Best savings accounts in Singapore with high interest rates [July 2026]

Savings

By Gerald Wong, CFA • 02 Jul 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Compare the best savings accounts in Singapore for July 2026, with rates of up to 5.85% p.a. depending on your cash balance and banking habits.

What happened?

Savings account rates are moving again in July 2026.

I noticed there several attractive fresh funds promotions this month, including from accounts such as CIMB FastSaver, Maybank iSAVvy and UOB.

At the same time, some high-yield savings accounts in Singapore continue to offer a maximum effective interest rate of up to 5.85% p.a.

However, I will have to meet certain conditions to earn these high interest rates on my savings account, such as salary crediting, card spend, fresh funds top-ups, or investment and insurance purchases.

This made me relook at the different savings accounts in Singapore and their ongoing promotions, especially whether the bonus interest applies to my entire balance or only to new funds I add.

After all, the best savings account will depend on how much cash I have and whether I can meet the qualifying criteria consistently.

In this guide, I compare the best savings accounts in Singapore in July 2026, outline the requirements to qualify for higher interest, and help you decide which account may work better for your situation.

The best savings accounts in Singapore

The best savings account in Singapore depends on how much cash you have and which requirements you can realistically meet.

Some accounts offer higher rates if you can credit your salary and spend on a linked credit card, while others may be more useful if you prefer fewer conditions.

Here is a quick summary of the savings accounts that may stand out for different situations, based on information available as of 2 July 2026.

| Scenario | Account to consider | Realistic interest rate (p.a.) |

| S$75,000 savings, salary credit, card spend, and investment or insurance purchase | Standard Chartered BonusSaver | Up to 5.85% p.a. |

| S$100,000 fresh funds in savings, salary credit or standing instruction of at least S$1,000, and S$800 monthly card spend | CIMB FastSaver Account | Up to 1.99% p.a. |

| S$150,000 savings, salary credit and S$500 monthly card spend | UOB One | Up to 1.90% p.a. |

| S$100,000 fresh funds in savings without salary credit or card spend | Maybank iSavvy (fresh funds) | Up to 1.68% p.a. |

| Student, NSF or no regular income, 29 years old and below with credit card or PayLah! retail spend | DBS Multiplier | 1.50% p.a. |

Best high-yield savings accounts in Singapore by maximum effective interest rate

A higher advertised effective interest rate may not always mean that an account is the best savings account for you.

Many of the highest headline rates require salary crediting, credit card spend, or the purchase of investment and insurance products.

To make the comparison clearer, I started by comparing the maximum effective interest rate offered by some of the most popular savings accounts in Singapore.

| Savings Account | Maximum Effective Interest Rate (p.a.) |

| Standard Chartered Bonus Saver | 5.85% |

| Bank of China SmartSaver | 4.60% |

| OCBC 360 | 4.45% |

| DBS Multiplier | 4.10% |

| CIMB FastSaver (Personal banking) | 2.70% |

| Trust Bank | 2.40% |

| CIMB StarSaver (Personal banking) | 2.09% |

| UOB One | 1.90% |

| Maybank iSAVvy (incremental ADB above S$200,000) | 1.68% |

| HSBC Everyday Global Account (fresh funds) | 1.65% |

| Standard Chartered eSaver (fresh funds) | 1.60% |

| Standard Chartered JumpStart | 1.50% |

| UOB Stash | 1.50% |

| SingFinance GoSaver | 1.30% |

| Singapura Finance Vivid Savings Account | 1.28% |

| Hong Leong Finance Premium SAVER Account | 1.20% |

| GXS* (Saving Pockets) | 1.08% |

| MariBank | 0.88% |

| Source: Various bank websites as of 2 July 2026. *Maximum deposit for GXS is S$95,000. | |

How we come up with the list of best savings accounts in Singapore

Does a higher advertised effective interest rate mean it is the best savings account in Singapore?

It depends.

The effective interest rate is the total annual interest earned as a percentage of your average balance in the savings account over the year.

We suggest looking at the effective interest rate rather than the headline interest rate, as a bank may offer an interest rate of “up to 6.0% p.a.”, but this rate may only apply to a specific deposit tier.

For example, the highest rate could apply only to balances above S$50,000, or only after you meet several qualifying conditions.

Hence, the best savings account would depend on whether you are able to fulfil these criteria, and how much cash you plan to keep in the account.

Featured high-yield savings accounts in Singapore

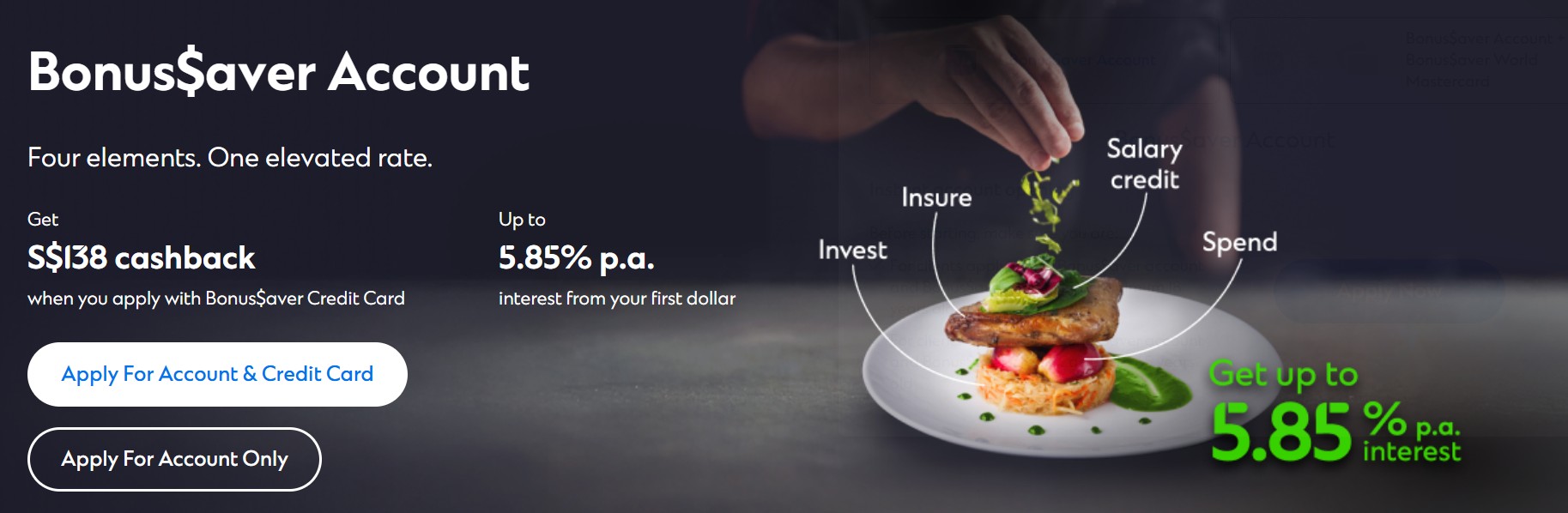

Standard Chartered Bonus Saver

Why we like it:

The Standard Chartered Bonus$aver Account stands out for its high headline rate, but it is not the simplest account to optimise.

It may be worth considering if you already plan to use Standard Chartered for card spend, salary crediting, investments or insurance.

However, I would be careful not to buy an investment or insurance product just to unlock a higher savings account rate.

The Standard Chartered Bonus$aver Account offers up to 5.85% p.a. on your first S$100,000 balance.

Unlike some other accounts, the same bonus rate applies across your eligible balance without complicated tiering, making it easier to estimate your potential returns.

To earn the highest rate, you’ll need to meet several conditions, including purchasing investment and insurance products.

However, even with just salary crediting of at least S$3,000 and S$1,000 card spend, you can unlock a rate of around 1.85% p.a.

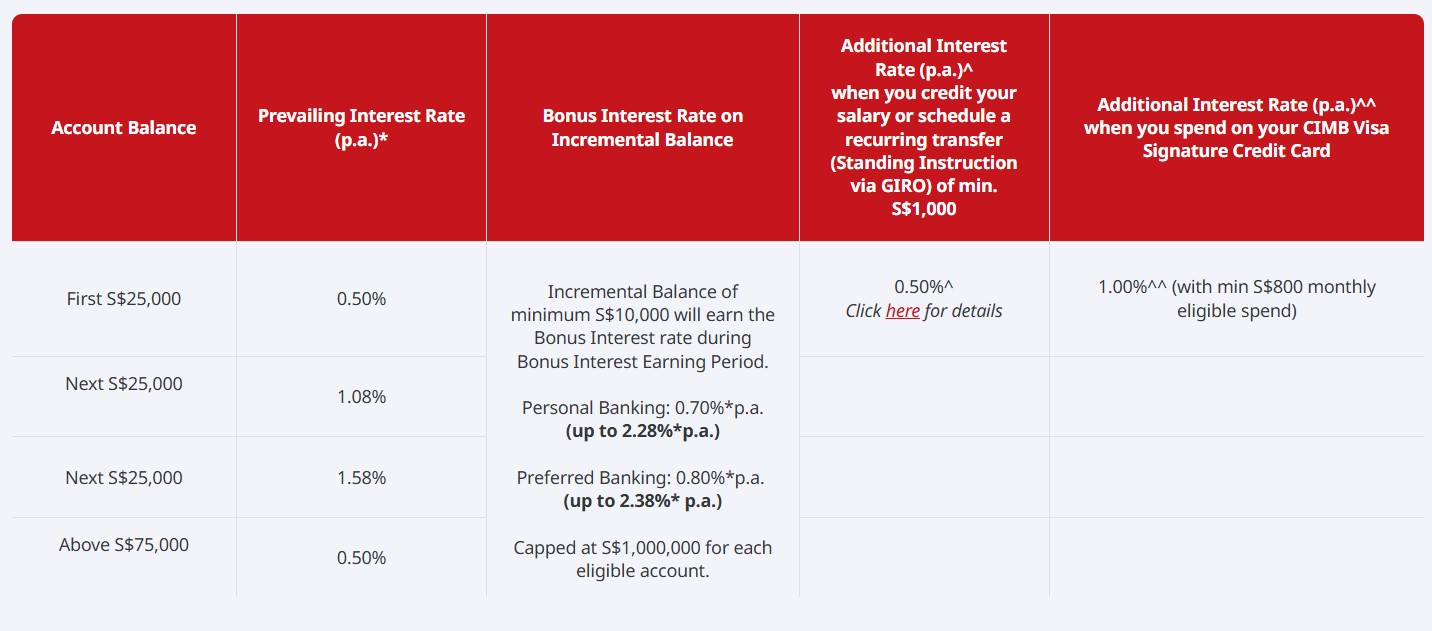

| Bonus interest component | Current Max EIR from 1 May 2026 |

|---|---|

| Card spend (minimum eligible spend of S$1,000 monthly) | 0.90% p.a. |

| Salary credit (regular inward credit through GIRO, PayNow or FAST) | 0.90% p.a. |

| Invest (invest in eligible Unit Trust or Online Equities of at least S$30,000; bonus interest paid for a consecutive period of 6 months) | 1.50% p.a. |

| Insure (bonus interest paid for a consecutive period of 6 months) | 2.50% p.a. |

| Prevailing interest rate | 0.05% p.a. |

| Total interest on your first S$100,000 eligible deposit balance | 5.85% p.a. |

There is a Bonus Saver sign-up promotion running from 1 July to 31 August 2026, where new customers can receive S$228 cashback when they apply for both a Bonus$aver account and a Bonus$aver World Mastercard Credit Card, as well as deposit and maintain at least S$50,000 in fresh funds.

Learn more about Standard Chartered Bonus Saver here.

CIMB FastSaver Account

Why we like it:

The CIMB FastSaver Account has become one of the more competitive options this month if you have fresh funds and can meet the salary or card spend requirements.

It may work best for savers who have spare cash outside CIMB, and are comfortable crediting salary or setting up a standing instruction of at least S$1,000 a month.

You will also need to spend at least S$800 a month on the CIMB Visa Signature card to maximise the bonus interest.

With the latest promotion, you can earn up to 2.70% p.a. on the first S$25,000 if all criteria are met.

For S$100,000 of eligible fresh funds, the effective interest rate works out to about 1.99% p.a. if you meet the fresh funds, salary or standing instruction, and card spend requirements.

However, the promotional rate needs to be understood carefully.

The fresh funds bonus applies only to eligible incremental balances compared with your 30 June 2026 balance, while the salary or standing instruction and card spend bonuses apply only on the first S$25,000.

This means CIMB FastSaver may work better as a stackable account for part of your savings, rather than a simple “park and forget” account.

Learn more about the CIMB FastSaver Account here.

UOB One Account

Why we like it:

The UOB One account is the flagship savings account of UOB which allows you to make minimal effort to earn the maximum interest rate possible.

The UOB One Account is useful for savers who want a relatively simple way to earn bonus interest without buying investment or insurance products.

It may work best if you already use UOB cards for everyday spending and can keep a larger balance of up to S$150,000 with the bank.

However, the effective return depends on your balance, as the highest rate is only reached at the upper deposit tiers.

The UOB One Account allows you to earn an effective interest rate of up to 1.90% p.a. on your first S$150,000.

To qualify, you need to spend a minimum of S$500 monthly on eligible UOB credit or debit cards and credit your salary of at least S$1,600 monthly.

You can also make use of the UOB Level Up Your Savings Promotion to earn up to S$800 guaranteed cash when you deposit fresh funds into your UOB One account.

Learn more about the UOB One Account here or sign up now to get started.

| Maximum effective interest rate for a saver who meets card spend of minimum $500 AND credit salary via GIRO of S$1,600 (p.a.) | |

| Account balance | Current Max EIR from 1 December 2025 |

| First $75,000 | 1.00% |

| $75,000 to $125,000 | 1.60% |

| $125,000 to $150,000 | 1.90% |

Maybank iSAVvy Savings Account

Why we like it:

The Maybank iSAVvy Savings Account is one of the more straightforward options if you have fresh funds to park and do not want to credit your salary or meet monthly card spend requirements.

It may work best for savers who have cash sitting outside Maybank and want to earn a promotional rate with fewer conditions.

From 1 July to 31 August 2026, Maybank iSAVvy offers up to 1.68% p.a. on eligible incremental balances when you top up at least S$20,000 in fresh funds.

However, the promotional rate applies only to the incremental average daily balance, not necessarily your entire account balance.

For example, if you already had S$20,000 in Maybank iSAVvy and top up another S$80,000, only the additional S$80,000 would qualify for the promotional rate. Assuming the original S$20,000 earns the base rate of 0.20% p.a., the blended interest rate across the full S$100,000 would work out to about 1.38% p.a.

Existing Maybank customers should check their reference balance, as only fresh funds above the reference balance may qualify.

For new Maybank customers, the promotion may be more straightforward, as the reference balance is treated as zero and eligible fresh funds could qualify for the promotional rate from the first S$20,000 of incremental ADB.

Learn more about the Maybank iSAVvy Savings Account here.

DBS Multiplier

Why we like it:

The DBS Multiplier Account is useful because it recognises a wider range of income and transaction types compared to some other savings accounts.

It may work well if you already use DBS or POSB for everyday banking, card spend, PayLah!, home loan, insurance or investments.

It is also worth highlighting for younger savers, as those aged 29 and below may have a separate pathway to earn bonus interest without regular income crediting.

The DBS Multiplier Account rewards users with up to 4.10% p.a. interest on the first S$100,000 in SGD balances, depending on their monthly banking activity.

It recognises a wide range of income types beyond just salaries, such as freelance and gig payments, as well as CPF contributions. This allows more people, including NSFs and retirees, to qualify for bonus interest.

To qualify for higher interest, users need to credit income and transact in one or more eligible categories such as credit card spending, PayLah! usage, home loan repayments, insurance, or investments.

You can also get up to S$588 in combined rewards when you credit your salary, pay your taxes via GIRO, open and contribute to a Supplementary Retirement Scheme (SRS) account, and sign up for the DBS yuu Card.

Learn more about how DBS Multiplier Account works and check out the latest promotions here.

Best savings account for S$100k of savings, salary credit, and credit card spend

If you have S$100,000 of fresh funds, can credit your salary or set up a monthly standing instruction, and spend at least S$800 a month on your credit card, CIMB FastSaver is one of the more competitive savings accounts to consider in July 2026.

With the latest fresh funds promotion, you can earn about 1.99% p.a. on S$100,000 if all criteria are met.

This puts CIMB FastSaver slightly ahead of OCBC 360, which offers up to 1.95% p.a. on the first S$100,000 when you meet the salary, save and spend criteria.

However, OCBC 360 remains a useful alternative if you prefer a more regular salary-crediting account and do not want to depend on a limited-time fresh funds promotion.

Standard Chartered BonusSaver is close behind at about 1.85% p.a. if you meet the salary credit and card spend requirements.

| Savings Account | Realistic interest rate (p.a.) |

| CIMB FastSaver (Personal banking) | 1.99% |

| OCBC 360 | 1.95% |

| Standard Chartered Bonus Saver | 1.85% |

| Maybank iSAVvy (fresh funds) | 1.68% |

| Bank of China Smart Saver | 1.60% |

| UOB Stash | 1.50% |

| HSBC Everyday Global Account (fresh funds) | 1.45% |

| UOB One | 1.375% |

| SingFinance GoSavers | 1.30% |

| Singapura Finance Vivid Savings Account | 1.28% |

| CIMB StarSaver (Personal banking) | 1.20% |

| Standard Chartered eSaver (fresh funds) | 1.20% |

| Hong Leong Finance Premium SAVER Account | 1.20% |

| GXS* (Saving Pockets) | 1.08% |

| Trust Bank | 1.00% |

| DBS Multiplier | 0.93% |

| MariBank | 0.88% |

| Standard Chartered JumpStart | 0.30% |

| Source: Various bank websites as of 2 July 2026. *Maximum deposit for GXS is S$95,000. | |

Best savings account for S$100k of savings without salary deposit and credit card spend

Maybank iSavvy offers up to 1.68% p.a. on eligible incremental balances from 1 July to 31 August 2026, when you top up at least S$20,000 in fresh funds. This makes it one of the more competitive options if your S$100,000 is currently sitting outside Maybank.

Alternatively, CIMB is running a limited-time 0.70% p.a. bonus on incremental fresh funds, if you increase your CIMB FastSaver balance by at least S$10,000. CIMB FastSaver offers about 1.62% p.a. on S$100,000 of eligible fresh funds without salary credit or card spend.

If you are able to credit your salary and meet the spending requirement, CIMB FastSaver can be worth a closer look, with up to 2.70% p.a. on the first S$25,000.

If you prefer something simpler without tracking fresh funds promotions, UOB Stash Account remains worth considering, with an effective interest rate of up to 1.50% p.a. on S$100,000.

You can also pair it with the UOB Level Up Your Savings Promotion, although the funds will be earmarked and cannot be withdrawn for about 7 months. If you deposit S$100,000 in new funds into an eligible UOB savings account, you can receive up to S$500 in guaranteed cash, although the deposited funds will be earmarked and cannot be withdrawn for about 7 months.

If you want other straightforward and simpler options, the SingFinance GoSavers Account offers 1.30% p.a. on the first S$100,000, while the Singapura Finance Vivid Savings Account offers 1.28% p.a. on balances from S$10,000.01 to S$200,000.00.

| Savings Account | Realistic interest rate (p.a.) |

| Maybank iSavvy (fresh funds) | 1.68% |

| CIMB FastSaver (Personal banking) | 1.62% |

| UOB Stash | 1.50% |

| HSBC Everyday Global Account (fresh funds) | 1.45% |

| SingFinance GoSavers | 1.30% |

| Singapura Finance Vivid Savings Account | 1.28% |

| Standard Chartered eSaver (fresh funds) | 1.20% |

| Hong Leong Finance Premium SAVER Account | 1.20% |

| CIMB StarSaver (Personal banking) | 1.20% |

| GXS Bank* (Saving Pockets) | 1.08% |

| MariBank | 0.88% |

| Trust Bank | 0.55% |

| Standard Chartered JumpStart | 0.30% |

| OCBC 360 | 0.05% |

| Bank of China SmartSaver | 0.10% |

| Standard Chartered Bonus Saver | 0.05% |

| DBS Multiplier | 0.05% |

| UOB One | 0.05% |

| Source: Company websites, Beansprout calculations as of 2 July 2026. *Maximum deposit for GXS is S$95,000. | |

Best savings account for S$75k of savings, salary credit, credit card spend, and investment/insurance products purchase

If you are also looking to buy an investment and/or insurance product with the bank in addition to depositing S$75,000 of savings, crediting your salary and spending on credit card, the good news is that you would be able to earn an even higher interest rate on your savings account!

The Standard Chartered Bonus Saver will offer you an interest rate of up to 5.85% p.a. on the first S$100,000. Even after the revision, it still offers the highest headline rate among the major savings accounts in this comparison, although it comes with higher qualifying hurdles.

This is followed by the Bank of China SmartSaver which offers up to 4.60% p.a. on the first S$100,000, while the OCBC 360 account currently offers up to 3.70% p.a. on the first S$75,000 for meeting the same criteria.

| Savings Account | Realistic interest rate (p.a.) |

| Standard Chartered Bonus Saver | 5.85% |

| Bank of China SmartSaver | 4.60% |

| OCBC 360 | 3.70% |

| DBS Multiplier | 2.40% |

| CIMB FastSaver | 1.99% |

| Maybank iSAVvy (incremental ADB) | 1.68% |

| HSBC Everyday Global Account (fresh funds) | 1.65% |

| Standard Chartered eSaver (fresh funds) | 1.60% |

| Trust Bank | 1.50% |

| UOB Stash | 1.34% |

| SingFinance GoSavers | 1.30% |

| Singapura Finance Vivid Savings Account | 1.28% |

| Hong Leong Finance Premium SAVER Account | 1.20% |

| CIMB StarSaver | 1.20% |

| GXS Bank* (Saving Pockets) | 1.08% |

| Standard Chartered JumpStart | 1.03% |

| UOB One | 1.00% |

| MariBank | 0.88% |

| Source: Company websites, Beansprout calculations as of 2 July 2026. *Maximum deposit for GXS is S$95,000. | |

What would Beansprout do?

I use savings accounts as one way to park my cash and ensure that I have enough set aside for emergencies and upcoming expenses.

With many savings accounts offering different interest rates and qualifying criteria, I would not just chase the highest headline rate. Instead, I would choose one, or a combination of accounts, based on the requirements I can realistically fulfil and how much cash I plan to keep in the account.

If I have S$150,000 of savings, can credit at least S$1,600 salary monthly, and spend S$500 on my credit card, I would consider the UOB One Account for its relatively straightforward two-step setup which offers me up to 1.90% p.a..

If I am considering either UOB Stash or UOB One, I would also participate in the UOB Level Up Your Savings Promotion, which offers up to S$800 in guaranteed cash for eligible fresh funds top-ups.

If I have around S$100,000 of fresh funds, can credit my salary or set up a monthly standing instruction, and spend at least S$800 a month on credit card, I would consider CIMB FastSaver.

With the latest fresh funds promotion, CIMB FastSaver offers up to 2.70% p.a. on the first S$25,000 if all criteria are met.

For S$100,000 of eligible fresh funds, the effective interest rate works out to about 1.99% p.a. This puts CIMB FastSaver slightly ahead of OCBC 360 Account, which offers up to 1.95% p.a. on the first S$100,000 when I meet the salary, save and spend criteria.

If I do not want to move my salary credit or commit to monthly card spend, I would look at Maybank iSavvy first. It offers up to 1.68% p.a. on eligible incremental balances from 1 July to 31 August 2026, when I top up at least S$20,000 in fresh funds.

If I prefer something simpler without tracking fresh funds promotions, I would still consider UOB Stash Account. It offers an effective interest rate of up to 1.50% p.a. on S$100,000 if I maintain or increase my monthly average balance. I would also participate in the UOB Level Up Your Savings Promotion.

If I want other straightforward alternatives with even fewer hoops, I would also consider SingFinance GoSavers as it offer up to 1.30% p.a., although it is lower than UOB Stash.

If I am a student, NSF or do not have regular income, I would also look at the DBS Multiplier Account if I am 29 years old and below. This is because users in this age group may earn 1.50% p.a. on the first S$50,000 with eligible credit card or PayLah! retail spend, even without income crediting.

If I am already planning to purchase an investment or insurance product with a bank, then I would explore accounts such as Standard Chartered Bonus Saver, OCBC 360 Account, or Bank of China SmartSaver. However, I would compare the requirements closely, as the qualifying criteria and interest rates differ across these accounts.

Finally, I would also think about safety and flexibility, not just yield. If scam-risk is a concern, it might be worthwhile considering a "money lock" account which allow you to only access your deposits in person.

Apart from savings accounts, I would also use a mix of fixed deposits, T-bills, Singapore Savings Bonds (SSBs) and money market funds for my pot of liquidity funds.

If you are open to having your money locked in, check out our guide to best fixed deposit rates in Singapore.

You can also find out more about Singapore T-bills and Singapore Savings Bonds here.

Once you have already set aside enough cash for your safety buffer and upcoming expenses, you may also want to explore how the Four Pots of Wealth framework can help you grow your wealth beyond savings accounts.

Curious how much your money could grow in the long run? Explore different scenarios with our compound interest calculator

Interested in the best promos this month? Check out other on-going deals happening right now.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

4 comments

- Kelvin Tan • 02 Jul 2026 12:40 AM

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20160.45%20160.45'%20style='enable-background:new%200%200%20160.45%20160.45;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%2300DBA4;}%20%3c/style%3e%3cg%3e%3cg%3e%3cpath%20class='st0'%20d='M80.23,0C35.99,0,0,35.99,0,80.23s35.99,80.23,80.23,80.23c44.24,0,80.23-35.99,80.23-80.23S124.46,0,80.23,0%20z%20M80.23,149.37c-1.73,0-3.45-0.09-5.15-0.21l0-38.76c-1.44-31.08,14.86-34.75,32.13-38.65c5.66-1.28,11.08-2.5,15.76-4.7%20c1.78,15.32-1.66,28.48-9.68,37.18c-0.11,0.11-10.83,10.24-23.27,10.24c-1.12,0-2.26-0.08-3.4-0.26l-1.72,10.94%20c1.73,0.27,3.44,0.4,5.11,0.4c16.97,0,30.39-12.77,31.2-13.57c11.35-12.3,15.63-30.42,12.07-51.01l-2.17-12.46l-10.42,7.15%20c-3.7,2.54-9.63,3.87-15.93,5.29c-16.97,3.82-42.62,9.6-40.75,49.71v36.77c-30.32-7.32-52.92-34.67-52.92-67.21%20c0-38.13,31.02-69.15,69.15-69.15c38.13,0,69.15,31.02,69.15,69.15S118.36,149.37,80.23,149.37z'/%3e%3cpath%20class='st0'%20d='M56.13,44.13c-3.86-0.87-7.5-1.69-9.57-3.11l-9.25-6.35l-1.92,11.06c-2.41,13.89,0.52,26.16,8.48,34.77%20c0.37,0.36,7.58,7.23,17.36,8.83c0.43-1.57,0.92-3.09,1.48-4.54c0.85-2.19,1.85-4.26,3-6.21c-7.3,0.3-13.91-5.81-13.92-5.81%20c0,0,0,0,0,0c-4.44-4.81-6.53-11.78-6.09-19.96c2.57,0.91,5.31,1.52,8.01,2.13c8.98,2.02,16.94,3.83,18.8,15.11%20c0.56-0.52,1.13-1.04,1.72-1.53c2.54-2.12,5.24-3.84,8-5.27C77.55,48.96,64.62,46.04,56.13,44.13z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Beansprout • 07 Jul 2026 03:42 AM

Beansprout • 07 Jul 2026 03:42 AM

- Singa • 12 Apr 2026 10:28 AM

- CIMB • 02 Jul 2025 07:49 AM

- Beansprout • 07 Jul 2026 04:07 AM

- James • 18 Apr 2025 03:28 AM

- Beansprout • 07 Jul 2026 03:45 AM