Is the 1-year T-bill better than the 6-month T-bill and fixed deposits?

Bonds

By Gerald Wong, CFA • 20 Jul 2025

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

The closing yield on the 1-year Singapore T-bill of 1.76% is close to the 6-month T-bill yield. However, investors of the 1-year T-bill may face lower re-investment risks.

What happened?

The yield on the 6-month T-bill has fallen over the past few months.

The cut-off yield on the most recent 6-month T-bill (BS25114N) declined to 1.79% from 1.85% in the previous auction.

At the same time, fixed deposit rates in Singapore have declined in recent months too.

As such, I've seen fewer discussions in the Beansprout community about where is the best place to park cash for higher yields - T-bills, fixed deposits or SSBs?

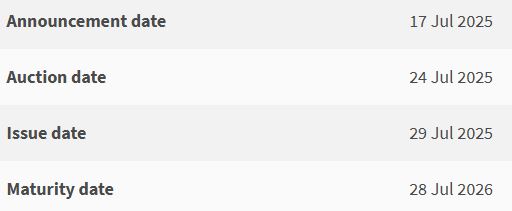

With an upcoming 1-year Singapore T-bill auction (BY25102X) on 24 July 2025, I will be looking at some of the latest indicators to find out if it is worthwhile applying for the 1-year Singapore T-bill as a way to generate passive income.

What is the likely yield on the 1-year Singapore T-bill?

The Singapore 10-year government bond yield has continued its downward trend in recent months. After briefly rebounding to around 2.74% in early 2025, it has since fallen sharply, dropping to below 2.0% in recent months.

This decline reflects growing market expectations of interest rate cuts by the US Federal Reserve, as well as strong demand for Singapore government bonds with its safe haven status amid economic uncertainty.

The 1-year Singapore T-bill has also followed the same downward momentum. The closing yield on the 1-year T-bill was 1.76% as of 18 July, based on MAS data.

This is well below the 2.29% cut-off yield seen in the April 1-year T-bill auction.

However, it is worth noting that the eventual cut-off yield in the auction may differ from the closing yield, as it will depend on the bids in the auction.

From the past few rounds of the 1-year T-bill auctions, we can see that demand for the T-bill has been fairly elevated.

This has put pressure on the cut-off yield of the 1-year T-bill.

Buying Singapore 1-year T-bill – better than 6-month T-bill?

Rather than applying for the 1-year T-bill, one option to consider is to invest in two consecutive tranches of 6-month T-bills.

Specifically, we could invest in the upcoming 6-month T-bill auction on 31 July 2025, and reinvest the funds again when the T-bill matures in February 2026.

If we apply for the next 6-month T-bill which will be issued on 5 August, the maturity date would be on 3 Feb 2026. We could then choose to reinvest based on the prevailing interest rates at that time.

However, there’s a risk that yields may fall further in the second half of the year — especially if the U.S. Federal Reserve begins rate cuts. In this scenario, locking in the 1-year T-bill now could offer better overall returns with less reinvestment uncertainty.

While the current closing yield of 1.76% on the 1-year Singapore T-bill is close to the cut-off yield of 1.79% in the most recent 6-month T-bill auction, I will ask myself if I would want to lock in the rate now for 12 months, or take on reinvestment risk with the 6-month T-bill if yields drop significantly by February 2026.

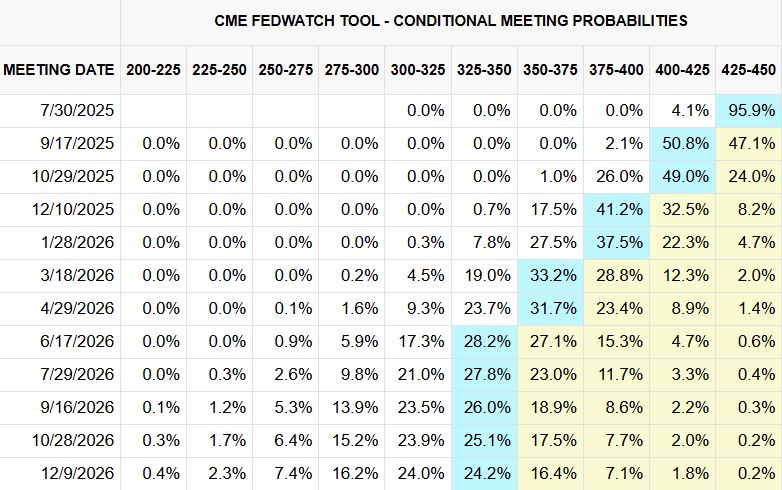

According to the latest US interest rate expectations, markets now expect the first U.S. interest rate cut to happen in September 2025, with over 50% chance of rates being lowered to the 400–425 bps range.

Further cuts are also expected by the end of the year, pointing to lower interest rates in the coming months.

This means that we may get a potentially lower yield on the 6-month T-bill, when we are re-investing the proceeds from the first 6-month T-bill.

However, with significant economic uncertainty with the tariffs announced, we will have to keep a close watch on interest rate trends.

For example, if the tariffs announced lead to a spike in inflation in the US, the Fed may have to raise interest rates rather than cut interest rates as expected currently.

Buying Singapore 1-year T-bill using CPF – Is it worth it?

We shared earlier that due to the loss of CPF interest, it is generally more worthwhile to use your CPF funds to invest in the T-bill when the bond has a longer maturity.

For example, the breakeven cut-off yield for T-bill applications using CPF OA falls to about 2.7% for a 1-year T-bill from 2.9% for a 6-month T-bill, assuming the loss of one additional month of CPF interest.

However, with the closing yield on the 1-year T-bill now at 1.76%, it is below the breakeven yield for T-bill applications using CPF OA.

Buying 1-year T-bill using cash – better than fixed deposit?

Most Singapore banks have lowered their fixed deposit rates in January. Currently, the best 1-year fixed deposit rate we found is at 2.45% p.a.

However, we can only earn the fixed deposit rate of 2.45% for deposits of below S$20,000.

For larger deposit amounts, the best 1-year fixed deposit rate is at 1.65% p.a.

This would then be lower than the latest closing yield of 1.76% on the 1-year T-bill

Buying 1-year T-bill – better than Singapore Savings Bonds?

The current issuance of the Singapore Savings Bonds (SSB) offer a 1-year return of 1.82%.

This is close to the current closing yield on the 1-year Singapore T-bill.

Apart from offering a 1-year return of 1.82%, the latest SSB also allows us to lock-in a rate of 2.29% over 10 years, while having the flexibility to redeem prior to maturity.

What would Beansprout do?

The current closing yield of the 1-year Singapore T-bill is 1.76%, which is close to the recent 6-month T-bill cut-off yield of 1.79%.

However, it might still be worthwhile considering the 1-year T-bill over the 6-month T-bill to avoid the uncertainty of reinvesting six months later, especially if significant rate cuts were to come through in the coming months.

If you are looking to park an amount below S$20,000, the 1-year T-bill yield is significantly lower to the best 1-year fixed deposit rate, which is currently at 2.45%

However, for an amount of S$20,000 and above, the best 1-year fixed deposit rate of 1.65% p.a. would be below the closing yield of the 1-year Singapore T-bill.

One of the ways to secure a potentially higher yield is to consider the Singapore Savings Bonds (SSB), which offers a 1-year return of 1.82% and average annual return of 2.29% over 10 years, while having the flexibility to redeem prior to maturity.

To explore these alternative places to park your cash, check out our comparison of T-bills, fixed deposits and SSBs to find the best place to park your cash.

Earlier, we also shared a few other ways to generate passive income in Singapore, including endowment plans which may offer a guaranteed return.

The 1-year Singapore T-bill auction will be held on Thursday 24 July 2025.

As cash applications for the T-bill close one business day before the auction date, we would need to put in our cash applications for the T-bill by 9pm on 23 July (Wednesday).

Applications for the T-bill using CPF-OA will close 1-2 business days before the auction date, and the dates differ across the three local banks.

Applications for T-bills online using CPF OA via DBS close at 9pm on 23 July (Wednesday). Read our step-by-step guide to applying via DBS.

Application for T-bills online using CPF OA via OCBC close at 9pm on 23 July (Wednesday). Read our step-by-step guide to applying via OCBC

Applications for T-bills online using CPF OA via UOB close at 9pm on 22 July (Tuesday) Read our step-by-step guide to applying via UOB.

To learn more about T-bills and find out how to apply, check out our Comprehensive Guide to T-bills.

Join the Beansprout Telegram group get the latest insights on Singapore bonds, stocks, REITs, and ETFs.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

1 comments

- Colin • 21 Jul 2025 12:21 AM