Alibaba earnings reflect higher cloud spending as it targets long-term growth

Singapore Depository Receipts

Powered by

By Ng Hui Min • 27 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

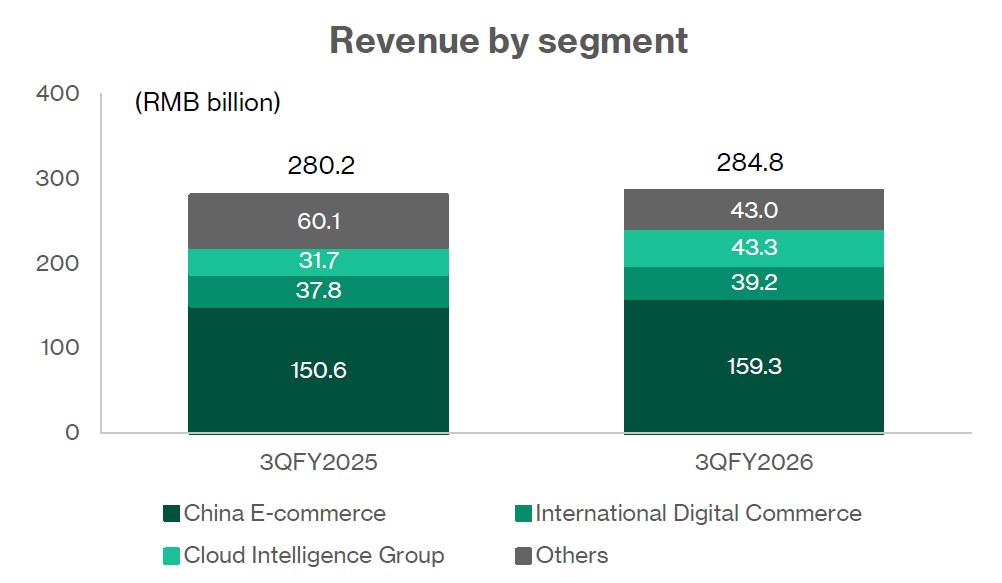

Alibaba reported 3QFY26 revenue which rose 2 percent year-on-year (YoY) to RMB 284.8 billion, while adjusted EBITA fell 57 percent and non-GAAP net income declined 67 percent.

Alibaba HK SDR 5to1 (SGX: HBBD) - Not Rated

3QFY2026 revenue rose 2% year-on-year

Reported revenue rose just 2 percent year-on-year (YoY) to RMB 284.8 billion, while adjusted EBITA fell 57 percent and non-GAAP net income declined 67 percent.

First, reported revenue was dragged down by the disposal of Sun Art and Intime, two physical retail businesses. Excluding these, underlying revenue growth was closer to 9 percent YoY, which gives a better picture of the momentum in Alibaba’s core digital businesses.

Second, the weaker profitability was largely intentional.

Management is investing aggressively in two areas that are strategically important but currently dilutive to margins. The first is quick commerce, where Alibaba is still spending heavily on subsidies to build scale and compete more effectively with Meituan. The second is AI and cloud infrastructure, where capital spending is being brought forward ahead of revenue recognition.

During the earnings call, management also said profitability is likely to remain volatile quarter to quarter because of intense competition and continued investment.

Cloud intelligence group is the fastest growing segment

Cloud Intelligence Group was the clear standout in 3Q FY2026.

Revenue rose 36 percent YoY to RMB 43.3 billion, marking its strongest quarter in several years and continuing the sharp acceleration seen over recent quarters. Revenue from external customers also grew 35 percent, suggesting demand is broadening beyond Alibaba’s internal ecosystem.

AI-related products remained the main growth engine, delivering triple-digit growth for the tenth straight quarter. Usage on Model Studio was especially strong, with token consumption increasing about six-fold in just three months.

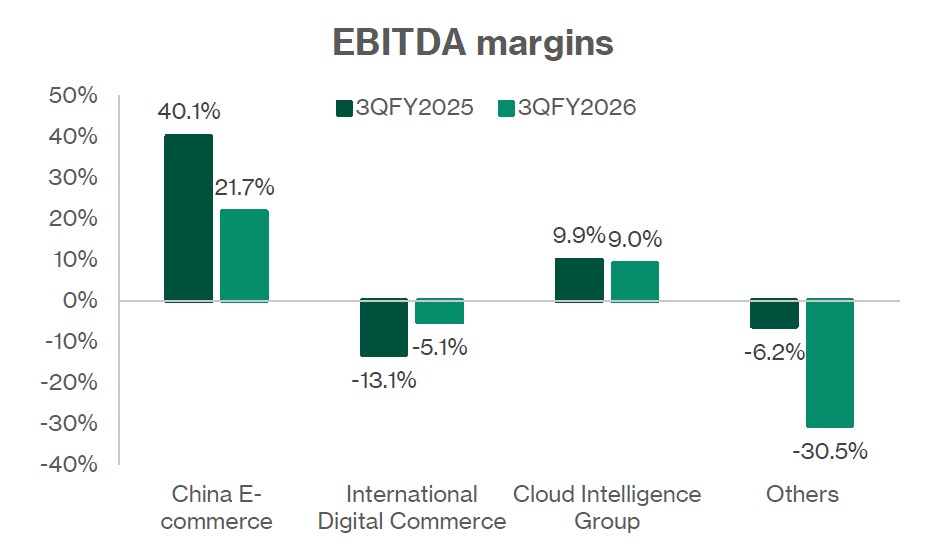

Even with continued heavy investment in infrastructure and customer acquisition, adjusted EBITDA margin held broadly steady at around 9 percent. Alibaba Cloud also continued gaining share in China, with market share rising for the third consecutive quarter to 36 percent.

On the earnings call, management said it is targeting US$100 billion in combined external cloud and AI revenue within five years, highlighting just how central this business has become to Alibaba’s long-term growth story.

China e-commerce segment is still the cash engine

China E-Commerce Group remained Alibaba’s largest segment, with revenue rising 6 percent YoY to RMB 159.3 billion in 3Q FY2026.

The performance, however, was mixed across its main revenue lines.

Customer management revenue, which includes merchant advertising and commissions on Taobao and Tmall, grew just 1 percent YoY to RMB 102.7 billion. Management attributed the softer growth to weaker consumer sentiment, an unusually warm winter that hurt apparel demand, and the later timing of Chinese New Year in 2026, which shifted some shopping activity from December into January.

By contrast, quick commerce continued to grow strongly. Revenue from Taobao Instant Commerce rose 56 percent YoY to RMB 20.8 billion, showing that Alibaba is still gaining traction in this newer part of the market.

Importantly, management said on the earnings call that physical goods’ gross merchandise value (GMV) and customer management revenue recovered significantly in the March quarter, suggesting the softer December quarter was more seasonal than structural.

Alibaba International Digital Commerce Group (AIDC) and other businesses

Alibaba International Digital Commerce Group is the group’s overseas e-commerce arm, serving consumers and businesses across more than 200 countries.

Its main platforms include AliExpress, which remains the largest contributor, Trendyol, the leading e-commerce platform in Turkey, and Lazada, which operates across Southeast Asia, including Singapore, Indonesia, Thailand, Malaysia, Vietnam, and the Philippines. The group also runs Alibaba.com, its international wholesale marketplace, which serves buyers in more than 190 countries.

In 3Q FY2026, AIDC revenue rose 4 percent YoY to RMB 39.2 billion, while adjusted EBITDA losses narrowed meaningfully. Management attributed the improvement to better logistics efficiency, more disciplined investment, and improving unit economics at AliExpress Choice.

There are also signs that parts of the business are maturing. Trendyol’s domestic business in Turkey is now profitable, while Lazada continues to improve. Overall, this remains more of a medium-term growth story than a near-term profit driver, but the narrowing losses suggest execution is getting better.

Meanwhile, revenue from the “All Others” segment fell 25 percent YoY to RMB 67.3 billion. This was mainly due to the disposal of Sun Art and Intime, and was partly offset by continued growth at Freshippo and Alibaba Health.

Share price pulled back after the results

The results triggered a negative share price reaction despite strong cloud growth, with investor concerns centred on four areas that each carry different implications for Alibaba’s near-term earnings outlook.

Profitability came in weaker than many investors expected.

Non-GAAP net income fell 67 percent YoY to RMB 16.7 billion, while free cash flow dropped 71 percent to RMB 11.3 billion, both well below expectations. The scale of the decline suggests the pressure is coming not just from quick commerce subsidies, but also from much heavier spending on AI and cloud infrastructure.

Management gave little comfort on a near-term recovery, noting that profitability is likely to remain volatile because of intense competition and continued investment. This means earnings pressure may persist for some time before the benefits of these investments become more visible.

Alibaba’s core e-commerce monetisation weaker than expected.

Customer management revenue, Alibaba’s core e-commerce monetisation metric, grew just 1 percent YoY to RMB 102.7 billion in 3Q FY2026, slowing from the stronger pace seen in FY2025 and coming in below market expectations.

