How I invest with clarity using the Four Pots of Wealth

Investing

By Gerald Wong, CFA • 24 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Here's how I invest with clarity using the Four Pots of Wealth, a practical framework for balancing liquidity, income, growth and opportunity.

Since starting Beansprout, the question I get asked most often is simple:

“Is this stock a buy?”

It’s a fair question as we all want clarity on our investment decisions.

But over the years, I’ve realised that the better question is not whether a stock is a buy. It’s how that stock fits into your overall portfolio.

Since launching Beansprout, I’ve also been forced to think much more intentionally about how I structure my own money to meet my unique life circumstances.

I’m self-employed, which means I need my portfolio to generate some passive income. At the same time, I still have a relatively long runway ahead of me, so I want exposure to long-term growth. And as a former analyst, I’ll admit, I still enjoy picking individual stocks and forming views.

Those goals may not be aligned with one another at the same time.

That’s when I started thinking differently. Instead of seeing my portfolio as one big pool of capital, I began organising it into separate pots, each with a specific role.

That was how the Four Pots of Wealth came about at Beansprout, a simple framework to help us think more clearly about how we structure money.

Building My Four Pots of Wealth

The Four Pots of Wealth starts by giving every dollar in my portfolio a specific role, instead of treating it as one big pool of money.

That matters because many investors keep everything in one mental bucket. When that happens, every market fall can feel like a threat to everything at once, from emergency savings to retirement plans, children’s education, and near term expenses.

That is often what leads to panic selling, one of the most damaging mistakes an investor can make.

I have seen investors who understand the theory still sell in downturns because their portfolio gave them no clear separation between money they may need soon and money they can leave invested for years.

The Four Pots of Wealth changes that.

Once my money is clearly allocated, a 30 percent drop in equities does not feel like a 30 percent hit to my entire financial life. It is simply a decline in one pot, the growth pot, which I have already set aside for the long term.

My liquidity pot stays stable in cash or low risk instruments. My income pot can continue generating distributions. There is no pressure to react.

That separation creates calm, and calm leads to better decisions.

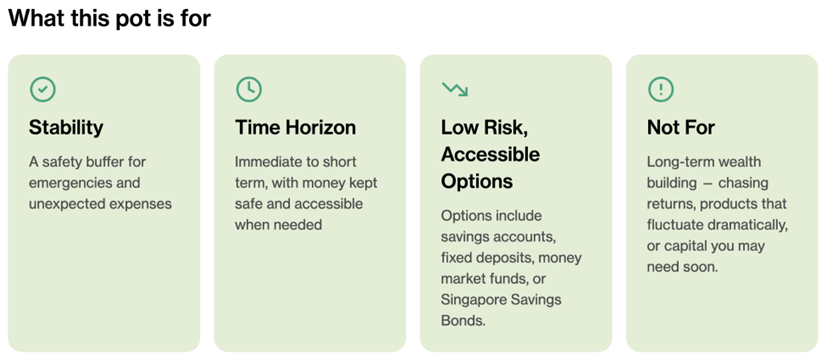

The Liquidity Pot

The Liquidity Pot is probably the least exciting part of my portfolio, but it is also one of the most important.

Its role is simple. It is there to protect me when life does not go according to plan.

For me, this usually means keeping three to six months of living expenses in cash or in low risk, accessible instruments such as savings accounts, fixed deposits, money market funds or Singapore Savings Bonds. I do not expect this pot to deliver high returns, and I am comfortable with that. Its purpose is not to grow quickly. Its purpose is to give me peace of mind.

When I know this buffer is in place, I do not have to worry about selling long term investments at the wrong time just to cover a short term need. Whether it is a temporary loss of income, a medical expense, or an unexpected repair at home, I know I have something set aside for moments like these.

That sense of security matters more than people sometimes realise. It is what allows me to stay patient with the rest of my portfolio, even when markets are volatile.

At the same time, I do not think this pot should be completely neglected. Just because it is not meant to generate high returns does not mean it should sit idle. I still want to manage it thoughtfully, whether that means comparing the best fixed deposit rates, looking at savings account options, or considering instruments like Singapore Savings Bonds and money market funds.

This pot may not feel exciting, but I have come to see it as the foundation for everything else. When this part of my finances is secure, I find it much easier to invest the rest of my portfolio with clarity and confidence.

Learn more about the Liquidity Pot here.

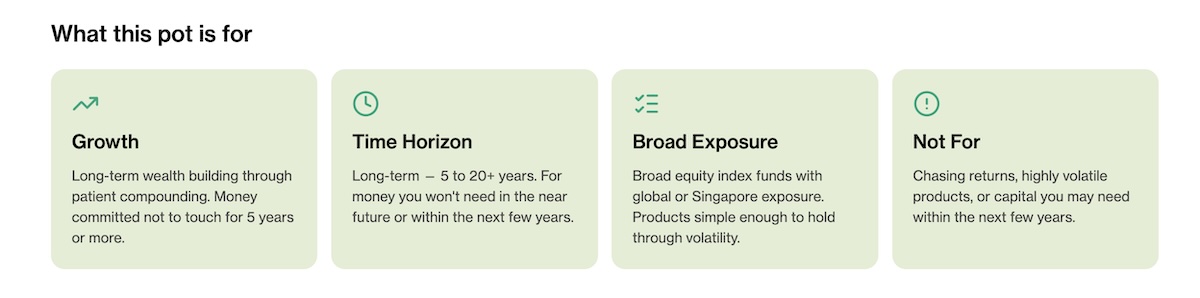

The Growth Pot

The Growth Pot is where I invest for the long term, with money that I do not expect to need for at least five years, and often much longer.

This is where I put broad equity funds, global index exposure, and other assets that I can genuinely hold through multiple market cycles without feeling the need to react to every headline or check prices every day.

What matters most in this pot is time. I accept that there will be short term volatility, because that is part of the price of earning higher long term returns.

This is also where the real power of compounding comes through. When returns are reinvested consistently over time, those gains begin to generate their own gains. It may not feel dramatic at first, but over the years, that snowball effect can become incredibly powerful.

That is why I try to keep the guiding principles here very simple. Diversify, keep it simple, and stay consistent.

Diversification matters because I do not want my long term progress to depend too heavily on any single company or market. Simplicity matters because the easier it is to understand what I own, the easier it is to stay invested when markets turn volatile. And consistency matters because compounding only really works when I give it the time and discipline to do its job.

In many ways, this is the part of my portfolio that reflects a philosophy Warren Buffett has spoken about for years, owning quality assets patiently and allowing time to do the heavy lifting.

Most of my long term wealth building happens in this pot. And one reason I place so much importance on the Liquidity Pot is that it gives me the financial and emotional stability to leave this Growth Pot untouched during downturns, so compounding can continue without interruption.

Learn more about the Growth Pot here.

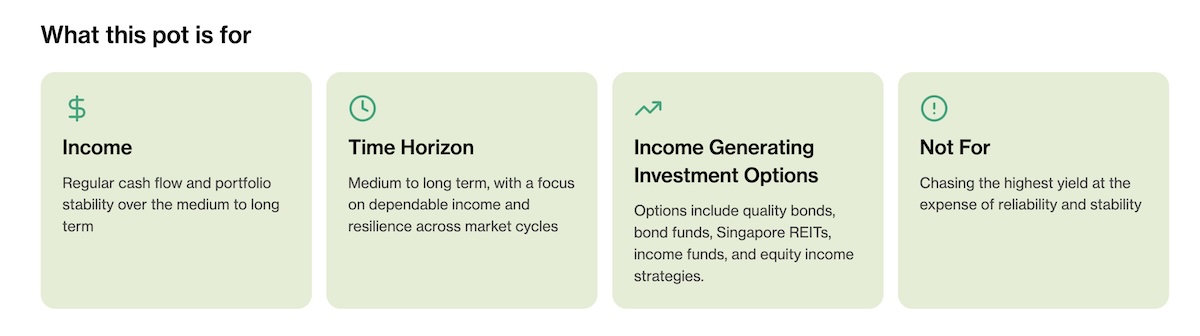

The Income Pot

The Income Pot plays a different role in my portfolio. It is there to provide regular cash flow, but also a greater sense of stability over the medium to long term.

This is where I tend to hold assets such as quality bonds, bond funds, Singapore REITs, income funds, and equity income strategies. The aim is to generate recurring dividends, coupons, and distributions, while generally taking on less volatility than pure equities.

I have come to see that this pot does more than one job. In normal market conditions, it helps to produce a stream of income. But during more uncertain periods, it also helps me stay grounded. It becomes an emotional anchor in the portfolio, especially when growth assets are under pressure.

That is why I think it is easy to get this pot wrong if I focus too much on headline yield alone.

The temptation is always to look for the highest yielding asset and assume that more income is better. But I have learnt that a very high yield can sometimes come with weaker resilience, whether that means greater price swings, more fragile cash flows, or distributions that are harder to sustain in a downturn.

When that happens, the Income Pot stops doing what I need it to do most.

So over time, I have become more focused on reliability than maximisation. I would rather earn a slightly lower but more dependable stream of income than reach for a higher yield that may be cut when conditions turn more difficult.

To me, the real purpose of this pot is not to squeeze out the last bit of yield. It is to build a base of income that I can count on across market cycles, and a part of the portfolio that helps me stay calm enough to keep the rest of my plan on track.

Learn more about the Income Pot here.

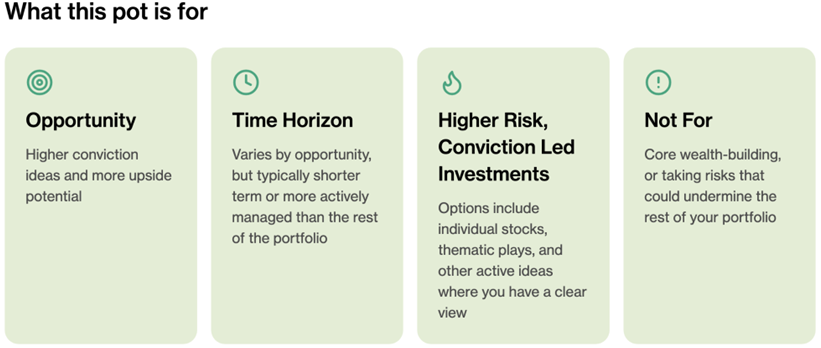

The Opportunity Pot

The Opportunity Pot is the most active part of my portfolio. It is where I place higher conviction ideas, positions where I feel I have a genuine view and am prepared to take a more active stance.

This may include individual stocks, thematic opportunities, or shorter term ideas that sit outside the steadier role of my other pots.

I also want to be honest about this part of the framework. If I look at the evidence objectively, most retail investors would probably do better over the long term by sticking to diversified funds rather than trying to pick individual winners. Stock picking can be rewarding at times, but it is also one of the easiest places for overconfidence to creep in quietly.

But I still think this pot has an important role.

The reality is that most of us will sometimes feel strongly about a particular idea and want to act on it. I know that is true for me too. Pretending that impulse does not exist does not make it go away. In fact, it can make it harder to manage well.

What I have found more helpful is to give that instinct a boundary.

By carving out a separate Opportunity Pot, I can express conviction in a controlled way without allowing it to spill into the rest of my portfolio. It gives me room to act, but within limits that I have already decided on in advance.

Those limits matter a lot. This pot has a fixed maximum size. I do not top it up from my Liquidity, Income, or Growth Pots under any circumstances. And I go into it knowing that this is the part of my portfolio where I am taking more risk, and where the odds may not always be in my favour.

From a textbook point of view, this may not be the most optimal part of the framework. But from a real life point of view, I think it is one of the most practical.

It allows me to act on conviction from time to time, while still protecting the rest of my portfolio from unnecessary damage.

Learn more about the opportunity pot here.

What does this actually look like in practice?

Let me illustrate with simple numbers.

Imagine starting with $100,000 in your early 30s, with each pot given a clear role from the start:

- $15,000 in the Liquidity Pot

- $20,000 in the Income Pot

- $10,000 in the Opportunity Pot

- $55,000 in the Growth Pot

From there, I commit to investing $1,000 each month. I allocate $550 to the Growth Pot, $250 to the Income Pot, $100 to the Opportunity Pot, and $100 to the Liquidity Pot.

Now assume the following long term returns for illustration purposes: 2% for the Liquidity Pot, 5% for the Income Pot, 8% for the Growth Pot, and 12% for the Opportunity Pot.

Over 20 years, this is what the portfolio could look like:

| Pot | Starting | Monthly | Return/Year | End Value (20 yrs) |

| Growth Pot | $55,000 | $550 | 8% | ~$595,000 |

| Income Pot | $20,000 | $250 | 5% | ~$157,000 |

| Opportunity Pot | $10,000 | $100 | 12% | ~$208,000 |

| Liquidity Pot | $15,000 | $100 | 2% | ~$44,000 |

| Total | $100,000 | $1,000 | ~$1,004,000 |

What stands out to me is that reaching $1 million is less about one big investment callpick, and more about having the right structure in place.

- The Liquidity Pot ensured I never had to sell during downturns.

- The Growth Pot did most of the heavy lifting through compounding.

- The Income Pot provided increasing stability and cash flow over time.

- The Opportunity Pot allowed me to express conviction without risking the entire plan.

Of course, this is only an illustration. Real life returns will vary, and the exact outcome will look different for every investor.

But that is really the point of the framework. The Four Pots of Wealth is not about predicting the perfect investment. It is about putting structure around your money, so you can stay consistent, avoid costly mistakes, and give compounding enough time to work.

Who this framework is for, and how it changes over time

What I find most helpful about the Four Pots of Wealth is that the framework stays the same, even as life changes.

The four pots stay the same, but how much I put in each one can change over time.

The Liquidity Pot is usually the most stable, shaped more by spending needs than by net worth.

Earlier in life, the Growth Pot will often take up a bigger share, as time and compounding are your biggest advantages. As responsibilities grow, the Income Pot may become more important, as steady cash flow and stability matter more. Closer to retirement, Income may take the lead, while Growth still helps to keep up with inflation and Opportunity becomes a smaller allocation.

The exact mix will look different for everyone. But the key idea is simple. This is not a fixed formula. It is a framework that adapts as your income, goals, and life stage change.

I also think this framework is most useful for investors who have moved beyond the very first step. Maybe you have built up some savings, been through a market wobble before, and started to realise that portfolio structure matters just as much as the investments you own.

If you are just starting out, you do not need all four pots right away. In the beginning, two is often enough, Liquidity and Growth. First, build your emergency buffer. Then start investing consistently for the long term.

As your savings grow and your financial life becomes more complex, you can gradually add the Income and Opportunity Pots.

What would Beansprout do?

At Beansprout, we believe long-term wealth is built on clarity, and the Four Pots of Wealth is one way to put that into practice.

For me, this framework has helped me think about investing more clearly. Instead of reacting to headlines or asking if something is a buy, I try to ask a simpler question, what role is this meant to play in my portfolio?

That shift matters most when markets turn volatile. The investors who stay on track are usually not the ones who can predict every move, but the ones who already have a plan.

That is what this framework is meant to do, give each part of your portfolio a purpose, and help you build around your real goals and risk tolerance.

It will not remove volatility or prevent drawdowns. But it can make it easier to stay steady when markets get noisy.

In the coming weeks, we will be sharing more about how to think about each pot, what to look for, what to avoid, and how to build them more thoughtfully.

Learn more about each pot here:

- Liquidity Pot: Keep your safety buffer ready for short term needs and unexpected expenses.

- Growth Pot: Grow your wealth over time through long term compounding.

- Income Pot: Create a dependable stream of passive income for stability across market cycles.

- Opportunity Pot: Capture higher conviction ideas within clear and controlled limits.

If there is one takeaway, it is this, financial security is rarely built from one perfect trade. It is built by growing the right pots, in the right balance, over time.

At Beansprout, we believe wealth building should feel steady, thoughtful, and sustainable.

Happy growing!

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments