Capitaland Ascendas REIT invests S$1.4 billion in Singapore and Japan assets

Stocks

By Gerald Wong, CFA • 27 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

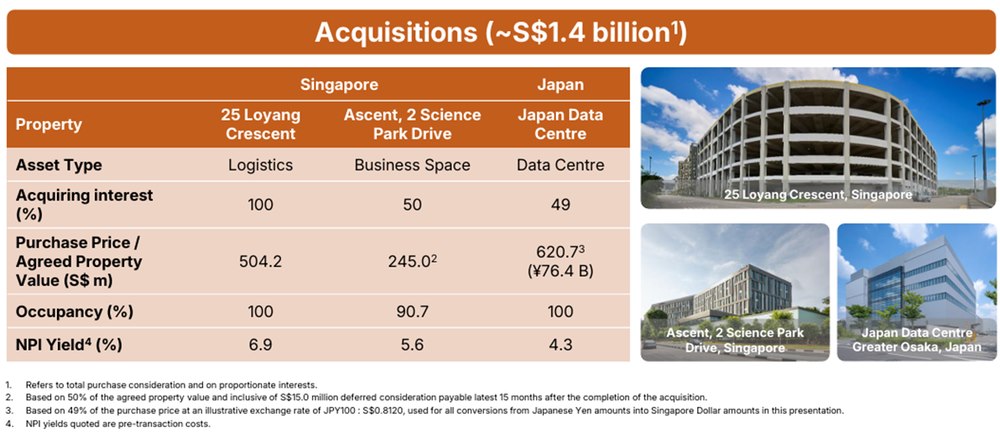

On 24 March 2026, CapitaLand Ascendas REIT announced three acquisitions valued at around S$1.41 billion.

What happened?

CapitaLand Ascendas REIT has been on an acquisition spree recently.

Last month, they entered Spain with S$185.4 million logistics portfolio acquisition, added a US logistics property for S$94.5 million in January and acquired 2 Singapore assets for around S$700 million in June last year.

On 24 March 2026, CapitaLand Ascendas REIT announced three acquisitions valued at around S$1.41 billion.

This would include a logistics property in Loyang, Singapore; a 50 percent stake in Ascent, a business space asset at Singapore Science Park; and, for the first time, a 49 percent stake in a Tier III hyperscale data centre in Greater Osaka, Japan.

To fund them, CapitaLand Ascendas REIT launched an equity fund raising of at least S$900 million through a private placement and preferential offering.

I saw a question in the Beansprout Telegram group asking about our view on CapitaLand Ascendas REIT’s latest acquisition.

In this article, I will dive deeper in the acquisition and find out what it means for unitholders.

What you need to know about CapitaLand Ascendas REIT’s latest acquisitions

#1 - Loyang logistics asset with long lease visibility

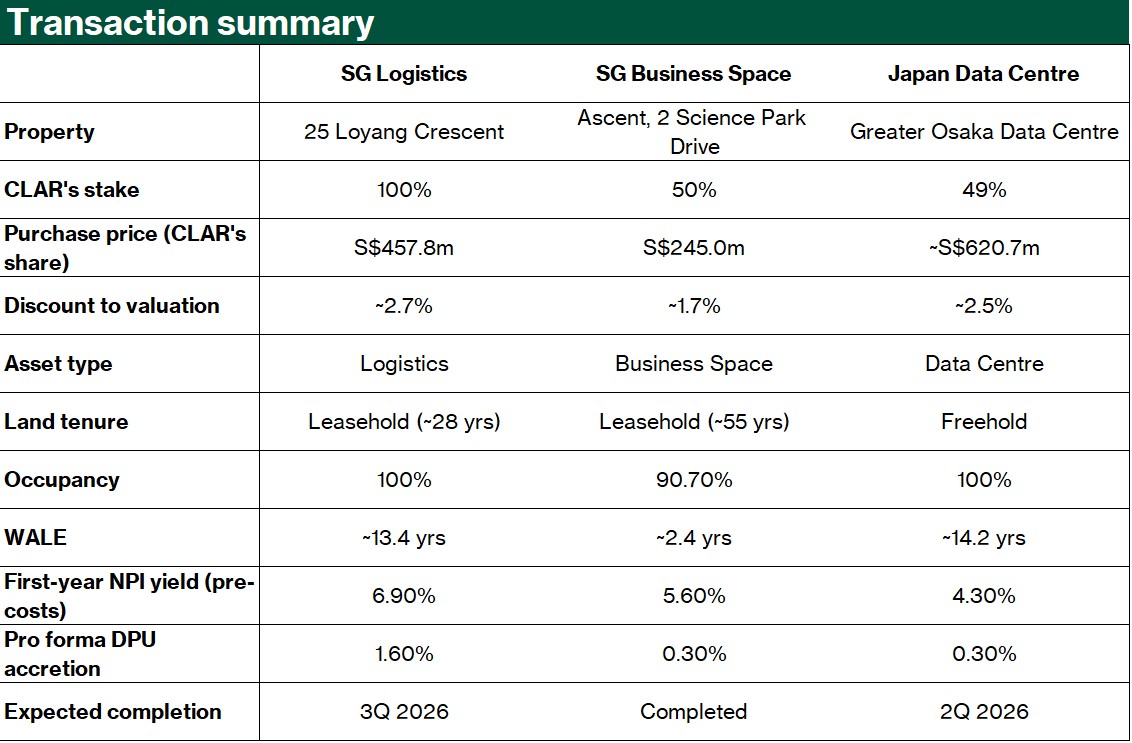

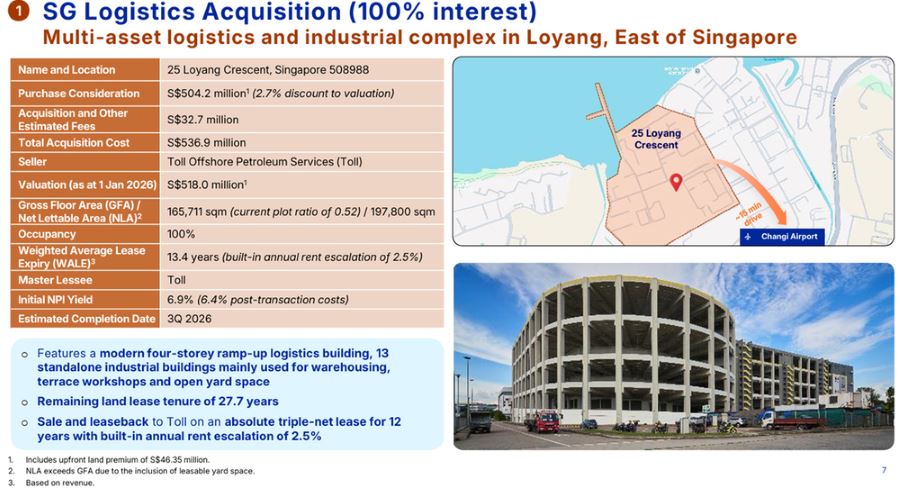

One of the three acquisitions is 25 Loyang Crescent, which CapitaLand Ascendas REIT is buying for S$457.8 million.

This is a sizeable logistics and industrial complex in eastern Singapore, and the purchase price is about 2.7 percent below its independent valuation.

The asset is not just a standard warehouse. It includes marine and offshore logistics facilities, multiple industrial buildings and workshops, ramp-up warehouses, and even a plot leased out for a floating data centre.

One feature that stands out is the income visibility.

The seller, Toll Offshore Petroleum Services, will lease the property back to CLAR under a 12-year absolute triple-net lease. This means the tenant will bear the operating costs and capital expenditure, while CLAR will receive more stable rental income.

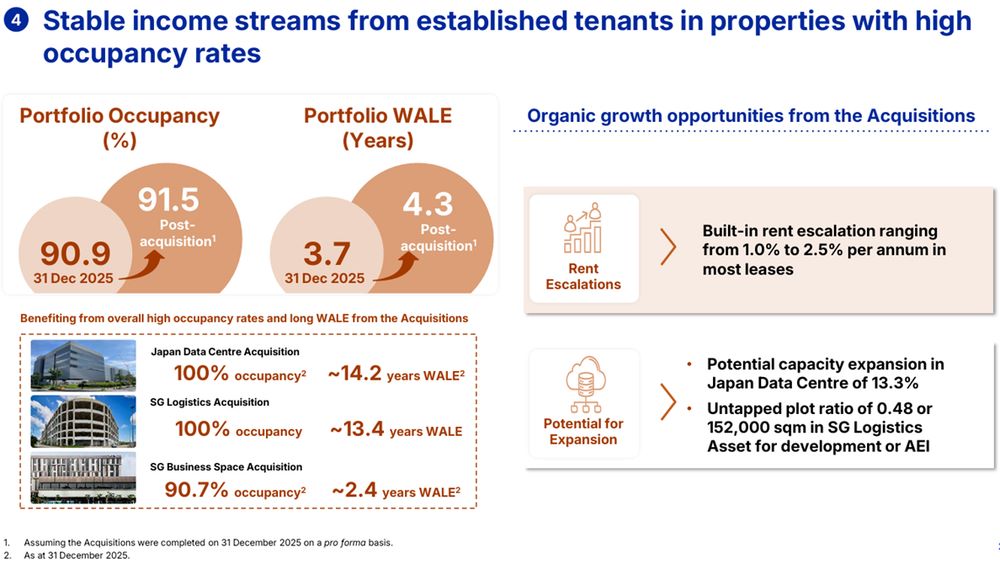

The lease also comes with 2.5 percent annual rent escalations, and the weighted average lease expiry is about 13.4 years by revenue.

The property’s first-year net property income yield is expected to be 6.9 percent before transaction costs, which looks attractive relative to CLAR’s funding cost.

There is also some longer-term optionality here. The site has an untapped plot ratio, which means there may be room for future development or asset enhancement over time.

This acquisition is a yield-accretive addition that strengthens CLAR’s Singapore logistics exposure while offering long lease visibility and some future upside from redevelopment potential.

#2 — Ascent at Science Park: strengthening CLAR’s Science Park presence

CapitaLand Ascendas REIT is also acquiring a 50 percent stake in Ascent, a premium business space property at 2 Science Park Drive, for S$245 million.

Ascent sits at the entrance to Singapore Science Park 1, close to Kent Ridge MRT, and directly opposite Geneo, the new life sciences and innovation cluster developed by CLAR and CapitaLand Development.

Its tenants include major names such as Johnson & Johnson, Dyson, and Merck, which gives the asset stronger quality and relevance within Singapore’s R&D and life sciences ecosystem.

With this deal, CapitaLand Ascendas REIT’s assets under management in Singapore Science Park will rise to about S$2.3 billion, further strengthening its position in one of Singapore’s key business space and life sciences hubs.

The first-year net property income yield is 5.6 percent before transaction costs, with a modest pro forma DPU accretion of 0.3 percent. The acquisition had also already been completed at the time of announcement.

This deal deepens CLAR’s exposure to a higher-quality, more specialised business park cluster with longer-term relevance.

#3 — Japan debut: a hyperscale data centre with long lease visibility is the largest of the three deals

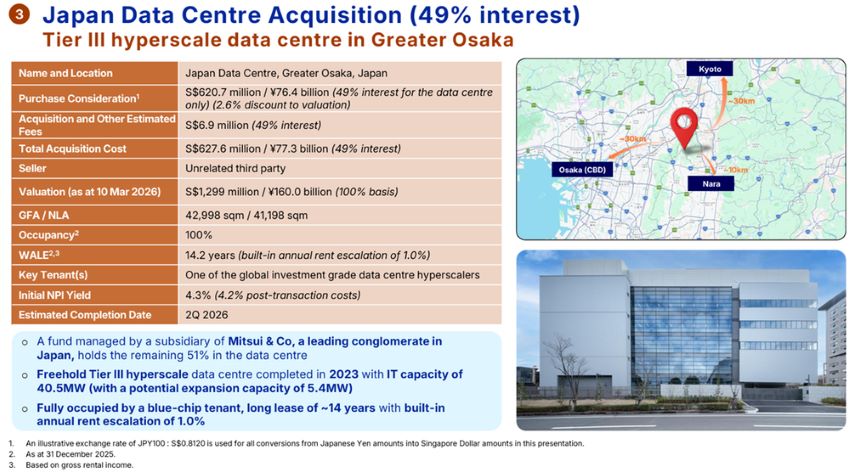

CapitaLand Ascendas REIT is also making its first move into Japan through the acquisition of a 49 percent stake in a Tier III hyperscale data centre in Greater Osaka for about S$620.7 million.

The remaining 51 percent will be held by a fund managed by Mitsui & Co. Realty Management.

The asset was completed in 2023 and is currently fully leased to a global investment-grade hyperscaler, with a long weighted average lease expiry of about 14.2 years and annual rent escalations of 1 percent.

That gives CLAR relatively strong income visibility, even though the first-year net property income yield of 4.3 percent is lower than the Singapore logistics deal.

What makes this acquisition notable is the strategic angle.

Japan is one of the largest and fastest-growing data centre markets in developed Asia Pacific, and Osaka is emerging as a key secondary hub alongside Tokyo.

Demand from hyperscalers remains strong, while new supply is still relatively tight.

This gives CapitaLand Ascendas REIT exposure to a sector with long-term structural demand, supported by cloud adoption and AI-related infrastructure needs.

After this acquisition, CLAR’s data centre portfolio will span six markets and total about S$2.6 billion in assets under management.

It also lifts the share of newer data centre assets in the portfolio, which should help improve overall asset quality.

This marks CLAR’s entry into Japan while increasing its exposure to modern data centre assets backed by long leases and structural demand growth.

#4 — Singapore remains the anchor of the portfolio

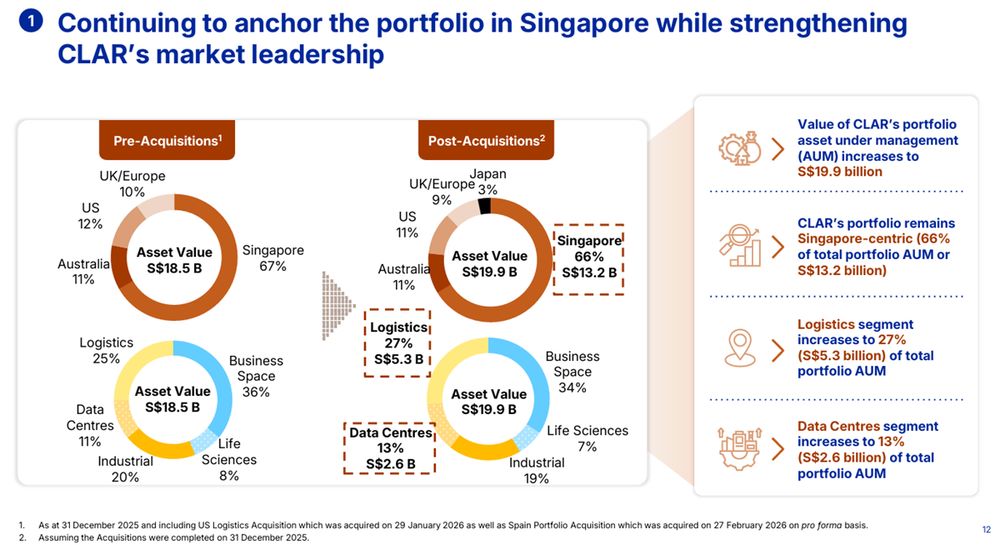

Taken together, the three acquisitions will lift CLAR’s assets under management from about S$18.5 billion to S$19.9 billion.

Singapore will still remain the main part of the portfolio, making up 66 percent of total AUM, while Japan will account for a new 3 percent slice. The deals also increase CLAR’s exposure to logistics and data centres, with these segments rising to 27 percent and 13 percent of total portfolio AUM respectively.

CapitaLand Ascendas REIT’s portfolio occupancy would rise from 90.9 percent to 91.5 percent, while weighted average lease expiry would extend from 3.7 years to 4.3 years.

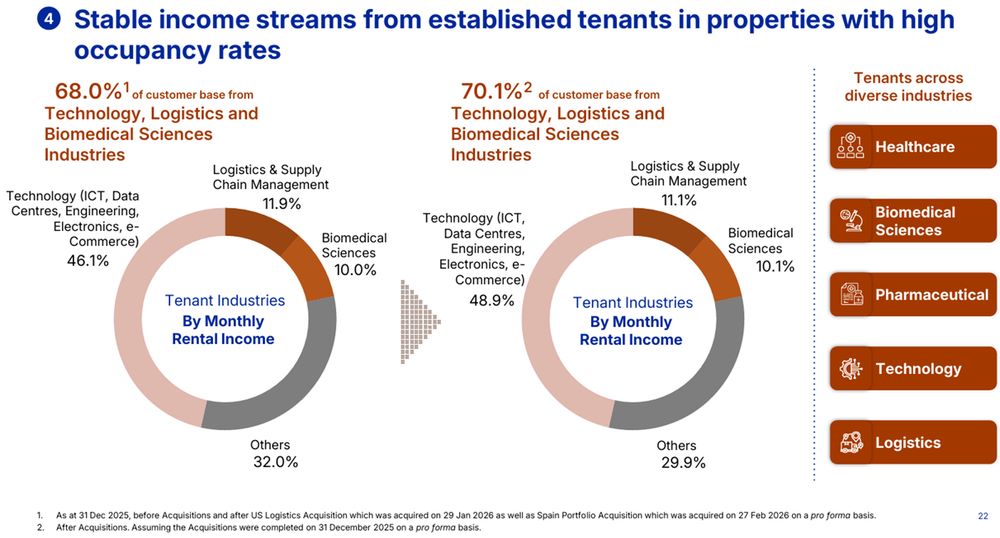

At the same time, the share of monthly rental income coming from technology, logistics and biomedical sciences tenants would increase from 68 percent to 70.1 percent.

#5 — All three acquisitions are expected to be DPU-accretive.

All three assets were bought below independent valuation, at discounts of 2.7 percent for Loyang, 1.7 percent for Ascent, and 2.5 percent for the Osaka data centre.

To fund the acquisitions, CLAR launched both a private placement and a preferential offering, raising total gross proceeds of about S$903.5 million.

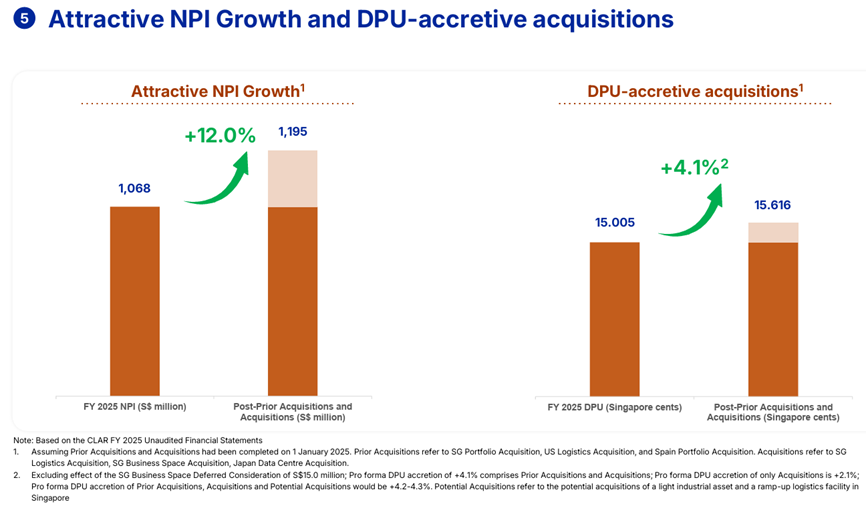

Based on CLAR’s pro forma figures, the three acquisitions together are expected to raise FY2025 DPU by about 0.318 Singapore cents, or 2.1 percent, from 15.005 Singapore cents to 15.323 Singapore cents, assuming all three had been completed on 1 January 2025.

Each acquisition is also expected to be DPU-accretive on a standalone basis.

Including the acquisitions announced since October 2025, total pro forma DPU accretion rises to about 4.1 percent.

CLAR is also evaluating two more Singapore assets, a light industrial property and a ramp-up logistics facility. If these proceed, pro forma DPU accretion could rise further to around 4.2 to 4.3 percent.

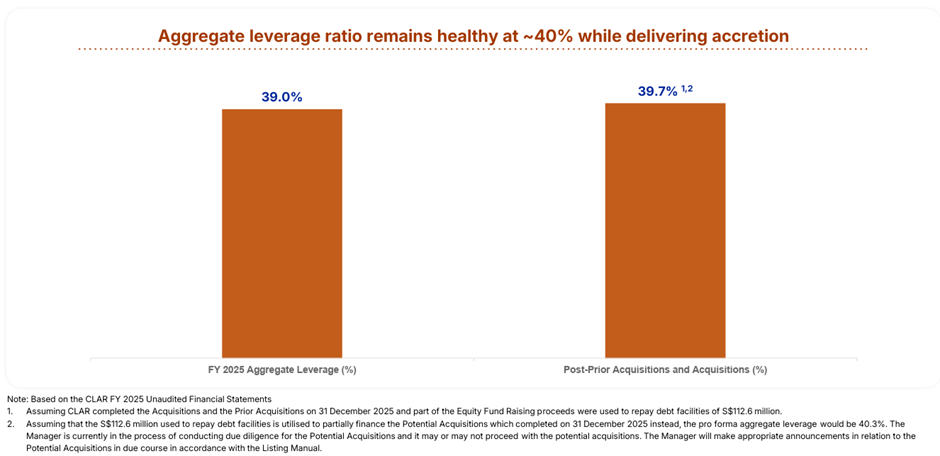

#6 — All three assets were acquired at discounts, with leverage still manageable.

After the acquisitions and fund raising, aggregate leverage is expected to rise only slightly from 39.0 percent to 39.7 percent.

Net asset value per unit is also expected to edge up from S$2.29 to S$2.36 on a pro forma basis.

What would Beansprout do?

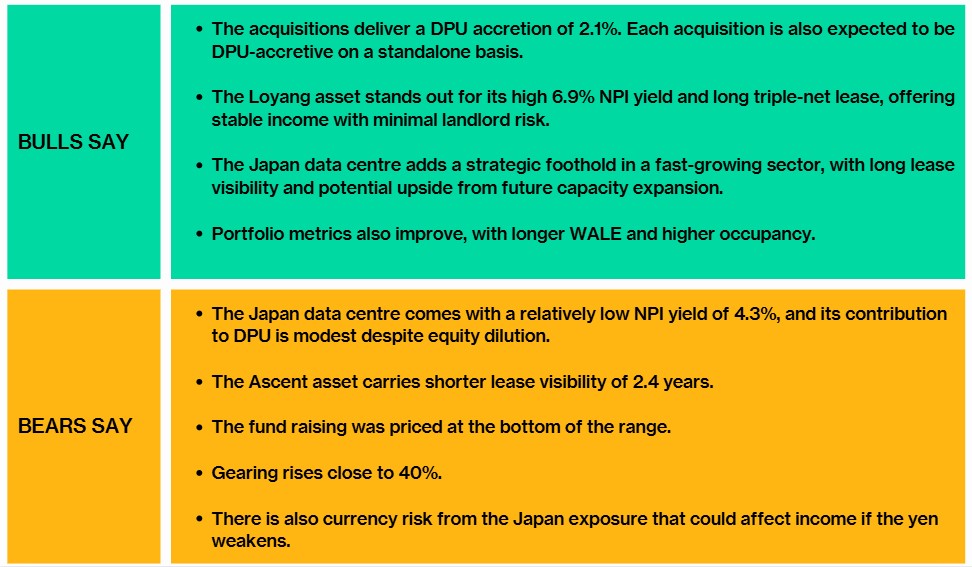

These are sizeable acquisitions by CapitaLand Ascendas REIT, with the Japan data centre standing out as the most strategic.

It marks CapitaLand Ascendas REIT’s first entry into Japan and strengthens its exposure to the fast-growing data centre segment in Asia Pacific.

The long 14.2-year lease to an investment-grade tenant provides strong income visibility, though the 4.3% yield is lower than the logistics asset.

The Loyang logistics estate looks the most immediately attractive.

It offers a higher yield, a long triple-net leaseback with annual rent escalations, and potential upside from redevelopment, making it a solid contributor to income resilience.

The Ascent acquisition is smaller but still adds value by deepening CapitaLand Ascendas REIT’s presence in Singapore Science Park and increasing its exposure to life sciences.

The shorter lease profile of 2.4 years of WALE does introduce some near-term leasing risk, but this is partly offset by location and tenant quality.

Overall, the deals appear DPU-accretive and aligned with CapitaLand Ascendas REIT’s strategy.

The DPU accretion from these acquisitions may help to mitigate the slight decline in DPU reported by CapitaLand Ascendas REIT in its 2H25 results.

CapitaLand Ascendas REIT is currently trading at about 1.1 times book value based on its pre-acquisition book value, or around 1.06 times based on pro forma NAV.

Both are below its long-term average of 1.2 times book, suggesting valuation still looks reasonable relative to its own history.

Based on the pro forma DPU of 15.323 Singapore cents and a closing price of S$2.51 as of 25 March 2026, CapitaLand Ascendas REIT would offer a dividend yield of about 6.1%.

This is above its long-term average dividend yield of 5.5%, and above the 10-year Singapore bond yield, reflecting the recent pullback in its share price with expectations of Fed rate cuts easing.

If I am looking for Singapore blue chip REITs with a dividend yield of above 5% to add to my income portfolio, I would be adding CapitaLand Ascendas REIT to my watchlist.

Which Singapore blue chip REIT are you looking at with the recent share price pullback? Leave a comment below or share with us in the Beansprout telegram group.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments