Budget 2026 at a Glance: 8 Ways It Could Affect Your Wallet

Retirement

By Gerald Wong, CFA • 12 Feb 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Discover how Singapore Budget 2026 could impact your finances: CDC vouchers, CPF contribution changes, new CPF investment scheme and more.

Prime Minister and Finance Minister Lawrence Wong has shared that Singapore 2026’s Budget is the first step in refreshing Singapore’s strategies for a more uncertain and fractured world.

Last year, we saw a round of household support measures, including additional CDC vouchers, cash payouts to help with cost pressures, and enhanced assistance for families and seniors announced as part of Budget 2025.

Some of the key measures announced as part of Budget 2026 include a new CPF investment scheme, CDC vouchers, Cost-of-Living Special Payment and U-Save rebates, Child LifeSG credits for families with young children, and strengthened retirement and long-term care measures such as CPF top-ups for eligible seniors and higher CPF contributions for older workers.

Let us take a look at some of the key announcements made today as part of his Budget 2026 speech and evaluate how they may potentially impact you.

8 ways Singapore Budget 2026 could affect you

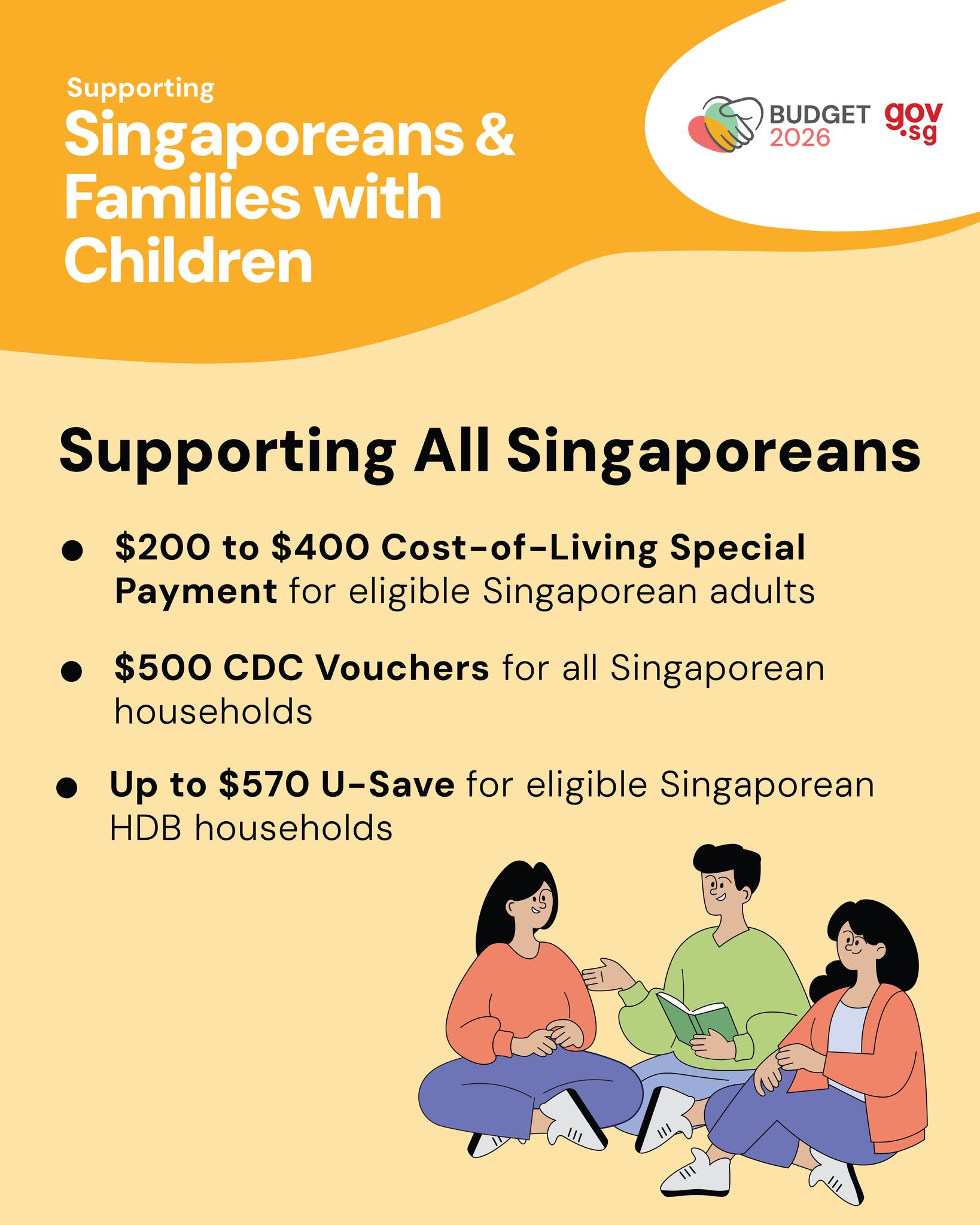

#1 – CDC vouchers (S$500 per household)

Who is it for: All Singaporean households

All Singaporean households will receive S$500 in CDC vouchers in Jan 2027, to help with daily expenses at participating supermarkets and heartland merchants/hawkers.

#2 – Cost-of-Living Special Payment (S$200 to S$400 cash)

Who is it for: Eligible Singaporeans aged 21 and above

Eligible Singaporeans will receive a one-off S$200 to S$400 Cost-of-Living Special Payment in Sep 2026, tiered by income and housing profile.

#3 – U-Save Rebates (up to S$570)

Who is it for: Eligible HDB households

Eligible HDB households will receive up to S$570 in U-Save rebates in FY2026, with rebates credited in Apr 2026 and Jul 2026, to help cushion utility bills.

#4 – Child LifeSG Credits (S$500 per child)

Who is it for: Families with Singaporean children aged 12 and below

Families will receive S$500 in Child LifeSG credits per child, which can be used to offset household spending such as groceries and utilities.

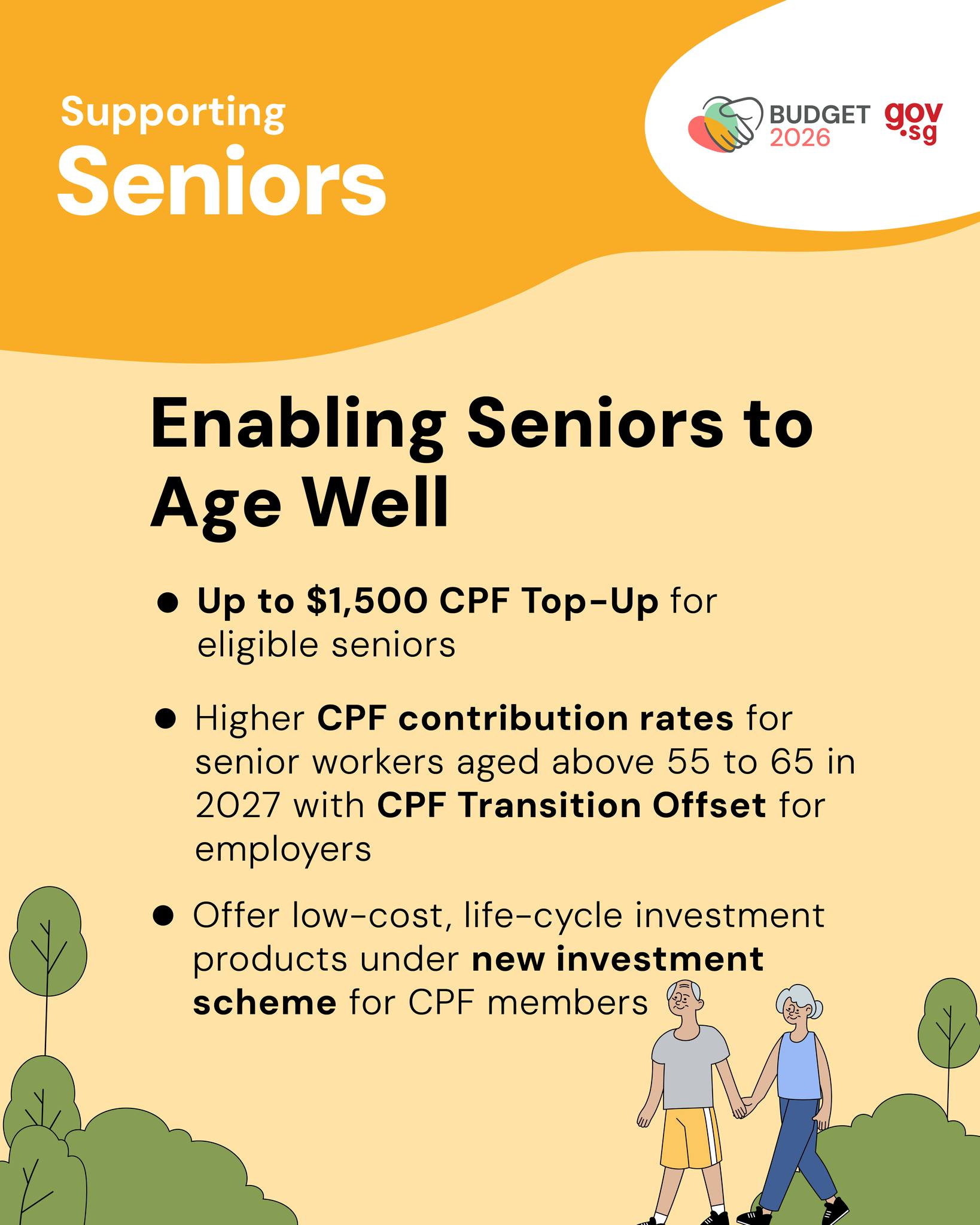

#5 – One-time CPF Top-up for Eligible Seniors (up to S$1,500)

Who is it for: Eligible Singaporeans born in 1976 or earlier who have lower CPF retirement savings.

Through a one-time CPF top-up of up to $1,500 for those who have not met their Basic Retirement Sum (BRS), retirement support for seniors will be strengthened.

The top-up will be credited in December 2026 into the individual’s CPF Retirement Account (RA). If the RA has not been created, the top-up will be credited into the Special Account.

Learn more about CPF Retirement Sum: Guide to FRS, ERS and BRS in 2026 here.

#6 - CPF contribution rate increases for senior workers

Who is it for: Senior workers aged above 55 to 65 (and their employers)

The Government will proceed with the next step of CPF contribution rate increases for senior workers in 2027.

From Jan 1, 2027, the CPF contribution rates for workers aged above 55 to 60 will increase by 1.5 percentage points.

Employees’ contribution will increase from 18 per cent to 19 per cent, while the employers’ contribution will increase from 16 per cent to 16.5 per cent.

For workers aged above 60 to 65, both the employees’ and employers’ contribution rates will each increase 0.5 percentage point to 13 per cent.

Employers will receive a CPF Transition Offset that covers half of the employer increase for 2027.

Read also: CPF contribution changes from 1 January: How will they affect you

#7 - New CPF life-cycle investment scheme (launching in 2028)

Who is it for: CPF members who want a simpler, long-term investing option and are willing to take some risk for potentially higher returns.

The CPF Board will introduce a new voluntary life-cycle investment scheme, where members’ portfolios are automatically adjusted to become more conservative over time.

The scheme is expected to be launched in the first half of 2028. Members who prefer greater flexibility can continue using the existing CPF Investment Scheme (CPFIS) options.

This new approach is designed to support long-term investors who are willing to take some investment risk for potentially higher returns, but who may prefer a simpler, more hands-off experience.

Under the scheme, the CPF Board will work with commercial providers to offer simplified, low-cost, and diversified investment products. These portfolios will automatically rebalance towards lower-risk assets as members approach their target date.

The scheme will cater to members who wish to stay invested for the long term without having to actively manage their CPF investments.

Participation in the scheme will be entirely voluntary.

Learn more about CPF investment scheme here.

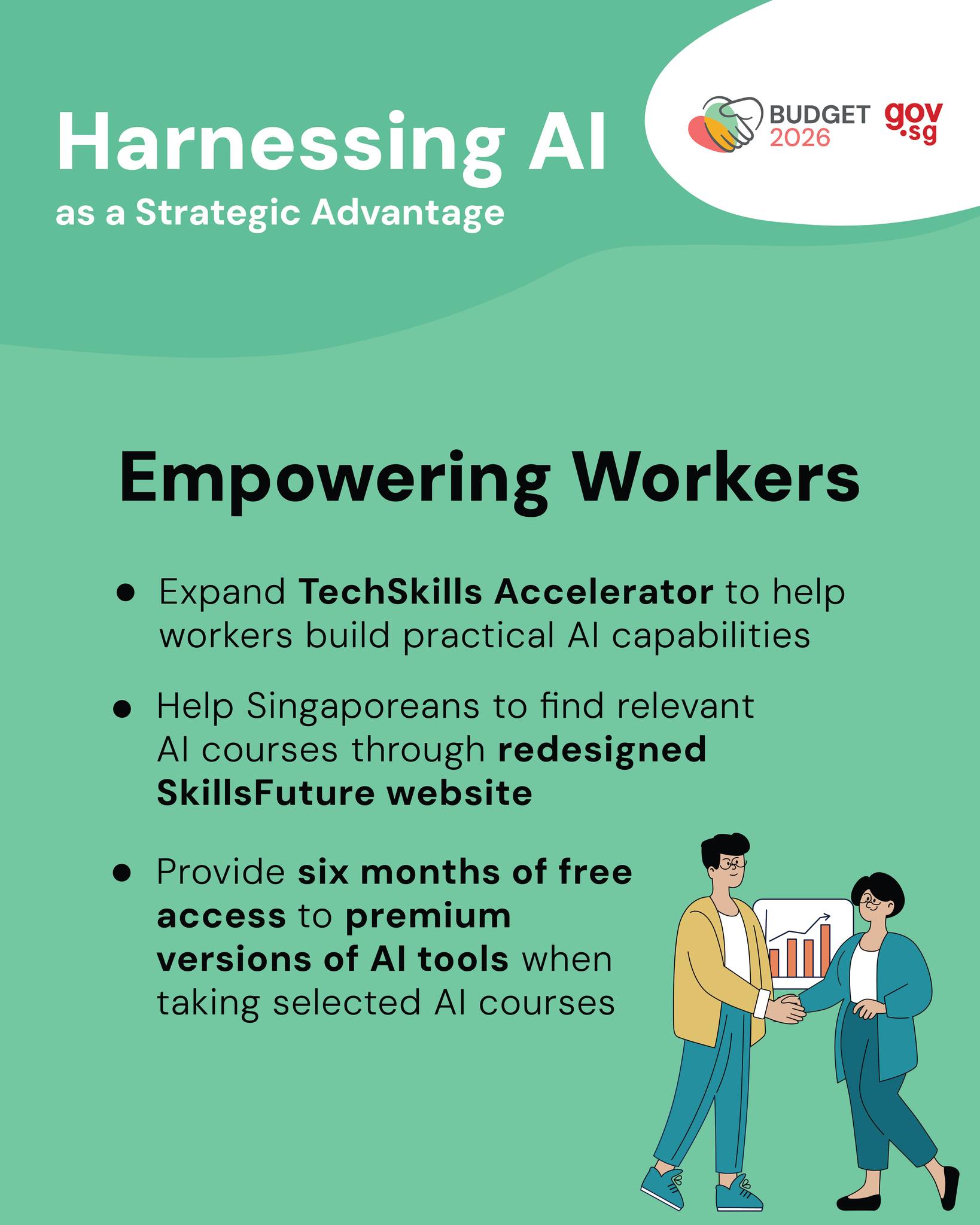

#8 – More Support for AI Upskilling (SkillsFuture)

Who is it for: Working Singaporeans taking selected AI courses

Singaporeans who complete selected AI training will get six months’ free access to premium AI tools, and SkillsFuture resources will be enhanced to make AI learning pathways easier to navigate.

What would Beansprout do?

While the vouchers to offset living expenses are helpful, taking steps to build our long-term financial security remains essential.

To ensure retirement adequacy, I will consider different ways to grow our CPF retirement savings.

One of the options is to transfer funds from our CPF Ordinary Account (OA) to your CPF Special Account (SA) to earn a higher interest rate. We discuss the pros and cons of transferring to your SA here.

I can consider a Retirement Sum Top-Up (RSTU), which will also allow me to enjoy tax relief.

Alternatively, I may also choose to invest my CPF funds. We look at the different investment options eligible for the CPF Investment Scheme here.

Outside of the CPF, I will also be looking at other ways to generate passive income to strengthen my retirement nest egg. Learn more about the different ways to generate passive income.

Finally, retirement goals and financial circumstances can change over time, so reviewing your plan periodically is a prudent approach.

Join the Beansprout Telegram group for the latest financial insights to grow your wealth.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments