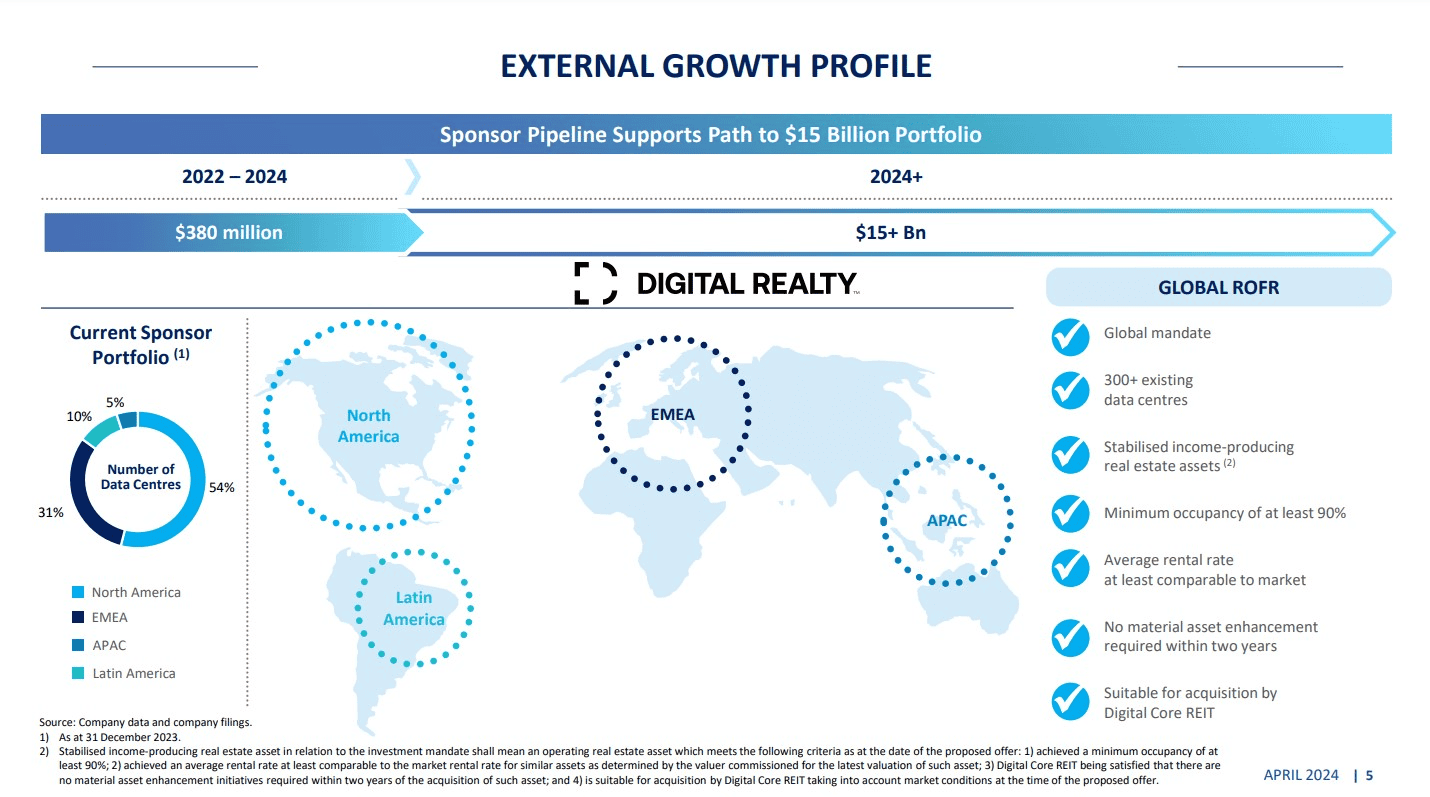

#4 – A healthy pipeline of assets

Digital Core REIT reiterated that its sponsor, Digital Realty Trust, supports the path to a US$15 billion portfolio as the latter has a healthy pipeline of assets that can be injected.

The value in a strong sponsor is apparent with DCR acquiring its additional stake in the Frankfurt facility at a 6% discount to its appraised value from its sponsor.

The slide above also shows that Digital Core REIT has a right of first refusal on approximately 300 data centres with a global mandate.

More than half of Digital Realty Trust’s portfolio of data centres are located in Latin America with another 31% in the Europe, Middle East and Africa (EMEA) region.

However, Digital Core REIT will only look for assets with a minimum occupancy of at least 90% with an average rental rate that is comparable to the market rate.

These properties should also be stabilised and be able to produce a dependable flow of rental income with no significant asset enhancements required within two years.

What would Beansprout do?

Digital Core REIT went through a turbulent period last year when news of Cyxtera’s bankruptcy broke.

Fortunately, the REIT manager went through a series of transactions that helped to stabilise the ship.

The data centre market fundamentals are still sturdy with digitalisation and artificial intelligence requiring massive amounts of data storage in the years to come.

Digital Core REIT currently offers a dividend yield of 5.9%, above Keppel DC REIT’s dividend yield of 5.3%.

Find out how much dividends you would have received as a shareholder of Digital Core REIT in the past 12 months with the calculator below.

However, we will be watchful of the decline in its net property income as well as significant exposure towards its top three customers.

If you are interested to learn about income opportunities in the Singapore market, join our upcoming webinar on 14 May 2024 to find out how you can identify these opportunities.

Join the Beansprout Telegram group to get the latest updates on Singapore REITs, stocks, bonds and ETFs.

Related links:

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments