Digital Core REIT: Stable distributable income amid positive leasing momentum

REITs

By Goh Lay Peng • 23 Apr 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

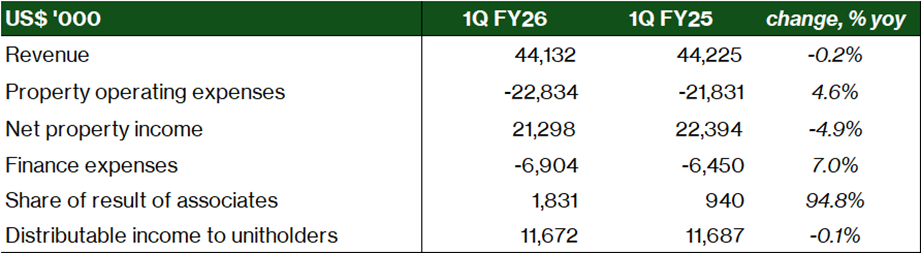

Digital Core REIT reported resilient distributable income amid positive leasing momentum. Distributable income to unitholders was US$11.67 million in 1Q FY2026, -0.1% year-on-year.

Stable distributable income despite margin pressure

Revenue was flat at US$44.1 million in 1Q FY26 versus US$44.2 million in 1Q FY25 (-0.2% year-on-year). The near-unchanged revenue reflects steady contributions from the in-service portfolio, which maintained 97% occupancy.

Net property income (NPI) declined 4.9% year-on-year to US$21.3 million in 1Q26 (1Q25: US$22.4 million). The compression was driven by a 4.6% increase in property expenses to US$22.8 million.

The higher expenses partially reflect additional costs from the expanded Frankfurt and Osaka portfolio, as well as higher utilities costs. NPI margin for 1Q FY26 stands at approximately 48%, down from approximately 51% in 1Q FY25.

That said, Digital Core REIT is mostly insulated from rising energy costs, as more than 85% of the rental revenue is structured on pass-through lease agreements, where the customer is responsible for all utility expenses.

For the leases without full pass-through, Digital Core REIT generally lock in fixed utility pricing. In addition, Digital Core REIT has right to reprice customer contracts in the event that utility costs increase by more than 5%.

One notable positive was the significant improvement in share of results from associates (Osaka assets), which grew 94.8% year-on-year to US$1.8 million in 1Q26. This reflects improving occupancy and rents from Digital Osaka 2 and Digital Osaka 3, which were 99.1% occupied as at 31 March 2026.

Near full portfolio occupancy with positive rental revision

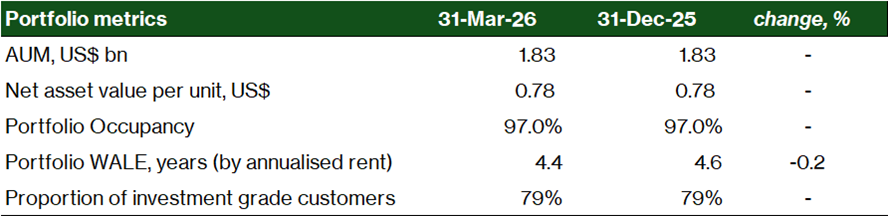

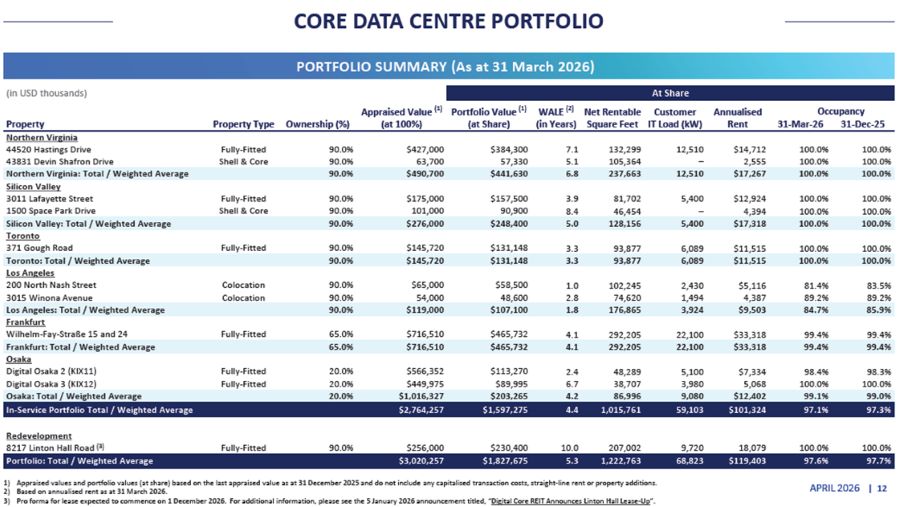

With focused asset management, Digital Core REIT has built a quality portfolio with high income visibility. Weighted average lease expiry (WALE) was relatively stable at 4.4 years at 31 March 2026, from 4.6 years as at 31 December 2025.

Committed portfolio occupancy was unchanged at 97% as at 31 March 2026.

Digital Core REIT's in-service portfolio maintained near-full occupancy of 97% as at 31 March 2026, unchanged from 31 December 2025. The high occupancy across most assets reflects the critical nature of data centre infrastructure and the difficulty of moving hyperscale tenants who have made significant investments in their deployments.

In 1Q FY26, Digital Core REIT signed new and renewal leases totalling US$3 million in annualised rent at share, achieving a very strong cash rental reversion of +44%. This positive reversion reflects the significant improvement in market rents across key markets, particularly Northern Virginia where pricing has risen from US$95/kW/month in 2023 to US$235/kW/month in 2026.

With 90% of the portfolio re-leased, there are limited future mark-to-market opportunities.

As at 31 March 2026, asset under management (AUM) remains unchanged, at US$1.83 billion.

Los Angeles remains the only submarket with meaningful vacancy at 84.7% occupancy. As noted in prior periods, this reflects the multi-tenant colocation nature of the two Los Angeles assets, which are more susceptible to tenant churn. However, we note that Monterey Park's proposed permanent ban on data centres may support occupancy and rents in the medium term by constraining new supply in the broader Los Angeles area. Separately, colocation facilities in Los Angeles also represents the most exposure to leases with no pass through on utilities.

Updates on progress of Linton Hall

The Linton Hall refurbishment remains a key near-term catalyst. The fully-fitted 207,002 sq ft facility in Northern Virginia (8217 Linton Hall Road) is currently undergoing a comprehensive upgrade, including a new roof, high-security perimeter fence, enhanced chiller plant efficiency, new battery room cabinets, and exterior vapor barrier sealing.

Upon completion, the refurbishment will expand sellable capacity by 13%, contributing to a 35% increase over the previous net rent.

The new lease with a global cloud service provider is a 10-year contract expected to generate US$18.1 million in annualised rent, with the lease commencement on 1 December 2026. Including Linton Hall, total portfolio annualised rent at share would rise to US$119.4 million.

We estimate that the full contribution from Linton Hall in FY2027 will be a significant DPU uplift driver. Accounting for the new lease alongside the existing portfolio, we project DPU to increase to approximately 3.76 US cents in FY2027E.

Linton Hall lease-up at 20% positive rental revision. After six months of downtime, Digital Core REIT successfully lease-up the space at 20% positive rental revision. The new lease is a 10-year contract with a global cloud service provider. It is expected to generate US$13.3 million in net property income, representing 15% of the Trust’s FY2025 net property income.

Currently undergoing a US$40 million redevelopment plan, the lease will commence on 1 December 2026.

Healthy balance sheet

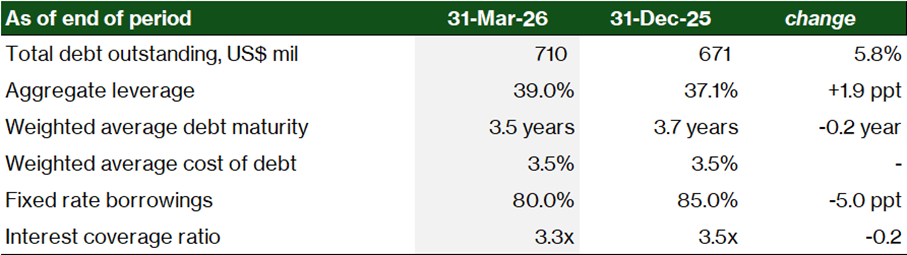

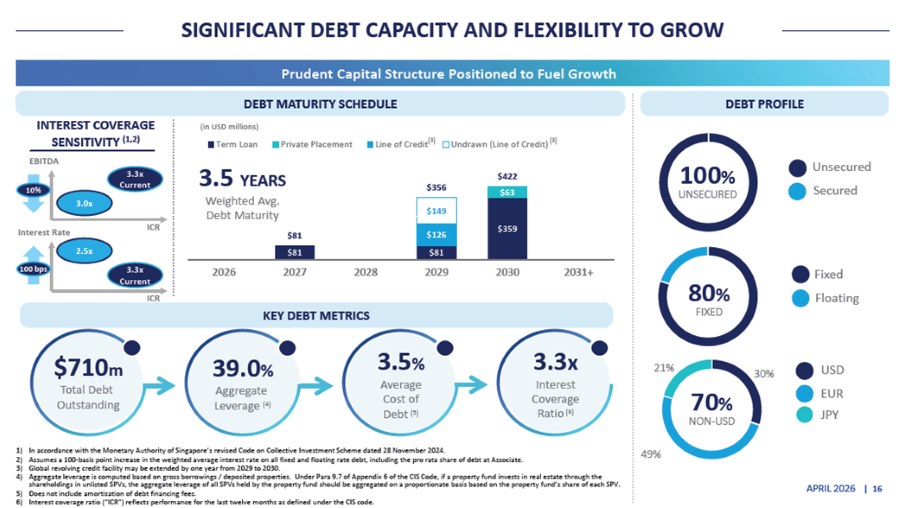

Total debt increased by 5.8% to US$710 million, primarily reflecting the new debt drawdown to fund capital expenditure, share buyback and dividend payment.

Aggregate leverage increased to 39.0% as at 31 March 2026, from 37.1% as at 31 December 2025.

Significant debt headroom of US$428 million remains available before reaching the 50% aggregate leverage limit.

Digital Core REIT maintains a conservative 80% fixed rate debt mix and a weighted average debt maturity of 3.5 years, providing substantial protection against rising interest rates.

Average cost of debt remains attractive at 3.5%, with interest coverage ratio of 3.3x based on the last twelve months.

Digital Core REIT’s debt maturity profile is termed-out, with no refinancing requirements in 2026 and the next major maturity to happen only in 2029 (US$356m), mitigating near-term interest rate and liquidity risks.

Outlook stays positive with strong demand across key markets

Data centre market fundamentals remain favourable, underpinned by AI-driven demand and constrained new supply. AI workloads are expected to grow 3.5x between 2025-2030, and by 2027, AI inference is projected to overtake AI training as the dominant workload, favouring the latency-sensitive, well-connected facilities in Digital Core REIT’s portfolio.

Northern Virginia

Northern Virginia remains the world's largest data centre market, with vacancy close to zero and wholesale pricing rising to US$235/kW/month in 1Q26, up from US$95/kW/month in 2023. The Virginia General Assembly's 2026 session adjourned without resolving the fate of the data centre tax exemption (estimated at US$1.6–1.9 billion in annual value), deferring this to a special session in late April 2026. Incremental regulatory reforms passed include mandatory impact assessments, stricter diesel generator standards, and water use transparency requirements. Prince William County is also tightening zoning approvals for new data centre developments, which will further limit new supply in this key submarket.

Digital Core REIT's 44520 Hastings Drive facility in Northern Virginia is 100% occupied with a WALE of 7.1 years, and the Linton Hall redevelopment is on track to add meaningful capacity at materially higher rents.

Silicon Valley

Silicon Valley Power's Santa Clara grid hit a critical inflection point in 1Q26, with over 500 MW of planned demand unable to be serviced until a US$450 million upgrade completes in 2028. This near-term power constraint is pushing some demand to San Jose but also keeps vacancy near zero in the market. Wholesale pricing reached US$265/kW/month in 1Q26, up from US$135/kW/month in 2023. Digital Core REIT's two Silicon Valley assets are 100% occupied.

Frankfurt

Germany adopted a National Data Centre Strategy in March 2026 targeting a doubling of national data centre capacity and a quadrupling of AI and HPC capacity by 2030. This pro-growth policy framework, combined with grid connection reforms and trade tax amendments favouring municipalities that host data centres, positions Frankfurt as a key beneficiary.

Digital Core REIT's Frankfurt portfolio is 99.4% occupied with a WALE of 4.1 years and annualised rent of US$33.3 million — the single largest geographic contribution at 33% of the in-service portfolio by annualised rent.

Osaka

Osaka continues to attract significant capital investment from multinational operators. KDDI launched a major D2C liquid-cooled GPU deployment for Google's Gemini AI model in January 2026, and EdgeConneX is developing a new 200 MW campus. CapitaLand Ascendas REIT has also entered Japan through an Osaka data centre acquisition. Digital Core REIT's Osaka assets are 99.1% occupied with healthy annualised rent of US$12.4 million.

Digital CORE REIT maintains a high-level strategy to double the asset under management over multiple years. Part of which will involve recycling North American assets to fund expansion in Asia Pacific.

Maintain BUY and target price at US$0.63

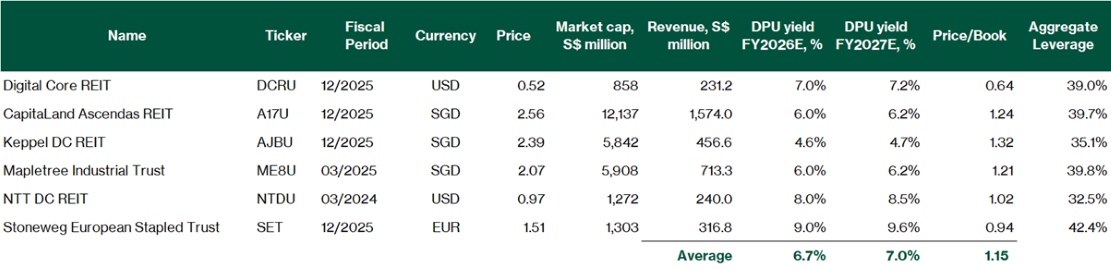

Digital Core REIT is trading at US$0.52, offering FY26 distribution yield of 7.0%.

In terms of P/B ratio, Digital Core REIT is trading at a steep discount to its book value, at P/B 0.64x. In comparison, Keppel DC REIT and NTT DC REIT are trading at P/B 1.32x and 1.02x.

We remain positive that Digital Core REIT’s valuation will converge with the peer valuation with improved income visibility and leasing of Linton Hall.

The unit buyback programme continued in 1Q FY26, with 7.1 million units repurchased at an average price of US$0.486. This capital allocation decision, buying back units at a substantial discount to net asset value (NAV), is distribution per unit (DPU) accretive (0.3% accretion) and reflects management's confidence in the intrinsic value of the Digital Core REIT.

Key re-rating catalysts include: (1) Linton Hall lease commencement in December 2026, adding meaningful DPU uplift; (2) continued positive rental reversions as leases roll in Northern Virginia and Silicon Valley where market rents have risen 100-200%; and (3) potential acquisitions from the sponsor's US$540 million ROFR pipeline and broader US$15 billion global platform.

Click here to download the full report.

Related links:

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in Digital Core REIT.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments