Is the 1-year T-bill better than the 6-month T-bill and fixed deposits?

Bonds

By Gerald Wong, CFA • 11 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

The closing yield on the 1-year Singapore T-bill of 1.46% is close to the 6-month T-bill yield. However, investors of the 1-year T-bill may face lower re-investment risks.

What happened?

The Singapore T-bill yield has seen some swings over the past few months.

After reaching a recent low of 1.36% in the auction on 26 February, the yield on the 6-month Singapore T-bill jumped to reach 1.47% in the latest 6-month T-bill auction.

Likewise, fixed deposit rates in Singapore have started to edge higher again.

This has sparked more discussion in the Beansprout community about where is the best place to park cash for higher yields.

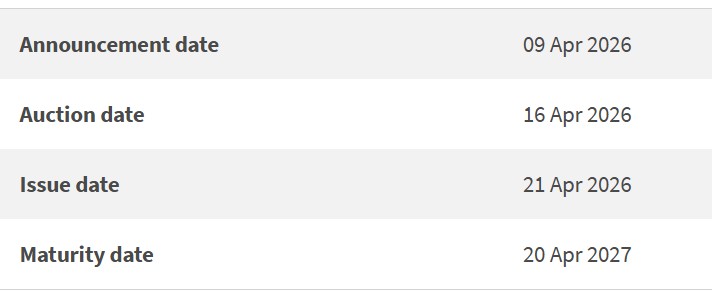

In this article, I will I will be looking at some of the latest indicators to find out if it is worthwhile applying for the upcoming 1-year Singapore T-bill auction (BY26101H) on 16 April 2026, and how it compared to the 6-month Singapore T-bill and fixed deposits.

What is the likely yield on the 1-year Singapore T-bill?

Like the 6-month Singapore T-bill yield, the 10-year Singapore government bond yield has fluctuated in recent months.

After reaching a low of below 1.8% last year October, the Singapore 10-year government bond yield bounced to above 2.4% in March with the Middle East conflict, before moderating to about 2.1% as of 10 April 2026.

This movements in the Singapore 10-year government bond yield reflects shifting expectations of interest rate cuts by the US Federal Reserve.

Likewise, we have seen less significant movements for the 1-year Singapore T-bill yield.

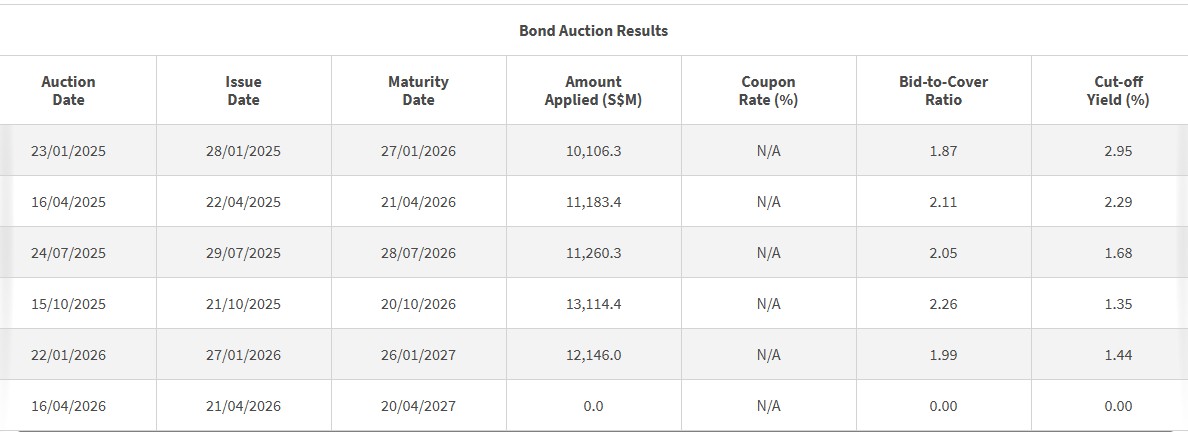

The closing yield on the 1-year T-bill was 1.46% as of 9 April 2026, hovering near the 1.44% cut-off yield seen in the January 1-year T-bill auction.

However, it is worth noting that the eventual cut-off yield in the auction may differ from the closing yield, as it will depend on the bids in the auction.

From the past few rounds of the 1-year T-bill auctions, we can see that demand for the T-bill has been fairly elevated.

This has put pressure on the cut-off yield of the 1-year T-bill.

Buying Singapore 1-year T-bill – better than 6-month T-bill?

Rather than applying for the 1-year T-bill, one option to consider is to invest in two consecutive tranches of 6-month T-bills.

Specifically, we could invest in the upcoming 6-month T-bill auction on 23 April 2026, and reinvest the funds again when the T-bill matures in October 2026.

If we apply for the next 6-month T-bill which will be issued on 28 April, the maturity date would be on 27 October 2026. We could then choose to reinvest based on the prevailing interest rates at that time.

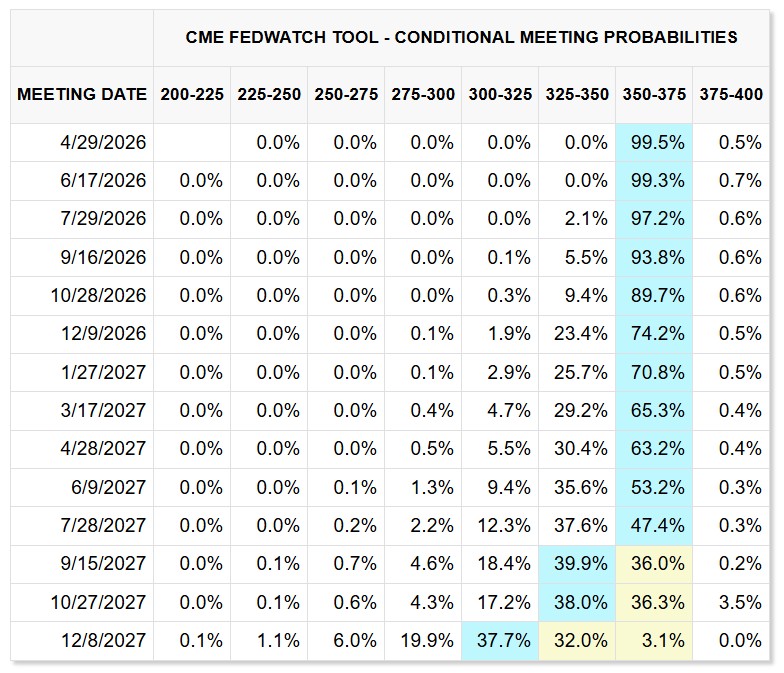

However, it is now less certain whether we will see further interest rate cuts, or potentially interest rate hikes in the next 6 months.

While the current closing yield of 1.46% on the 1-year Singapore T-bill is close to the cut-off yield of 1.47% in the most recent 6-month T-bill auction, I will ask myself if I would want to lock in the rate now for 12 months.

According to the latest US interest rate expectations, markets now expect the US Federal Reserve to hold interest rates steady in 2026, and only cut interest rates by 0.25% (25-basis-points) in 2027.

With significant economic uncertainty with global geopolitical developments, we will have to keep a close watch on interest rate trends.

Buying 1-year T-bill using cash – better than fixed deposit?

Some Singapore banks have raised their fixed deposit rates in April. Currently, the best 1-year fixed deposit rate we found is at 1.40% p.a.

This would then be lower than the latest closing yield of 1.46% on the 1-year T-bill.

For shorter tenure, the best 6-month fixed deposit rate is at 1.50% p.a.

However, we will require a minimum deposit of S$10,000 to earn the rate of 1.50%.

Buying 1-year T-bill – better than Singapore Savings Bonds?

The current issuance of the Singapore Savings Bonds (SSB) offer a 1-year return of 1.40%.

This is close to the current closing yield on the 1-year Singapore T-bill.

Apart from offering a 1-year return of 1.40%, the latest SSB also allows us to lock-in a rate of 2.14% over 10 years, while having the flexibility to redeem prior to maturity.

What would Beansprout do?

With the recent global geopolitical tensions, I have been evaluating my financial plan to make sure it offers me sufficient security and peace of mind.

The first step is to make sure I have sufficient cash put aside for emergency uses through my liquidity pot, where I would then put into a mix of savings accounts, fixed deposits, T-bills, SSBs and money market funds.

Then, I would see how I can earn a higher yield on this pot of emergency cash, while maintaining the liquidity I may need.

The current closing yield of the 1-year Singapore T-bill is 1.46%, which is close to the recent 6-month T-bill cut-off yield of 1.47%.

For me, this makes the 1-year T-bill worth considering, especially if I want to lock in my return now without having to worry about interest rate changes over the next 12 months.

At the same time, the 1-year T-bill yield is also higher than the best 1-year fixed deposit rate, which is currently at 1.40% p.a.

One of the other options to consider is the Singapore Savings Bonds (SSB), which offers a 1-year return of 1.40% and average annual return of 2.14% over 10 years, while having the flexibility to redeem prior to maturity.

I compare savings accounts, fixed deposits, T-bills, SSBs and money market funds. to find the best places to park your cash in April 2026 here.

Ultimately, the best option depends on whether I prioritise a slightly higher locked-in yield today, or greater flexibility for my cash.

By finding the best place to park my cash, I know that I have a stable base for the rest of my portfolio.

With this liquidity pot properly set up, I can stay invested through market ups and downs without worrying about being forced to sell my investments at the wrong time. Learn more about the liquidity pot here.

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win S$150 CapitaVouchers weekly! Promo ends on 30 April 2026. Learn more about the Longbridge promo here.

The 1-year Singapore T-bill auction is currently open.

As cash applications for the T-bill close one business day before the auction date, we would need to put in our cash applications for the T-bill by 9pm on 15 April (Wednesday).

Applications for the T-bill using CPF-OA will close 1-2 business days before the auction date, and the dates differ across the three local banks.

- Applications for T-bills online using CPF OA via DBS close at 9pm on 15 April (Wednesday). Read our step-by-step guide to applying via DBS.

- Application for T-bills online using CPF OA via OCBC close at 9pm on 15 April (Wednesday) Read our step-by-step guide to applying via OCBC

- Applications for T-bills online using CPF OA via UOB close at 9pm on 24 April (Tuesday) Read our step-by-step guide to applying via UOB.

To learn more about T-bills and find out how to apply, check out our comprehensive guide to T-bills.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments