Standard Chartered JumpStart review: Up to 1.50% p.a. interest for students and young adults

Savings Account

By Beansprout • 05 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Standard Chartered Jumpstart now offers up to 1.50% p.a. on the first S$50,000. Learn about the eligibility, pros, cons, and interest rates of this entry level savings account.

What happened?

The Standard Chartered JumpStart Account interest rate has been revised.

The account now offers a base interest rate of 0.50% p.a. on the first S$50,000 of deposits.

You can earn an additional 1.00% p.a. step-up interest on deposit balances of up to S$50,000 when you invest with Standard Chartered.

This means the maximum interest rate on the JumpStart Account is now 1.50% p.a., down from 2.00% p.a. previously.

If you are a student or young adult between 18 and 26 years old looking for a simple savings account to park your spare cash, read on to find out how to earn a higher interest on the Standard Chartered JumpStart Account.

What is the Standard Chartered JumpStart Account?

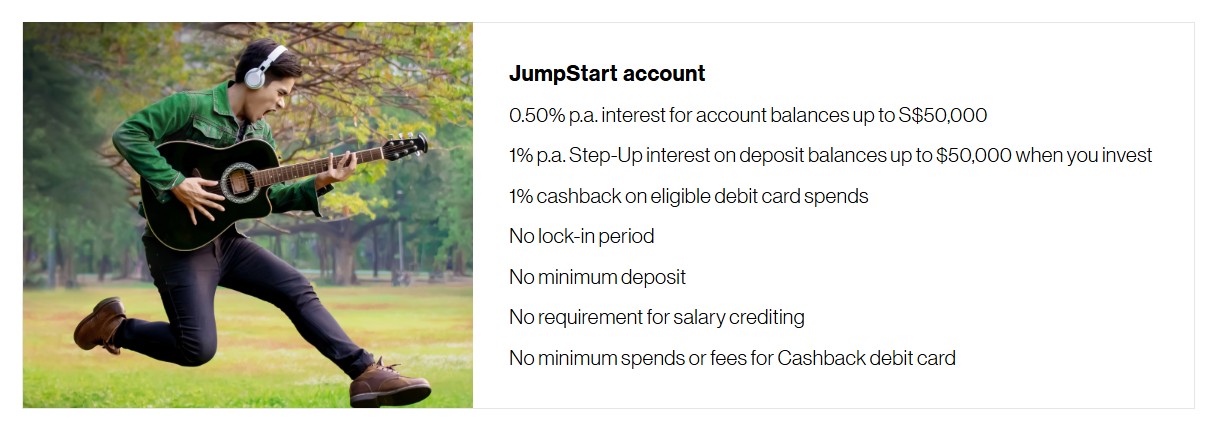

The Standard Chartered JumpStart Account is a fuss-free, high-interest-rate savings account for young individuals between the ages of 18 to 26 years old.

You can earn an interest rate of 0.50% p.a. on the first S$50,000 of balances. If you invest with StanChart, you will earn an additional step-up interest of 1.00% p.a., bringing the interest earned to 1.50% p.a.

There is also no lock-in period, no minimum deposit, no salary crediting requirement, and no minimum spend requirement to earn the base interest.

What is the interest rate for the Standard Chartered JumpStart Account?

The SC JumpStart account will give you an interest rate of 0.50% p.a. for the first S$50,000, and a step-up interest rate of 1.00% p.a. if you invest.

If you have more than S$50,000 in your account, you will earn an interest rate of 0.10% p.a. on incremental balances above S$50,000.

| Account balance | Base interest rate | Step-up interest when you invest | Maximum interest rate |

| First S$50,000 | 0.50% p.a. | 1.00% p.a. | 1.50% p.a. |

| Incremental balance above S$50,000 | 0.10% p.a. | Not applicable | 0.10% p.a. |

| Source: Standard Chartered, as of 5 May 2026 | |||

For example, if you have S$50,000 in the account, you would earn about S$250 in base interest over a year.

If you also qualify for the 1.00% p.a. step-up interest by investing with Standard Chartered, you would earn about S$750 in total interest over a year.

However, balances above S$50,000 will earn only 0.10% p.a.

This means the effective interest rate starts to fall once your account balance goes above S$50,000.

The following table summarises the maximum effective interest rate earned on the SC JumpStart Account over different deposit levels.

| Cash available for deposit | SC JumpStart effective interest rate (EIR) without investing with the bank (p.a.) | SC JumpStart effective interest rate (EIR) with an investment with the bank (p.a.) |

| First S$50,000 | 0.50% | 1.50% |

| S$60,000 | 0.43% | 1.27% |

| S$70,000 | 0.39% | 1.10% |

| S$80,000 | 0.35% | 0.98% |

| S$90,000 | 0.32% | 0.88% |

| S$100,000 | 0.30% | 0.80% |

| Source: Beansprout calculations, as of 5 May 2025 | ||

How to earn the 1.00% p.a. Step-up interest on the Standard Chartered JumpStart Account?

You do not need to make an investment to earn 0.50% p.a. on your first S$50,000 of deposits.

However, you can earn an additional step-up interest of 1.00% p.a. if you invest with the bank.

You can either invest in:

- Unit Trusts or Regular Savings Plan

- Equities through SC Online Trading

All you will need to do is to perform at least one buy transaction on the SC Online Trading platform, Online Unit Trust platform, or any bank branch every month to earn the highest interest rate of 1.50% p.a.

You can find out more by reading the T&Cs here.

What are the advantages of the Standard Chartered JumpStart Account?

The main advantage of the Standard Chartered JumpStart Account is that it remains simple to use.

This means you don’t have to make any minimum spend, invest with the bank, or credit your salary to be eligible for the base interest rate.

There is also no minimum deposit, no lock-in period, and no fall-below fee.

This may make it useful for students or young adults who want a first savings account without too many conditions.

You can earn the 0.50% p.a. interest rate while having the flexibility to access the funds anytime.

The SC JumpStart account also has a debit card that offers up to 1% cashback on eligible spend, capped at S$60 per month.

However, card spending is not required to earn the base interest on the account.

What are the disadvantages of the Standard Chartered JumpStart Account?

The main drawback is that the base interest rate has been reduced to 0.50% p.a. on the first S$50,000.

This makes the account less attractive than before for those who are looking purely for a high savings rate.

To earn the higher rate of 1.50% p.a., you would need to invest with Standard Chartered.

This may not be suitable for everyone, especially if you are still building your emergency fund or are not ready to take on investment risk.

Another limitation is the age restriction.

You need to be between 18 and 26 years old at the time of application to open a JumpStart Account.

Do I have to close my Standard Chartered JumpStart Account after I reach 26 years old?

No, you do not have to close your Standard Chartered JumpStart Account after you turn 26.

Standard Chartered states that there is no requirement to close the account when you turn 26, and you can continue to maintain the account beyond your 26th birthday.

However, you must be between 18 and 26 years old when you apply for the account.

How does the Standard Chartered JumpStart Account compare to UOB Stash and CIMB FastSaver?

The SC JumpStart is a no-frills account that allows you to earn a higher interest rate with very few additional requirements.

Let’s compare the SC JumpStart Account to other similar savings accounts, such as the UOB Stash and CIMB FastSaver accounts, assuming that you don't need to credit salary or spend on a card.

Based on the latest rates, the Standard Chartered JumpStart Account is simple, but its base interest rate is no longer the most competitive among fuss-free traditional bank accounts.

The UOB Stash Account may offer a higher effective interest rate if you are able to maintain or increase your account balance every month.

CIMB FastSaver Account may also offer a higher effective interest rate than JumpStart for balances above S$25,000, based on its prevailing tiered rates.

However, JumpStart still has one clear difference.

It is specifically designed for students and young adults between 18 and 26 years old, with no minimum deposit, no salary crediting requirement, no minimum card spend requirement, and a debit card that offers 1% cashback on eligible spend.

For students who are just starting to build their savings, the simplicity of JumpStart may still be useful.

But if you are focused mainly on earning a higher base interest rate on your cash, UOB Stash and CIMB FastSaver may be worth comparing as alternatives.

Total deposits | UOB Stash EIR (p.a.) | Standard Chartered JumpStart Account EIR (p.a.) | CIMB FastSaver Savings Account EIR (p.a.) | Winner |

| S$20,000 | 0.73% | 0.50% | 0.50% | UOB Stash |

| S$40,000 | 1.06% | 0.50% | 0.72% | UOB Stash |

| S$60,000 | 1.24% | 0.43% | 0.92% | UOB Stash |

| S$80,000 | 1.38% | 0.35% | 1.02% | UOB Stash |

| S$100,000 | 1.50% | 0.30% | 0.92% | UOB Stash |

| Source: Beansprout calculation, as of 5 May 2026, based on published rates from Standard Chartered, UOB and CIMB. | ||||

How does Standard Chartered JumpStart compare with digital bank savings accounts?

The other useful comparison is against digital bank savings accounts such as MariBank and GXS.

This may be especially relevant for students and young adults, since digital bank accounts are usually app-based, easy to open, and do not require salary crediting or card spend to earn their basic savings rates.

Here is how JumpStart compares with MariBank and GXS:

Account | Interest rate | Main conditions |

| Standard Chartered JumpStart | 0.50% p.a. on first S$50,000; up to 1.50% p.a. if you invest | Must be 18 to 26 years old to apply. Step-up interest requires investing |

| Mari Savings Account | 0.88% p.a. on all balances | No salary crediting, no minimum spend, no fall-below fee |

| GXS Savings Account | 0.88% p.a. on Main Account, 1.08% p.a. on Saving Pockets, and up to 1.40% p.a. on Boost Pockets | Higher Boost Pocket rate requires setting aside funds for selected tenures |

| Source: Beansprout calculation, as of 5 May 2026, based on published rates from Standard Chartered, GXS and MariBank. | ||

Compared with digital bank savings accounts, JumpStart’s base interest rate of 0.50% p.a. looks less attractive.

MariBank currently offers a flat 0.88% p.a. on the Mari Savings Account, without requiring salary crediting or card spend.

GXS offers 0.88% p.a. on its Main Account, 1.08% p.a. on Saving Pockets, and up to 1.40% p.a. on Boost Pockets if you are prepared to set aside your funds for selected tenures.

This means that for a student or young adult who simply wants a fuss-free place to park cash, MariBank and GXS may offer higher base rates than JumpStart.

That said, JumpStart may still appeal to those who prefer a traditional bank account, want a debit card with cashback, or are already using Standard Chartered’s banking ecosystem.

How to apply for the Standard Chartered JumpStart Account

To open an SC JumpStart account, you have to be aged between 18 to 26 years old (inclusive) at the point of application.

Step 1: Visit their application webpage.

Step 2: Choose to apply via Singpass (for Singapore citizens and PR) or Online Banking.

Alternatively, you can also choose to apply at their branches. To do this, you will require the below documents:

| Singapore citizens and permanent residents | Foreigners residing in Singapore |

|

|

What would Beansprout do?

The Standard Chartered JumpStart Account may still be worth considering for students and young adults who want a simple savings account with few conditions.

It offers a base interest rate of 0.50% p.a. on the first S$50,000, with no salary crediting or minimum card spend required.

You can earn a higher rate of up to 1.50% p.a. on the first S$50,000 if you invest with Standard Chartered.

However, I would not invest just to earn the additional step-up interest unless the investment itself fits my financial goals and risk appetite.

For students or young adults who are still building their first savings buffer, the priority may be to keep cash accessible and avoid taking on unnecessary investment risk.

To find out which savings account allows your money to work harder, check out our guide to the best savings account with highest interest rates in Singapore.

If you are deciding where to park your cash, you can also explore how the GXS Savings Account fits into your broader Liquidity Pot, alongside fixed deposits, T-bills, Singapore Savings Bonds and money market funds.

Once you have already set aside enough cash for your safety buffer and upcoming expenses, you may also want to explore how the Four Pots of Wealth framework can help you grow your wealth beyond savings accounts.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Questions and Answers

1 questions

- Kwan • 11 Nov 2024 09:17 AM

- JT • 28 Nov 2024 02:22 AM