UOB Stash Account: A simple way to grow your savings

Savings Account

By Beansprout • 01 Dec 2025

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

The UOB Stash Account now offers an interest rate of up to 1.50% p.a. Read our review to see how the new rates compare to GXS, MariBank, and more.

The UOB Stash Account currently offers an effective interest rate of up to 1.500% p.a. for deposits of S$100,000 with very few requirements to earn a higher interest rate.

Unlike typical high-yield savings accounts such as UOB One, OCBC 360, or DBS Multiplier, the UOB Stash Account functions more like a traditional savings account where you don’t need to meet multiple spending or income crediting criteria to earn bonus interest.

Whether you are a student, a retiree or simply looking for a fuss-free account to park your cash, the UOB Stash Account could be worth a closer look.

So read on to find out more about the UOB Stash Account.

What is the UOB Stash Account?

Effective 1 December 2025, the UOB Stash Account is a savings account that allows you to earn an effective interest rate of up to 1.50% p.a. on your deposits simply when you maintain or increase your balances.

Interest gets paid out monthly and there’s no lock-in period for your money!

What is the current interest rate for the UOB Stash Account?

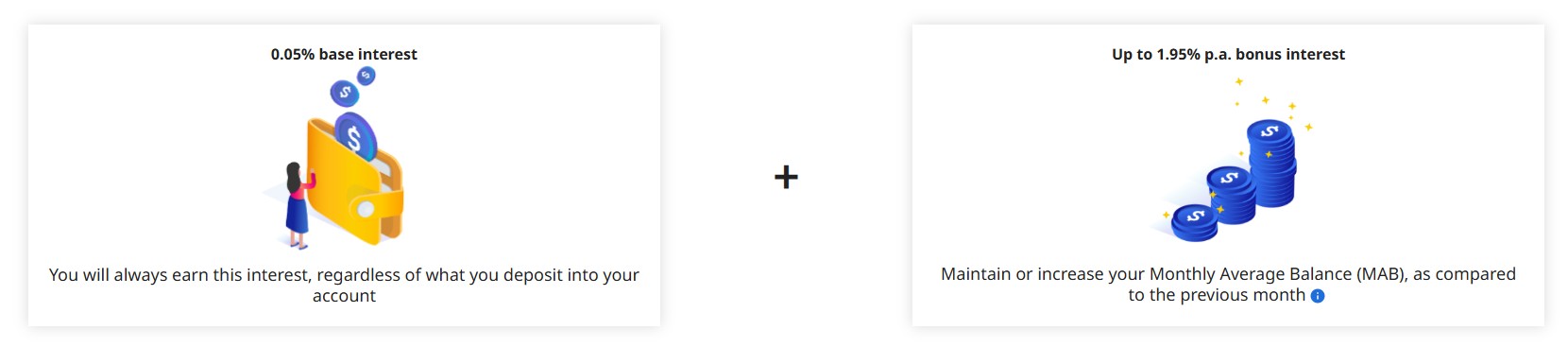

The UOB Stash Account offers a base interest rate of 0.05% p.a., and a bonus interest rate of up to 1.95% p.a.

Unlike other high-yield deposit accounts where you need to perform complicated steps, you will only need to do these to qualify for the bonus interest rate:

- Have more than S$10,000 in your monthly account balance and;

- Maintain or increase the account balance from last month’s balance.

Let me break it down and calculate the effective interest rate (EIR) in tiers for you!

If you have a monthly average balance of S$100,000 in the UOB Stash account, you will earn a total interest of about S$1,500 over one year.

Cash available for deposit | UOB Stash Account (p.a.) |

| First S$10,000 | 0.05% |

| More than S$10,000 Less than S$40,000 | Max EIR 1.027% |

| More than S$40,000 Less than S$70,000 | Max EIR 1.21% |

| More than S$70,000 Less than S$100,000 | Max EIR 1.50% |

| Source: UOB as of 1 December 2025 | |

Also, the UOB Stash Account does not require you to fulfill numerous requirements to receive the bonus interest rates.

There’s no need to spend a minimum amount on a credit card, make investment/insurance purchases or credit your salary.

Putting it simply, the key to unlocking the bonus interest of the UOB Stash account is to have an account balance that is similar or higher than the previous month - yay!

We do not need to constantly increase/top-up the account balance each month unless we want to!

Another advantage of the UOB Stash Account is that it is easy to qualify for opening an account. You can open an account if you are 15 years old and above.

The minimum balance for the UOB Stash Account is S$1,000.

If your monthly account balance falls below S$1,000, a S$2 fall-below fee will be imposed.

This is waived for the first six months for accounts opened online. Not bad huh?

Enjoy hassle-free savings growth without complex requirements. Open your UOB Stash Account today.

