Financially free at 36, she’s now designing life for her own definition of success: Money Diaries #7

Retirement

By Julian Wong • 18 Jul 2025

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We speak to a design leader on how she is approaching life and her investment portfolio post-FIRE.

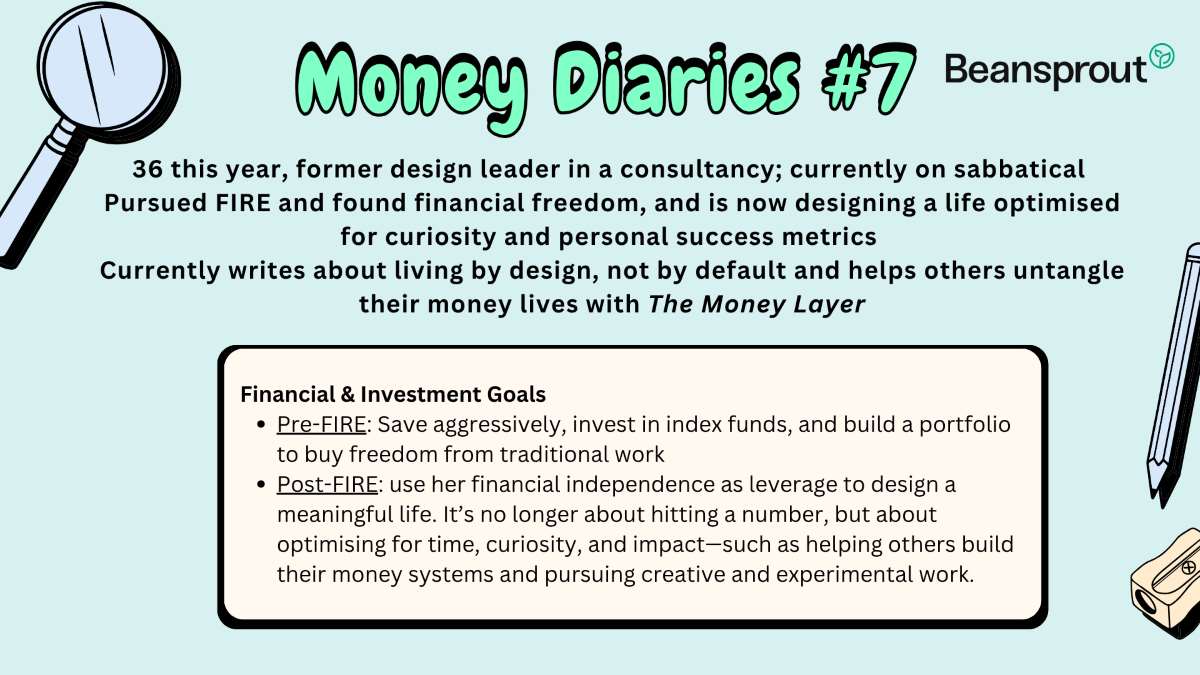

In this week’s Money Diaries, we speak to Jalyn Cai. Jalyn is 36 this year, and was formerly part of the design leadership team in a consultancy. Currently, she is on sabbatical—in what she describes as her ‘post-job era’—and still figuring out how to best describe the life stage she is in. She doesn’t draw a salary, and is fact drawing down on her existing portfolio.

Jalyn also writes about living by design, not by default at By Design, breaks it down into systems with The Full Stack, and helps others untangle their money lives with The Money Layer.

Money Diaries #7: Financially free at 36, she’s now designing life for her own definition of success

How would you describe the life stage you are in at the moment?

The RE stage of FIRE, after 15 years in the corporate world, though “retire” still makes me cringe (it conjures images of golf clubs and early dinners, and here I’m just trying to figure out what to eat for breakfast).

I’m treating this chapter as an experiment in what happens when you stop optimizing for performance reviews, and start treating your own life as your most important product.

Financial independence gave me the runway — now I’m designing the thing I’m calling my full stack life.

Living situation:

I live with my family — I cover the bills, maintenance, and contribute to my parents’ expenses. It’s about equivalent to renting my own place, but this arrangement helped accelerate my FI timeline while making sure they’re financially secure too.

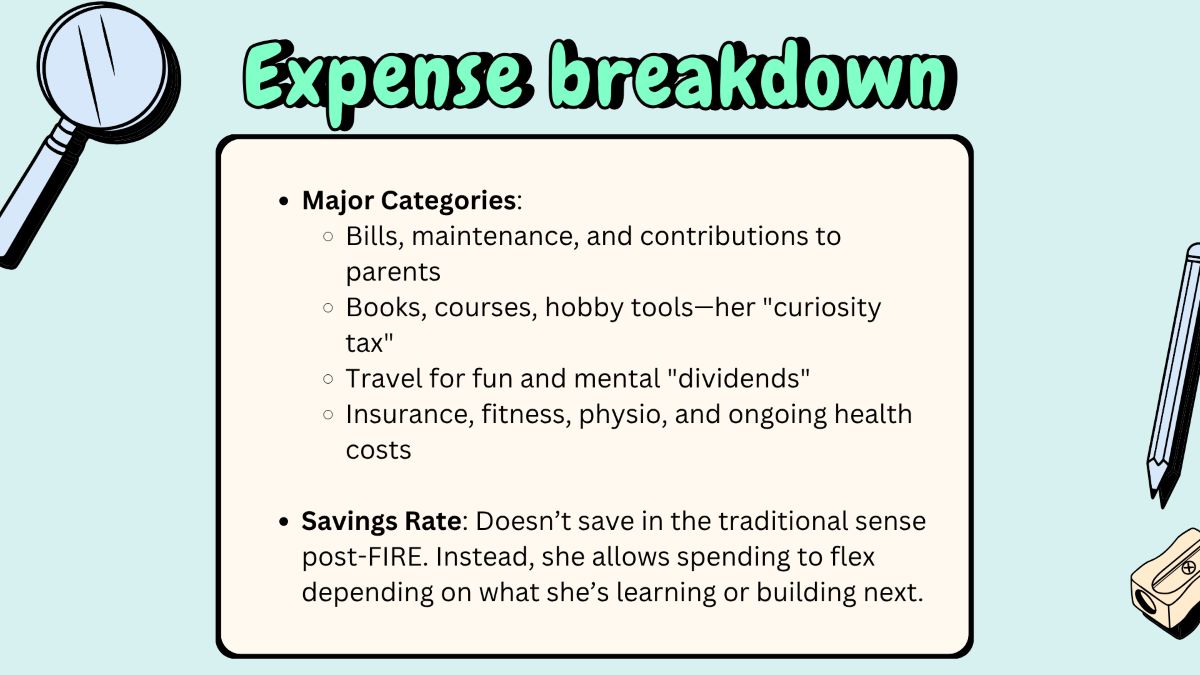

Breakdown of typical weekly expenses: A few years ago, this would’ve looked very different — I tracked every cent, said no to lattes, and treated fun spending like a failing.

These days, my portfolio covers the baseline. I let future experiments (writing, consulting, small projects) earn the fun. Here’s the rough breakdown, averaged weekly:

Baseline

Family/housing: $575 Bills, maintenance, and contributions to my family’s expenses

Food: $120/week The ratio shifts between groceries and dining out, plus snacks!

Medical/Health: $80/week Insurance, fitness, physio, and whatever health issues are plaguing me that week

Transport: $25/week Public transport most of the time, with the occasional Grab for late nights

Subscriptions: $35/week Your usual suspects: Streaming, storage, that green owl threatening when I lose my Duolingo streak, and a few health/fitness apps to keep me honest

Fun (and variable)

Vacations: Not an every week thing, but enough to cover fun stuff like skiing, diving, and generating mental dividends in new places

Growth and experiments: Courses, books, new hobby attempts, tools — what I call the curiosity tax that comes with having time again

Giving: Ad-hoc support, spontaneous treats, and contributing where it feels meaningful

Estimate of how much you save every month:

In accumulation mode, I saved ~60% of my take-home salary for the past five years.

These days, I don’t “save” in the traditional sense, but I also don’t aim to spend to the last cent. I let my spending flex based on what I want to learn or build next.

What are your financial/investment goals:

When I first found FIRE in 2018, the goal was clear: buy my freedom. Save as much as I can, invest in boring index funds, and build a portfolio that could support me without a job.

Now, the goal has shifted. It stopped being about hitting a number, and started being about what that number could unlock.

I want to use what I’ve built as leverage — not just for comfort, but to create something useful. I’m helping friends build their own money systems, and designing a life where choice comes from curiosity, not obligation.

How close/far would you say you are from your financial goals?

Financially? I overshot the target without realising it.

I’d always ignored CPF, SRS, and anything I couldn’t touch immediately. In my head, if it wasn’t liquid, it didn’t count. So when I left my job, I still thought I was four years away.

Turns out I was already over the line — I just hadn’t done the full calculation.

I was spiraling over whether my bubble tea consumption is getting out of hand (60 cups in the first half of 2025, so maybe not ruinous financially, but definitely on thin ice nutritionally 😅), while technically being financially independent for months.

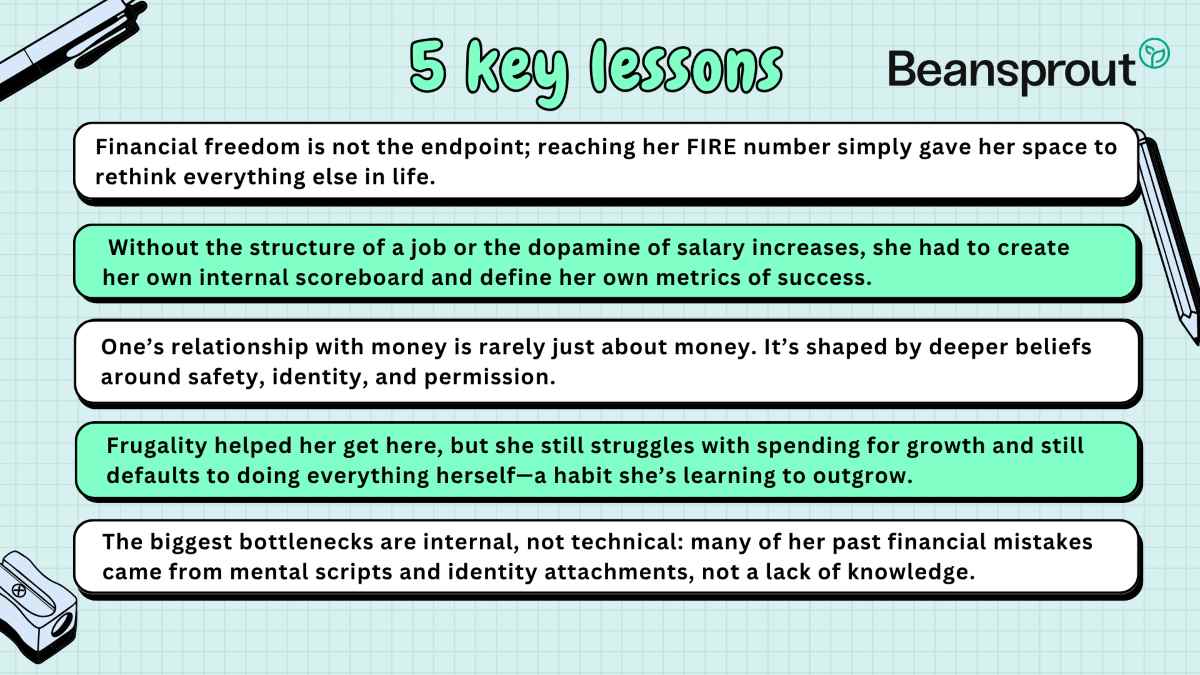

So yes, the money goal’s been hit. But the real one — designing my full stack life, and helping others do it too — is a work in progress. The money bought me time, and now I’m learning how to spend it on the right things.

Describe your investment approach:

I started from zero liquid assets in 2017, and got here through a boringly systematic approach:

- Broad-based ETFs via Interactive Brokers (SWRD + EIMI split; I like managing my allocation instead of defaulting to VWRA)

- A sprinkling of the STI ETF for local exposure

- A few blue chip stocks, just for fun (and mild regret, considering their performance)

I didn’t dabble in crypto or meme stocks, and while it’s caused me FOMO over not having massive gains, I’ve realized that my own system of consistency over intensity makes me feel better as an investor.

I also maxed out my SRS annually. My CPF OA is invested through Endowus too, and both have long horizons in the same world index fund, so I treat them like very slow-cooking rice cookers.

What are some challenges you've faced?

Learning how to shift from building, to being.

In accumulation mode, everything made sense: save, invest, repeat. There’s a dopamine hit to seeing numbers go up. Post-FI, the feedback loop is quieter — there’s no “level up” moment, no annual bonus, and no scoreboard.

You have to define your own metrics of success, and that’s harder than it sounds.

How would you describe your mindset with regards to money?

It's complicated.

On paper, I have a healthy relationship with money. I understand it's a tool, I have a good runway, and I've built margin for optionality — all the things you're supposed to say.

But I’ve also spent an hour researching a $50 purchase, and gone five rounds with myself about whether I deserve the nice version of something.

The weirdest part is realizing that I optimized my way to financial freedom, while knowing that actually being free is something I’m still learning.

Is there an experience that shaped your relationship with money?

Finding FIRE was the first shift — realising that you could save aggressively, invest systematically, and eventually buy your time back. It reframed money from a source of stress into something you could design around.

But the deeper shift came later: realising that money was just one layer.

I’d optimised my finances while letting everything else run on autopilot — my health, relationships, sense of meaning. I thought freedom would feel like arrival, but it just exposed how under-built the rest of my life was.

Money didn’t fix those things. But it gave me the space to finally see them — and the breathing room to start rebuilding from the inside out.

What is one money habit you struggle with the most?

Spending-for-growth.

I’ll drop money into investments with no problem, but hesitate to pay for tools or services that would save me time and mental load.

I still catch myself DIY-ing things I have no business doing. Frugality got me here, but it’s not what will take me forward.

Is there a financial decision you wish you could do over?

Most of the “mistakes” weren’t about money — they were lapses in thinking.

Starting to invest earlier wasn’t about not knowing index funds existed; it was about not having the framework to see money as a design tool, rather than something that just happened to me.

Not job-hopping for better pay wasn’t about ignorance; it was because I’d tied my identity to being the “good employee”, so making strategic moves felt like betrayal.

Even the mental accounting error that delayed my FI realization by months wasn’t a math issue. It was me following arbitrary rules about what “counts”, without questioning where those rules came from.

The financial mechanics were never the bottleneck. The bottleneck was the operating system underneath — all the default scripts about work, money, identity, and risk that I’d never thought to examine.

That’s why I believe now: the real work isn’t just optimizing your portfolio. It’s upgrading the frameworks that drive how you think in the first place.

What are you most concerned about when it comes to personal finances?

That I’ll forget what the money was for.

It’s tempting to keep optimizing forever — tweaking allocations, chasing efficiency, running Monte Carlo simulations, holding back “just in case”… but I didn’t do all this to optimise spreadsheets. I did it to build something meaningful, and I don’t want to miss out on actually living.

If you won S$1m tomorrow, what would you do?

Probably the same thing I'm doing now, just with even less background anxiety.

I might upgrade a few conveniences, but the fundamentals wouldn’t change. The real luxury is space to design your life fully on your own terms, and I already have a degree of that.

What is one practical financial tip that has been useful?

Automate everything you can — investments, bills, even transfers to fun money accounts.

Most financial stress comes from needing to make the same decisions over and over. Systems > willpower.

What is a lesson you've learned that others might benefit from?

Your relationship with money is rarely about the actual money.

It’s about safety, control, permission, and identity. Track your numbers (yes, please) but if you’re still telling yourself the same old stories about yourself, you’ll just be a different kind of stuck.

Hitting my number didn’t free me from decisions — it freed me to finally make them on purpose.

Key Lessons

Want to share your financial journey? Reach out to us to be featured in our Money Diaries series!

Join our Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

1 comments

- Wei • 20 Jul 2025 06:03 AM