This metric reflects the health of Taobao and Tmall’s advertising and commission income.

Management attributed it mainly to softer consumer sentiment, unusually warm winter weather that reduced apparel demand, and the later timing of Chinese New Year in 2026.

Importantly, management also said on the earnings call that physical goods GMV and customer management revenue recovered significantly in the March quarter, which suggests the softer December quarter was more seasonal than structural, even as competition from PDD and Douyin remains an ongoing risk to monitor.

Quick commerce losses were wider than guided

Quick commerce losses were another key area of concern.

China E-Commerce Group adjusted EBITDA fell 43 percent YoY to RMB 34.6 billion, with quick commerce subsidies being the main drag. Revenue from Taobao Instant Commerce still grew strongly, rising 56 percent YoY to RMB 20.8 billion, but the associated losses came in worse than investors had expected.

Part of the challenge is that Alibaba is competing against Meituan, which still has a stronger position in logistics density and consumer mindshare built over many years.

While management said unit economics improved through the quarter, helped by better fulfilment efficiency and order mix, the overall profit drag remained heavy.

On the earnings call, management shared that they are targeting RMB 1 trillion in quick commerce GMV by FY2028, positive cash flow at that scale, and full profitability by FY2029.

For now, though, the market remains focused on how much earnings pressure this business will continue to create in the near term.

Lack of clear near-term guidance

Management did not provide quantitative direction on when earnings or free cash flow might recover, and commentary on margins remained cautious.

While this reflects the reality of investing in fast-moving areas such as AI and quick commerce, it also leaves investors with limited visibility on the near-term path back to stronger profitability.

Focus on medium- to long-term growth drivers

Medium- to long-term growth is the key to the thesis.

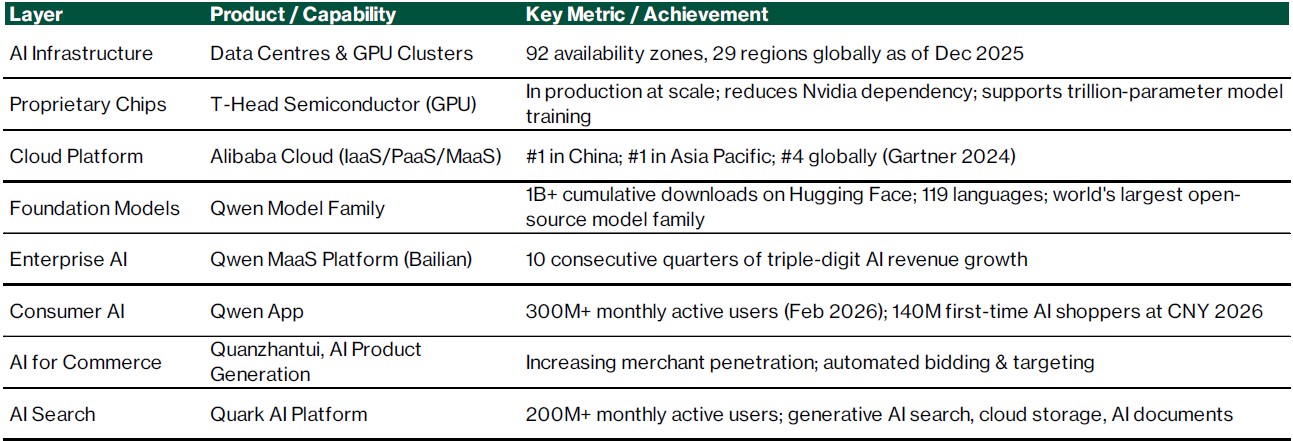

Near-term earnings are being deliberately compressed by investment, so the case for Alibaba depends on whether its main structural growth drivers — AI cloud infrastructure, quick commerce, the Qwen ecosystem, and T-Head chips — can deliver a meaningful and durable uplift in revenue and earnings over the next three to five years.

Cloud is emerging as Alibaba’s clearest growth engine

Cloud Intelligence is now the clearest medium-term driver of Alibaba’s transformation.

Revenue in the segment grew 36 percent YoY in 3Q FY2026, a sharp acceleration from just 7 percent a year earlier, while AI-related product revenue continued to deliver triple-digit growth for the tenth consecutive quarter.

Usage is also scaling quickly, with token consumption on Alibaba’s Model Studio platform rising about six-fold in just three months, suggesting that more enterprise customers are building and deploying AI applications on Alibaba’s infrastructure.

This matters because China’s cloud market is still at an earlier stage of development than the US according to IDC in 2024, which means Alibaba still has a long runway if enterprise digitalisation and AI adoption continue to rise.

With a 36 percent share of China’s public cloud market and management targeting US$100 billion in combined cloud and AI external revenue within five years, Cloud Intelligence has become the business most likely to drive Alibaba’s next rerating.

The main question is not whether demand is improving, but how quickly stronger revenue growth can eventually translate into more visible profit growth at the group level.

Quick commerce could become a larger platform driver over time.

Taobao Instant Commerce is one of Alibaba’s biggest medium-term investment bets.

Revenue in the segment grew 56 percent YoY to RMB 20.8 billion in 3Q FY2026, but the more important point is what this business is doing for Alibaba’s broader ecosystem.

In the 12 months to December 2025, quick commerce helped bring in 150 million new annual active consumers, more than the previous three years combined.

These users are likely lower-value customers at first, but they create a larger base for future monetisation as order frequency, basket size, and engagement improve over time.

Management is targeting RMB 1 trillion of quick commerce GMV by FY2028, with positive cash flow at that scale and full profitability by FY2029.

There are also early signs that the economics are improving, with better logistics efficiency, stronger monetisation, and a more favourable order mix helping unit economics through the quarter.

Over time, tighter integration with Qwen could also help drive more order volume without requiring the same level of subsidy intensity.

The main risk is that Meituan still holds a stronger position in instant delivery, both in logistics density and consumer mindshare, which means Alibaba may need to absorb heavy investment for longer before this business contributes meaningfully to profits.

Qwen could become a powerful monetisation and distribution layer

Qwen is becoming one of Alibaba’s most strategically important AI assets.

Its open-source model family had surpassed one billion cumulative downloads by January 2026, giving Alibaba broad developer reach and helping embed Qwen across a growing global AI ecosystem.

This matters because the monetisation path is not mainly through selling the model itself, but through drawing developers and enterprises onto Alibaba Cloud’s model-as-a-service infrastructure for deployment, inference, and fine-tuning.

On the consumer side, the Qwen app had already reached 300 million monthly active users by February 2026, and was integrated across major Alibaba services such as Taobao, Tmall, Taobao Instant Commerce, Alipay, Fliggy, and Amap.

That makes Qwen more than just a chatbot. It is increasingly becoming a new interface layer for Alibaba’s broader ecosystem, helping users complete real-world tasks such as shopping, travel booking, payments, and food delivery.

Over time, this gives Alibaba two potential sources of value creation: stronger cloud monetisation through enterprise AI adoption, and deeper user engagement across its consumer platforms.

The near-term challenge is that Qwen’s direct financial contribution is still not separately visible, so investors will need to be patient as usage scales before monetisation becomes clearer.

T-Head chips add strategic depth and hidden optionality

T-Head, Alibaba’s in-house chip design arm, is a longer-term part of the AI story that may not yet be fully reflected in the stock.

Its strategic value goes beyond revenue. By developing its own AI chips, Alibaba can reduce reliance on external suppliers, improve supply security, and potentially lower the cost of delivering AI services across its cloud platform.

This is especially relevant at a time when global AI chip supply remains tight and US semiconductor restrictions continue to shape the competitive landscape for Chinese technology companies.

Over time, T-Head could strengthen Alibaba’s cost position in model inference and cloud deployment, while also giving the group more control over how its AI stack is built.

The business still looks like embedded option value rather than a near-term earnings driver, but it could become increasingly important if Alibaba’s AI and cloud ambitions continue to scale.

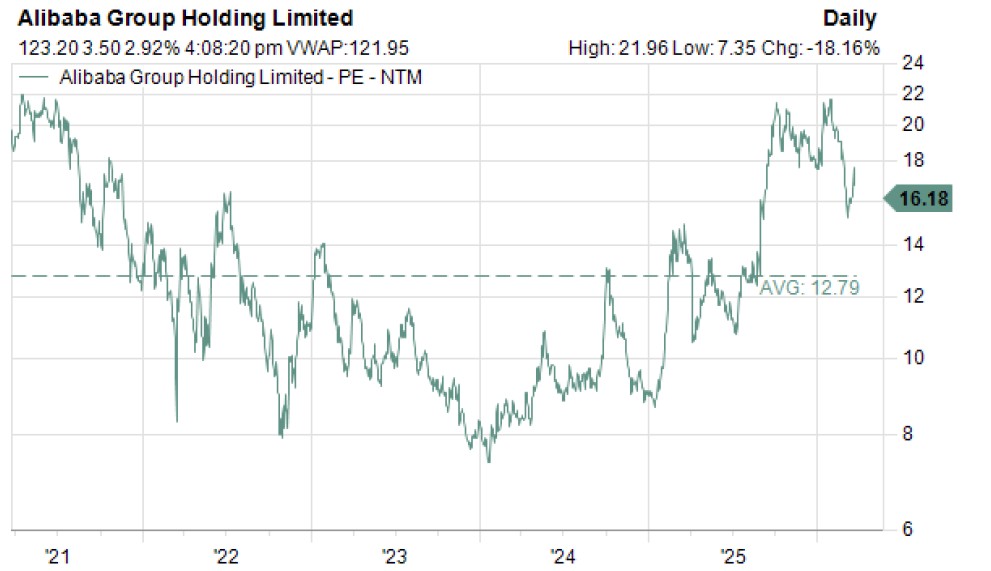

P/E valuation in line with sector average

Alibaba is currently trading at about 16.2x forward earnings, which is above its longer-term average of around 12.8x, based on the chart below.

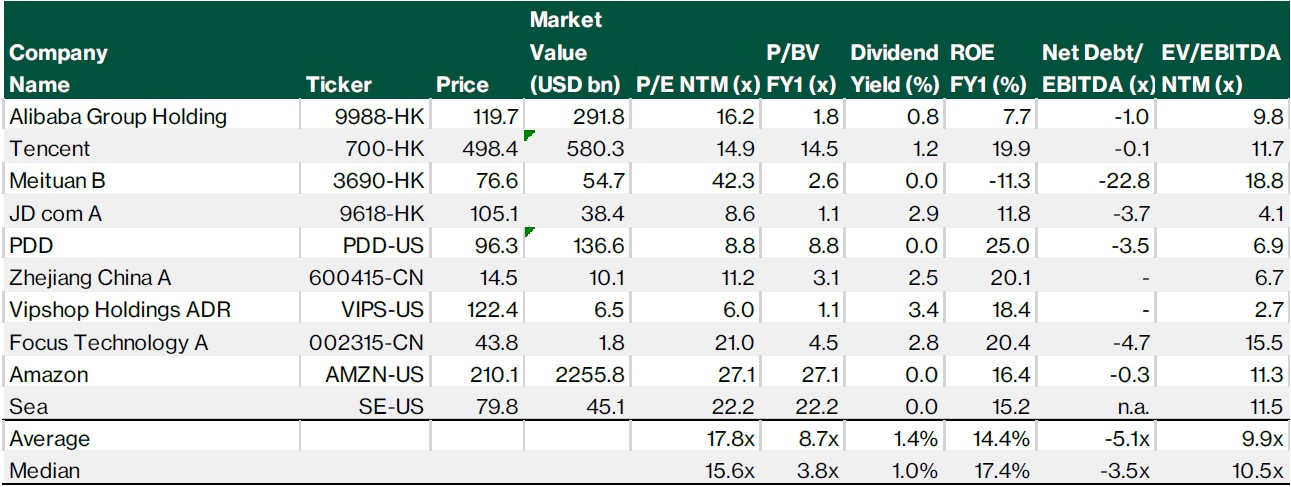

On peer comparisons, Alibaba trades at 16.2x forward earnings and 1.8x forward book, which places it slightly above the peer median of 15.6x P/E but well below higher-growth global platform names such as Amazon on 27.1x, Sea on 22.2x and Meituan on 42.3x. At 9.8x EV/EBITDA, Alibaba is trading close to the peer median of 10.5x.

Key risks

Key risks include regulatory and policy uncertainty in China, renewed US-China geopolitical tensions and semiconductor export restrictions, the structural limits of the VIE ownership structure, and intense competition from PDD, Douyin, and Meituan in Alibaba’s core markets.

You can now trade Alibaba through Hong Kong Singapore Depository Receipts (SDRs). These HK SDRs offer investors a more accessible way to invest in Hong Kong-listed companies.

According to SGX data, Alibaba HK SDR is amongst the top 3 most traded SDRs on SGX in 2026 year-to-date.

The introduction of Singapore Depository Receipts allows investors to purchase Alibaba shares with a lower minimum investment outlay compared to buying Hong Kong-listed shares directly.

Additionally, SDR holdings will be custodised within investors’ Central Depository (CDP) accounts, providing seamless integration with their existing Singapore-based portfolios.

Download the full report here.

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in Alibaba HK SDR 5to1.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Beansprout received monetary compensation from Singapore Exchange (SGX) to provide independent research on Singapore Depository Receipts (SDRs).

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments