Haw Par Corporation: More than just Tiger Balm

Stocks

By Ng Hui Min • 02 Jul 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Haw Par Corporation is a Singapore-listed holding company best known for its Tiger Balm consumer healthcare business, supported by a portfolio of strategic investments and property and leisure assets.

Singapore-listed consumer healthcare brand

About Haw Par

Haw Par Corporation is a Singapore-listed holding company with three main business pillars: consumer healthcare, strategic investments, and property and leisure.

Its consumer healthcare business is anchored by well-known brands such as Tiger Balm and Kwan Loong, which sell pain-relief products across global markets.

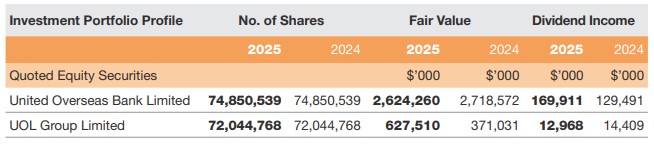

The group also owns significant strategic stakes in United Overseas Bank and UOL Group, giving it exposure to Singapore’s banking and property sectors.

In simple terms, Haw Par generates cash flow from its consumer healthcare business and reinvests part of that capital into blue-chip Singapore assets, creating a long-term compounding model supported by both operating earnings and investment income.

The Tiger Balm franchise

Tiger Balm is Haw Par’s core consumer healthcare brand, with more than 150 years of history.

It sells topical pain-relief products such as ointments, gels, sprays, patches and aromatherapy products across more than 100 countries.

The brand is widely distributed through pharmacies, supermarkets, airports and e-commerce platforms, with manufacturing carried out in Singapore, Malaysia, China and through contract manufacturers in India and Thailand.

Management noted that the original Tiger Balm ointment remains the strongest part of the portfolio. It accounts for about half of healthcare revenue and carries the highest margins because it requires relatively little marketing support.

This is because Tiger Balm ointment already has strong brand recognition and a long track record with consumers.

By contrast, newer products such as gels, sprays and patches require more advertising and promotion when launched.

Tiger Balm’s ointment business remains a high-return cash generator, while newer product lines provide potential growth but may require more upfront marketing investment.

Distribution model

Haw Par operates mainly as a manufacturer rather than a retailer.

It does not own retail stores or run wholesale operations directly. Instead, the company typically works with one exclusive distributor in each key market.

These distributors manage relationships with pharmacy chains, supermarkets and other retail channels such as Guardian, Watsons and Unity.

This creates a mutually dependent relationship. Haw Par needs retail shelf space to reach consumers, while retailers benefit from carrying a recognised brand like Tiger Balm that attracts repeat purchases.

Management described this as a balanced relationship rather than one where either side has excessive bargaining power.

This distribution model keeps Haw Par asset-light and focused on manufacturing, brand management and product development, while allowing local partners to handle market-level retail execution.

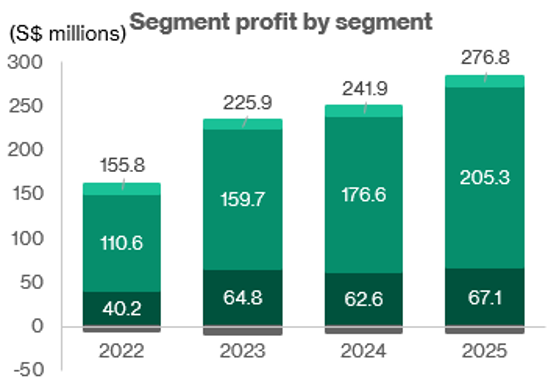

Segment overview

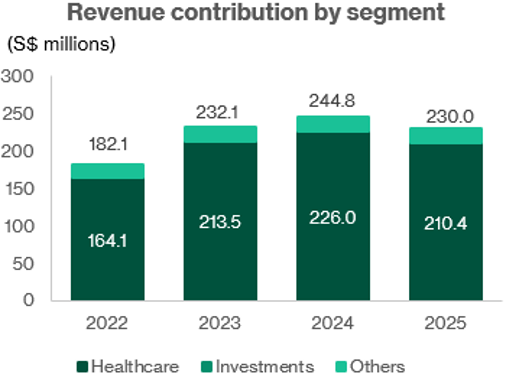

Healthcare segment is the main operating business segment.

Haw Par’s Healthcare segment, which includes Tiger Balm and Kwan Loong products, remained the group’s main operating business in FY2025.

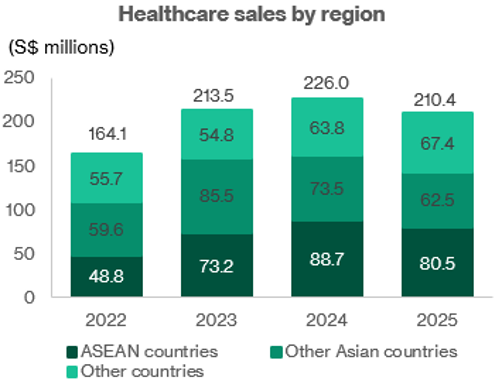

Healthcare revenue fell 7% year-on-year to S$240.5 million, mainly due to weaker sales in ASEAN and other Asian markets. ASEAN revenue declined 9% to S$80.5 million, while revenue from other Asian countries fell 15% to S$62.5 million.

Management attributed part of the weakness to softer travel flows, particularly fewer Chinese travellers to key ASEAN markets such as Thailand, Hong Kong and Singapore.

This was partly offset by stronger sales in other markets, mainly the Americas, Europe and the Middle East, where revenue rose 6% to S$67.4 million.

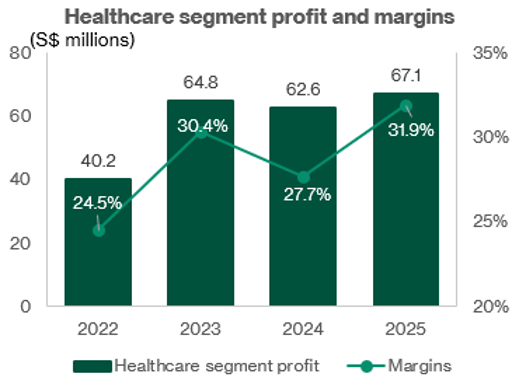

Despite the lower revenue, Healthcare segment profit increased 7% to S$67.1 million.

This was helped by a 16% reduction in distribution and marketing expenses, which lifted the Healthcare operating margin to 31.9%, a multi-year high.

Tiger Balm remains a highly profitable franchise, even when revenue growth is uneven across regions. However, the FY2025 results also show that travel patterns and regional demand can still affect sales momentum.

Investment segment is the largest contributor to group profit

Haw Par’s Investment segment is now the largest contributor to group profit.

The segment generated S$205.3 million in profit in FY2025, mainly from dividends from UOB and UOL Group, as well as interest income from cash deposits and debt securities.

UOB is especially important. Dividends from UOB rose 31% to S$169.9 million in FY2025, making UOB’s dividend policy a key driver of Haw Par’s earnings and cash flow.

The Investment segment’s profit is now more than three times the operating profit generated by Tiger Balm.

Management described the UOB and UOL stakes as long-held legacy assets in two core Singapore industries: banking and property.

Importantly, management said there is no intention to sell these stakes. Selling them would reduce the dividend income that supports Haw Par’s own dividends and cash balance.

Haw Par is not just a consumer healthcare company. It is also a long-term holding vehicle for blue-chip Singapore assets, with UOB dividends playing a particularly important role in group earnings.

Others: Property and leisure

Haw Par’s smaller Property and Leisure segment generated S$10.6 million in profit in FY2025.

The property portfolio provides stable rental income, mainly from three Singapore investment properties: Haw Par Centre, Haw Par Glass Tower and Haw Par Technocentre. These assets generate around S$16 million of annual rental income, with occupancy ranging from 72% to 100%.

Menara Haw Par in Kuala Lumpur remains the weaker asset, with occupancy of about 38% due to oversupply in the KL office market.

In leisure, Underwater World Pattaya saw better visitor numbers in FY2025 after the launch of its Jellyfish Zone.

However, competition in Pattaya is increasing, so management remains focused on disciplined cost control and execution.

FY2025 results overview

Weaker revenue but stronger net profit

FY2025 highlighted the resilience of Haw Par’s business model.

Group revenue fell 6.1% to S$230.0 million, mainly due to weaker Healthcare sales. However, this was more than offset by stronger investment income, which rose 17.3% to S$211.3 million.

As a result, group net profit increased 16.3% to a record S$265.5 million, while earnings per share rose from 103.1 cents to 119.9 cents.

The key point is that Haw Par now operates with two major earnings engines.

The first is its Tiger Balm consumer healthcare business, while the second is its investment portfolio, particularly dividends from UOB and UOL.

This dual-income structure provides an important buffer. Weakness in the operating business can be partly offset by stronger investment income, giving Haw Par a level of earnings resilience that is relatively uncommon among Singapore-listed consumer companies.

Margins: the cost discipline story

The standout operational achievement in FY2025 was the improvement in Healthcare margins.

Even though Healthcare revenue fell, segment profit rose as Haw Par managed costs more tightly.

Distribution and marketing expenses were reduced by S$8.4 million, while cost of sales fell by S$9.5 million. This reflected both production efficiencies and a more favourable product mix, with higher-margin ointments holding up better than some newer product formats.

As a result, Healthcare operating margin improved from 27.7% to 31.9%.

Gross margin also rose to 56.0%, the highest level in five years.

This suggests that Tiger Balm’s pricing power remains intact, and that Haw Par can protect profitability even when sales volumes are softer.

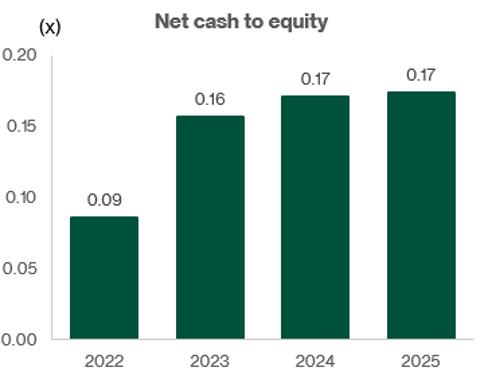

Balance sheet strength

Haw Par’s balance sheet remains highly conservative.

As at 31 December 2025, total assets stood at S$4.42 billion. Of this, S$3.39 billion, or 77%, came from its strategic investment portfolio, while S$0.79 billion, or 18%, was held in cash.

Total liabilities were just S$126.8 million, with a net cash-to-equity ratio of 0.17 times.

Its S$44 million of borrowings are secured against investment properties and carry annual interest costs of just S$1.5 million.

This gives Haw Par significant financial flexibility and reinforces its reputation as a conservatively managed holding company.

The listed stakes are worth more than the company

At a market capitalisation of about S$3.2 billion, Haw Par trades below the combined market value of its UOB and UOL stakes, which are worth about S$3.25 billion.

This means investors are effectively paying less than the value of Haw Par’s listed investments alone.

In other words, the Tiger Balm business, S$791 million in cash and the group’s investment properties are not fully reflected in the share price.

This discount is a central part of the investment case.

Cash flow and dividends

Haw Par generated S$57.1 million in operating cash flow from its Tiger Balm business in FY2025, up from S$53.8 million in FY2024.

However, this understates the group’s full cash generation, because Haw Par also receives significant dividend and interest income from its investment portfolio.

Including S$211.9 million of dividend and interest income, total cash inflows were about S$269 million.

Capital expenditure was just S$2.1 million, or less than 1% of revenue, reinforcing the asset-light nature of the business.

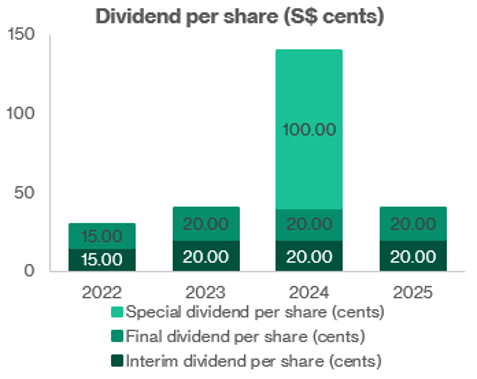

Dividend policy and track record

Haw Par does not have a formal dividend policy, but management aims to keep dividends predictable.

Management shared that once the dividend per share is raised, the intention is to maintain it at that higher level where possible.

In practice, Haw Par’s base dividend has been S$0.40 per share since FY2023, up from S$0.20 previously.

The S$1.00 per share special dividend paid in FY2024 also showed management’s willingness to return excess cash to shareholders when the balance sheet allows.

Corporate growth strategy

Deepen product range in key markets

The most capital-efficient growth lever for Haw Par is to sell more Tiger Balm products in markets where the brand is already known.

In Singapore, Tiger Balm has a full shelf presence, with more than 15 products across ointments, gels, patches, sprays and newer formats. In some overseas markets, however, only one or two products are currently registered and available.

Expanding the product range in these markets could support growth without requiring major capital investment.

The challenge is that each new product must go through local pharmaceutical registration, which can take years. This slows expansion, but it also creates barriers for competitors.

In FY2025, Haw Par launched new products including the Tiger Balm ACTIVE range, Tiger Balm Neck & Shoulder Rub, Tiger Balm Sensorial Therapy and Tiger Balm Lotion.

Management is also working on product development for Western markets, including packaging compliance in Europe and stronger product claims where regulations allow.

Geographic expansion: India, North America and Europe

Geographic expansion is another growth pillar for Haw Par.

India appears to be the clearest near-term opportunity. Management noted that product registration is less restrictive than in China, making it easier to introduce more Tiger Balm products. Tiger Balm Oil, launched in Tamil Nadu in 2024, has started gaining traction in southern India.

Management sees room to expand distribution across both retail and online channels. If sales volumes reach a certain scale, the business could become more self-sustaining.

North America also performed well in FY2025, with double-digit consumer sales growth in the US and market share gains in Canada. This was supported by marketing campaigns such as the Sony Pictures/Karate Kid partnership and new product launches like Muscle & Tension Lotion.

Europe grew more moderately, supported by sports-related marketing such as FC Bayern Munich partnerships and sponsorships of marathons and triathlons in France, Germany and the UK.

Haw Par’s geographic growth is likely to be gradual rather than explosive. India offers the largest runway, while North America and Europe provide opportunities to deepen brand awareness through sports, wellness and pain-relief positioning.

Malaysia manufacturing expansion

Haw Par is expanding its manufacturing facility in Malaysia, which management said will be around 10 times the capacity of the previous plant.

This serves two purposes.

First, it improves production resilience. If one manufacturing site faces disruption, other facilities can help support supply.

Second, it gives Haw Par more capacity to support medium-term growth in Tiger Balm demand.

Management described the old Malaysia plant as very small, so the new facility represents a meaningful upgrade in both capacity and operational flexibility.

Importantly, this expansion does not appear to require heavy capital spending relative to Haw Par’s balance sheet.

Total capex was just S$2.1 million in FY2025, suggesting the project is being phased carefully and funded comfortably from internal resources.

M&A: wellness and consumer healthcare acquisitions

Haw Par has significant financial firepower, with S$791 million in cash, or about 25% of its market capitalisation.

Management has signalled interest in acquisitions within the wellness and over-the-counter healthcare space.

The ideal target would be a well-known brand with a regional footprint, where Haw Par can add value through manufacturing, distribution and brand-building capabilities.

However, management appears disciplined on price.

It is not looking for early-stage brands with inflated valuations or businesses that are too localised. The preference is for brands with regional scale and a clear fit with Haw Par’s existing consumer healthcare platform.

Management also acknowledged that overpaying would not create value for shareholders, especially if targets are priced at high revenue multiples.

This suggests that Haw Par is likely to remain patient and selective.

In the meantime, management has kept capital deployment options open, including potential bolt-on investments and even increasing its UOB stake if valuations are attractive.

Investment portfolio: growing dividend income passively

The group’s stakes in UOB and UOL, worth about S$3.25 billion, are viewed by management as legacy assets to be held for the long term.

They collect dividends from UOB and UOL, reinvest excess cash into T-bills, equities or acquisitions, and return surplus capital to shareholders when appropriate.

This worked especially well in FY2025. UOB’s higher dividend lifted Haw Par’s dividend receipts by 31% to S$169.9 million.

UOL’s share price appreciation also added S$256.5 million in fair value gains to Haw Par’s other comprehensive income, increasing the group’s net asset value even though it was a non-cash gain.

This investment portfolio provides Haw Par with a second compounding engine beyond Tiger Balm.

It gives shareholders exposure to Singapore banking, property and consumer healthcare within one conservatively managed holding company.

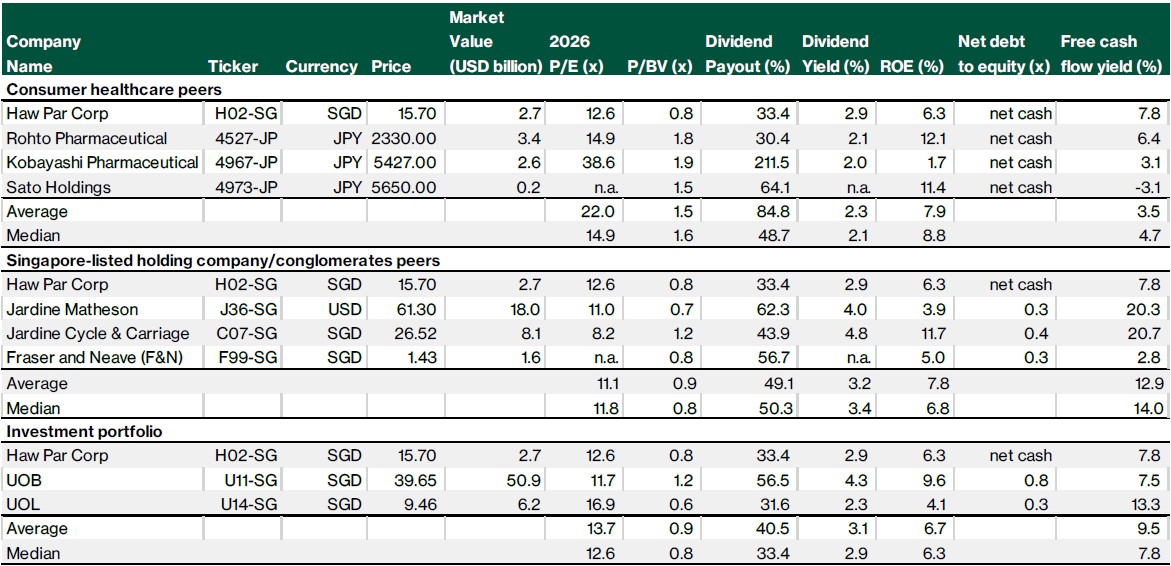

Valuations

Haw Par trades at low valuation multiples.

At S$15.70, Haw Par trades at about 12.6x FY2026 P/E and 0.8x P/B, which is below the consumer healthcare peer average of 22.0x P/E and 1.5x P/B.

Compared with regional consumer healthcare peers such as Rohto Pharmaceutical and Kobayashi Pharmaceutical, Haw Par also offers a higher free cash flow yield of 7.8%, versus the peer average of 3.5%. This reflects the strong cash-generative nature of its healthcare business and the additional cash income from its investment portfolio.

Against Singapore-listed holding company and conglomerate peers, Haw Par’s valuation also looks reasonable. Its 0.8x P/B is broadly in line with the peer median, while its 12.6x P/E is close to the group median of 11.8x. However, Haw Par has a cleaner balance sheet, with a net cash position compared with the net debt positions of Jardine Matheson, Jardine Cycle & Carriage and F&N.

The valuation discount reflects Haw Par’s hybrid structure as both a consumer healthcare company and an investment holding company. A significant portion of its asset value comes from its listed stakes in UOB and UOL, which may lead investors to apply a holding company discount.

At the same time, Haw Par’s investment portfolio remains liquid and income-generating, while its Tiger Balm business continues to be profitable and cash generative. The company is also supported by a net cash balance sheet and recurring dividend income from its listed investments.

At current levels, Haw Par trades below consumer healthcare peer averages on P/E and P/B, while offering a higher free cash flow yield. Key factors to watch include its dividend policy, potential special dividends or share buybacks, and how management allocates capital over time.

Investment conclusion

Haw Par has two main income streams: its asset-light Tiger Balm healthcare business, and dividend income from its sizeable stakes in UOB and UOL Group.

Based on the closing price of S$15.70 on 1 July, Haw Par’s regular dividend yield is about 2.9%. This is modest compared with Straits Times Index’s dividend yield of 3.8%.

However, the regular dividend of S$0.40 per share appears well supported. Haw Par has a strong balance sheet, with S$791 million in cash and just S$44 million of borrowings as at end-FY2025.

Its Tiger Balm business also remains cash generative, producing about S$55 million in free cash flow in FY2025 with very low capex needs. In addition, dividend income from UOB rose 31% year-on-year to S$169.9 million, providing another important source of cash flow.

The S$1.00 special dividend paid in FY2024 also shows that management is willing to return excess capital when conditions allow, although there is no formal policy for recurring special dividends.

At the current share price, Haw Par trades at about a 19.0% discount to its net asset value of S$19.38 per share as of 31 Dec 25. This discount is not unusual for Singapore holding companies.

The key things to watch are UOB’s dividend sustainability, how Haw Par uses its large cash balance, and whether the Healthcare segment can recover after ASEAN revenue declined in FY2025.

Key risks

Key risks for Haw Par include its reliance on Tiger Balm, potentially slower demand from younger consumers, limited growth visibility, volatility from its UOB and UOL investment holdings, foreign exchange and overseas market risks, and a persistent holding company discount due to lower share liquidity.

Related links:

- Haw Par Corporation share price and share price target

- Haw Par Corporation dividend history and forecast

Download the full report here.

Check out Beansprout guide to the best stock trading platforms in Singapore with the latest promotions to invest in LHN Limited.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments