CapitaLand India Trust: Strong underlying performance detracted by FX

Stocks, REITs

By Gerald Wong, CFA • 28 Apr 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

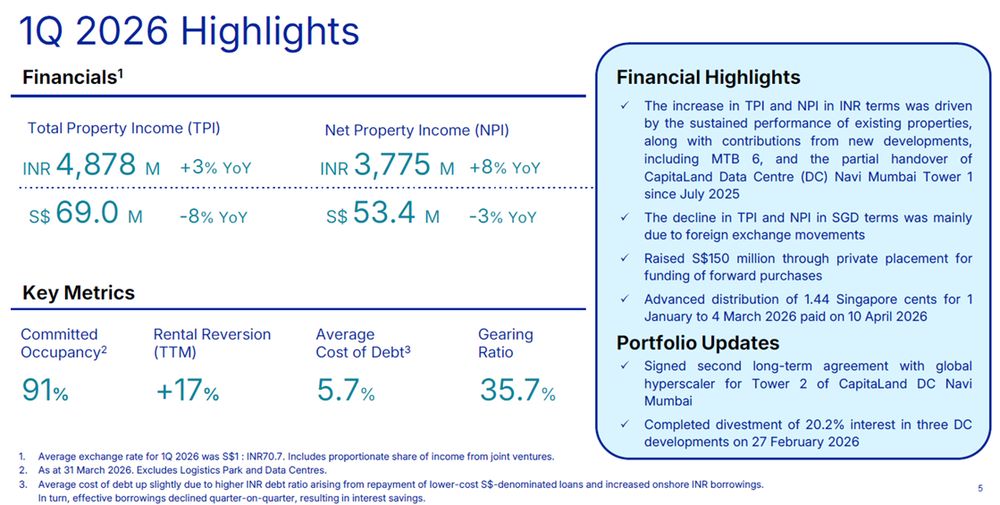

CapitaLand India Trust reported 1Q FY26 net property income of S$53.4 million, decline by 3% year-on-year, due to depreciation in Indian Rupees. Fundamental remains strong with firm portfolio occupancy and robust rental revision.

Strong underlying growth masked by weaker INR against SGD

CapitaLand India Trust reported total property income of INR4,878 million in 1Q FY26, increased by 3% year-on-year. Net property income (NPI) grew 8% year-on-year in 1Q FY26, to INR3,775 million. The stronger NPI growth relative to total property income reflects improved operating leverage — cost efficiencies are flowing through to the bottom line.

The INR growth was driven by sustained performance from existing properties, plus contributions from new developments — specifically MTB 6 and the partial handover of CapitaLand DC Navi Mumbai Tower 1 to the tenant since July 2025. As Tower 1 ramps up and Tower 2 comes online in 4Q26, NPI contributions from the data centre segment will grow substantially.

Management reiterated its focus on proactive cost management in light of recent geopolitical tensions. The impact is partly mitigated by the portfolio’s energy mix, with 57% sourced from renewable energy, while utility costs are largely passed through to tenants and are not expected to materially affect net property income. Although the recent spike in oil prices and potential inflationary pressures remain contained for now, CapitaLand India Trust will continue to monitor cost pressures, including any impact on its development pipeline.

In SGD currency terms, CapitaLand India Trust reported total property income of S$69.0 million in 1Q FY26, down 8% year-on-year in SGD terms (1Q FY25: S$75.0 million). NPI was S$53.4 million, down 3% year-on-year in SGD terms (1Q FY25: S$55.1 million). The SGD declines were wholly attributable to INR depreciation against SGD — the 1Q26 average exchange rate of S$1: INR 70.7 was weaker versus 1Q FY25.

Portfolio shows firm occupancy and robust rental revision

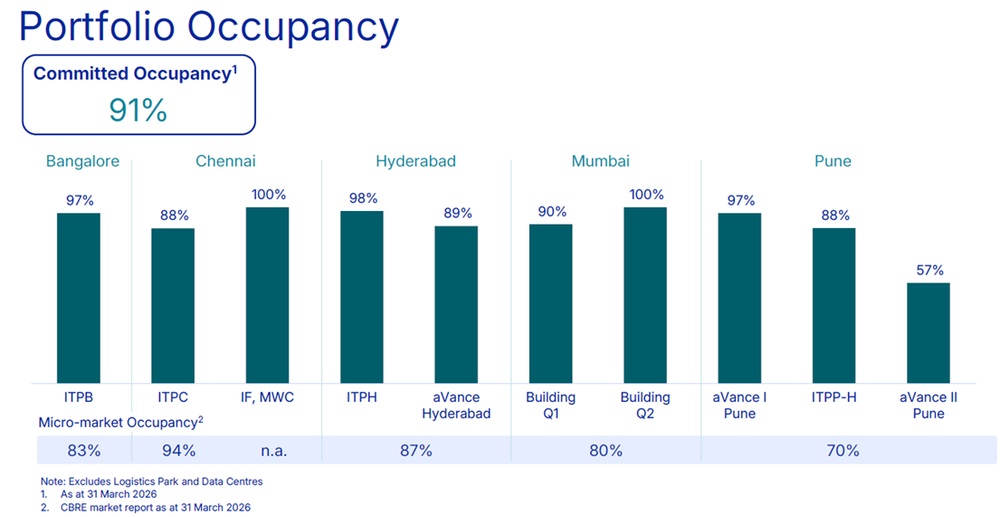

IT park committed occupancy was 91% as at 31 March 2026, unchanged from 31 December 2025. CapitaLand India Trust continues to outperform relevant submarket vacancy rates across all cities.

Bangalore micro-market occupancy is 83% versus CapitaLand India Trust's 88–100% across individual assets.

Hyderabad submarket is 87% versus CapitaLand India Trust's International Tech Park Hyderabad (ITPH) at 97% and aVance Hyderabad achieving 88–90%.

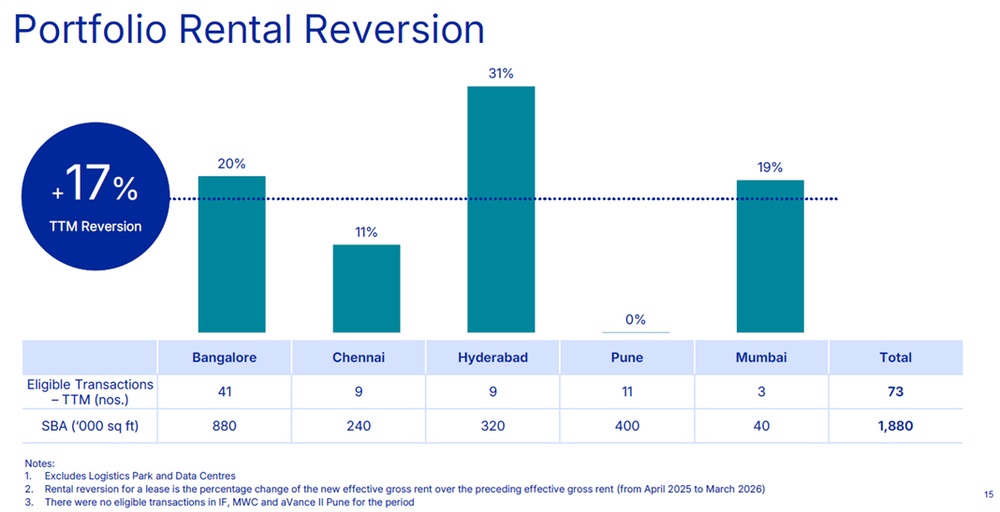

The portfolio achieved a trailing 12-month rental reversion of +17%, led by assets in Hyderabad and Bangalore. The strong reversions reflect tight vacancy, Global Capability Centres (GCC) demand, and quality asset positioning.

In total, CapitaLand India Trust secured 73 eligible transactions covering 1.88 million sq ft of super built-up area (SBA). To note, leasing continues to be competitive in Pune, where rental reversion was flat. This is mitigated by Capitaland India Trust’s diversified exposure across region, in terms of base rent.

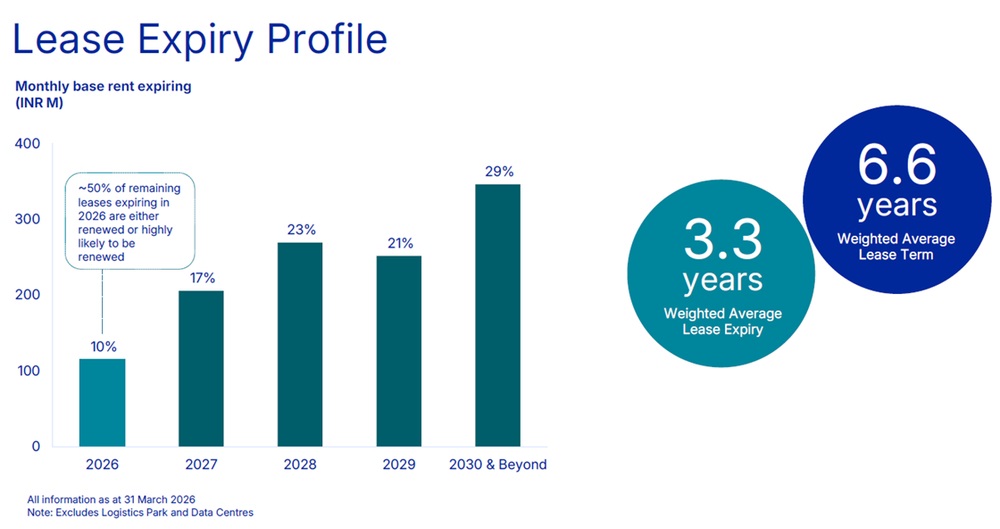

With proactive asset management, weighted average lease expiry was 3.3 years as of 31 March 2026, compared with 3.4 years at of December 2025.

Approximately 50% of remaining 2026 lease expiries are either already renewed or highly likely to be renewed, providing good near-term income visibility. The lease expiry profile is well-spread, with only 9.7% of base rent expiring in the remainder of 2026, followed by 17.3% in 2027 and 22.7% in 2028.

Updates on data centre portfolio

The three facilities totalling 200 MW are completing through 2026, all structured as long-term colocation leases to blue-chip hyperscalers.

Navi Mumbai Tower 1, the first completed data centre, has started handover to the tenant since July 2025. CapitaLand India Trust will record full contribution from Navi Mumbai Tower 1 in FY2026. Tower 2 Navi Mumbai will come online 4Q26. Both Tower 1 and Tower 2 are fully leased to a global hyperscaler, providing income visibility for FY2027.

International Tech Park Hyderabad and Chennai Data Centres are contributing from mid-2026.

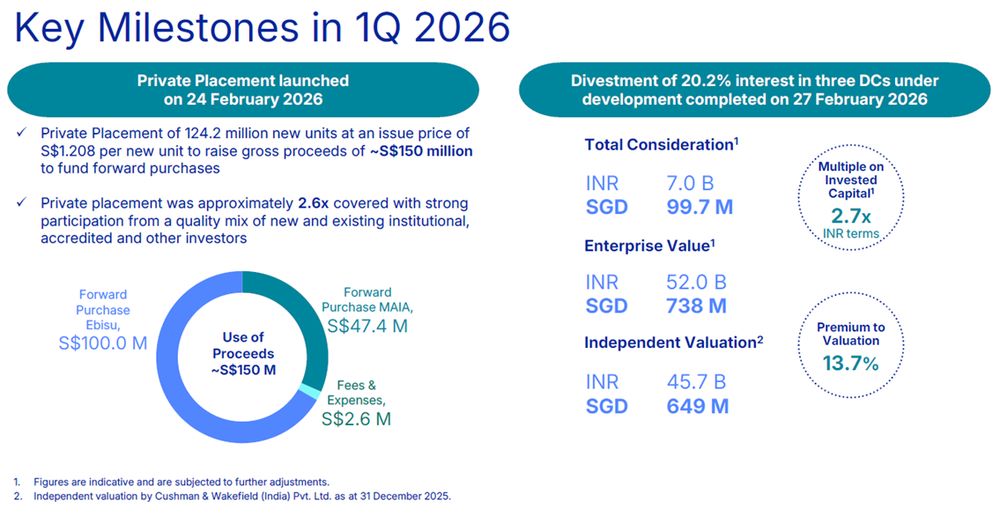

In February 2026, CapitaLand India Trust divested 20.2% stake in the development at 13.7% premium to independent valuation. The transaction raised about S$99.7 million. This active capital recycling is part of CapitaLand India Trust’s strategy and provides funding for other growth projects.

The premium valuation reflects the competitiveness of CapitaLand India Trust’s assets. For instance, Tower 2 is one of the largest single-tower implementations of liquid cooling in the region and has one of the best design power usage effectiveness achieved for a single data -centre tower, according to the management.

Adequate financial flexibility to fund growth pipeline

The divestment of a 20.2% stake in CapitaLand India Trust's three data centre developments (completed 27 February 2026) was highly value-accretive, realising proceeds at a 2.7x multiple on invested capital and a 13.7% premium to independent valuation.

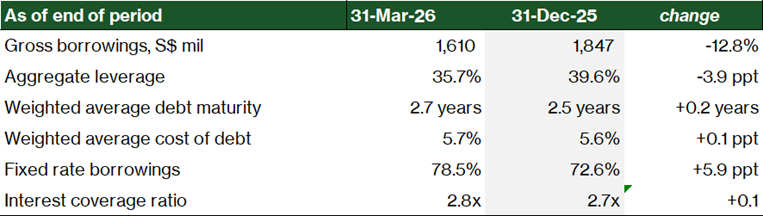

The transaction reduced gearing from 39.6% at end-2025 to 35.7% as at 31 March 2026, leaving CapitaLand India Trust with S$1.28bn of debt headroom to the 50% regulatory limit.

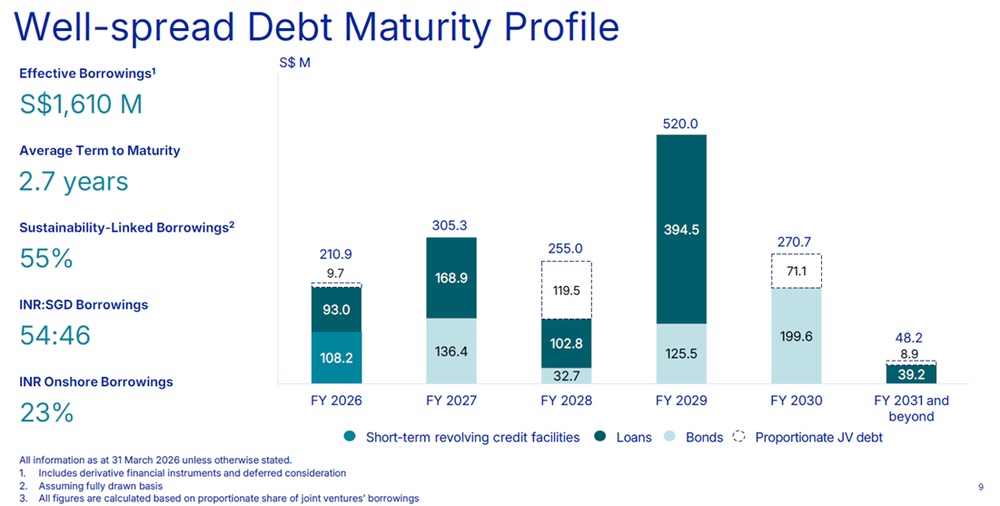

Effective borrowings stood at S$1,610 million as at 31 March 2026, with an average term to maturity of 2.7 years. Effective borrowings declined quarter-on-quarter due to this repayment, resulting in actual interest savings.

The INR:SGD borrowings split was 54:46, and management is targeting 40-50% onshore INR debt over the next few years to increase the natural hedge against INR depreciation. Currently, 54% of debt is INR-denominated.

Average cost of debt rose slightly to 5.7% from 5.6% at end-2025, due to a higher INR debt ratio as lower-cost SGD loans were repaid and replaced with onshore INR borrowings.

As at 31 March 2026, INR onshore borrowings accounts for 23% of total debt. CapitaLand India Trust plans to increase the portion of onshore borrowing to 40% - 50%, in order to take advantage of the lower borrowing cost and to leverage on the tax efficiency.

Interest coverage ratio (ICR) improved to 2.8x (end-2025: 2.7x), and 78.5% of borrowings are on fixed rate (up from 72.6%), providing strong protection against interest rate increases.

The debt maturity profile shows refinancing requirement of S$210.9 million in FY2026 and S$305.3 million in FY2027. We think the quantum is manageable, particularly given the lower gearing ratio as at 31 March 2026.

As part of the capital management strategy to keep gearing ratio at a prudent level, CapitaLand India Trust launched a private placement on 24 February 2026. The private placement of 124.2 million new units at S$1.208 per unit, raised approximately S$150 million. The proceeds will be used to fund the forward purchase pipeline, including assets Ebisu and MAIA.

Maintain BUY and target price at S$1.36

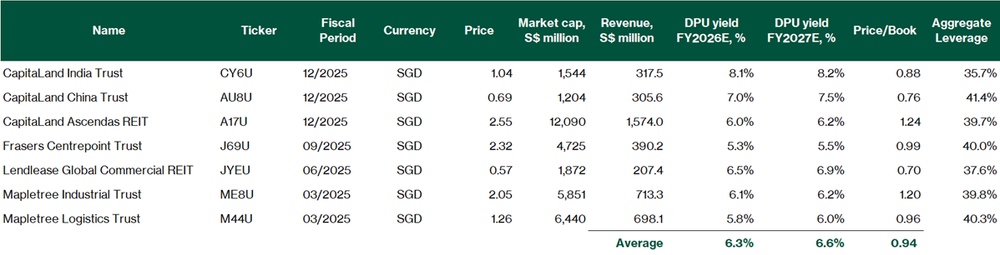

Currently, CapitaLand India Trust is trading at S$1.04, implying FY2026E distribution yield of 8.1%. This is relative more attractive than the comparables’ average FY2026E distribution yield of 6.3%.

In terms of P/B ratio, CapitaLand India Trust is trading at a discount to its book value, at P/B 0.88x. This is also cheaper than the comparables’ average P/B of 0.94x.

We maintain our BUY rating with a target price at S$1.36. With a quality growth pipeline and data centre projects on track for completion in 2026-2027, we expect upside potential to our estimates on their FY2027E DPU growth. Specifically, ITPH and Chennai Data Centre are contributing from mid-2026. Tower 2 Navi Mumbai will come online 4Q26.

Click here to download the full report.

Related links:

- CapitaLand India Trust share price and share price target

- CapitaLand India Trust dividend history and forecast

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in CapitaLand India Trust.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments