UOB One vs OCBC 360: Which savings account pays more interest in 2026

Savings

By Nicole Ng • 05 Aug 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

The UOB One and OCBC 360 accounts offer attractive interest rates to make your savings work harder. We find out which is the best savings account in Singapore.

What happened?

High-yield savings account rates in Singapore have shifted again.

OCBC has temporarily raised the Save bonus interest rate on its OCBC 360 Account from 1 August to 31 December 2026. This brings the effective interest rate to 2.20% p.a. on S$100,000 if I meet the Salary, Save and Spend requirements.

Meanwhile, the UOB One Account continues to offer an effective interest rate of up to 1.90% p.a. on S$150,000 when I credit my salary and spend on an eligible UOB card.

For a broader comparison, I have also looked at the best savings accounts in Singapore.

UOB One and OCBC 360 remain two popular options, but the account that pays more depends on how much savings I have and which requirements I can meet.

In this article, I compare both accounts head to head to find out which one could help me earn more interest on my savings.

UOB One vs OCBC 360 at a glance

Both UOB One and OCBC 360 allow me to earn more interest when I credit my salary and spend on an eligible credit card.

However, they reward me differently.

UOB One offers bonus interest on a larger balance of up to S$150,000 and does not require me to grow my savings every month.

OCBC 360 offers a higher effective interest rate on the first S$100,000 during its Save bonus promotion, but I need to increase my average daily balance by at least S$500 each month.

| UOB One Account | OCBC 360 Account | |

|---|---|---|

| Minimum salary credit | S$1,600 per month | S$1,800 per month |

| Minimum card spending | S$500 per month | S$500 per month |

| Monthly savings requirement | None | Increase average daily balance by at least S$500 |

| Balance earning main bonus interest | First S$150,000 | First S$100,000 |

| Highest EIR without insurance or investments | 1.90% p.a. on S$150,000 | 2.20% p.a. on S$100,000 during the promotion |

| Promotion period | Not applicable | 1 August to 31 December 2026 |

The main trade-off is therefore between the higher promotional rate offered by OCBC 360 and the larger bonus interest balance and simpler requirements offered by UOB One.

What you need to know about UOB One Savings Account

The UOB One Account lets me earn tiered interest of up to 3.40% p.a. when I meet two requirements:

- Spend at least S$500 monthly on eligible UOB credit or debit cards.

- Credit your salary via GIRO of at least S$1,600, or make at least three GIRO transactions per month.

Unlike some other high-yield accounts, there’s no need to buy insurance or investment products to unlock the highest interest rate tier.

All you have to do is spend a minimum of $500 monthly on eligible UOB credit/debit cards and credit your salary via GIRO or make 3 GIRO transactions a month.

For young working adults and anyone who doesn't want to complicate things too much, these requirements are easy to meet.

If you’re already using a UOB card for daily spending and crediting your salary, you’ll find it easy to qualify for the higher interest tiers.

If you can’t credit your salary into your UOB One account, the good news is, setting up three recurring GIRO debits is a straightforward alternative to still enjoy higher interest rates.

A GIRO debit transaction is an automatic deduction made directly from your UOB One account to pay a billing organisation such as utilities, telco bills, or insurance premiums.

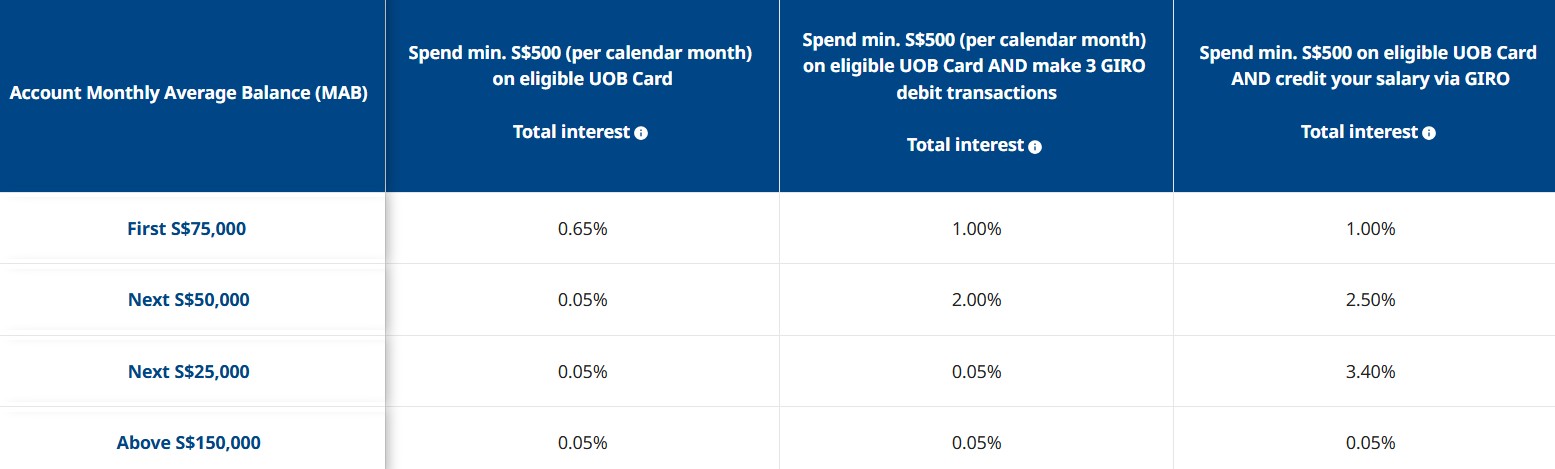

To understand how the interest rate on the UOB One account works, let's look at the breakdown below.

As you can see from the table, simply spending S$500 on your UOB card each month will earn you 0.65% p.a. interest on your first S$75,000.

If you make three GIRO transactions on top of your card spend, your rate increases to between 1.0% p.a. and 2.0% p.a., depending on your account balance.

To unlock the highest rates, you’ll need to credit your salary via GIRO on top of your card spend.

We illustrate the interest rate earned below on the UOB One account if you are able to credit your salary via GIRO.

| Account monthly average balance | Interest earned when you spend minimum S$500 on eligible UOB card and credit salary via GIRO, FAST or PayNow (p.a.) |

| First S$75,000 | 1.00% |

| Next S$50,000 | 2.50% |

| Next S$25,000 | 3.40% |

| Above S$150,000 | 0.05% |

| Source: UOB, as of 5 August 2026 | |

This allows you to earn up to 1.00% p.a. on your first S$75,000, 2.50% p.a. on the next S$50,000, and 3.40% p.a. on the final S$25,000, before the rate resets to 0.05% p.a. above S$150,000.

Note that the interest rates are tiered, meaning they apply only to portions of your balance rather than your entire deposit.

For example, if you have S$80,000 in your account, the first S$75,000 will earn 1.00% p.a., while the next S$5,000 (from S$75,000 to S$80,000) will earn 2.50% p.a.

The higher rate does not apply to your full balance, only to the portion within that tier.

To understand your actual returns, it’s useful to calculate the effective interest rate (EIR), which combines the total interest earned across all tiers to show the average rate on your overall balance.

| Total Balances | Effective interest rate earned when you spend minimum $500 on eligible UOB card and credit salary via GIRO, FAST or PayNow (p.a) |

| S$50,000 | 1.00% |

| S$75,000 | 1.00% |

| S$100,000 | 1.38% |

| S$125,000 | 1.60% |

| S$150,000 | 1.90% |

| Source: UOB, Beansprout Compare Savings Accounts tool, as of 5 August 2026 | |

As you can see when worked out as a whole based on the interest earned on the balances, the highest effective interest rate works out to 1.90% p.a. if you have a balance of S$150,000.

Read our detailed review of the UOB One account here.

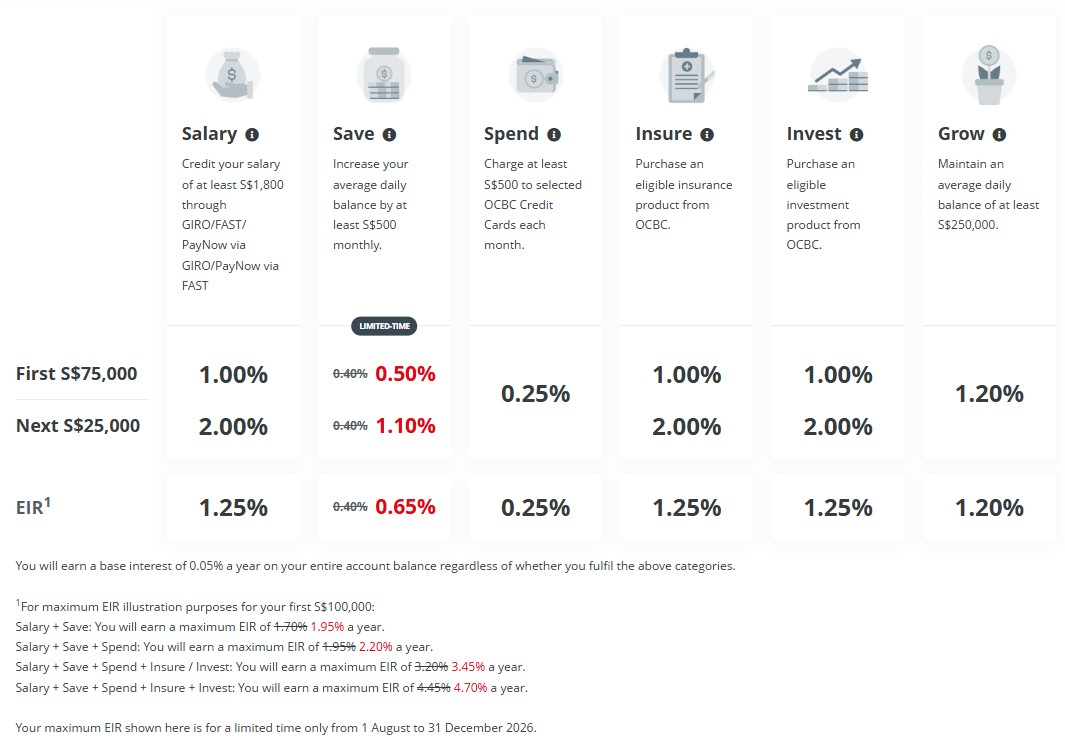

What you need to know about the OCBC 360 savings account

The OCBC 360 savings account offers an interest rate of up to 2.20% p.a. on the first S$100,000 of deposits when you meet three conditions: crediting your salary, saving more each month, and spending on an OCBC credit card.

On top of that, you can earn an additional 2.50% p.a. when you insure and invest through OCBC.

This makes the OCBC 360 one of the highest-yielding accounts in the market but also one of the harder ones to fully maximise.

Like the UOB One, the OCBC 360 uses a tiered interest structure, where the rates apply only to portions of your balance and are tied to specific categories.

These categories are:

- Salary: Credit a salary of at least S$1,800 each month through GIRO, FAST or PayNow.

- Save: Increase your average daily balance by at least S$500 monthly

- Spend: Charge at least S$500 to selected OCBC credit cards each month

- Insure: Purchase an eligible insurance product from OCBC

- Invest: Purchase an eligible investment product from OCBC

- Grow: Maintain an average daily balance of at least S$250,000

The interest you earn on the OCBC 360 account depends on two things: how many categories you fulfil and how much you have in your account.

The interest is tiered—applied first on balances up to S$75,000, and then on the next S$25,000, for a maximum of S$100,000 eligible for bonus interest.

Assuming you maintain a balance of S$100,000, here’s the maximum effective interest rate (EIR) you can achieve:

- Salary + Save: Maximum EIR of 1.95% a year.

- Salary + Save + Spend: Maximum EIR of 2.20% a year.

- Salary + Save + Spend + Insure / Invest: Maximum EIR of 3.45% a year

- Salary + Save + Spend + Insure + Invest: Maximum EIR of 4.70% a year

If you’re able to maintain at least S$250,000 in the account, you’ll unlock the Grow category, which adds an extra 1.20% p.a. on your first S$100,000. However, the remaining S$150,000 earns only the base interest of 0.05% p.a.

For most working adults, it’s relatively manageable to hit the Salary, Save, and Spend categories, which brings the EIR to up to 2.20% p.a.

However, it can be much harder to achieve the higher tiers, as they require you to purchase OCBC’s insurance or investment products.

Read our detailed review of the OCBC 360 account here.

UOB One vs OCBC 360: Which savings account pays more interest in Singapore

To find out whether the UOB One or OCBC 360 is the better savings account in Singapore, we compare the effective interest rate (EIR) across both accounts.

The EIR is the average interest you earn across your entire deposit balance, taking into account the tiered structure of each account.

For this comparison, we assume that you are someone who:

- Saves at least $500 a month

- Credits salary of at least S$1,800 every month

- Spends at least S$500 on eligible credit cards

- Does not buy insurance/investment products from the bank

Based on these conditions, the OCBC 360 account offers a higher effective interest rate than UOB One for balances up to around S$131,000.

Beyond that, UOB One starts to pull ahead because its bonus interest applies on balances of up to S$150,000, while OCBC 360’s main bonus categories are capped at the first S$100,000.

| Total Balances | UOB One | OCBC 360 | Winner |

| Max EIR (p.a.) | Max EIR (p.a.) | ||

| S$50,000 | 1.00% | 1.80% | OCBC 360 |

| S$75,000 | 1.00% | 1.80% | OCBC 360 |

| S$100,000 | 1.38% | 2.20% | OCBC 360 |

| S$125,000 | 1.60% | 1.77% | OCBC 360 |

| S$150,000 | 1.90% | 1.48% | UOB One |

| Source: UOB One, OCBC 360 as of 5 August 2026 | |||

How does OCBC 360 compare to UOB One when adding insurance and investment products?

The OCBC 360 account already offers competitive returns with just the salary, save, and spend categories.

But what happens if you also take up OCBC’s insurance and investment products?

By doing so, the maximum effective interest rate (EIR) on the first S$100,000 can go up to 3.45% p.a. if you add either insurance or investments, and as high as 4.70% p.a. if you take up both.

To find out how it stacks up against UOB One, let’s calculate the effective interest rate for someone who:

- Save: Increase the account’s average daily balance by at least S$500 compared with the previous calendar month

- Credits a salary of at least S$1,800 every month

- Spends at least S$500 on eligible OCBC credit cards

- Buys an insurance and/or investment product with OCBC

From the comparison below, the OCBC 360 account offers a higher effective interest rate compared to the UOB One account if you are looking to purchase an investment or insurance product (or both) from OCBC, regardless of your account balance.

| Total Balances | UOB One | OCBC 360 (invest OR insure) | OCBC 360 (invest AND insure) |

| Max EIR (p.a.) | Max EIR (p.a.) | Max EIR (p.a.) | |

| S$50,000 | 1.00% | 2.80% | 3.80% |

| S$75,000 | 1.00% | 2.80% | 3.80% |

| S$100,000 | 1.38% | 3.45% | 4.70% |

| S$125,000 | 1.60% | 2.77% | 3.77% |

| S$150,000 | 1.90% | 2.32% | 3.15% |

| Source: UOB One, OCBC 360 calculators as of 5 August 2026. | |||

Are there any promotions for UOB One and OCBC 360 in August 2026?

UOB is running its Level Up Your Savings Promotion until 30 September 2026.

Under the promotion, eligible customers can receive up to S$800 cash when they deposit new funds into eligible UOB savings accounts, including the UOB One Account. The funds will be earmarked for about seven months.

OCBC is also offering a cash reward for customers who open a new OCBC 360 Account and credit a salary of at least S$1,800 by the following month. New-to-OCBC customers may receive S$60, while existing OCBC customers opening a new 360 Account may receive S$30. This offer runs until 30 September 2026.

These promotions may improve the overall return, but they should be considered separately from the base account interest rates.

What would Beansprout do?

Both the UOB One and OCBC 360 are among the best high-yield savings accounts in Singapore, but which one works better for you depends on your priorities.

I would start with how much cash I intend to keep in the account.

If I have up to S$100,000 and can meet the Salary, Save and Spend requirements, OCBC 360 currently pays more interest than UOB One.

At a balance of S$100,000, OCBC 360 offers an EIR of 2.20% p.a., compared with 1.38% p.a. for UOB One.

However, I would keep in mind that the higher Save bonus is scheduled to end on 31 December 2026, and I need to increase my average daily balance by at least S$500 compared with the previous month to qualify.

If I am looking to take up OCBC’s insurance and investment products, the EIR can climb significantly, reaching as high as 4.70% p.a. on the first S$100,000.

If I have around S$131,000 to S$150,000, UOB One becomes more competitive because its bonus interest tiers extend up to S$150,000 with an EIR of 1.90% p.a, and does not require me to keep growing my account balance every month.

As an added note, UOB is currently running its Level Up Your Savings Promotion until 30 September 2026, offering up to S$800 in guaranteed cash for eligible account holders.

You can read our in-depth reviews to learn more about the UOB One account and the OCBC 360 account, depending on which is better suited to your needs.

For balances above the bonus interest caps, I would consider splitting my cash across more than one savings account instead of leaving the excess balance to earn only the base interest rate.

Check out our guide to the best savings accounts in Singapore to find other accounts that may complement UOB One or OCBC 360.

If you are deciding where to park your cash, you can also explore how these savings account fit into the broader Liquidity Pot, alongside fixed deposits, Singapore T-bills and Singapore Savings Bonds and money market funds.

Once you have already set aside enough cash for your safety buffer and upcoming expenses, you may also want to learn how the Four Pots of Wealth framework can help you grow your wealth, as well as read our beginner’s guide to start investing in Singapore.

To find out other ways to make your savings work harder, check out our guide to best ways to earn a passive income in Singapore.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Find out which savings account allows you to earn the highest interest rate on your savings.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments