OCBC 360 Review: Earn interest rate of up to 4.45% p.a.

Savings Account

By Beansprout • 04 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

OCBC 360 now offers up to 4.45% p.a. on the first S$100,000. We review its rates, requirements and whether it is still worth it.

What happened?

The OCBC 360 Account interest rates have been revised.

The account now offers up to 1.95% p.a. on the first S$100,000 when you credit your salary, save and spend.

You can earn a higher effective interest rate of up to 4.45% p.a. on the first S$100,000 if you also insure and invest with OCBC.

This is lower than the previous maximum effective interest rate of 5.45% p.a., as the Salary, Spend, Insure, Invest and Grow bonus rates have been reduced.

The OCBC 360 Account remains worth comparing for customers who can fulfil the Salary, Save and Spend categories each month.

With savings account rates coming down, I’ll take a closer look at how the OCBC 360 Account works, how much interest you can earn, and whether it is still worth considering.

What is the OCBC 360 account?

The OCBC 360 account is OCBC’s flagship savings account that rewards you with higher interest when you carry out everyday banking activities such as crediting your salary, saving regularly, and spending on an eligible OCBC credit card.

Instead of offering one flat interest rate, the account gives different bonus interest rates depending on which categories you are able to fulfil.

These bonus categories include Salary, Save, Spend, Insure, Invest, and Grow. This means you can earn more interest not just by using the account for day-to-day banking, but also by buying eligible insurance or investment products from OCBC, or by maintaining a higher account balance.

You will also continue to earn a base interest rate of 0.05% p.a. on your account balance regardless of whether you meet any bonus categories.

As OCBC’s flagship savings account, the 360 Account rewards you for everyday banking behaviour but you’ll need to meet certain criteria to unlock the higher interest rates.

What is the interest rate on the OCBC 360 account?

The OCBC 360 Account now offers up to 1.95% p.a. on the first S$100,000 when you meet the three core categories of Salary, Save and Spend.

You can earn an additional 2.50% p.a. when you insure and invest with OCBC, bringing the effective interest rate to 4.45% p.a. on the first S$100,000.

You will also earn a base interest rate of 0.05% p.a. on your account balance regardless of whether you fulfil any of the bonus categories.

Like the UOB One account and DBS Multiplier account, the OCBC 360 account offers a tiered interest rate depending on the amount of deposit in the account and your ability to meet different categories.

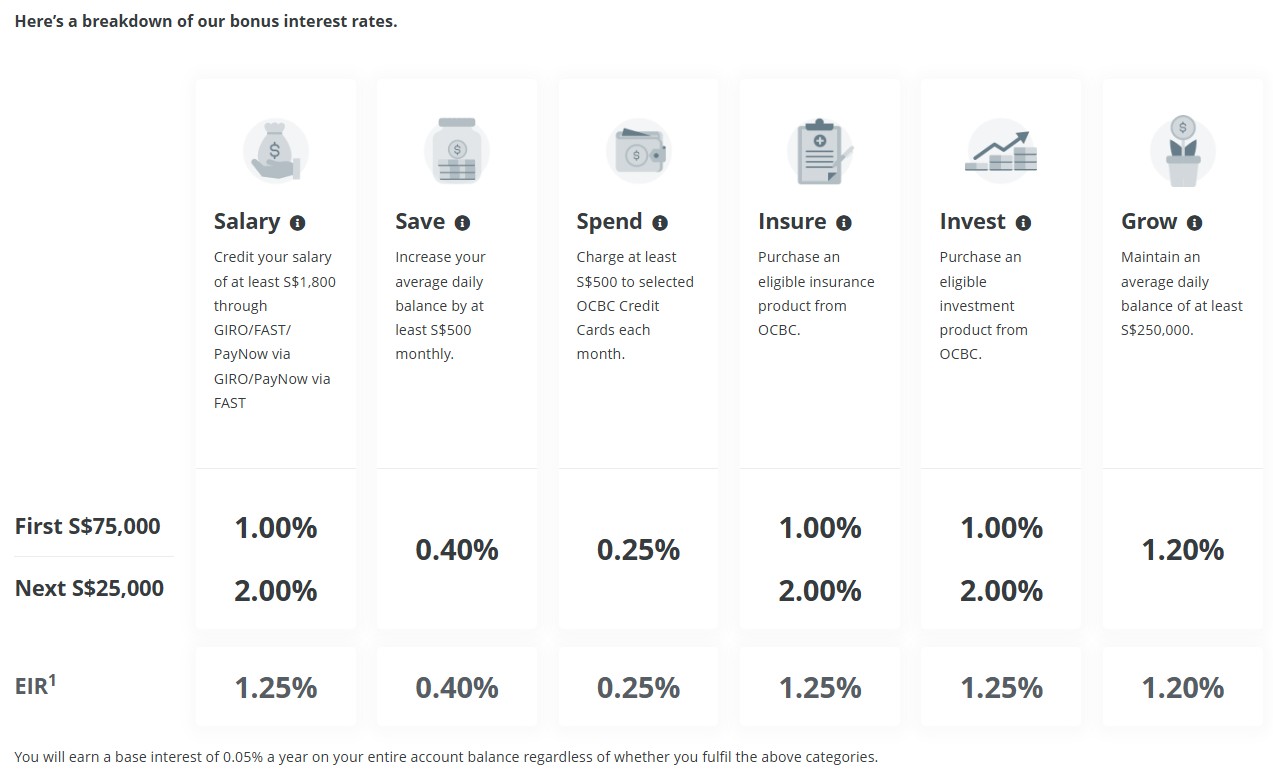

These categories include the following:

Salary: Credit your salary of at least S$1,800 through Giro

Save: Increase your average daily balance by at least S$500 monthly

Spend: Charge at least S$500 to selected OCBC credit cards each month

Insure: Purchase an eligible insurance product from OCBC

Invest: Purchase an eligible investment product from OCBC

Grow: Maintain an average daily balance of at least S$250,000

The interest rate you are able to earn on the OCBC 360 account will then depend on how many of these categories you are able to meet.

We can look at the effective interest rate (EIR) earned on the OCBC 360 account across various tiers. To calculate the effective interest rate, we can add the total interest received across different tiers.

The effective interest rate is the average interest rate you would get by dividing the total interest earned by your average balances.

Below is the maximum EIR as of 4 May 2026:

| Bonus Category | Criteria | Bonus Interest (p.a.) |

| Salary | Credit ≥ S$1,800 via GIRO/FAST/PayNow | 1.00% (first S$75k), 2.00% (next S$25k) |

| Save | Increase balance by ≥ S$500 monthly | 0.40% (first S$100k) |

| Spend | Spend ≥ S$500 on selected OCBC cards | 0.25% (first S$100k) |

| Insure | Buy eligible insurance | 1.00% (on first S$75k for 12 months) 2.00% (on next S$25k for 12 months) |

| Invest | Buy eligible investment | 1.00% (on first S$75k for 12 months) 2.00% (on next S$25k for 12 months) |

| Grow | Maintain ≥ S$250k avg. daily balance | 1.20% (on first S$100k) |

| Source: OCBC website as of 4 May 2026 | ||

You will still earn a base interest of 0.05% p.a. on your account balance regardless of bonus category fulfilment.

This would mean that the maximum effective interest rates for meeting each criteria will be the following:

| OCBC 360 Maximum Effective Interest Rates (after 1 May 2026) | |

| Categories Met | Max EIR (p.a.) |

| Salary + Save | 1.70% |

| Salary + Save + Spend | 1.95% |

| Salary + Save + Spend + Insure / Invest | 3.20% |

| Salary + Save + Spend + Insure + Invest | 4.45% |

This means the OCBC 360 Account is still more rewarding for users who can fulfil multiple categories.

How do I earn the maximum interest rate on the OCBC 360 account?

If you are able to hit the salary, save, spend, insure and invest categories and have S$100,000 of deposits in the OCBC 360 account, you will earn the maximum effective interest rate of 4.45% per annum as of April 2026.

The insure and invest categories will be harder to hit, which is why you get a much higher interest rate if you are able to fulfil them!

To qualify for the insurance and/or investment interest rate, you will need to purchase an eligible product from OCBC. The keyword here is eligible and it comes with a price tag.

For insurance, the minimum qualifying amount starts from S$2,000 in annual premium for selected regular premium protection, legacy or investment-linked policies. For single premium insurance, the minimum qualifying amount is S$20,000.

For Investment, you need to purchase a minimum amount of S$20,000 for Unit trusts and structured deposits or S$200,000 for bonds and structured products.

You should note that the financial products you buy will only qualify for 12 months of bonus interest.

This means that you will need to buy another financial product after the 12 months is up. The question you’ll have to ask yourself is whether you’d want to buy another insurance product next year.

What are the requirements for the OCBC 360 account?

To apply for the OCBC 360 account, you will need to be at least 18 years old.

You will need to make an initial deposit of S$1,000 and maintain a minimum average daily balance of S$3,000.

A fall-below fee of S$2 will be imposed if your minimum average daily balance falls below S$3,000. However, the good news is that the fall-below fee will be waived for the first year.

OCBC 360 vs UOB One vs DBS Multiplier – Which is the best savings account in Singapore?

Many of you are probably wondering if the OCBC 360 account is better than the UOB One account and DBS Multiplier account.

As there are many tiers involved, we have done the math to find out which is the best savings account in Singapore.

Our calculation is based on a few assumptions –

- You do not buy insurance/investment products from the Bank

- You save and/or spend at least S$500 respectively a month and

- You credit your monthly salary into the bank

- You spend the minimum amount with their credit cards

Here, we can see which bank offers the best interest rate across the various balance amount shown below.

Account monthly average balance | Maximum effective interest rate (per annum) | Winner |

| First S$75,000 |

| OCBC 360 |

| More than S$75,000 Less than S$100,000 |

| OCBC 360 |

| More than S$100,000 Less than S$150,000 |

| UOB One |

| More than S$150,000 Less than S$250,000 |

| UOB One |

| S$250,000 |

| OCBC 360 |

| Source: Various bank websites, Beansprout Compare Savings Accounts tool, as of 4 May 2026 | ||

Are there any sign-up promos for the OCBC 360 account?

If you are opening an OCBC 360 account, you can enjoy a welcome perk depending on whether you are new to OCBC or already banking with them.

- New-to-OCBC customers: Credit a salary of at least S$1,800 into your 360 Account by the next month after account opening, and you’ll get S$60 cash reward.

- Existing OCBC customers: Open a new 360 Account, credit a salary of at least S$1,800 into your 360 Account by the next month after account opening, and you’ll get S$30 cash reward.

The promotion runs from 1 July to 30 September 2026.

How to open a OCBC 360 Account

You can open a savings account online here, or head down to a OCBC branch.

To apply you will require the following:

- Singaporeans and Singapore PRs: NRIC and an image of your signature

- Foreigners: Passport and a valid pass (e.g. Employment Pass (EP) or S-Pass or Student Pass)

In addition, you will need any one of the following documents that shows your residential address

- Phone bill

- Half-yearly CPF statement

- Any bank statement

Final verdict on OCBC 360 account

The OCBC 360 Account has become less attractive after its latest interest rate cut.

If you credit your salary, increase your average daily balance by at least S$500 a month, and spend at least S$500 on an eligible OCBC credit card, you can now earn up to 1.95% p.a. on the first S$100,000.

This is lower than before, but it may still be useful for customers who already use OCBC as their main bank account.

However, the hurdle remains high if you want to earn the higher rate of 4.45% p.a..

That is because you would also need to insure and invest with OCBC, and these categories require you to purchase eligible financial products.

I would not buy an insurance or investment product just to earn more interest on a savings account. Instead, I would only consider these categories if the products are already suitable for my needs.

That said, the OCBC 360 Account still looks most compelling for those who are already able to meet the Salary, Save and Spend categories, and who are focused on balances of up to S$100,000.

The interest rate offered by the OCBC 360 account is also higher than the latest T-bill and it has the higher rate than the latest Singapore Savings Bond.

Like many other savings accounts in Singapore, the interest rate on the OCBC 360 accounts falls to 0.05% per annum for the portion of your monthly average balances above S$100,000.

To maximise your interest earned, you might want to consider another high yield savings account for balances above S$100,000.

If you are deciding where to park your cash, you can also explore how the OCBC 360 Account fits into the broader Liquidity Pot, alongside fixed deposits, T-bills, Singapore Savings Bonds and money market funds.

To find out other ways to make your savings work hard, check out our guide to best ways to earn a passive income in Singapore.

Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Find out which savings account allows you to earn the highest interest rate on your savings.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Questions and Answers

2 questions

- wong C • 03 May 2025 04:10 AM

- landi • 07 Nov 2024 03:42 AM

- perry • 27 Nov 2024 07:09 AM