REITs

Is CICT a safe REIT to hold into a potential recession?

By Beansprout • 25 Jun 2022 • 0 min read

We’d be watching out for CICT as a potential place to hide amidst rising market uncertainty.

In this article

TL;DR

- Sentiment towards CapitaLand Integrated Commercial Trust (CICT) has been improving with the recovery in CBD office rents and retail sales in Singapore.

- Tech companies have been taking up more prime office space. In the event of a slowdown in demand, rents may not fall sharply with limited new supply in the next few years.

- With 85% of its borrowing at fixed interest rates, CICT’s dividend payout is unlikely to be significantly impacted by higher interest rates.

- We’d be watching out for CICT as a potential place to hide amidst rising market uncertainty. CICT offers a dividend yield of 4.9%, above the average 10-year yield on the Singapore Savings Bonds of 2.7%.

What happened?

When we talk to others these days, a lot of the questions revolve around what’s a safe investment to hide in with rising risks of a recession.

It seems like we’re all stuck between a rock and a hard place.

Take too much risks with our investments, and we might end up with capital loss.

Hold our cash in a bank account, and its value might get eroded with sky-high inflation.

This might be why many are looking at REITs as a place to hide.

After all, it might appear quite attractive to be earning a dividend income while waiting for more clarity on how things will eventually pan out.

Hence, we thought it might be worth taking a deep dive into CapitaLand Integrated Commercial Trust (CICT), the OG of REITs in Singapore.

5 things you need to know about CICT

Currently, there is much to be positive about both office and retail rents in Singapore with the re-opening.

But what we really want to understand, is whether things will remain as rosy going forward if there is going to be an economic slowdown.

#1 - Demand for office space is recovering

If you have been in the Central Business District (CBD) recently, it wouldn’t be hard to notice that the buzz is back.

This comes as 100% of employees are allowed to return to the office from 26 April.

In fact, the average proportion of office community returning to Raffles Place properties in the week ended 20 May was at 59%, according to a Raffles Place Alliance spokesperson.

With an improvement in economic activity and work-from-home no longer the default, we have also seen more companies leasing space in Singapore’s CBD.

This would include companies in the technology and financial services sectors.

For example, it was reported that Bytedance, the parent company of TikTok, is in advanced negotiations to take up close to 120,000 square feet (sf) of office space at Capital Tower vacated by JP Morgan.

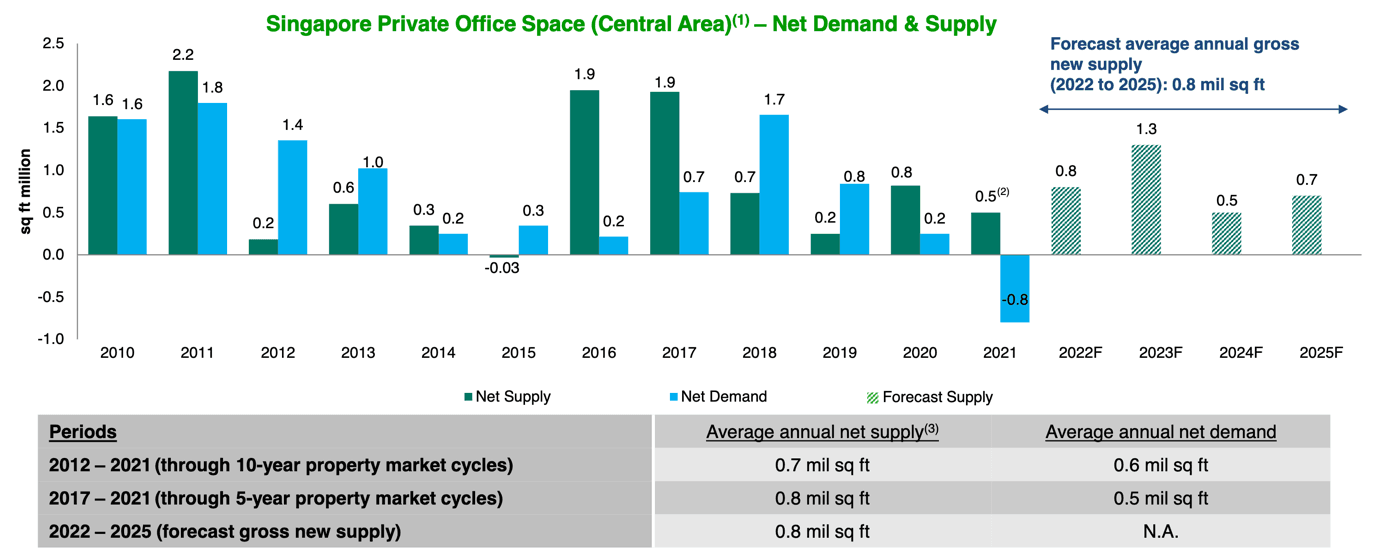

#2 – There isn’t much new upcoming supply of office space

While demand is recovering, there isn’t much new office space for companies to be choosing from.

The average annual increase in new supply in 2022-2025 is expected to be at 0.8 million square foot. This isn’t too different from what it was in the last 5 years and last 10 years.

Most of the increase is expected next year, with the completion of the IOI Central Boulevard Tower.

Once again, it seems like tech companies have taken an interest in taking up the office space, with Amazon and Meta Platforms reported to be in advanced negotiations to take up leases at IOI Central Boulevard Tower.

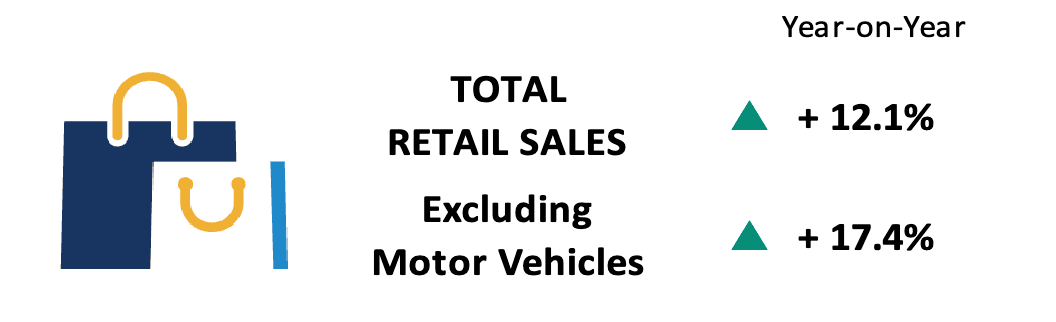

#3 – Increase in consumer spending helping to boost retail

Despite the growing concerns about an upcoming recession, it doesn’t seem to have hurt consumer spending too much as yet.

Retail sales excluding motor vehicles in Singapore rose 17.4% in April compared to the previous year.

Almost every retail sector saw an increase in sales. But this was more evident in the apparent and footwear industry, which grew by a whopping 46.6% YoY in April.

Clearly, the easing of border restrictions and higher tourist spending has helped to give the retail sector in Singapore a much needed boost.

The F&B sector also had much to cheer about, with a 11.4% growth compared to the previous year, as dine-in restrictions were relaxed.

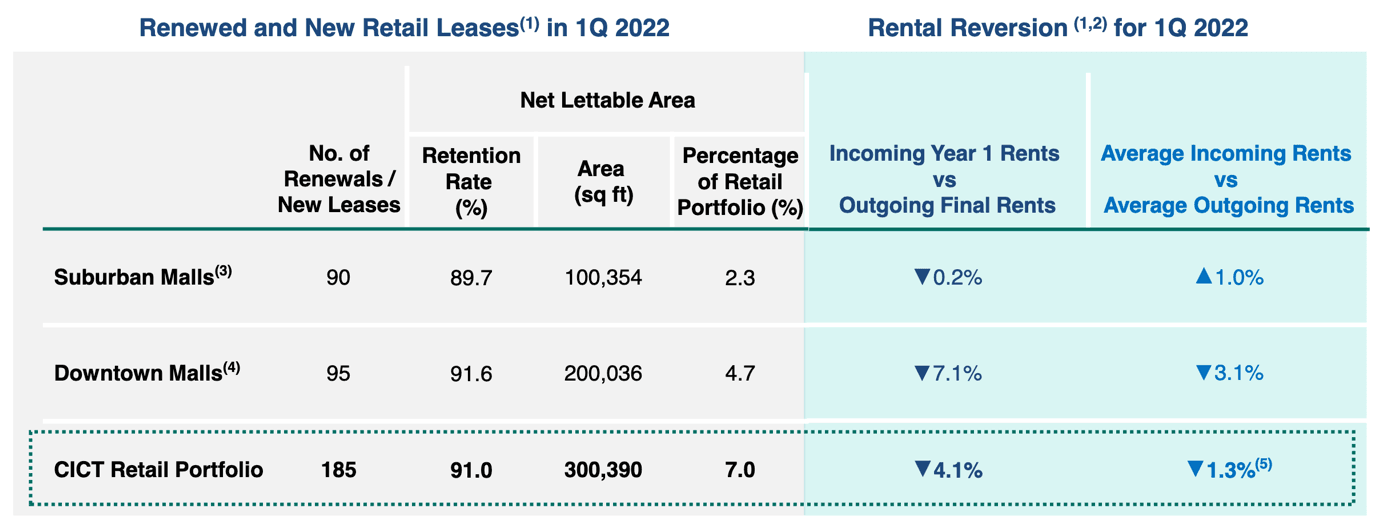

#4 – Recovery in retail rents more muted

Despite the improvement in retail sales, the rents that CICT is able to earn from its retail malls are still fairly weak.

This might be because retailers are taking a wait-and-see approach before deciding to take up new leases. Typically, it would take more than one year of sustained recovery before they would have the confidence to do so.

Hence, the average rents that CICT is able to earn for new retail leases it is signing is still lower than the average of the leases that are expiring.

Suburban malls have done slightly better, as the sales of its tenants in these malls have already recovered to pre-COVID levels.

Downtown malls have been where the rents have been weaker, with average rents of new leases about 3% lower than expiring leases.

Here, there might be a reason to be optimistic as its downtown malls such as Plaza Singapore, Raffles City, Bugis Junction and Funan could benefit from the increase in office crowd as well as tourists.

#5 - High proportion of borrowing on fixed interest rates

With the very aggressive rate hikes by the US Federal Reserve, there is naturally concern about how this will impact CICT.

CICT’s gearing (total debt over total assets) was at 39% as at March-2022. This would be put its debt levels at the middle of other retail and office REITs. The gearing is higher than SPH REIT (30%), but lower than Suntec REIT (43%).

The silver lining is that CICT has 85% of its borrowing on a fixed rate, which means that it would not have to incur much more interest costs in the near term as interest rates increase.

Based on management estimates, a 1% increase in interest rates would increase CICT’s interest expense by about S$12.9 million per year. This would reduce its Dividend Per Unit (DPU) by about 0.2 cents, or its dividend yield by about 0.1% (based on a share price of S$2.19).

What would Beansprout do?

#1 – Determine what the Fed is likely to do

It’s hard to make an investment today without first thinking about whether the US Federal Reserve will continue with its interest rate hikes.

The good news here is that with the signaling by the Fed, many investors are already expecting quite a few more rate hikes to be coming up.

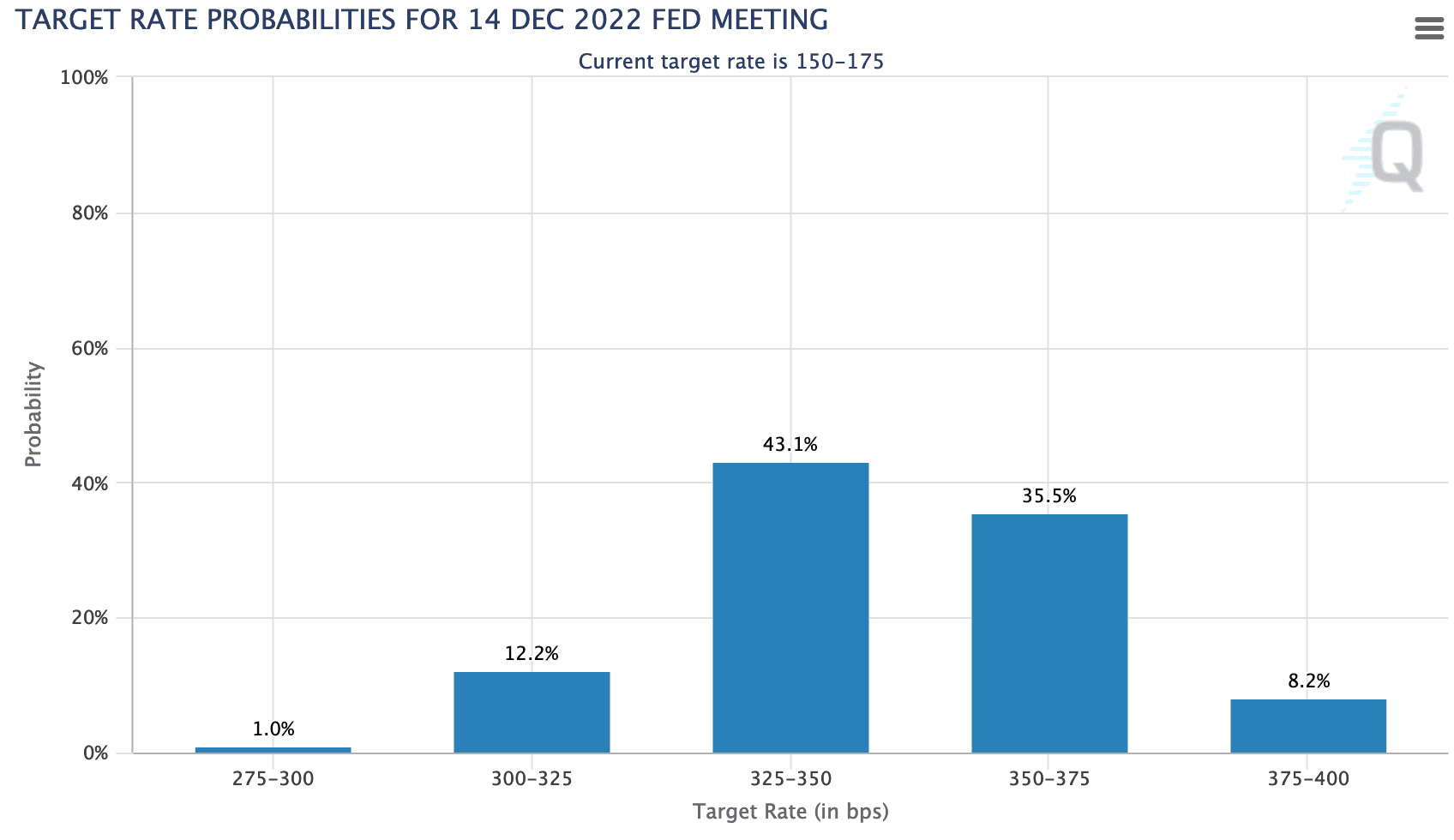

For example, the median FOMC member expects the Fed Fund rate to be 3.4% at the year end, implying another 165 bps increase in interest rates for the rest of the year.

Likewise, the CME Group has assigned a 43% probability to the event that the target rate would be at 3.25-3.5% in December this year. A 35% probability has been assigned to the event that the target rate would be 3.5-3.75% in December.

Of course, the key to watch here is inflation. If inflation remains persistently high, then the likelihood of further rate hikes would also increase.

#2 – Compare CICT's dividend yield to the SSB and SGS bonds

What draws many investors to CICT is probably its attractive dividend yield of about 4.9%.

This is still slightly higher than the average 10-year yield on the Singapore Savings Bonds.

It’s also higher than the yield on the 6-month Treasury bills of 2.36% in the most recent auction.

The question to me is whether the risks are worth taking for the higher yield on CICT. After all, while the SSB and SGS bonds have relatively low risks, CICT is not without its risks.

The comfort that we can take here is that even if there is a slowdown in office demand, there isn’t much supply that would drive down office rents sharply.

Also, while CICT has a modestly high gearing, the high proportion of borrowing on fixed rates will prevent interest costs from rising too sharply.

Another way to look at it – Would you be losing a lot of sleep should interest rates go up more than expected? And would the additional yield you are getting on CICT be worth it?

That will be litmus test on whether I’ll be holding CICT into a potential recession.

This article was first published on 25 June 2022 .

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments