Best Fixed Deposit Rates in Singapore [August 2026]: Up to 1.65% p.a.

Savings

By Gerald Wong, CFA • 03 Aug 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Compare the best fixed deposit rates in Singapore for August 2026, including promotional rates of up to 1.65% p.a. from RHB, GXS, CIMB, HL Bank and more.

Fixed deposit rates in Singapore are rising.

This month, I noticed several banks and finance companies rolling out more competitive rates and limited-time promotions ahead of National Day.

The highest fixed deposit rate I found was offered by RHB at 1.65% p.a. for 12-months, with a minimum deposit of S$20,000.

For now, best fixed deposit rates are available if you can set aside your cash at least 6 months, with the highest rates available for 12 months.

I last updated this guide on 1 August 2026, after checking the latest fixed deposit promotions from major banks and finance companies in Singapore.

I’ve pulled together the best fixed deposit rates in Singapore this month, to help you compare the latest offers before deciding where to place your savings.

Do check back regularly as I’ll be refreshing the best fixed deposit rates weekly.

The best fixed deposit rate in Singapore (Last updated as of 1 August 2026)

- The best 3-month fixed deposit rate we found was 1.40% p.a. by HL Bank.

- The best 6-month fixed deposit rate we found was 1.60% p.a. offered by RHB.

- The best 9-month fixed deposit rate we found was 1.55% p.a. offered by Bank of China and CIMB.

- The best 12-month fixed deposit rate we found was 1.65% p.a. offered by RHB.

| Bank | Interest rate per annum | Tenure | Minimum amount |

| RHB | 1.65% (Branch Placement) | 12 months | S$20,000 |

| 1.60% (Branch Placement) | 6 months | S$20,000 | |

| 1.30% (Branch Placement) | 3 months | S$20,000 | |

| 1.55% (Mobile Banking) | 12 months | S$20,000 | |

| 1.50% (Mobile Banking) | 6 months | S$20,000 | |

| 1.30% (Mobile Banking) | 3 months | S$20,000 | |

| GXS | 1.60% (Boost Pocket) | 12 months | S$100 (max S$95,000) |

| 1.40% (Boost Pocket) | 4 months | S$100 (max S$95,000) | |

| 1.30% (Boost Pocket) | 8 month | S$100 (max S$95,000) | |

| 1.22% (Boost Pocket) | 3 month | S$100 (max S$95,000) | |

| CIMB | 1.55% | 12 months | S$10,000 |

| 1.55% | 9 months | S$10,000 | |

| 1.50% | 6 months | S$10,000 | |

| 1.35% | 3 months | S$10,000 | |

| HL Bank | 1.50% (HLB Connect) | 12 months | S$10,000 |

| 1.55% (HLB Connect) | 6 months | S$10,000 | |

| 1.40% (HLB Connect) | 3 months | S$10,000 | |

| Bank of China | 1.55% (mobile banking) | 6/9/12 months | S$200,000 |

| 1.50% (mobile banking) | 6/9/12 months | S$500 | |

| 1.35% (mobile banking) | 3 months | S$500 | |

| SingFinance | 1.55% (fresh fund) | 6/12/18 months | S$61,000 |

| SBI | 1.50% | 6 months | S$50,000 |

| 1.40% | 12 months | S$50,000 | |

| Maybank | 1.50% (Deposits Bundle Promo at branches and online)^ | 12 months | S$20,000 |

| 1.45% (online banking) | 6/12 months | S$20,000 | |

| 1.32% (Deposits Bundle Promo at branches and online)^ | 9 months | S$20,000 | |

| 1.30% (online banking) | 9 months | S$20,000 | |

| Singapura Finance | 1.50% (Blue Sky FD Promo) | 6 months | S$61,000 |

| 1.48% (Vivid Fixed Deposit) | 12/13 months | S$50,000 | |

| 1.45% (Vivid Fixed Deposit) | 9 months | S$50,000 | |

| 1.45% (Counter FD Promo) | 7 months | S$20,000 and above | |

| 1.42% (Counter FD Promo) | 6 months | S$20,000 and above | |

| Hong Leong Finance | 1.50% (online banking) | 4/5 months | S$10,000 and above |

| 1.45% (online banking) | 12 months | S$20,000 and above | |

| 1.40% (online banking) | 12 months | S$5,000 to < S$20,000 | |

| 1.40% (online banking) | 9 months | S$20,000 and above | |

| 1.35% (online banking) | 9 months | S$5,000 to < S$20,000 | |

| 1.35% (online banking) | 6 months | S$20,000 and above | |

| 1.30% (online banking) | 6 months | S$5,000 to < S$20,000 | |

| ICBC | 1.45% (E-banking) | 12 months | S$20K and above |

| 1.15% (E-banking) | 12 months | S$500 and above | |

| 1.45% (E-banking) | 9 months | S$20K and above | |

| 1.10% (E-banking) | 9 months | S$500 and above | |

| 1.50% (E-banking) | 6 months | S$20K and above | |

| 1.30% (E-banking) | 6 months | S$500 to < S$20K | |

| 1.30% (E-banking) | 3 months | S$20K and above | |

| 1.25% (E-banking) | 3 months | S$500 to < S$20K | |

| MariBank | 1.30% | 12 months | S$100 (max S$100,000) |

| 1.20% | 6 months | S$100 (max S$100,000) | |

| 1.10% | 3 months | S$100 (max S$100,000) | |

| Citibank | 2.00% (Citigold, new funds) | 6 months | S$10K to S$10M |

| 1.40% (Citigold, new funds) | 3 months | S$10K to S$10M | |

| 0.70% | 12 months | S$10,000 | |

| 0.60% | 6 months | S$10,000 | |

| Standard Chartered | 1.30% (Fresh Fund Promo) | 6 months | S$25,000 (fresh funds) |

| UOB | 1.30% | 12 months | S$10,000 (fresh funds) |

| 1.25% | 10 months | S$10,000 (fresh funds) | |

| 1.20% | 6 months | S$10,000 (fresh funds) | |

| OCBC | 1.25% (online banking) | 6 months | S$20,000 |

| 1.30% (online banking) | 12 months | S$20,000 | |

| 1.30% (online banking) | 18 months | S$20,000 | |

| HSBC | 1.05% | 3 months | S$30,000 |

| 0.85% | 6 months | S$30,000 | |

| 0.90% | 9 months | S$30,000 | |

| 0.95% | 12 months | S$30,000 | |

| DBS/POSB | 1.00% | 9/12 months | S$1,000 (max S$19,999) |

| 0.80% | 6 months | S$1,000 (max S$19,999) | |

| Source: Various bank websites as of 1 August 2026 ^Maybank Deposits Bundle Promo: Based on a blended rate for S$10,000 Time Deposit with 10% of the time deposit amount earmarked in a Maybank savings account earning a base rate of 0.05% p.a. | |||

[Beansprout Exclusive Promotion] Get a free S$100 Fairprice voucher within 5 working days when you sign up for a Longbridge account via Beansprout. Promo ends on 31 August 2026. Learn more about the Longbridge promo here.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

What are the fixed deposit rates offered by banks in Singapore?

🌱 RHB fixed deposit rates

| Tenure | Personal Banking mobile placement | Premier Banking mobile placement | Personal Banking branch placement | Premier Banking branch placement |

| 3 months | 1.30% p.a. | 1.40% p.a. | 1.30% p.a. | 1.40% p.a. |

| 6 months | 1.50% p.a. | 1.60% p.a. | 1.60% p.a. | 1.70% p.a. |

| 12 months | 1.55% p.a. | 1.65% p.a. | 1.65% p.a. | 1.75% p.a. |

| Source: RHB website as of 1 August 2026 | ||||

RHB Personal Banking customers can earn 1.30% p.a. for a 3-month fixed deposit through either mobile banking or a branch.

For the longer tenures, the rates are higher when the placement is made at a branch. RHB offers Personal Banking customers 1.60% p.a. for six months and 1.65% p.a. for 12 months at a branch, compared with 1.50% p.a. and 1.55% p.a. respectively through mobile banking.

RHB Premier Banking customers can earn an additional 0.10 percentage points across all tenures. The highest rate is 1.75% p.a. for a 12-month fixed deposit placed at a branch.

The minimum placement amount for the promotional rates is S$20,000.

However, do note that the fixed deposit rates offered by RHB are promotional rates that are subject to change without prior notice.

You can find out the latest fixed deposit rate offered by RHB here.

🌱 GXS Boost Pocket rates

| Tenor | Base Interest Rate( p.a.) | Bonus Interest (p.a.) | Total interest rate (p.a. |

| 1 month | 0.88% | 0.13% | 1.01% |

| 3 months | 0.34% | 1.22% | |

| 4 months | 0.52% | 1.40% | |

| 8 months | 0.42% | 1.30% | |

| 12 months | 0.72% | 1.60% | |

| Source: GXS website as of 1 August 2026 | |||

GXS Bank’s Boost Pocket offers a base interest rate of 0.88% p.a., credited daily, with optional bonus interest if you hold your funds to maturity.

Depending on the tenure selected, you can earn up to an additional 0.52% p.a., bringing the total return to:

- 1.01% p.a. for the 1-month tenure

- 1.22% p.a. for the 3-month tenure

- 1.30% p.a. for the 8-month tenure

- 1.40% p.a. for the 4-month tenures

- 1.60% p.a. for the 12-month tenures

There is no penalty for early withdrawal, and you’ll still receive the base interest of 0.88% p.a. up to the date you withdraw.

Find out more about GXS Savings Account here.

🌱 CIMB fixed deposit rates

| Tenure | Personal Banking | Preferred Banking |

| Interest rate per annum (%) | Interest rate per annum (%) | |

| 3 Months | 1.35 | 1.40 |

| 6 Months | 1.50 | 1.55 |

| 9 Months | 1.55 | 1.60 |

| 12 Months | 1.55 | 1.60 |

| Source: CIMB website as of 1 August 2026 | ||

CIMB is offering a 9-month and 12-month fixed deposit rate of 1.55% p.a. for Personal Banking customers, which is the highest rate currently available for CIMB online placements. For Preferred Banking customers, the highest rate is 1.60% p.a. on the 9-month and 12-month tenure.

For a shorter placement, the 6-month fixed deposit rate is 1.50% p.a. for Personal Banking customers and 1.55% p.a. for Preferred Banking customers.

The 3-month fixed deposit rate is 1.35% p.a. for Personal Banking customers and 1.40% p.a. for Preferred Banking customers.

To earn the promotional interest rate, the minimum deposit required is S$10,000. You can find out more here.

🌱 HL Bank fixed deposit rates

| Fixed deposit tenure | Promotional interest rate | Minimum placement |

| 3 months | 1.40% p.a. | S$10,000 |

| 6 months | 1.55% p.a. | S$10,000 |

| 9 months | 1.50% p.a. | S$10,000 |

| Source: HL Bank website as of 1 August 2026. | ||

HL Bank is offering promotional fixed deposit rates of up to 1.55% p.a. for placements made online through HLB Connect.

You can earn 1.40% p.a. for a 3-month fixed deposit, 1.55% p.a. for six months and 1.50% p.a. for nine months. The minimum placement amount is S$10,000.

The highest rate is available for the 6-month tenure, which may be worth considering if you are looking for a relatively short fixed deposit period.

To make a placement, you will need to transfer the funds into your HL Bank account and place the fixed deposit through HLB Connect Online. New customers can first open an HL Bank iSavings Account online before making their placement.

HL Bank adjusts its fixed deposit rate fairly regularly and may offer promotional rates from time to time, you can find out the latest fixed deposit rate offered by HL Bank here.

🌱 Bank of China fixed deposit rates

| Via Mobile Banking Placement (new placement) (Min S$200,000) | Via Mobile Banking Placement (new placement) (Min S$500) | |

| Tenor | Interest rate per annum (%) | Interest rate per annum (%) |

| 3 months | - | 1.35 |

| 6 months | 1.55 | 1.50 |

| 9 months | 1.55 | 1.50 |

| 12 months | 1.55 | 1.50 |

| Source: Bank of China website as of 1 August 2026. | ||

Bank of China is currently offering SGD fixed deposit promotional rates from 1.10% p.a. to 1.55% p.a. for new placements made via the BOC Mobile Banking app.

If I have at least S$500 to set aside, I can earn 1.35% p.a. for 3 months, or 1.50% p.a. for 6, 9 or 12 months.

A higher rate of 1.55% p.a. is available for 6, 9 and 12 months, although this requires a much larger minimum placement of S$200,000.

To earn any promotional fixed deposit rate, you will need to make a new placement with the bank.

The Bank of China adjusts its fixed deposit rate fairly regularly and may offer promotional rates from time to time, you can find out the latest fixed deposit rate offered by Bank of China here.

🌱 SBI fixed deposit rates

| Tenor | Promotional Interest Rate (p.a) | Minimum Deposit |

| 6 months | 1.50% | S$50,000 |

| 12 months | 1.40% | S$50,000 |

| Source: SBI website as of 1 August 2026 | ||

SBI is offering a promotional rate of 1.50% p.a. for a 6-month fixed deposit and 1.40% p.a. for a 12-month fixed deposit, respectively.

The minimum deposit required to earn the higher promotional rate is S$50,000, and the promotion applies to new SGD fixed deposits.

You can find the latest fixed deposit rates offered by SBI here and their latest promotional fixed deposit rates here.

🌱 Maybank fixed deposit rates

| Tenure | iSAVvy Promotional Rate (p.a.) |

| 12-month | 1.50% (Via Deposits Bundle Promotion^) |

| 9-month | 1.32% (Via Deposits Bundle Promotion^) |

| 12-month | 1.45% |

| 9-month | 1.30% |

| 6-month | 1.45% |

| Source: Maybank website as of as of 1 August 2026 ^Effective Rate | |

Maybank is currently offering a standalone interest rate of 1.45% p.a. on its 6-month and 12-month Singapore Dollar Time Deposit / Term Deposit-i promotion, with a minimum placement of S$20,000. This is available at branches and online.

For those who are willing to bundle their fixed deposit with funds in a Maybank savings or current account, Maybank is offering a higher promotional rate of 1.45%p.a. and 1.65% p.a. for its 9-month and 12-month Deposits Bundle Promotion respectively. This works out to an effective rate of 1.32% p.a. and 1.50% p.a for the respective period.

To access the bundle promotional rates, you will need to place fresh funds into a Time Deposit and a Maybank savings or current account at a 1:10 ratio. This means that for every S$10,000 placed in the Time Deposit, S$1,000 has to be earmarked in a savings or current account for the same tenure as the Time Deposit.

Because the savings or current account portion earns a lower base interest rate, the combined effective return is lower than the headline fixed deposit rate.

You can find out the full terms and conditions of the Maybank fixed deposit promotion here.

🌱 Singapura Finance fixed deposit rates

| Product | Tenure | Interest rate (p.a.) | Minimum deposit |

|---|---|---|---|

| Blue Sky Fixed Deposit (National Day Promotion) | 6 months | 1.50% | S$61,000 |

| Vivid Fixed Deposit | 12/13 months | 1.48% | S$50,000 |

| 9 months | 1.45% | S$50,000 | |

| Counter Fixed Deposit Promotion | 7 months | 1.45% | S$20,000 |

| 6 months | 1.42% | S$20,000 | |

| Source: Singapura Finance website as of 1 August 2026 | |||

Singapura Finance is offering a limited-time National Day promotional fixed deposit rate of 1.50% p.a. for a 6-month tenure.

To receive this rate, you will need to place at least S$61,000 in fresh funds in a Blue Sky Fixed Deposit at one of Singapura Finance’s Customer Centres. The promotion is available to new and existing customers from 31 July to 8 August 2026. You will also need an existing savings account with Singapura Finance or open one with a minimum deposit of S$200.

For a lower minimum placement, the Counter Fixed Deposit Promotion offers 1.42% p.a. for six months and 1.45% p.a. for seven months, with a minimum deposit of S$20,000 in fresh funds.

If you prefer placing your deposit digitally, the Vivid Fixed Deposit offers 1.45% p.a. for nine months and 1.48% p.a. for 12 or 13 months. The minimum deposit is S$50,000.

The Vivid Fixed Deposit is available to Singaporeans and Permanent Residents aged 16 and above with an active Vivid Savings Account. For the National Day and Counter Fixed Deposit promotions, no interest will be paid if the fixed deposit is withdrawn before maturity.

You can find out more about the Singapura Finance Fixed Deposit Promo here and the Singapura Finance National Day Promotion 2026 here.

🌱 ICBC fixed deposit rates

| Via E-banking | Via E-banking | |

| S$500 to S$19,999 | S$20,000 to S$200,000 | |

| Tenor | Promotion Rates per annum | Promotion Rates per annum |

| 1 month | 1.05% | 1.10% |

| 3 months | 1.25% | 1.30% |

| 6 months | 1.30% | 1.50% |

| 9 months | 1.10% | 1.45% |

| 1 year | 1.15% | 1.45% |

| Source: ICBC website as of 1 August 2026 | ||

ICBC is currently offering SGD fixed deposit promotional rates from 1.05% p.a. to 1.45% p.a., with the latest rates effective from 1 July 2026.

For e-banking placements, the minimum deposit is S$500. Savers can earn 1.25% p.a. for a 3-month tenure and 1.30% p.a. for a 6-month tenure.

For larger deposits of S$20,000 and above, the 3-month rate rises to 1.30% p.a., while the -month and 12-month rate rises to 1.45% p.a.

The highest promotional rate of 1.50% p.a. is available for placements of at least S$20,000 for 6-month.

The promotional rate is only applicable via online banking deposits.

ICBC adjusts its fixed deposit rate fairly regularly, and you can find out the latest fixed deposit rate offered by ICBC here.

🌱 Hong Leong Finance fixed deposit rates

| Product | Tenure | Interest rate (p.a.) | Minimum deposit |

| Special Fixed Deposit Promotion | 4 or 5 months | 1.50% | S$10,000 |

| Online Fixed Deposit Special | 6 months | 1.30% | S$5,000 to < S$20,000 |

| Online Fixed Deposit Special | 6 months | 1.35% | S$20,000 and above |

| Online Fixed Deposit Special | 9 months | 1.35% | S$5,000 to < S$20,000 |

| Online Fixed Deposit Special | 9 months | 1.40% | S$20,000 and above |

| Online Fixed Deposit Special | 12 months | 1.40% | S$5,000 to < S$20,000 |

| Online Fixed Deposit Special | 12 months | 1.45% | S$20,000 and above |

| Source: Hong Leong Finance website as of 1 August 2026. | |||

Hong Leong Finance is offering its highest promotional fixed deposit rate of 1.50% p.a. for a 4-month or 5-month tenure. The minimum placement is S$10,000 in fresh funds, and you will need to be an HLF Digital user to qualify.

For placements made online through HLF Digital, you can earn up to 1.45% p.a. under the Online Fixed Deposit Special. This is available to existing customers with both a Hong Leong Finance fixed deposit account and savings account.

For deposits of S$5,000 to below S$20,000, the promotional rate is 1.30% p.a. for 6 months, 1.35% p.a. for 9 months and 1.40% p.a. for 12 months.

For deposits of S$20,000 and above, you can earn 1.35% p.a. for six months, 1.40% p.a. for nine months and 1.45% p.a. for 12 months.

Do note that no interest will be paid if the fixed deposit is withdrawn before maturity. Upon maturity, the deposit will be automatically renewed at the prevailing board or special rate.

Hong Leong Finance adjusts its fixed deposit rate fairly regularly, and you can find out the latest fixed deposit rate offered by Hong Leong Finance here.

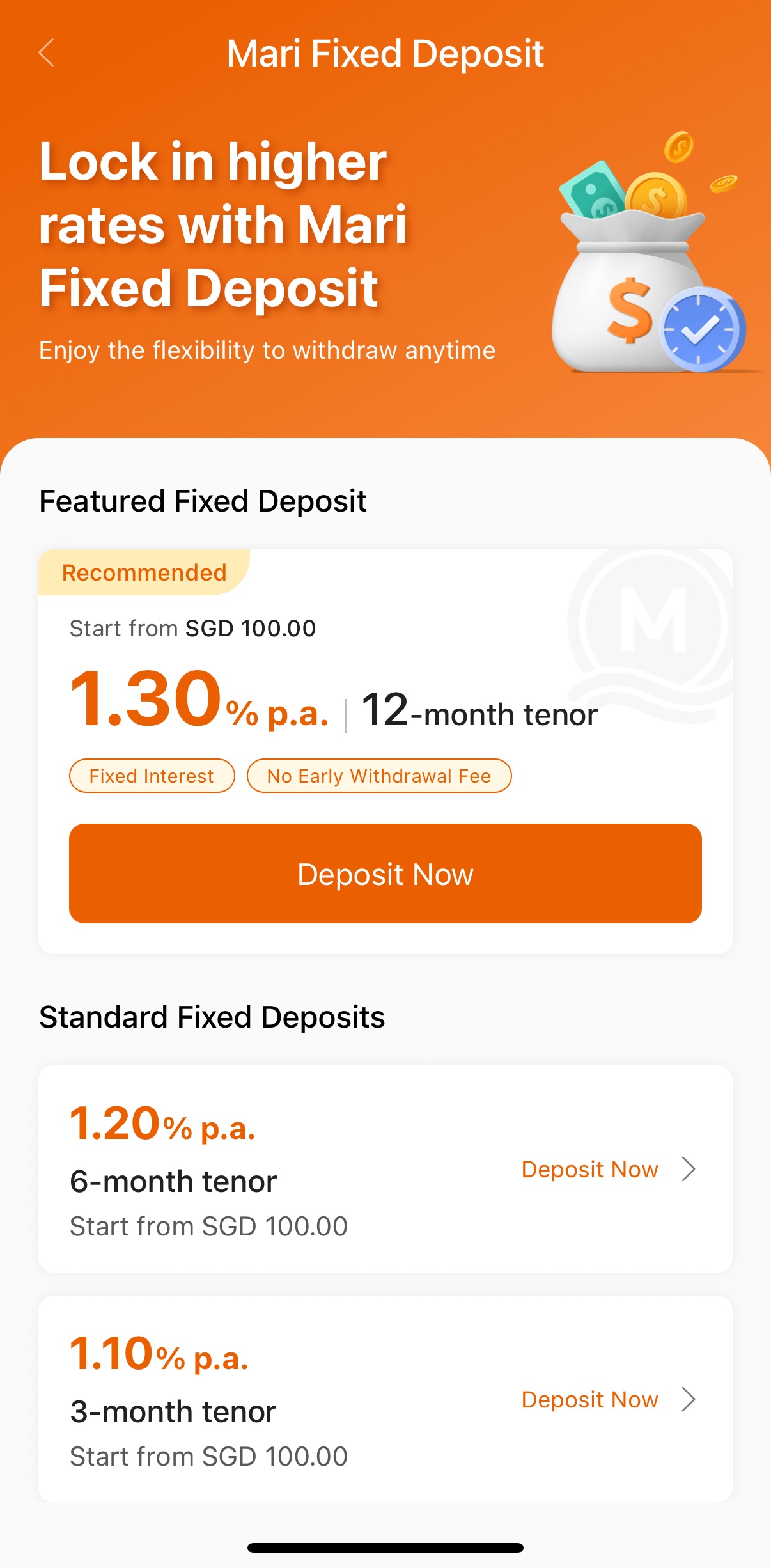

🌱 MariBank fixed deposit rates

MariBank is currently offering fixed deposit rates of 1.30% p.a. for 12 months and 1.20% p.a. for 6 months, with placements starting from as little as S$100.

Do note that the maximum amount of deposit you can maintain in your Mari Savings Account, which includes any Fixed Deposits would be S$100,000.

This means if you have deposited S$5,000 in your Mari Savings Account, the maximum amount you can hold across all your Mari Fixed Deposits is S$95,000.

Be sure to check your MariBank app for the latest fixed deposit rates that apply to your account.

Find out more about MariBank Savings Account here.

🌱 UOB fixed deposit rates

| Tenure | Promotional | Promotional | Minimum amount |

| 6-month | 1.20% | 1.25% | S$10,000 (fresh funds) |

| 10-month | 1.25% | 1.30% | |

| 12-month | 1.30% | 1.35% | |

| Source: UOB website as of 1 August 2026 | |||

UOB is currently offering Singapore Dollar fixed deposit promotional rates of up to 1.30% p.a. for customers placing fresh funds of at least S$10,000.

Customers without wealth products can earn 1.20% p.a. for a 6-month fixed deposit, 1.25% p.a. for a 10-month fixed deposit, and 1.30% p.a. for a 12-month fixed deposit.

Customers with selected UOB wealth products may receive higher promotional rates of up to 1.35% p.a.

You can find the latest fixed deposit rate offered by UOB here.

The fixed deposit rate of 1.15% p.a. is still lower than the highest effective interest rate that can be earned on the UOB One account.

🌱 OCBC fixed deposit rates

| Tenure | Banking type | Promotional Interest rate (p.a.) |

| 6 month | Branch | 1.20% |

| 12 month | 1.25% | |

| 18 month | 1.25% | |

| 6 month | Online | 1.25% |

| 12 month | 1.30% | |

| 18 month | 1.30% | |

| Source: OCBC website as of 1 August 2026 | ||

OCBC is now offering a promotional interest rate of 1.25% p.a. and 1.30% p.a. for a 6-month and 12-month fixed deposit respectively for internet banking customers.

You will need to place a minimum of S$20,000.

You can find the terms and conditions of the OCBC fixed deposit here.

🌱 Standard Chartered fixed deposit rates

| Tenure | Promotional personal banking rate | Promotional priority banking rate | Minimum Placement Amount (Fresh Funds in SGD) |

| 6 months | 1.30% p.a. | 1.40% p.a. | S$25,000 |

| Source: Standard Chartered website as of 28 July 2026 | |||

Standard Chartered Fresh Funds Time Deposit Promotion is on-going from 1 July 2026 to 28 July 2026.

For a 6-month time deposit, Standard Chartered is currently offering a rate of 1.30% p.a. for Personal Banking customers with a minimum placement of S$25,000.

Priority Banking customers can enjoy a higher rate of 1.40% p.a. for the same 6-month tenure.

You can find the latest promotional fixed deposit rates offered by Standard Chartered here.

🌱 DBS fixed deposit rates

| Interest rate per annum (%) | |||||||

| Tenure | S$1,000 - S$9,999 | S$10,000 - S$19,999 | S$20,000 - S$49,999 | S$50,000 - S$99,999 | S$100,000 - S$249,999 | S$250,000 - S$499,999 | S$500,000 - S$999,999 |

| 1 mth | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 2 mths | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 3 mths | 0.1500 | 0.1500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 4 mths | 0.2500 | 0.2500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 5 mths | 0.4000 | 0.4000 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 6 mths | 0.8000 | 0.8000 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 7 mths | 0.9500 | 0.9500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 8 mths | 1.0000 | 1.0000 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 9 mths | 1.0000 | 1.0000 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 10 mths | 1.0000 | 1.0000 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 11 mths | 1.0000 | 1.0000 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| 12 mths | 1.0000 | 1.0000 | 0.0500 | 0.0500 | 0.0500 | 0.0500 | 0.0500 |

| Source: DBS website as of 1 August 2026 | |||||||

You can earn an interest rate of 0.80% p.a. for a 6-month fixed deposit and 1.00% p.a for a 9-month and 12-month fixed deposit with a maximum deposit amount of S$19,999.

I also noticed some sharing in the Beansprout community about the senior citizen fixed deposit rate offered by DBS.

If you are 55 years and above, you can earn an additional 0.10% p.a. interest on your fixed deposit for tenors of at least six months with the Premier Income Account (PIA), and a minimum deposit of S$10,000 per placement.

This means that you can get a 12-month fixed deposit rate of 1.10% p.a. instead of 1.00% p.a. for deposits of S$10,000 to S$19,999 with DBS.

Unlike other banks, DBS offers a higher fixed deposit interest rate for smaller deposit amounts.

For example, the interest rate you would earn falls to just 0.05% p.a. for deposits of S$20,000 and above.

You can find the latest fixed deposit rate offered by DBS here.

🌱 HSBC fixed deposit rates

| Types of customers | Tenure | Interest rate per annum |

| Personal banking | 3 month | 1.05% |

| 6 month | 0.85% | |

| 9 month | 0.90% | |

| 12 month | 0.95% | |

| Source: HSBC website as of 1 August 2026 | ||

HSBC is offering a 1.05% p.a. fixed deposit rate with a minimum deposit of S$30,000 for personal banking customers for 3-month.

You may get the HSBC promotional fixed deposit rate at 0.85% p.a., 0.90% p.a., and 0.95% p.a. for longer tenures of 6-, 9- and 12- months respectively.

You can find out more about the fixed deposit rate offered by HSBC here.

🌱 Citibank fixed deposit rates

| Tenure | Board Rate (p.a.) |

| 3 months | 0.60% |

| 6 months | 0.60% |

| 12 months | 0.70% |

| Source: Citi website as of 1 August 2026 | |

Citibank is now offering a fixed deposit rate of 0.60% p.a. for 3-month. The minimum deposit required is S$10,000, up to a maximum of S$3 million.

If you are a Citigold client, you may be able to earn up to 1.40% p.a. for a 3-month tenure and 2.00% for a 6-month tenure with new funds. The minimum deposit required is S$10,000, up to a maximum of S$10 million.

You can find the latest fixed deposit rates offered by Citi here.

What are fixed deposits?

Fixed deposits earn you a guaranteed amount of interest for the money you put in over a specific period of time.

Typically, you will lock in a sum of money (usually a minimum of $10,000) and the bank will pay you interest after a fixed period.

The downside to a fixed deposit is that you will have to pay a penalty fee if you want to withdraw your money early.

Hence, Fixed deposits tend to work best as part of your Liquidity Pot, especially for money you do not need for the next few months.

How do fixed deposit accounts compare to best savings accounts?

As seen from the Telegram group, many people are also interested in the best savings accounts apart from fixed deposit accounts.

However, do note that the interest rates offered by savings accounts are subject to change, and you are not able to ‘lock-in’ the interest rates like for fixed deposits.

The highest maximum effective interest rate offered by savings accounts currently is 5.85% p.a., above the best fixed deposit rate.

Check out the best savings accounts with the highest interest rates here.

How do fixed deposit rates compare to Singapore T-bill?

Beansprout has written enough on the Singapore treasury bill (T-bill) , so I will not be going into too much detail on them.

The yield for the most recent 6-month Singapore T-bill auction was 1.59% is lower than with the 6-month promotional fixed deposit rate of 1.60% p.a. offered by RHB.

What is also important to note is that fixed deposits are covered under the Deposit Insurance Scheme.

This means that in the event that the bank faces problems repaying your money, all your insured deposits will be insured up to S$100,000 by the Singapore Deposit Insurance Corporation Limited (SDIC).

The Singapore T-bill is backed by the Singapore Government, but this does not make them entirely risk free.

For example, you may lose part of your capital if you decide to sell your T-bill before six months. In this case, it might not just be the interest rates you are losing out on!

I have summarised my thoughts comparing fixed deposit rates with the Singapore T-bills below.

Learn more about the Singapore T-bill here.

| What I like | What I do not like | |

| Singapore 6-month T- bill | Principal sum is locked up for 6 months only Low risk of default Minimum investment of S$1000 | May not be liquid in the secondary market |

| Fixed Deposits | Low risk of default | Principal sum is locked up for at least 6-12 months Potential penalty for early withdrawal Usually higher deposit amount |

How do fixed deposit rates compare to Singapore Savings Bonds (SSBs)?

The Singapore Savings Bond (SSB) provides you with a simple and low-cost way to generate safe returns. Backed by the Singapore government, the SSB allows you to lock in long-term interest rates while offering flexibility of redeeming with no penalty.

The 1-year average return on the most recent issuance of the Singapore Savings Bonds (SSB) is 1.46%, lower than the best 12-month fixed deposit rate offered by the banks.

The minimum investment amount for the SSB is S$500, while the minimum fixed deposit amount is typically S$5,000 and above.

Learn more about Singapore Savings Bonds here.

| What I like | What I do not like | |

| Singapore Savings Bond | - Step-up interest rate of up to 10 years - Redeemable at any point but have to wait for up to a month for payment - Low risk of default - Minimum investment of S$500 | - 1-year return is lower than best fixed deposit interest rate |

| Fixed Deposits | - Low risk of default | - Deposit is typically locked up for at least 3 months - Potential penalty for early withdrawal - Typically higher deposit amount |

How do fixed deposit rates compare to cash management accounts?

You might have heard of Moomoo Cash Plus, Webull Moneybull or Longbridge Cash Plus discussed amongst investors in recent months.

These are all cash management accounts that are seen as relatively safe and highly liquid alternatives to cash in the bank.

By putting your money in a cash management account, you will be investing in money market funds or bond funds.

These professionally managed funds will put your cash in instruments such as bank deposits or short-term debt to earn higher interest rates.

Cash management accounts offer a relatively low-risk option for us to earn a potentially higher return on our cash.

For example, the indicative 7-day annualised yield of the Fullerton SGD Cash Fund was about +1.08% as of 31 July 2026.

Learn more about the Fullerton SGD Cash Fund here.

Compared to fixed deposits, cash management accounts offer more flexibility as they can be redeemed at short notice, usually in a few days.

Unlike fixed deposits, cash management accounts are not capital guaranteed and are not insured under Singapore Deposit Insurance Corporation (SDIC).

Check out our comprehensive guide to cash management accounts in Singapore to select the best cash management account for your portfolio.

Some robo-advisors have also introduced cash management solutions that offer guaranteed rates. They generate the returns by investing your funds into fixed deposits products provided by banks in Singapore.

For example, Syfe Cash+ Guaranteed is the cash management solution offered by Syfe which offers investors guaranteed rates for their idle cash.

Learn more about Syfe Cash+ Guaranteed here.

In addition, StashAway Simple Guaranteed also offers a cash management solution for 1 month, 3 months, 6 months or 12 months.

Learn more about StashAway Simple Guaranteed here.

How do fixed deposit rates compare to best USD fixed deposit rates?

Some of you may have noticed that foreign currency fixed deposit accounts are now offering a higher interest rate compared to Singapore dollar fixed deposit accounts.

While USD fixed deposit rates are higher compared to Singapore dollar fixed deposit rates, you should beware of foreign currency risk. Also, foreign currency fixed deposits are not covered by the Singapore Deposit Insurance Scheme.

Check out our guide to the best USD fixed deposit rates in Singapore to get the latest foreign currency fixed deposit rates.

Are there better fixed deposit rates for priority banking accounts?

Some banks may also offer priority banking customers a higher interest rate for fixed deposit accounts.

For example, Citigold customers can earn 1.40% p.a. for a three-month fixed deposit or 2.00% p.a. for six months using fresh funds. The minimum placement is S$10,000.

RHB Premier Banking customers can earn up to 1.75% p.a. with a minimum placement of S$20,000 at a branch. The promotional rates are 1.40% p.a. for three months, 1.70% p.a. for six months and 1.75% p.a. for 12 months. These rates are slightly higher than those available to regular RHB customers.

CIMB offers preferred banking customers a promotional interest rate of 1.60% p.a. for 9- and 12-month fixed deposits, above its normal fixed deposit rate of 1.55% p.a.

To find out the best fixed deposit interest rates for priority banking accounts, check out our comprehensive guide to priority banking accounts in Singapore.

What would Beansprout do?

I use fixed deposit as one of the ways to park my cash and ensure I have sufficient cash set aside for emergency uses.

When comparing fixed deposits, I would consider the interest rate, minimum placement amount and how long I am comfortable setting aside my money.

As of 1 August 2026, HL Bank offers the highest 3-month fixed deposit rate I found at 1.40% p.a., while RHB offers the highest 6-month rate at 1.60% p.a. For a 9-month placement, Bank of China and CIMB offer the highest rate of 1.55% p.a.

If I do not need access to my money for 12 months and can meet the minimum deposit requirement, I may consider RHB, which offers the highest 12-month fixed deposit rate I found at 1.65% p.a. for branch placements of at least S$20,000. Alternatively, GXS offers 1.60% p.a. with a much lower minimum placement of S$100, which may provide greater flexibility for smaller deposit amounts.

Apart from fixed deposits, I would also use a mix of savings accounts, T-bills, Singapore Savings Bonds (SSBs) and money market funds for my pot of liquidity funds.

I share more about the best savings accounts with the highest interest rate in Singapore here.

You can also find out more about Singapore T-bills and Singapore Savings Bonds here.

By finding the best place to park my cash, I know that I have a stable base for the rest of my portfolio to stay invested through markets ups and downs.

When this pot is properly set up, I know I can ride through market volatility without being forced to sell my investments at the wrong time.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments