DBS profit rises 1% and declares S$0.81 in total dividends in 1Q26: Our Quick Take

Stocks

By Gerald Wong, CFA • 30 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

DBS reported a 1% increase in profit and maintained its 1Q26 ordinary dividend of S$0.66, alongside a S$0.15 capital return, bringing total dividends to S$0.81.

DBS 1Q26 earnings and dividend highlights

DBS has announced its earnings for first quarter of 2026. Key highlights include:

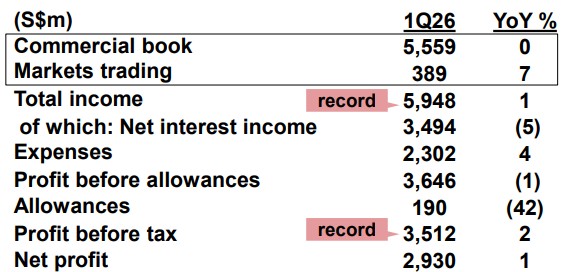

- 1Q 2026 pre-tax profit: SGD 3.51 billion (+2% year-over-year)

- 1Q 2026 net profit: SGD 2.93 billion (+1% year-over-year), a record start to the year

- Total income: SGD 5.95 billion, a new high (+1% year-over-year, +12% quarter-on-quarter)

- Return on equity: 17.0%

- Ordinary dividend of 66 cents per share for 1Q 2026

- Capital return dividend of 15 cents per share for 1Q 2026

What we learnt from DBS 1Q26 earnings

#1 - Total income at record high despite continued rate headwinds

1Q26 net profit rose 1% year-on-year to S$2.93 billion as record fee income, stronger treasury customer sales and higher markets trading income more than offset the impact of lower interest rates and a stronger Singapore dollar.

Compared to the previous quarter, net profit was 24% higher.

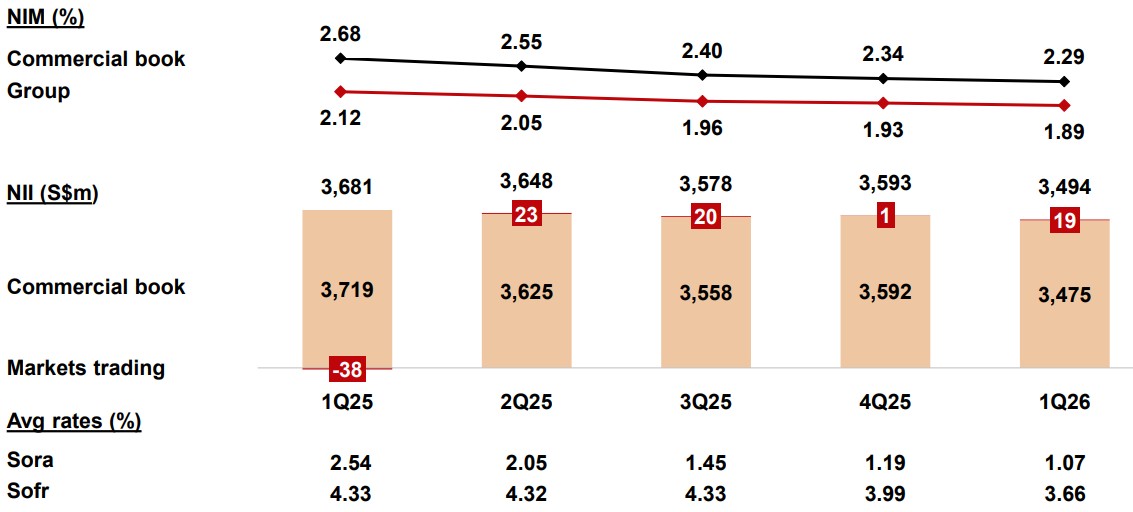

Group net interest income declined 5% year-on-year to S$3.49 billion, as net interest margin (NIM) narrowed 23 basis points (0.23%) to 1.89% on lower SORA and HIBOR rates and a stronger Singapore dollar.

On a quarter-on-quarter basis, NIM compressed only four basis points (0.04%) and group net interest income was little changed on a day-adjusted basis, as rate pressures were offset by hedging activities and balance sheet growth.

Loans grew S$25 billion (+6% year-on-year) in constant-currency terms to S$453 billion, led by corporate loans.

On a quarter-on-quarter basis, loans rose 2% or S$8 billion, with broad-based growth in non-trade corporate loans across the region.

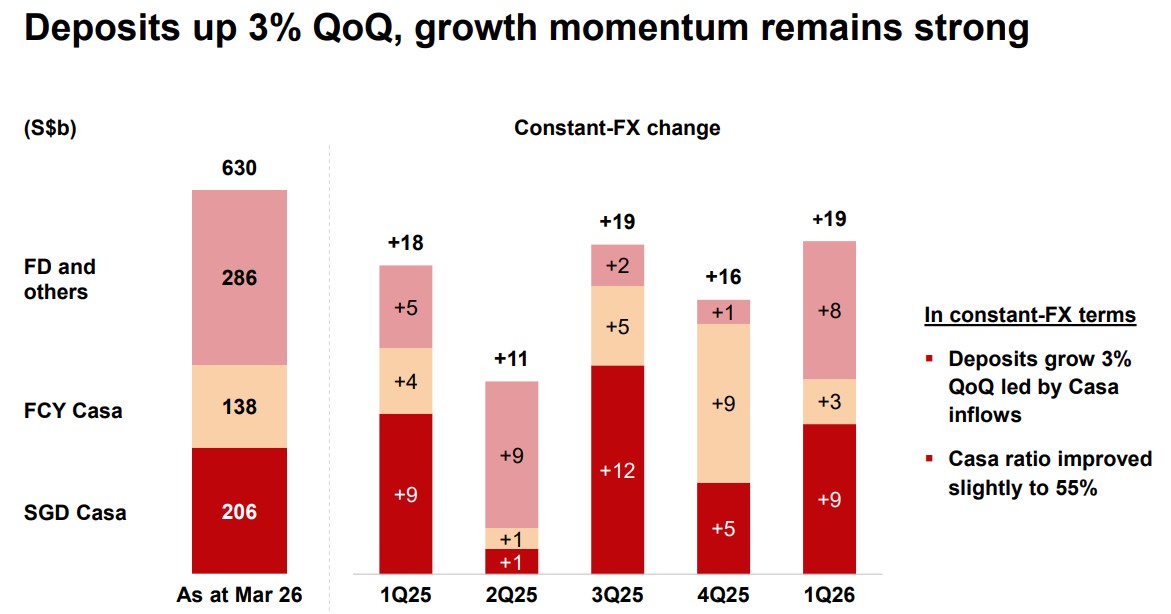

Deposits rose S$66 billion (+12% year-on-year) to S$630 billion, with more than two-thirds of the increase coming from CASA balances.

Compared to the previous quarter, deposits grew 3% or S$19 billion, and the CASA ratio improved slightly to 55%.

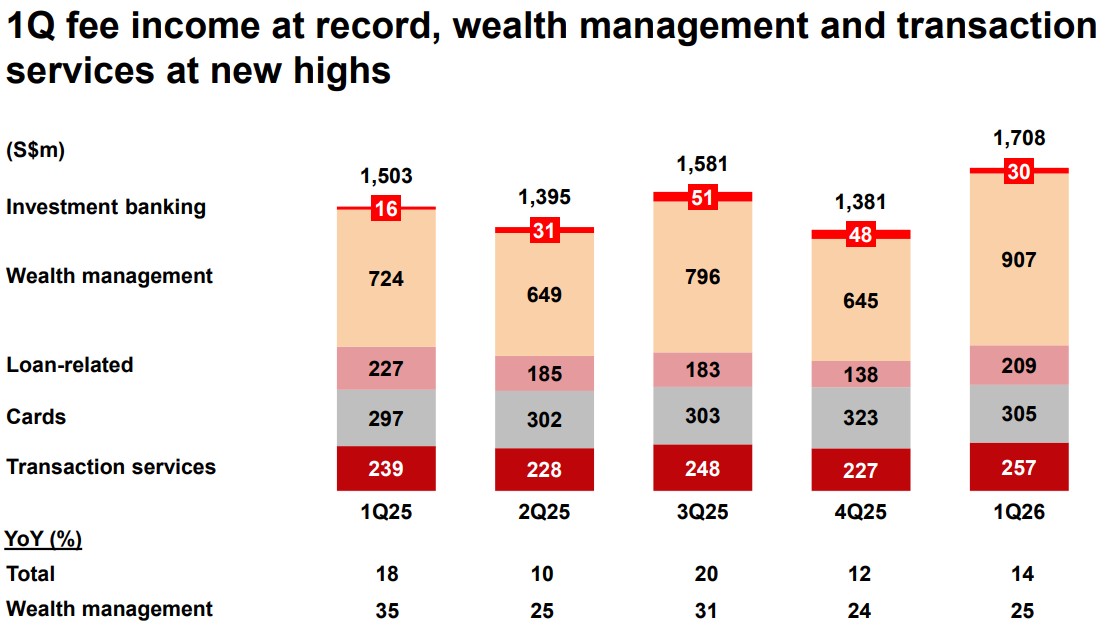

#2 - Record fee income led by wealth management

Commercial book net fee income rose 16% year-on-year (and 35% quarter-on-quarter) to a record S$1.48 billion in 1Q26.

Wealth management fees reached a record S$907 million, driven by higher investment product sales and bancassurance. The wealth segment's total income hit a record S$1.59 billion, with assets under management at S$492 billion.

Transaction services fees were also at a new high of S$257 million, while loan-related fees were higher at S$209 million. These were partially offset by lower investment banking and card fees compared to the previous quarter.

Commercial book other non-interest income rose 10% year-on-year to S$602 million, driven by record treasury customer sales to wealth management and corporate customers.

Markets trading income rose 7% year-on-year to S$389 million, supported by lower funding costs and improved trading conditions, more than doubling from the prior quarter.

#3 - Asset quality resilient, specific allowances normalised

DBS' non-performing loan (NPL) ratio remained stable at 1.0%.

Non-performing assets fell 3% from the previous quarter to S$4.72 billion, as new NPA formation was low and more than offset by repayments and write-offs.

Specific allowances eased significantly to S$157 million in 1Q26 (or 14 basis points of loans), down sharply from S$415 million in 4Q25 when real estate-related exposures had driven a spike.

General provisions remain prudent, with allowance coverage at 131% (or 200% after considering collateral).

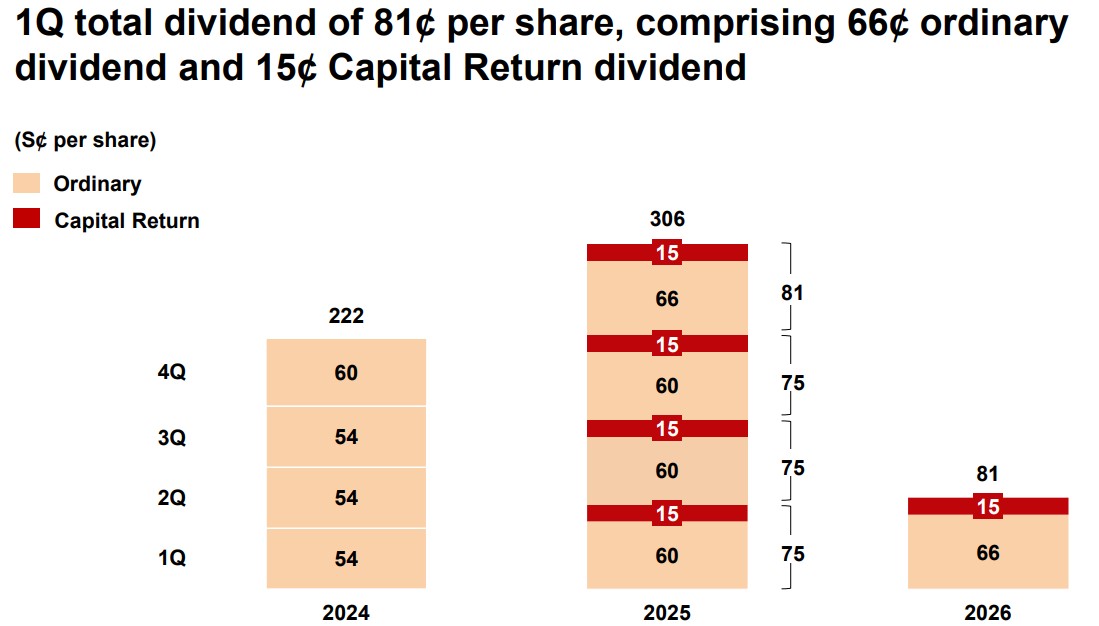

#4 - Dividend maintained at 81 cents per quarter

The board declared an interim dividend of SGD 66 cents per share and a Capital Return dividend of SGD 15 cents per share for 1Q 2026, in line with the previous quarter. This brings the annualised total dividend to S$3.24 per share.

Management has previously reaffirmed that the capital return dividend of 15 cents per quarter will be maintained through 2026 and 2027.

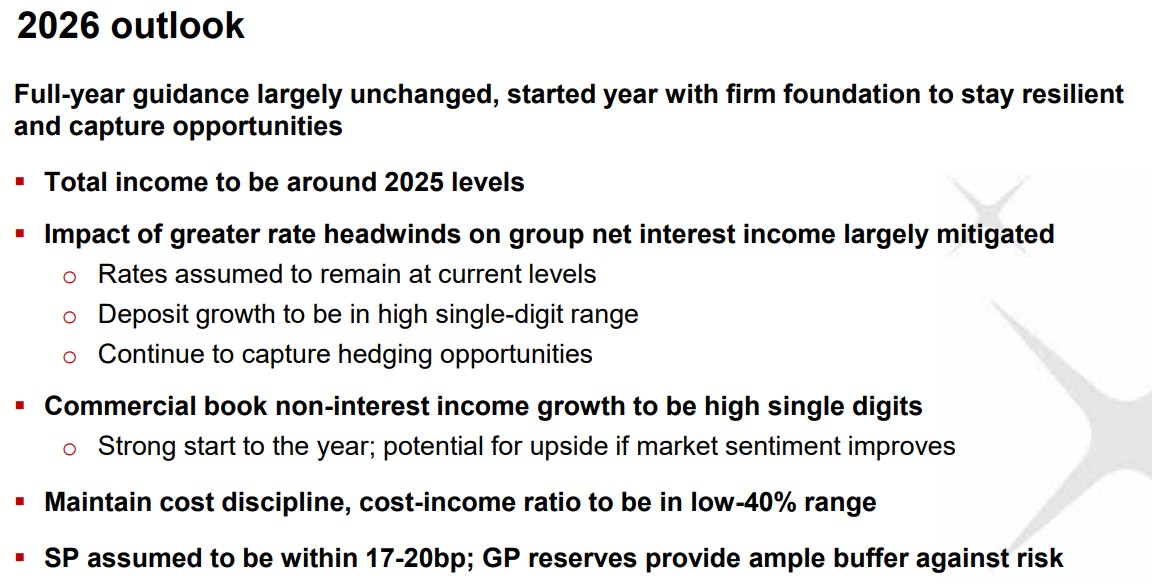

#5 - Full-year 2026 guidance largely unchanged

DBS maintained its FY2026 guidance of total income to be around 2025 levels despite continued rate headwinds and heightened geopolitical uncertainty.

Management now assumes interest rates remain at current levels (versus its earlier assumption of two Fed rate cuts), with the impact of greater rate headwinds on group net interest income largely mitigated by deposit growth (now expected to be in the high single-digit range) and ongoing hedging activities.

Commercial book non-interest income is still expected to grow at high single-digit rates, with management flagging potential upside if market sentiment improves given the strong start to the year.

The cost-income ratio is expected to remain in the low-40% range, while specific provisions are assumed at 17–20bp, with general provision reserves providing an ample buffer against risk.

CEO Tan Su Shan flagged the Iran war and its potential second-order effects as adding uncertainty to the outlook, but noted that DBS' stress tests indicate the credit portfolio remains sound, with limited direct exposure to the Middle East.

Beansprout’s Quick Take on DBS earnings

DBS delivered a strong start to 2026, with 1Q net profit up 1% year-on-year to S$2.93 billion and total income reaching a record S$5.95 billion.

Record wealth management performance, robust deposit growth and stronger markets trading income more than offset the drag from lower interest rates.

Importantly, return on equity of 17.0% remains healthy and asset quality looks resilient, with specific allowances normalising sharply from the elevated 4Q25 level.

Management's full-year 2026 guidance is largely intact, with rate headwinds now expected to be largely mitigated by hedging and deposit growth even under a "higher-for-longer" rates assumption.

DBS declared a 1Q total dividend of 81 cents, which translates to an annualised total dividend per share of $3.24. Based on the closing price of S$56.56 (as of 29 April 2026), this implies a dividend yield of about 5.7%.

For income investors, DBS still offers a higher forward dividend yield among the three local banks, stronger franchise quality and market leadership.

DBS currently trades at a price-to-book valuation of about 2.3x, above its historical average of 1.5x.

Related links:

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in DBS.

Follow us on Telegram, Youtube, Facebook and Instagram to get the latest financial insights.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments