Standard Chartered Bonus$aver: Earn up to 5.85% p.a. after latest rate cut

Savings, Savings Account

By Beansprout • 04 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Standard Chartered Bonus$aver offers bonus interest with salary credit, card spend, and wealth products of up to 5.85% p.a. Read our review of its rates, requirements, and May 2026 changes.

What happened?

Standard Chartered has cut Bonus$aver interest rates for the second time in 2026.

The latest revision took effect from 1 May 2026, lowering the account’s maximum interest rate on the first S$100,000 eligible deposit balance from 7.05% p.a. to 5.85% p.a.

This follows an earlier revision on 1 January 2026, when Bonus$aver rates were also reduced to align with longer-term market expectations.

Still, the Standard Chartered Bonus$aver account remains one of the higher-yield savings accounts in Singapore for those willing to meet multiple banking and wealth criteria.

With savings account rates coming down, I’ll take a closer look at how the Standard Chartered Bonus$aver Account works, how much interest you can earn, and whether it is still worth considering.

What is the Stanchart Bonus Saver (Bonus$aver) account?

The Standard Chartered Bonus$aver Account is a high-interest savings account offering a high interest rate if you are able to fulfil certain requirements.

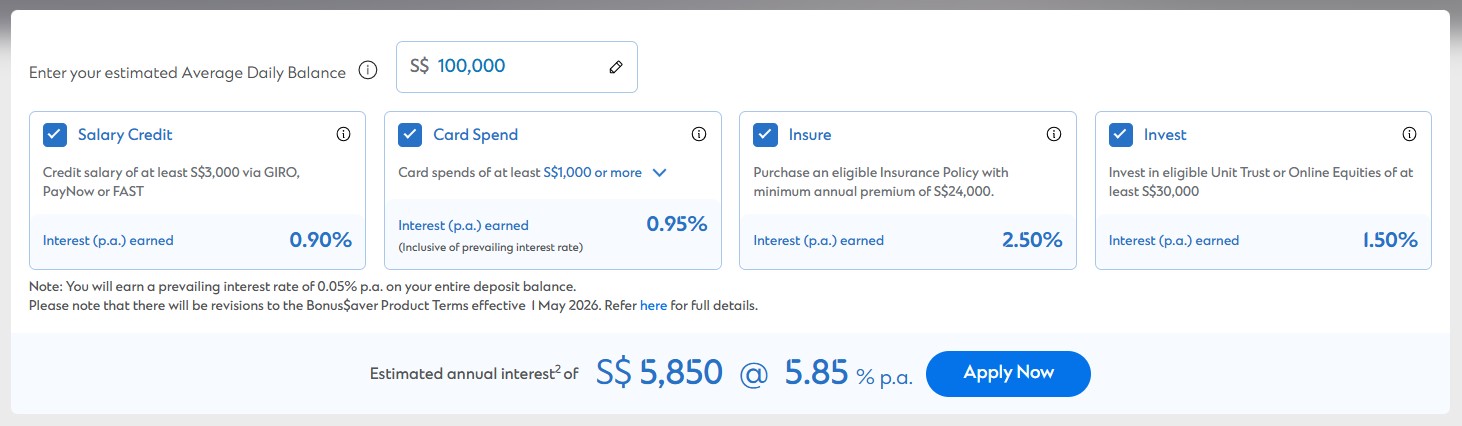

By meeting specific monthly criteria, you can earn interest rates of up to 5.85% per annum. To achieve this, you must:

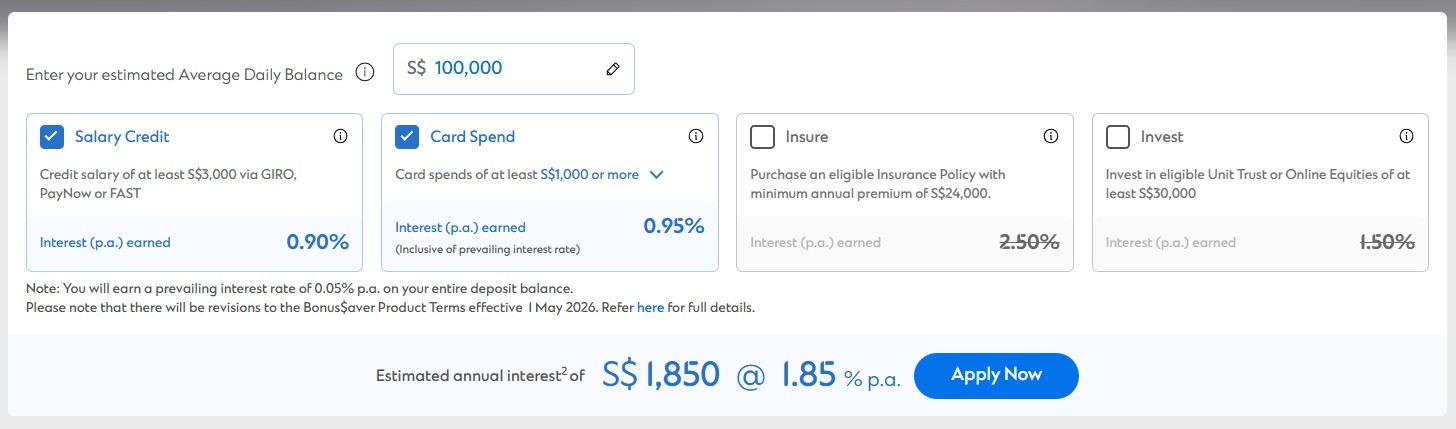

- Credit Salary: Deposit a minimum of S$3,000 monthly via GIRO, PayNow, or FAST.

- Card Spend: Charge at least S$1,000 monthly on a Standard Chartered credit card.

- Insure: Purchase an eligible insurance policy with a minimum annual premium of S$24,000.

- Invest: Invest a minimum of S$30,000 in eligible unit trusts.

How much interest can you earn with the Standard Chartered Bonus$aver Account?

The amount of interest you can earn depends on which criteria you are able to meet.

Based on the latest rates, here are the approximate maximum interest rates you can earn on the first S$100,000 eligible deposit balance:

| Bonus interest component | From 1 May 2026 onwards |

|---|---|

| Card spend (minimum eligible spend of S$1,000 monthly) | 0.90% p.a. |

| Salary credit (regular inward credit through GIRO, PayNow or FAST) | 0.90% p.a. |

| Invest (invest in eligible Unit Trust or Online Equities of at least S$30,000; bonus interest paid for a consecutive period of 6 months) | 1.50% p.a. |

| Insure (bonus interest paid for a consecutive period of 6 months) | 2.50% p.a. |

| Prevailing interest rate | 0.05% p.a. |

| Total interest on your first S$100,000 eligible deposit balance | 5.85% p.a. |

Based on Standard Chartered’s revised rates, here are the new maximum effective interest rates effective 1 May 2026 onwards:

- Salary + Card Spend: 1.85% p.a.

- Salary + Card Spend + Invest: 3.35% p.a.

- Salary + Card Spend + Insure: 4.35% p.a.

- Salary + Card Spend + Invest + Insure: 5.85% p.a.

For most savers, the more realistic rate may be 1.85% p.a., assuming they credit their salary and spend at least S$1,000 on eligible card transactions each month.

The higher rates require you to invest or buy insurance through Standard Chartered.

It is also worth noting that the Invest and Insure bonus interest is only paid for six consecutive months after you meet the criteria.

Let me share what I like and dislike about this deposit account in the next section.

What I like about Stanchart Bonus Saver (Bonus$aver) account

#1 - Uniform interest rate on the first S$100,000 regardless of deposit amount

Let’s kick things off on a positive note.

This deposit account stands out because it doesn’t use a tiered system for interest rates. Whether you have $50k or $100k in your account, you’ll earn the same interest rate on all your deposits.

This makes the interest earned on this account fairly straightforward to calculate, so long as you are able to meet the requirements of various categories.

#2 - Multi-currency feature

Also, this deposit account comes with a multi-currency feature, which provides convenience, reduces fees, and gives you the financial agility to manage your money efficiently across borders.

It allows you to hold and transact in multiple currencies without the need for separate accounts or frequent conversions, which means more flexibility and savings.

Whether you’re traveling, investing abroad, or making payments in different currencies, this feature helps you avoid the often hidden costs of foreign exchange fees.

What I dislike about Stanchart Bonus Saver (Bonus$aver) account

#1 - Investment and insurance required to unlock higher interest rates

The headline interest rate of 5.85% p.a. may look attractive.

However, it requires you to meet all four categories: Salary Credit, Card Spend, Invest and Insure.

So, what’s a realistic interest rate to expect with the Standard Chartered Bonus$aver (Bonus$aver) account?

If you’re able to:

- Spend at least $1,000 on your credit card

- Credit at least $3,000 monthly salary

Then, the realistic interest rate you can expect will be around 1.85% per annum—much lower than the advertised 5.85%.

Also, the $1,000 credit card spend must be on eligible transactions. Unfortunately, things like online bill payments, income tax payments, EZ-link transactions, top-ups, and AXS payments do not count towards the qualifying spend.

To unlock a higher interest on the Stanchart Bonus Saver account, you will need to meet the criteria for the Insure and Invest categories:

- You’ll need to purchase new insurance policies or investments to qualify.

- The bonus interest is only paid for six consecutive months, after which you'll need to make fresh purchases to continue earning the bonus rate.

Comparing the Stanchart Bonus Saver (Bonus$aver) account to the UOB One account

In the high-yield savings account category, I’ll be comparing the Stanchart BonusSaver account with the OCBC 360 and UOB One savings accounts.

When it comes to interest rates, the Stanchart BonusSaver account still outshines the UOB One savings account.

If you can meet these basic requirements such as salary credit and card spend, Stanchart BonusSaver offers a higher interest rate compared to the UOB One.

| Cash available for deposit | Stanchart Bonus Saver (Max EIR) | UOB One (Max EIR) |

| Less than $75,000 | 1.85% | 1.00% |

| $75,000 - $100,000 | 1.85% | 1.38% |

Comparing the Stanchart Bonus Saver (Bonus$aver) account to the OCBC 360 account

If you are able to meet the investment and insurance requirements, then it might be worthwhile comparing with the OCBC 360 account.

For those who only meet the salary credit and spending criteria, the Stanchart BonusSaver offers a maximum EIR of 1.85%, while the OCBC 360 provides a higher rate of 1.95%.

However, if you are also able to meet either the Insure or Invest category, the Stanchart BonusSaver’s rate increases to 4.35%, the OCBC 360 lags with a 3.20% EIR.

For those who meet all the criteria—Salary, Save, Spend, Insure, and Invest—the Stanchart BonusSaver offers an EIR of 5.85%, whereas OCBC 360 maxes out at 4.45%.

1st May 2026 onwards, Bonus$aver continues to offer the higher maximum rate at 5.85% p.a., versus 4.45% p.a. for OCBC 360.

OCBC 360 offers a slightly better return for those meeting only the basic banking criteria, but Standard Chartered Bonus$aver still pulls ahead if you are able to meet the Insure or Invest categories.

From 1 May 2026 onwards | ||

| Categories met | Stanchart Bonus Saver (Max EIR) | OCBC 360 (Max EIR) |

| Salary + Save + Spend | 1.85% | 1.95% |

| Salary + Save + Spend + Insure/Invest | up to 4.35% | 3.20% |

| Salary + Save + Spend + Insure + Invest | 5.85% | 4.45% |

What are the latest Standard Chartered Bonus$aver promotions?

Standard Chartered is currently running a Bonus$aver sign-up promotion from 1 July to 31 August 2026.

Get S$228 cashback when you:

- Open a Bonus$aver Savings Account and a Bonus$aver World Mastercard Credit Card.

- Deposit and maintain at least S$50,000 in fresh funds in your new Bonus$aver account upon account opening.

Fresh funds means money not existing with Standard Chartered in the recent 30 days.

The promotion is valid from 1 July to 31 August 2026.

Find out more about the promotion and Terms and Conditions here.

What would Beansprout do?

The Standard Chartered Bonus$aver Account may still appeal to savers who want a high-interest savings account with a multi-currency feature for travel, overseas spending or international investing.

Even after the latest revision, Bonus$aver can still offer a headline interest rate of up to 5.85% p.a. on the first S$100,000.

However, this comes with fairly high hurdles.

To unlock the higher interest rate, you would need to meet the Invest and Insure categories, which require larger financial commitments.

For most savers who only credit their salary and meet the eligible card spend requirement, the more realistic rate is 1.85% p.a.

At this level, Bonus$aver remains competitive against some savings accounts, although it is less attractive than before the latest rate cut.

I would not buy an investment or insurance product just to earn a higher savings account interest rate.

If you're unable to meet these requirements, you may want to consider a more basic, no-frills savings account instead.

To find out how Standard Chartered Bonus$aver compares to other savings account in Singapore, check out our guide to the best savings accounts in Singapore.

If you are deciding where to park your cash, you can also explore how the Standard Chartered Bonus$aver Account fits into the broader Liquidity Pot, alongside fixed deposits, T-bills, Singapore Savings Bonds and money market funds.

To find out other ways to make your savings work hard, check out our guide to best ways to earn a passive income in Singapore.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Find out which savings account allows you to earn the highest interest rate on your savings.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Questions and Answers

2 questions

- unknown • 12 Apr 2026 04:12 AM

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20160.45%20160.45'%20style='enable-background:new%200%200%20160.45%20160.45;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%2300DBA4;}%20%3c/style%3e%3cg%3e%3cg%3e%3cpath%20class='st0'%20d='M80.23,0C35.99,0,0,35.99,0,80.23s35.99,80.23,80.23,80.23c44.24,0,80.23-35.99,80.23-80.23S124.46,0,80.23,0%20z%20M80.23,149.37c-1.73,0-3.45-0.09-5.15-0.21l0-38.76c-1.44-31.08,14.86-34.75,32.13-38.65c5.66-1.28,11.08-2.5,15.76-4.7%20c1.78,15.32-1.66,28.48-9.68,37.18c-0.11,0.11-10.83,10.24-23.27,10.24c-1.12,0-2.26-0.08-3.4-0.26l-1.72,10.94%20c1.73,0.27,3.44,0.4,5.11,0.4c16.97,0,30.39-12.77,31.2-13.57c11.35-12.3,15.63-30.42,12.07-51.01l-2.17-12.46l-10.42,7.15%20c-3.7,2.54-9.63,3.87-15.93,5.29c-16.97,3.82-42.62,9.6-40.75,49.71v36.77c-30.32-7.32-52.92-34.67-52.92-67.21%20c0-38.13,31.02-69.15,69.15-69.15c38.13,0,69.15,31.02,69.15,69.15S118.36,149.37,80.23,149.37z'/%3e%3cpath%20class='st0'%20d='M56.13,44.13c-3.86-0.87-7.5-1.69-9.57-3.11l-9.25-6.35l-1.92,11.06c-2.41,13.89,0.52,26.16,8.48,34.77%20c0.37,0.36,7.58,7.23,17.36,8.83c0.43-1.57,0.92-3.09,1.48-4.54c0.85-2.19,1.85-4.26,3-6.21c-7.3,0.3-13.91-5.81-13.92-5.81%20c0,0,0,0,0,0c-4.44-4.81-6.53-11.78-6.09-19.96c2.57,0.91,5.31,1.52,8.01,2.13c8.98,2.02,16.94,3.83,18.8,15.11%20c0.56-0.52,1.13-1.04,1.72-1.53c2.54-2.12,5.24-3.84,8-5.27C77.55,48.96,64.62,46.04,56.13,44.13z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Beansprout • 13 Apr 2026 02:57 AM

Beansprout • 13 Apr 2026 02:57 AM

- Eddy Tham • 07 Dec 2025 08:56 AM