How does the UOB Stash Account compare to other deposit accounts?

As fellow Singaporeans, we always like to compare and make sure we get the best deal for ourselves. So here’s how the UOB Stash Account stacks up against other savings options with minimal requirements.

For now, the UOB Stash Account still offers a maximum effective interest rate of 1.50% p.a., making it one of the higher-yield choices for fuss-free savers.

However, its returns are now closer to other simple savings accounts in Singapore.

| Account | Key conditions | Max effective interest rate (p.a.) | Deposit limit |

|---|---|---|---|

| UOB Stash Account | Maintain or increase monthly average balance | 1.50% | Up to S$100,000 |

| GXS Boost Pocket | 3-month lock-in per pocket | 1.38% | Up to S$85,000 |

| Mari Savings Account | No conditions | 0.88% | Up to S$100,000 |

| Stanchart JumpStart Account | Aged 19 – 26 only | 1.00% | Up to S$50,000 |

| Source: Beansprout calculations as of 1 December 2025 | |||

With the 1 December 2025 revision, the UOB Stash Account still offers a better rate than other fuss-free savings accounts.

If you prefer to keep things simple without juggling multiple criteria, it remains a convenient option.

Looking for a straightforward way to grow your savings? Get started with the UOB Stash Account.

Combo hack Dynamic Duo: UOB One Account + UOB Stash Account!

Here’s one way to make your savings work harder by combining both the UOB One Account and the UOB Stash Account.

As mentioned in the previous section, the UOB Stash Account lets you earn up to 1.50% p.a.

If you keep S$150,000 in the UOB One Account and S$100,000 in the UOB Stash Account, you can still earn about S$4,350 in total annual interest under current rates.

That works out to an average return of roughly 1.74% p.a., higher than the best fixed deposit interest rate and the latest 6-month T-bill interest rate.

This combination is simple and convenient if you already bank with UOB. It also avoids locking in your funds.

Both accounts remain flexible choices for those who prefer to keep their savings liquid, but the overall return is now lower than before.

Is there any catch to the UOB Stash Account?

The main drawback of the UOB Stash Account would be the need to maintain or increase your account balance from that of the previous month to qualify for the bonus interest.

For example, if your monthly average balance falls to S$99,500 from S$100,000 the month before, the amount of interest you will earn for the month falls to the base interest rate of 0.05%.

Also, the first S$10,000 in the UOB Stash Account earns just a 0.05% interest rate. As your balance goes above S$100,000, it will revert to the base interest rate of only 0.05%.

The flip side of the liquidity offered by a deposit account is that the interest rates are subject to change, and you are not able to ‘lock-in’ the interest rates like for fixed deposits.

Are there any promotions for the UOB Stash Account?

Learn more about the UOB Level Up Your Savings Promotion here.

How to apply for the UOB Stash Account

To open a UOB Stash Account, follow these simple steps.

Step 1: Visit the UOB Stash account sign up form.

Step 2: Click on “Next”

Step 3: Apply with bank details or Singpass

Here’s a pro tip: You can even select to open the UOB One Account simultaneously if you don’t already have one!

Learn more about the UOB Stash Account here.

Final verdict on UOB Stash Account

The UOB Stash account currently offers an easy way to earn a higher effective interest rate of up to 1.50% p.a. on your deposit account without compromising on liquidity.

If you have a monthly average balance of S$100,000 in the UOB Stash account, you will earn a total interest of about S$1,500 over one year under the current rate structure.

By combining with the UOB Level Up Your Savings Promotion, you can get up to an additional S$500 cash credit when you top up S$100,000 new funds into your UOB Stash Account.

You don’t need a minimal credit card spend, or even need to credit your salary into the account.

All you need to do is to maintain or increase your account balance compared to the previous month.

If you’re already hitting the $150,000 limit on UOB One Account, you can also use the UOB Stash Account to earn a higher interest rate on your additional spare cash.

The account remains a good low-effort option for keeping funds liquid.

Check out our guide to the best savings account in Singapore to find out which savings account offers the highest interest rate.

If you would prefer to lock in interest rates for a longer period of time, find out which are the best fixed deposit interest rates currently.

This article contains affiliate links. Beansprout may receive a share of the revenue from your sign-ups to keep our site sustainable. You can view our editorial guidelines here.

Find out which savings account allows you to earn the highest interest rate on your savings.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Questions and Answers

3 questions

- Jonathan • 21 Jun 2025 09:41 AM

- junyuan • 07 Nov 2024 03:53 AM

- rk • 27 Nov 2024 07:11 AM

- Dan • 04 Oct 2024 06:40 AM

- faridah • 07 Nov 2024 03:56 AM