Beginner's guide to start investing in Singapore (2026)

Stocks 101

By Nicole Ng • 12 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Learn how to start investing in Singapore in 2026, from building your cash buffer to choosing a brokerage, ETFs, REITs, stocks and CPF.

What happened?

Many of us want to start investing in Singapore, but it can be hard to know where to begin.

Saving alone may not be enough, as prices tend to rise over time and the money in my bank account may lose purchasing power if it grows more slowly than inflation.

That is why investing matters.

For beginners, investing is not about finding the next hot stock or getting rich quickly, but about helping our money grow steadily over time while managing risk.

Today, it has become easier to start investing in Singapore, with options ranging from Singapore Savings Bonds, T-bills and ETFs to stocks, REITs, robo-advisors and regular savings plans.

In this guide, we look at what to do before investing, which accounts you may need, and the common investment options available to beginners.

Why should you invest? The power of compounding

To me, investing is about making my money work harder over time.

When I invest, I am putting money into assets that may grow in value, generate income, or both. This could include stocks, ETFs, bonds, REITs, funds or other investment products.

Unlike a savings account, investment returns are not guaranteed. But by taking a sensible amount of risk, I may have a better chance of growing my wealth over the long term.

The key reason is compounding.

Compounding happens when the returns I earn are reinvested, so they can generate even more returns in future.

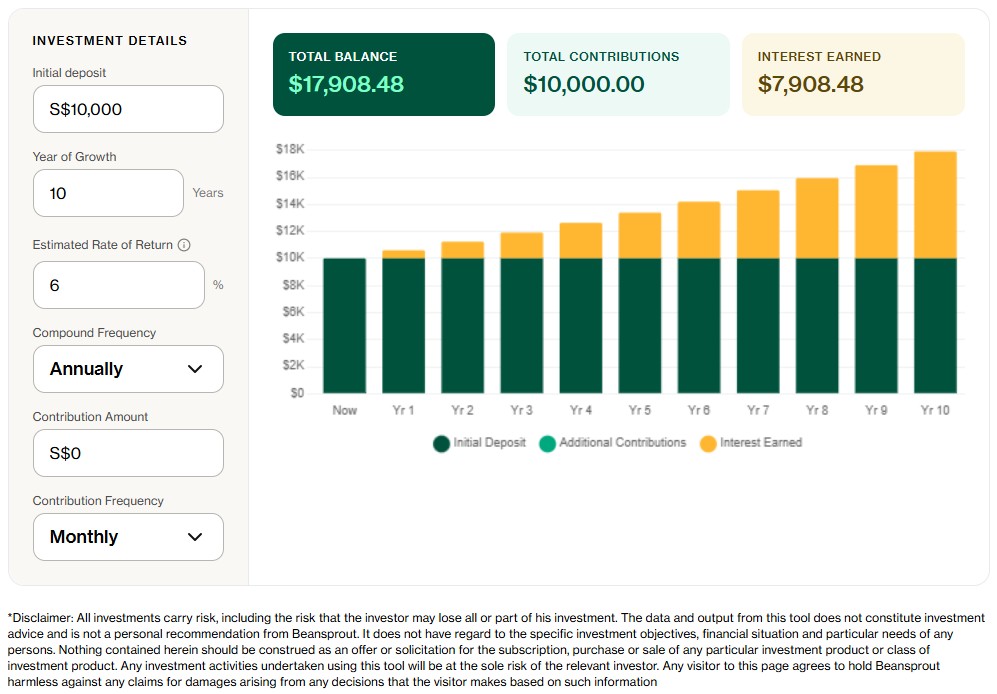

For example, if I invest S$10,000 and earn 6% a year, the amount could grow to about S$17,900 after 10 years. If I keep it invested for 20 years, it could grow to about S$32,100.

This is why starting early can make a big difference.

Even if I do not begin with a large amount, investing consistently over time can help me build wealth gradually.

You can use our compound interest calculator to see how regular contributions and compounding may grow your portfolio over time.

Things to consider before starting investing

Before I start investing, I would first make sure that my financial foundation is in place.

Investing involves risk. The value of investments can go up and down, and there may be times when I have to wait years before seeing meaningful returns.

That is why I would not invest money that I may need urgently in the short term.

At Beansprout, we think about this through the Four Pots of Wealth framework, where each part of our money has a clear role. The first pot to build is the Liquidity Pot, which is meant to keep our safety buffer ready for short-term needs and unexpected expenses.

For me, this usually means setting aside enough cash for emergencies and near-term goals before taking on more investment risk.

This money could be kept in lower-risk and accessible instruments such as savings accounts, fixed deposits, T-bills, Singapore Savings Bonds or money market funds.

Once this Liquidity Pot is in place, I would feel more comfortable investing the rest of my money for longer-term goals.

Here are some things I would check before getting started.

| Checklist | Why it matters |

| I have paid off high-interest debt | It may not make sense to invest if my debt is costing me more than what I can reasonably earn |

| I have an emergency fund | This helps me avoid selling my investments during a market downturn |

| I have basic insurance protection | This protects me from large unexpected expenses |

| I have set aside money needed in the next 1 to 3 years | Short-term goals should not be exposed to too much market volatility |

| I understand what I am investing in | This reduces the risk of buying products based only on hype |

As a simple rule, money that I need soon should usually stay in safer and more liquid options.

For example, if I am saving for a BTO down payment, wedding, renovation or school fees in the next few years, I would be more careful about putting that money into volatile investments.

Instead, I may look at savings accounts, fixed deposits, T-bills, SSBs or money market funds as part of my Liquidity Pot.

Once my short-term needs are covered, I can start thinking about how to grow my wealth over the longer term.

What account do I need to start investing in Singapore?

Before choosing what to invest in, it helps to understand the accounts and platforms I may need.

For most investors in Singapore, there are two main things to think about: a brokerage account and how the investment is held.

With a CDP account, eligible Singapore-listed shares are held directly under my name with the Central Depository. With a custodian account, the brokerage or platform holds the investments on my behalf.

| Account type | What it means | What to note |

| CDP account | Shares are held directly under my name | Often used for Singapore-listed stocks and REITs, bonds and T-bills |

| Custodian account | Shares are held by the brokerage or platform on my behalf | Common for overseas stocks, ETFs and lower-cost platforms |

There is no single best option for everyone.

Some investors prefer CDP because they like holding Singapore shares directly under their own name. Others may prefer custodian platforms because they often offer lower fees, easier access to overseas markets, and more features for investors who want to buy US stocks, ETFs or set up regular savings plans.

If you are unsure which option is better for you, you can read our guide on CDP vs custodian accounts.

If you decide to use a CDP account, here’s a step-by-step guide on how to open a CDP account and start trading on SGX.

Once the account setup is clear, the next step is to choose a brokerage that fits what I want to invest in, whether that is Singapore stocks, US stocks, ETFs, REITs or a regular savings plan.

If you are still deciding which platform to use, you can read our guide to the best online brokerages in Singapore, where we compare the fees, products and features of different trading platforms.

You can also check our exclusive brokerage promotions to see the latest Beansprout offers and sign-up rewards available for selected platforms.

Common investment options for beginners in Singapore

Once my Liquidity Pot is in place and I’ve opened my brokerage accounts, the next step is to understand the different ways I can start investing.

There are many investment options in Singapore, and they do not all serve the same purpose. Some are better for short-term cash parking, while others are more suitable for long-term growth or income.

Here are some of the common options beginners may come across.

#1 - Guide to Stocks

Buying stocks means owning a share of a company.

If the company performs well, its share price may rise over time. Some companies may also pay dividends to shareholders.

This is why stocks can be useful for investors who are looking for long-term growth or dividend income.

The trade-off is that stocks also come with higher risk and bigger price swings, so their value can move up or down sharply. Investing in stocks usually requires more research, patience, and confidence to manage actively.

In Singapore, well-known stocks include DBS and Singapore Airlines (SIA). Globally, popular names include Apple and Nvidia in the US, and Alibaba in China.

These examples show how stock investing lets you own a piece of companies you already know and use in your daily life.

You can learn more through these guides and tools:

- Beansprout's guide to Singapore blue chip stocks

- Best Singapore high dividend stocks

- Best Singapore dividend stocks

#2 - Guide to REITs

Real Estate Investment Trusts, or REITs, allow investors to gain exposure to income-generating properties without having to buy a physical property directly.

In Singapore, REITs may own malls, offices, industrial buildings, hotels, logistics assets or data centres.

REITs are popular with income investors because they typically distribute rental income to unitholders.

However, REITs are not risk-free. Their unit prices can be affected by interest rates, property demand, rental income, debt levels and refinancing costs.

In Singapore, some well-known examples include CapitaLand Integrated Commercial Trust, which owns malls like Plaza Singapura and Bugis Junction, and Mapletree Pan Asia Commercial Trust, which owns iconic properties such as VivoCity. These familiar names make it easier to see how REITs connect to places we visit and enjoy every day.

You can learn more through these guides and tools:

#3 - Guide to ETFs

Exchange-traded funds, or ETFs, allow me to invest in a basket of stocks, bonds or other assets through a single product.

This makes ETFs one of the simpler ways to diversify.

For example, an STI ETF gives me exposure to a basket of Singapore blue chip stocks, while an S&P 500 ETF gives me exposure to large US companies.

ETFs can be useful for beginners because I do not need to pick individual stocks from day one.

However, ETFs still carry market risk. If the market or asset class falls, the ETF can fall too.

You can learn more through these ETF guides:

- Beginner guide to ETF investing: How to choose your first ETF

- Overview of Exchange Traded Funds (ETFs) in Singapore

- Guide to Straits Times Index ETF: How to choose the best STI ETF for your portfolio

- Best S&P 500 ETFs for Singapore investors in 2025

- Best Singapore REIT ETFs: How to choose for your portfolio

- Best gold ETF in Singapore

#4 - Guide to Unit Trusts and Mutual Funds

Unit trusts and mutual funds pool money from many investors to invest in a portfolio of assets.

These funds are managed by professional fund managers and may invest in stocks, bonds or a mix of both.

They can be useful if I want diversification and professional management without choosing individual stocks or bonds myself.

The trade-off is that fees can be higher than some ETFs. These may include management fees, platform fees or sales charges.

Before investing, I would check the fund’s objective, holdings, fees, performance history and risk level.

You can learn more through these guides:

- Unit Trusts in Singapore: A Complete Guide for Investors

- Best platforms to buy unit trusts in Singapore

- Guide to mutual fund pricing and fees

#5 - Guide to Robo-Advisors

Robo-advisors are digital platforms that build and manage investment portfolios based on my goals and risk profile.

They may be useful if I want a more guided way to start investing and do not want to choose individual ETFs or stocks myself.

The benefit is convenience. Many robo-advisors allow investors to start with a relatively small amount and invest regularly over time.

The trade-off is that I have less control over the exact investments, and platform fees still apply.

Before using a robo-advisor, I would check what the portfolio invests in, how much risk I am taking, and what fees I am paying.

You can learn more through these robo-advisor guides and reviews:

- Best robo-advisors in Singapore

- Syfe Review: A robo-advisor that makes investing easy

- StashAway Review: A beginner-friendly platform to start investing

#6 - Guide to Singapore Savings Bonds (SSBs)

Singapore Savings Bonds, or SSBs, are backed by the Singapore Government.

They pay interest every six months and can be redeemed before maturity, which makes them more flexible than many traditional bonds.

This can make SSBs useful for investors who want a lower-risk option but do not want to lock up their money for too long.

The main thing to note is that redemptions follow a monthly schedule, so I may not receive my cash immediately.

You can learn more through this guide:

#7 - Guide to Treasury Bills (T-bills)

Treasury bills, or T-bills, are short-term securities backed by the Singapore Government.

They are commonly used by investors who want a low-risk place to park cash for 6 or 12 months.

T-bills can be useful when yields are attractive, but I should be comfortable holding them to maturity. If I need to sell before maturity, the price may move depending on market conditions.

You can learn more through these guides:

- Singapore Treasury Bills (T-bills): A Complete Guide

- Complete guide to buying Singapore Treasury Bill using your CPF

- Apply for T-bills using CPF OA via DBS i-banking: A step-by-step guide

- Apply for T-bills online using CPF OA via OCBC: A step-by-step guide

- Apply for T-bills online using CPF OA via UOB: A step-by-step guide

- Guide to T-bill auction: How to make competitive bids

#8 - Guide to Cash Management Accounts

Cash management accounts are offered by digital investment platforms and are often used to make idle cash work harder.

They typically invest in lower-risk instruments such as money market funds, short-term bonds or deposits.

They may offer higher potential returns than a regular savings account, while still keeping cash relatively accessible.

However, returns are not guaranteed, and the value of the account may move slightly depending on market conditions.

You can learn more through this guide:

#9 - Guide to CPF and SRS

Your CPF is an important part of your financial planning and retirement.

For many Singaporeans, CPF savings form the base of their long-term retirement plan. CPF savings already earn interest, so I would not treat CPF investing in the same way as investing with spare cash.

Before investing my CPF savings, I would first ask whether the investment can realistically do better than the CPF interest I would otherwise earn, after fees and risks. This is especially important because CPF savings may be used for major life goals such as housing, healthcare and retirement.

Under the CPF Investment Scheme, eligible CPF members can invest their CPF Ordinary Account or Special Account savings in selected products, subject to CPF rules. However, CPF investing is not something I would rush into as a beginner.

Instead, I would first understand how CPF fits into my broader financial plan. This includes how to grow CPF savings for retirement, how CPF LIFE payouts work, and what to consider before investing CPF savings.

You can learn more through these CPF and SRS guides:

- How to grow your CPF for retirement adequacy

- Guide to the CPF Investment Scheme (CPFIS)

- CPF Retirement Sum: Guide to FRS, ERS and BRS in 2026

- Guide to CPF LIFE: Lifelong payouts for your retirement

- Tax Relief in Singapore: Ways to Reduce Your Income Tax

- SRS in Singapore: How to unlock tax savings with Supplementary Retirement Scheme

- CPF SA interest rate at 4.05%. Should you do a top-up?

- CPF SA interest rate raised to 4.01%. Should you transfer from OA to SA?

- 8 ways to invest your SRS to grow your retirement savings

#10 - Guide to Alternative Investments (Gold and Silver)

Gold and silver are often seen as alternative assets.

Gold, in particular, is sometimes used as a store of value or portfolio diversifier during periods of inflation, market stress or currency uncertainty.

However, gold and silver do not generate dividends or interest. This means returns depend mainly on price movements.

There are several ways to gain exposure, including physical gold and silver, gold savings accounts, ETFs and funds.

I would view precious metals as a diversifier, rather than the foundation of my portfolio.

You can learn more through these guides:

- How to buy gold in Singapore

- How to buy gold from UOB: A step-by-step guide

- How to buy silver in Singapore

How to decide on your first investment options

With so many investment options available, it can be hard to know where to begin.

Before choosing a product, I would first ask: what is this money meant for?

At Beansprout, we think about this through the Four Pots of Wealth framework.

| Pot | What it is for | What matters most |

| Liquidity Pot | Emergency cash and near-term needs | Safety and easy access |

| Growth Pot | Long-term wealth building | Compounding and diversification |

| Income Pot | Regular income and retirement cash flow | Sustainable payouts |

| Opportunity Pot | Higher-conviction ideas | Upside potential and risk control |

This matters because not all money should be invested in the same way.

Money needed in the next few years, such as for a wedding, renovation or BTO down payment, should usually be kept in lower-risk and more liquid options.

Money meant for long-term goals, such as retirement or wealth building, can usually take more volatility because there is more time to ride through market ups and downs.

I would also consider a few key factors before investing:

- Time horizon: How long I can keep the money invested

- Risk tolerance: Whether I can stay calm when markets are volatile

- Liquidity: How quickly I may need the cash back

- Expected returns: How much the investment may grow over time

- Volatility: How much the value may move up or down

In short, I would not start by asking, “What is the best investment?”

I would start by asking, “Which pot is this money meant for?” Once that is clear, it becomes easier to decide whether the money belongs in safer options, diversified investments, income assets, or higher-risk opportunities.

What would Beansprout do?

If I were just getting started, I would not rush into buying stocks immediately.

First, I would build my Liquidity Pot so that I have enough cash set aside for emergencies and near-term goals. This is part of Beansprout’s Four Pots of Wealth framework, which helps us organise our money based on its purpose.

Next, I would make sure I have my account setup, including understanding the difference between a CDP and custodian account, and choosing a brokerage that fits what I want to invest in.

If I plan to invest in Singapore Savings Bonds or apply for T-bills using cash, I would also make sure I have opened a CDP account.

For money that I may need soon, I would keep it in lower-volatility options such as T-bills, Singapore Savings Bonds or cash management accounts.

Once my short-term needs are covered, I would start investing for longer-term goals through simple and diversified options such as ETFs, robo-advisors or regular savings plans.

As I become more confident, I may explore individual stocks, REITs, unit trusts or other assets depending on whether I am building my Growth Pot, Income Pot or Opportunity Pot.

For investors focused on building an Income Pot, our guide to best ways to earn passive income in Singapore can also offer useful ideas.

I would also treat CPF and SRS as important parts of my retirement foundation.

For CPF, I would only invest my CPF savings if I understand the risks and believe the investment can do better than CPF interest over time. For SRS, I would consider how SRS can help with tax savings today, while making sure the money is invested prudently for long-term retirement needs.

The key is not to find the best investment from day one, but to build a structure that matches my goals, time horizon and risk appetite.

For those of us who are just beginning our investment journey, the key is to start small, build confidence gradually, and focus on long-term consistency rather than quick wins.

To get a sense of the long-term impact of compounding, try our compound interest calculator and explore different scenarios with it.

If you are just starting to invest in Singapore, which option are you considering first? Share with us in the comments below or in our Telegram group!

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments