T-bill yields are falling. Time to look at Singapore REITs?

REITs

By Gerald Wong, CFA • 05 Apr 2025

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Falling T-bill yields and rising concerns of a global recession have led to renewed interest in Singapore REITs. We find out if they are a safe place to ride out market volatility.

Interest rates have fallen sharply in the past few weeks.

Recently, we saw the 6-month Singapore T-bill fall to 2.56%. The best 6-month fixed deposit rate in Singapore has also declined to 2.5%.

Not surprisingly, the interest rates on the UOB One and OCBC 360 accounts have also been cut.

At the same time, we have seen rising economic uncertainty following the sweeping tariffs announced by US President Donald Trump.

As a result, I have seen more discussion on Singapore REITs in the Beansprout telegram community.

Many investors are wondering if Singapore REITs will benefit from falling interest rates, and if they are a safe place to ride out the current market volatility. After all, some of these REITs appear to offer fairly attractive dividend yields.

Let us dive deeper to find out.

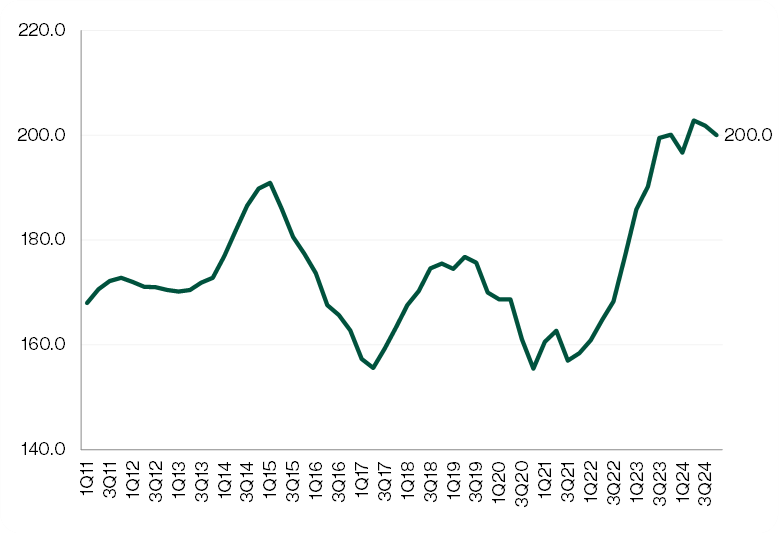

Singapore government bond yields have fallen

With rising concerns of potential global recession following sweeping tariffs announced by the US, the 10-year Singapore government bond yield has fallen to 2.47% on 4 April 2025 from 2.92% on 1 January 2025.

However, a divergence in outlooks across sub-sectors, strength of the Singapore dollar relative to regional currencies, and elevated borrowing costs may continue to put pressure on their distributions.

In 2024, distributable income growth of Singapore REITs continues to be tempered by higher finance costs, even in spite of revenue growth, as the majority of the REITS have more than 60% of debt on fixed rates. The effect of rate cuts in 2024 are thus likely to only begin to materialise over the next 12 months.

In the meantime, there is a divergence in the outlook across various REIT subsectors, as reflected in the most recent 4Q24 data.

Office rents continue to moderate

Vacancy rates for Category 1 offices saw a surprise decline by 1.2 percentage points to 9.1% as at 4Q24.

Category 1 offices are office space in buildings located in core business areas in Downtown Core and Orchard Planning Area which are relatively modern or recently refurbished, command relatively high rentals and have large floor plate size and gross floor area.

Category 2 offices, which refer to the remainder of the office stock, however, saw vacancy rates remaining elevated at 11.3%.

This suggests a continued flight to quality in a tenants’ market, amid significant new additions to Grade A CBD office supply, with IOI Central Boulevard Towers adding a total of 1.26 million sq ft of premium Grade-A office space and 30,000 sq ft of retail and F&B space in 2024.

Amid heightened net supply, particularly in the CBD area, office rents continue to be muted, with the URA office rental index down 0.9% QoQ in 4Q24.

| Office rental index fell by 0.9% QoQ in 4Q24 |

|

Rising operating costs against a cautious macroeconomic and hiring outlook are expected to keep overall office rents subdued, especially given elevated market vacancy rates and sizable new supply.

In 2025, Keppel South Central is expected to add 613,500 sq ft of CBD office space, while the completion of the Shaw Tower redevelopment and Solitaire on Cecil in 2026 are expected to add a further 631,500 sq ft of office space in the CBD.

Retail rents stable

Over the last four quarters, retail vacancy rates have remained largely steady, with outside Central Area and within the Central Area but Outside Orchard vacancy rates at 5.9% and 6.8% respectively.

Orchard vacancy rates continued to decline in 4Q24, down 0.7pp QoQ to 6.3%, and more than halving from close to 14% as at 1Q23, likely reflecting rising retailers’ confidence in a continued recovery in visitor arrivals into Singapore, led by both leisure travellers and MICE (Meetings, Incentives, Conferences, and Exhibitions) events.

Singapore’s tourism arrivals increased by 21% to 16.5 million in 2024, reaching the upper end of the Singapore Tourism Board (STB)’s forecast. STB expects a further improvement in tourist arrivals to 17.0 to 18.5 million in 2025.

As a result, the URA retail rental index has been stable, rising 0.6% QoQ in 4Q24. With below-historical-average supply over the next few years, property consultancy CBRE expects overall prime retail rents to recover to pre-pandemic levels in 2025.

| Retail rents have remained stable |

|

Industrial rent growth slowest since 4Q21

Overall industrial rents were up marginally in 4Q24, led by Multiple-User Factories with a strong 3.1% QoQ growth, followed by Warehouses at 0.9% QoQ, Business Park at 0.2% QoQ and Single-User Factories at 0.1% QoQ.

It was a year of healthy 3.5% rental growth for industrial properties for the full year 2024, albeit a moderation from the 8.9% increase seen in 2023.

| Industrial rent growth has slowed down |

|

While vacancy rates at Business Parks saw a surprise dip in 3Q24, this was reversed in 4Q24, with vacancy rates up 0.9pp to 22.1%, as vacancy rates continued to inch towards the high of 25.1% seen in 2010.

For the full year, vacancy rates across other industrial subsectors were mixed but broadly stable: Multiple-User Factories improving 0.5pp YoY to 9.0%, Single-User Factories saw vacancies flat YoY at 12.0% while Warehouses saw vacancies up a modest 0.1pp YoY to 8.5%.

An additional 1.2 mn sqm of industrial space is expected to be completed in 2025, with a further 1.1 mn sqm of space to be completed in 2026, totalling a significant 2.3 mn sqm of industrial space over the next two years.

In contrast, average annual supply of industrial space was 0.9 mn sqm in the past three years, with average annual demand of only 0.6 mn sqm.

While the total expected completion over the next two years includes 0.9 mn sqm of single-user factory space, which is typically developed by the industrialists for their own use, the significant supply pipeline of industrial space across warehouses, multiple-user factories and business parks are expected to add pressure to rents and vacancies in the near term.

Business parks in particular are expected to see the greatest pressure, given muted new demand and the consolidation of space requirements by companies looking to optimise their real estate footprint, amid a flight to quality and supported by a continued pipeline of new CBD office space and elevated vacancy rates.

Singapore REITs’ distributions remain under pressure

The majority of Singapore REITs continued to see a decline in their distribution per unit in the most recent earnings announcement.

The most significant decline in distributions were seen in REITs with significant overseas assets and were impacted by currency weakness relative to the Singapore dollar, as well as those which saw significantly higher borrowing costs.

On the other hand, REITs in the industrial and retail sub-sectors, particularly those with a sizeable portion of their assets in Singapore, had relatively resilient distributions compared to other REITs.

| Change in distribution per unit (in %) of Singapore REITs |

|

What would Beansprout do?

Despite falling bond yields, we remain selective as we expect the distributions of REITs with weaker fundamentals to remain under pressure with the mixed outlook across various sub-sectors.

Our preference is for REITs with the ability to improve on distributions including AIMS APAC REIT, OUE REIT, and Elite UK REIT.

Find the best Singapore REITs and compare their latest valuation with our Singapore REITs Screener.

| Price to book valuation of Singapore REITs |

|

If you are interested to learn more about the outlook of Singapore REITs, join us for our upcoming free webinar on 16 April, where we will discuss if the share prices of Singapore REITs will recover with falling bond yields. Register for free here.

Download the full report here.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments