ComfortDelGro worth a look for income? Dividend yield rises above 6% after share price weakness

Stocks

By Ng Hui Min • 12 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

ComfortDelGro’s yield has risen above 6% after share price weakness. We look at its dividend, cash flow and key risks for income investors.

What happened?

ComfortDelGro’s dividend yield has risen above 6%.

The higher yield comes after its share price weakened, even though the Group crossed S$5 billion in revenue for the first time in FY2025, grew its profit, and raised its total dividend to 8.5 cents per share.

We had previously highlighted ComfortDelGro as one of the more balanced dividend stocks among Singapore blue chips offering yields above 5%, supported by its earnings growth and expanding overseas operations.

We also spoke with Group CFO Christopher White recently in our kopi-C interview, where he shared how the market may still be underappreciating ComfortDelGro’s transformation into a global multi-modal transport group.

However, year-to-date, ComfortDelGro is down 13.5% while STI is up 6.9% as of 8 Jun 2026.

In our Beansprout community, investors have been asking whether ComfortDelGro looks more attractive as a dividend stock after the recent share price weakness.

In this article, we take a closer look at why ComfortDelGro’s share price has underperformed, what stood out from its recent updates, and whether it still makes sense for dividend investors.

Why has ComfortDelGro's share price underperformed the STI?

The headline numbers look healthy at first glance, with revenue, profits and dividends all moving higher.

However, investors appear to be looking beyond the headline growth and focusing on several concerns beneath the surface.

#1 — Free cash flow has been negative

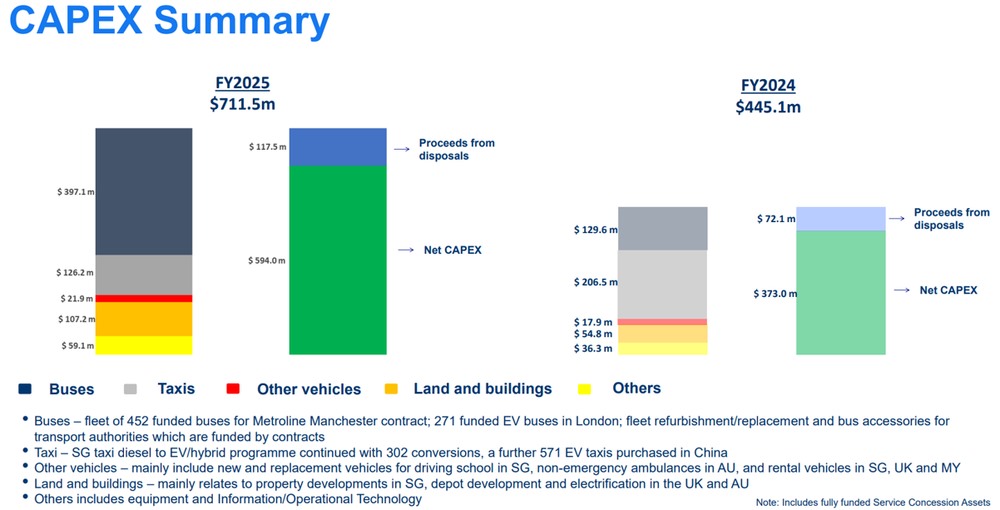

The first concern is free cash flow, which is the cash left after a company spends on capex to maintain and grow its business.

This matters for dividend investors because dividends are ultimately paid in cash, not accounting profits.

ComfortDelGro has been investing heavily. In FY2025, net operating cash flow was S$451.3 million, while net capex came in at about S$594 million after disposal proceeds and fully funded Service Concession Assets. This resulted in free cash flow of approximately negative S$59 million before acquisitions and debt servicing.

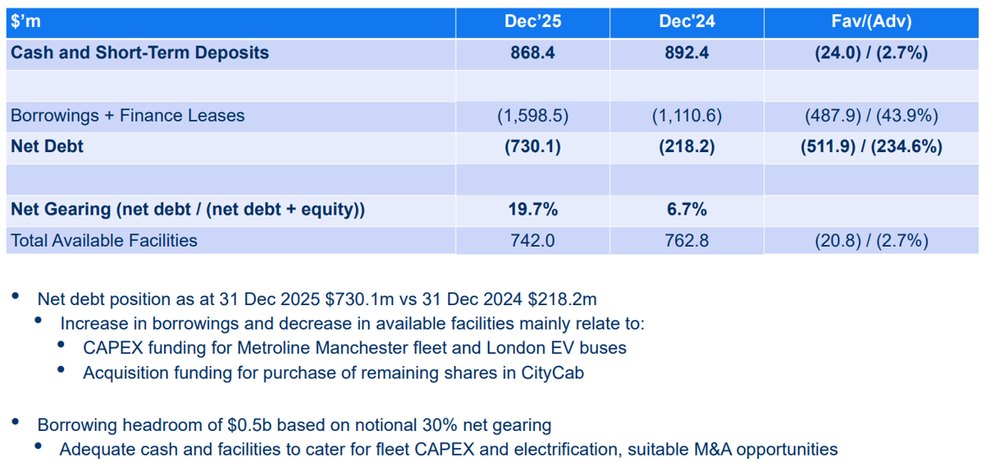

At the same time, the Group spent S$49 million on acquisitions in FY2025, after deploying S$604.5 million in FY2024. As a result, net debt rose from S$218.2 million at end-2024 to S$730.1 million at end-2025.

Net gearing also increased from 6.7% to 19.7% in one year. While this remains below management’s internal limit of 30%, the balance sheet has clearly become more leveraged.

For income-focused investors, the key question is whether ComfortDelGro can keep supporting its 80% payout ratio if free cash flow remains tight and debt continues to rise.

#2 — Taxi and private hire remains under pressure

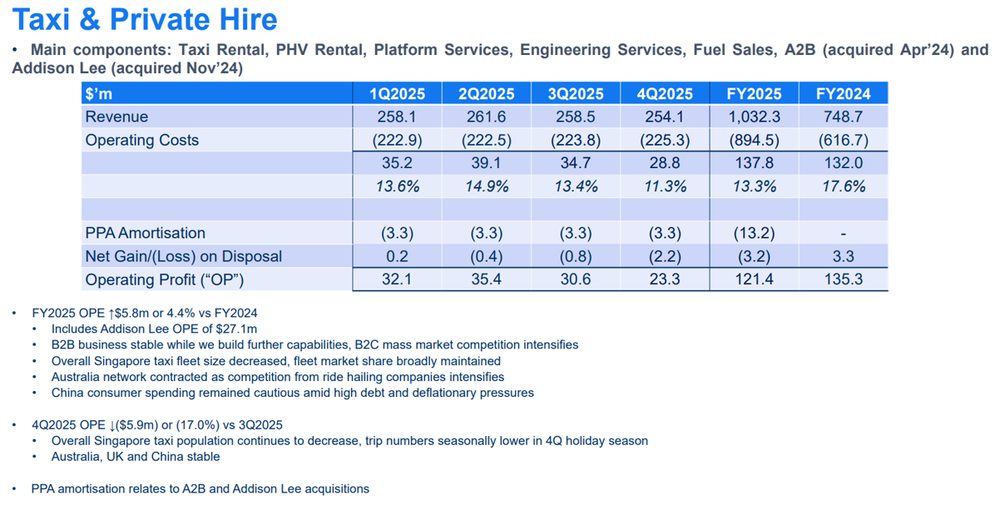

The second concern is ComfortDelGro’s taxi and private hire business, which continues to face structural headwinds.

Revenue from the segment rose to S$1.03 billion in FY2025, helped by a full-year contribution from the A2B Australia and Addison Lee acquisitions.

However, profitability was less impressive. Operating profit excluding purchase price allocation amortisation rose only modestly, while operating margin fell from 17.6% in FY2024 to 13.3% in FY2025.

This suggests that the new overseas businesses are lower-margin, while the segment also continues to face competition from ride-hailing and softer consumer demand across Singapore, Australia and the UK.

The weakness was more visible in Q4 2025, when segment operating profit excluding PPA fell 17% quarter-on-quarter to S$28.8 million.

In our kopi-C interview, CFO Christopher White also highlighted that the challenge is not only competition, but also a shortage of drivers. In Singapore, taxi and private hire drivers must be at least 30 years old and Singapore citizens, which limits the available driver pool for the industry.

#3 — Acquisitions have raised execution risk and leverage

The third concern is execution risk from ComfortDelGro’s recent acquisitions.

The Group has been active on the M&A front

It acquired CMAC in February 2024, A2B Australia in April 2024, and Addison Lee in November 2024.

It also bought out the remaining minority stake in CityCab in 2025 for S$119.2 million.

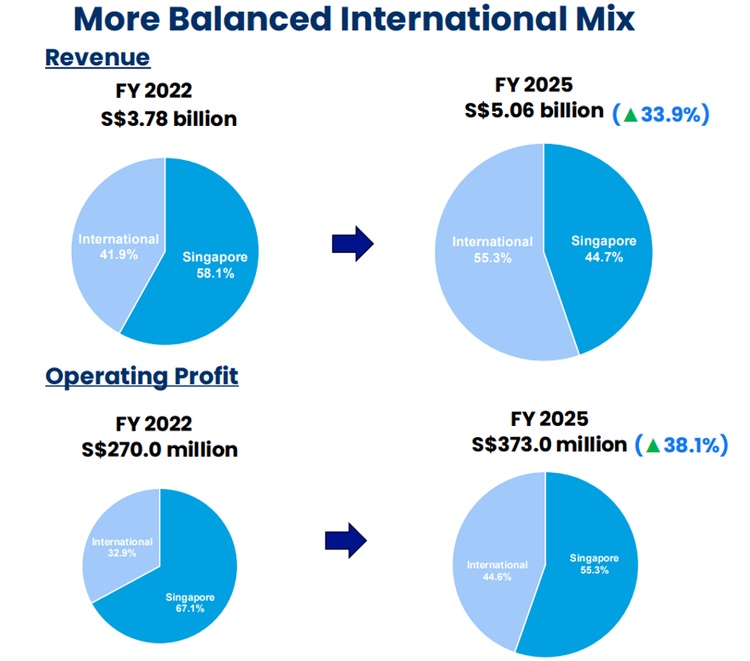

These deals have changed ComfortDelGro’s business mix. Overseas revenue now makes up 55.3% of total revenue, up from 49.1% in FY2024.

However, the expansion has also increased leverage.

Total borrowings and finance leases rose from S$1.11 billion to S$1.60 billion, while net interest expense increased from S$6.4 million in FY2024 to S$22.3 million in FY2025.

Reported profits were also affected by purchase price allocation amortisation, a non-cash accounting charge linked to acquired intangible assets, which added S$15.6 million in costs in FY2025.

For now, investors appear to be waiting for clearer evidence that these acquisitions can deliver stronger margins and cash flow.

The integration of Addison Lee is still at an early stage, and management has said the focus remains on extracting efficiencies from its point-to-point transport portfolio.

#4 — Inspection and testing had a one-off boost

The fourth concern is that one of ComfortDelGro’s strongest FY2025 earnings drivers may not repeat.

Its Inspection & Testing Services segment, which includes VICOM, saw operating profit jump 56.1% year-on-year to S$54.0 million in FY2025.

This was mainly driven by the surge in On-Board Unit (OBU) installations for Singapore’s ERP 2.0 project.

However, ComfortDelGro has guided that this revenue stream is expected to taper progressively in 2026 as OBU installations are substantially completed.

This creates a profit headwind for FY2026, even if other parts of the business continue to improve.

#5 — Loss of Singapore bus tenders

Another watch point is ComfortDelGro’s loss of recent Singapore bus tenders.

SBS Transit has lost the Jurong West and Tampines bus packages, with Tampines to be handed over to Go-Ahead Singapore from July 2026.

The estimated earnings impact is manageable, at about S$7.4 million annually or around 1.4% of FY2026 earnings forecasts.

However, the trend bears watching, as SBS Transit’s share of Singapore’s bus market has declined from about 62% at its peak to around 57%.

The next key tender is the Serangoon-Eunos package, where investors will be watching whether ComfortDelGro can defend its domestic bus market share.

What stood out from ComfortDelGro's FY2025 results?

Despite the share price weakness, ComfortDelGro's FY2025 results had several genuine bright spots worth highlighting.

These are worth looking at, especially for investors considering the stock for income.

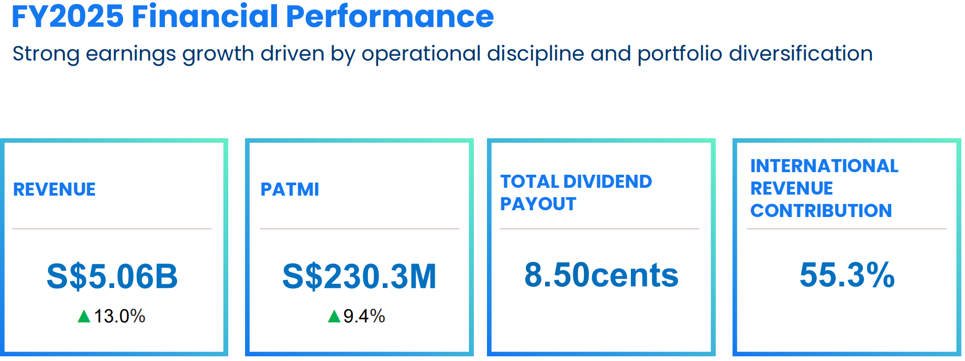

#1 — Revenue crossed S$5 billion for the first time

ComfortDelGro’s FY2025 revenue rose 13.0% year-on-year to S$5.06 billion, crossing the S$5 billion mark for the first time.

A key driver was its growing overseas business.

International operations contributed 55.3% of total revenue in FY2025, up from 49.1% in FY2024.

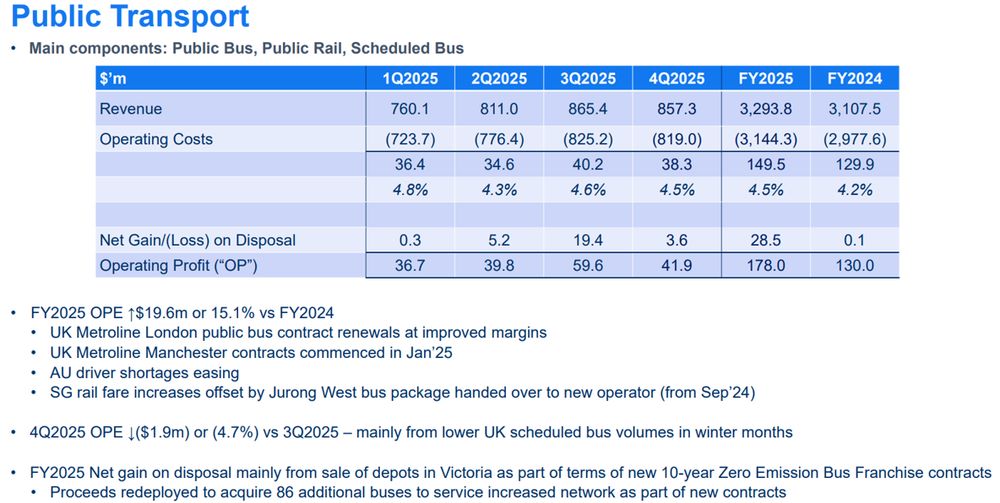

#2 — UK Public Transport delivered strong profit growth

The standout performer in FY2025 was ComfortDelGro’s Public Transport segment.

Operating profit rose 36.9% year-on-year to S$178.0 million, supported by better-margin bus contract renewals in London and the start of new Metroline Manchester contracts in January 2025.

In Australia, the segment also benefited from new 10-year Zero Emission Bus Franchise contracts in Victoria, which began in July 2025.

The Stockholm rail joint venture started full operations in November 2025 and should contribute a full year of earnings in 2026.

ComfortDelGro has also guided that London public bus contract renewals are expected to continue at improved margins, which may help offset inflationary cost pressures.

#3 — Second half showed improving momentum

ComfortDelGro’s earnings momentum improved in the second half of FY2025.

PATMI rose to S$124.3 million in 2H2025, up 17.3% from S$106.0 million in 1H2025.

This was partly supported by the ramp-up in OBU installations and seasonal strength from CMAC during the summer months.

However, improved UK public transport contracts also contributed, suggesting that the Group’s core operations were gaining traction as the year progressed.

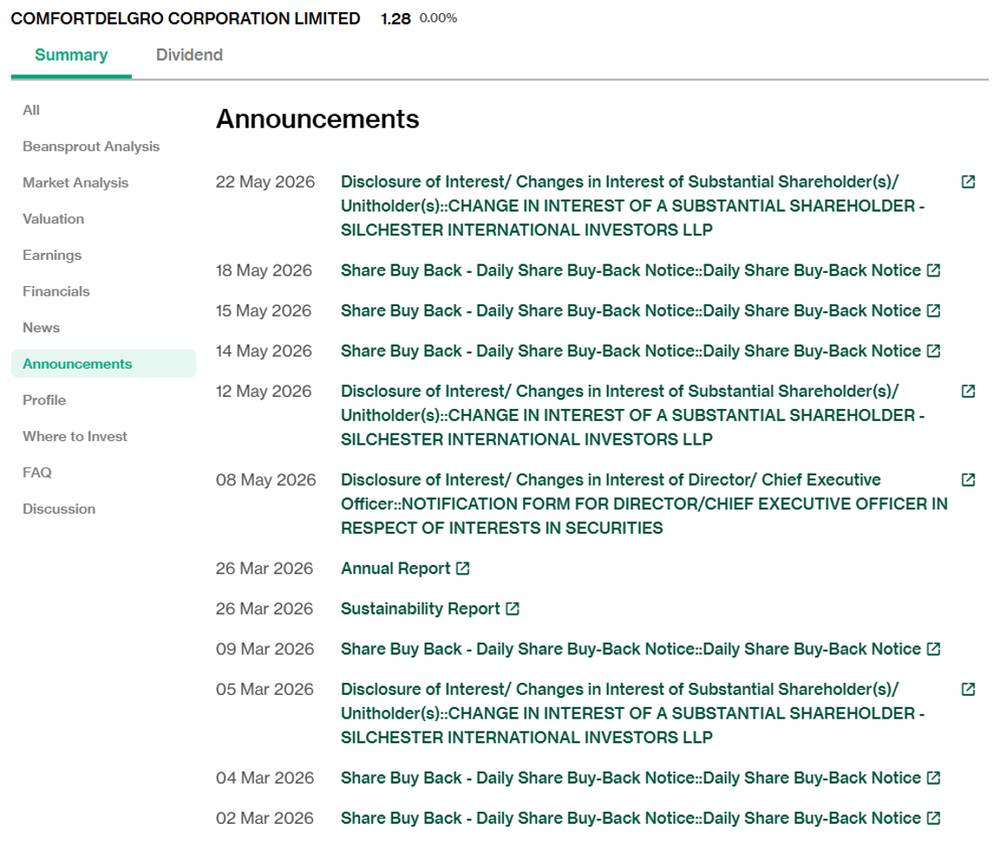

#4 — Silchester has built its stake above 9%

Another development that has caught investors’ attention is the buying by Silchester International Investors.

Silchester is a London-based fund manager known for its long-term value investing approach in international equities.

Its accumulation of ComfortDelGro shares has been notable. After crossing the 5% threshold in January 2026, Silchester raised its stake above 6% in February, 7% in March, 8% in May, and then 9.087% after further purchases on 21 May.

The pace of buying has been faster than its previous accumulation cycle in 2023 to 2024.

While this does not guarantee future share price performance, it suggests that a long-term institutional investor sees value in ComfortDelGro at current levels.

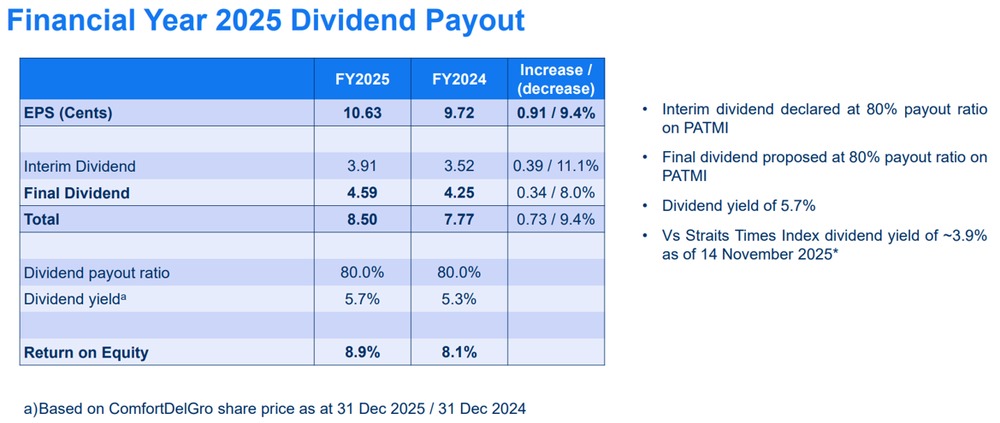

#5 — ComfortDelGro raised its dividend to 8.5 cents per share, maintaining its 80% payout commitment

ComfortDelGro increased its total dividend from 7.77 cents in FY2024 to 8.5 cents in FY2025.

This comprises an interim dividend of 3.91 cents and a final dividend of 4.59 cents.

Both dividends were based on an 80% payout ratio on PATMI.

Based on ComfortDelGro's share price of around S$1.29 as of 8 June 2026, this represents a trailing dividend yield of approximately 6.6%.

According to Factset, consensus is expecting a FY2026 dividend per share of S$0.078. This would represent a potential forward dividend yield of approximately 6.0%.

Is ComfortDelGro still attractive as a dividend stock?

At around S$1.29, ComfortDelGro offers a trailing dividend yield of about 6.6%, based on its FY2025 dividend of 8.5 cents per share.

This is higher than STI’s current dividend yield of around 3.4%.

The key support for the dividend is the public transport business.

ComfortDelGro’s contracts in Singapore, the UK and Australia are largely long-term and government-backed, providing a more resilient earnings base.

In Singapore, the Group earns a stable per-kilometre service fee, while the Jurong Regional Line could provide another growth driver when it begins full operations from 2027.

ComfortDelGro has also maintained its 80% payout ratio through a period of acquisitions and balance sheet expansion, showing management’s commitment to shareholder returns.

However, we would not look at the dividend yield alone.

The first watch point is free cash flow.

ComfortDelGro’s FY2025 free cash flow was negative after heavy capital expenditure of S$510.3 million, so investors may want to see whether cash flow improves as the fleet investment cycle normalises.

The second is the tapering of Inspection and Testing earnings.

The ERP 2.0 OBU installation project gave FY2025 earnings a meaningful boost, but this contribution is expected to decline in 2026.

The third is the taxi and private hire segment.

The Singapore taxi fleet continues to shrink, while competition and softer demand in Australia and the UK remain a drag. Segment margins were also weakest in Q4 2025.

Overall, ComfortDelGro’s dividend yield looks more attractive after the share price decline, especially given the resilience of its public transport business.

However, for the stock to re-rate, we think investors will need to see clearer evidence of free cash flow recovery, stable margins from recent acquisitions, and less pressure from the taxi and private hire segment.

What would Beansprout do?

In my view, ComfortDelGro can still have a place in an income-focused portfolio, but investors may need to be patient.

At around S$1.29, ComfortDelGro offers a dividend yield of about 6.6%, supported by its 80% payout ratio and a more resilient public transport earnings base across Singapore, the UK and Australia.

That said, I would not look at dividend yield alone. If I am investing in a stock for dividend, I would also check for healthy free cash flow, a stable business, a consistent dividend track record, and a yield that meaningfully beats the risk-free rate.

ComfortDelGro could look interesting, with its attractive yield, stable public transport contracts and consistent dividend track record.

However, there are still areas to watch. Free cash flow remains tight after a heavy capex cycle, the ERP 2.0 boost from Inspection and Testing is expected to fade, and the taxi and private hire business remains under pressure.

Hence, while ComfortDelGro may appeal to investors focused on the Income Pot, I would prefer to see stronger free cash flow recovery and more evidence of sustainable earnings growth before turning more positive on the stock.

You can find out some of our investment ideas to capture opportunities in the market here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

Would you consider ComfortDelGro as an income stock at current prices, or would you wait for more clarity from the August results? Share with us in the comments below or in our Telegram group!

Planning to invest in ComfortDelGro? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments