Stoneweg Europe Stapled Trust: Positioning for Income and Growth

REITs

By Goh Lay Peng • 07 Apr 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Stoneweg Europe Stapled Trust (SERT) provides exposure to logistics and data centre assets in Western Europe and the Nordics. Rental reversion of logistics assets are protected by built-in rental appreciation. With a medium-term strategic goal to increase the logistics/light industrial weighting, we see upside potential to the income stream.

Singapore’s only pure Europe-focused REIT

About Stoneweg Europe Stapled Trust

Stoneweg Europe Stapled Trust, formerly known Cromwell European Real Estate Investment Trust (REIT), was formed upon the transition to the new sponsor, Swiss-based SWI Group, in 2024.

SWI Group acquired a 27.8% stake in Stoneweg Europe Stapled Trust and its management platform in Singapore and Europe for €280 million. SWI Group is a diversified alternative investment platform with more than €10 billion across real estate, infrastructure, data centres and other commercial assets across Europe.

Established in 2017, Stoneweg Europe Stapled Trust is listed on the Singapore Stock Exchange with market capitalisation of approximate S$1.4 billion. According to the investment mandate, at least 75% of the portfolio must be located in Western Europe, and at least 75% must be allocated to the logistics/light industrial and office sectors.

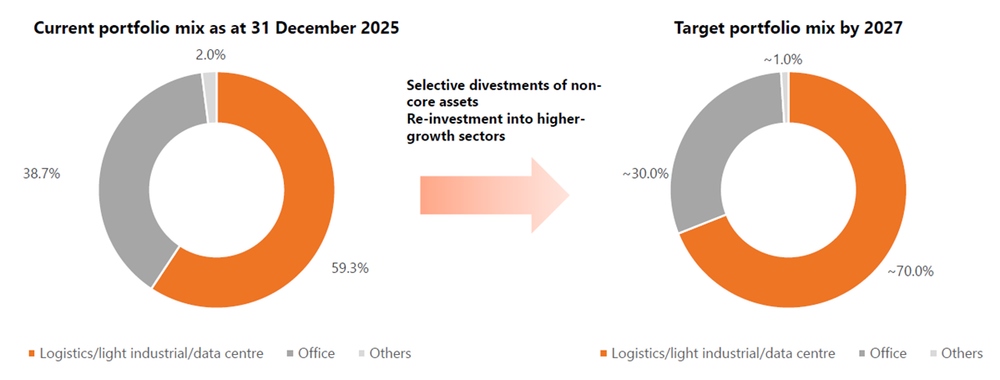

As at 31 December 2025, 90% of the portfolio is concentrated in Western Europe and the Nordics, while logistics/light industrial and data centre assets account for approximately 60% of the portfolio. Management has a medium-term strategic goal to increase the logistics/light industrial weighting further, reflecting the sector's favourable structural demand dynamics relative to traditional office.

Total portfolio valued at €2.16 billion

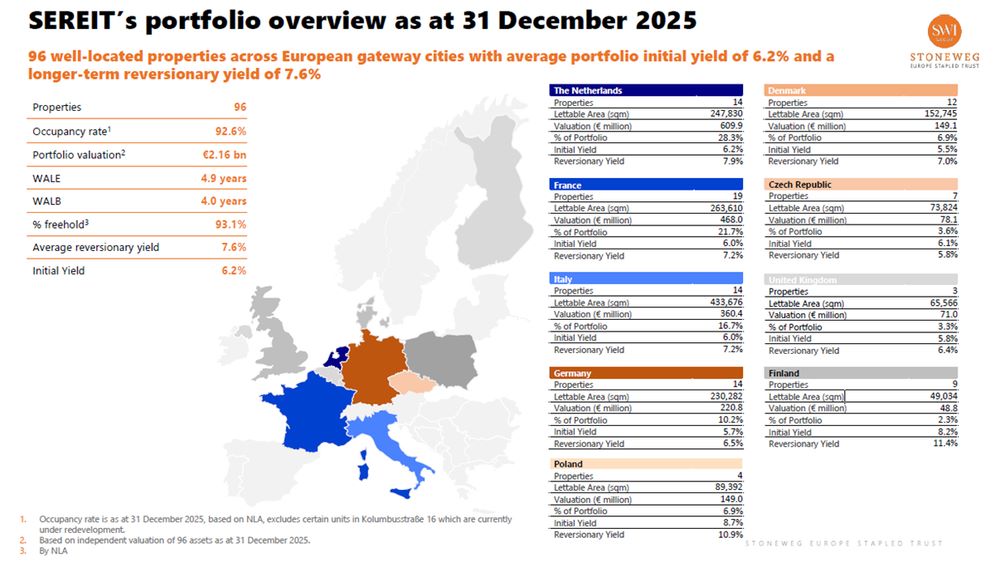

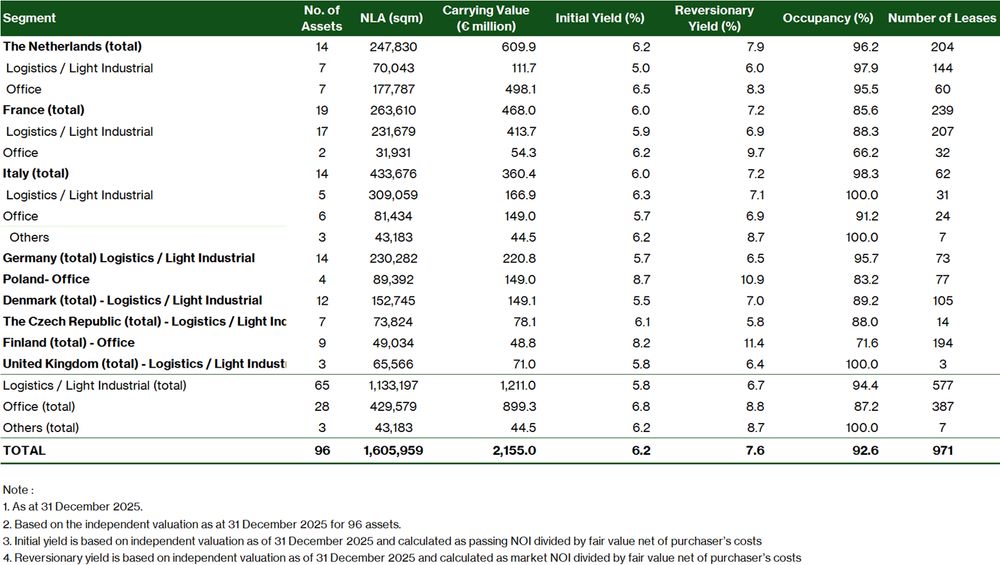

Stoneweg Europe Stapled Trust’s portfolio is valued at €2.16 billion, as at 31 December 2025. The portfolio comprises 96 predominantly freehold properties located in or near major gateway cities in the Netherlands, Italy, France, Germany, Finland, Denmark, the Czech Republic and the United Kingdom.

As at 31 December 2025, the portfolio has an aggregate lettable area of approximately 1.6 million square metres and 700+ tenant-customers.

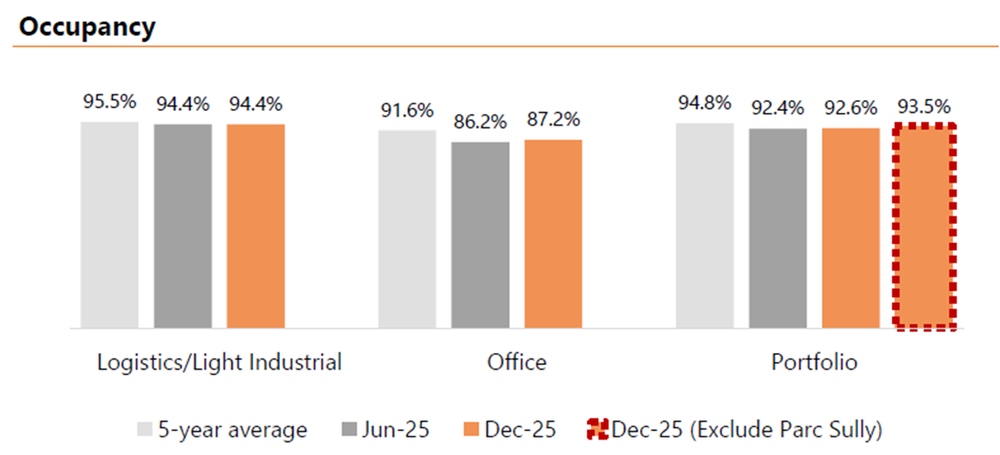

Portfolio occupancy stood at 92.6%, down slightly from 93.5% a year earlier, mainly due to tenant departures in the Polish office portfolio and at a couple of Dutch properties. The weighted average lease expiry (WALE) was 4.9 years by headline rent, easing from 5.1 years at end-2024.

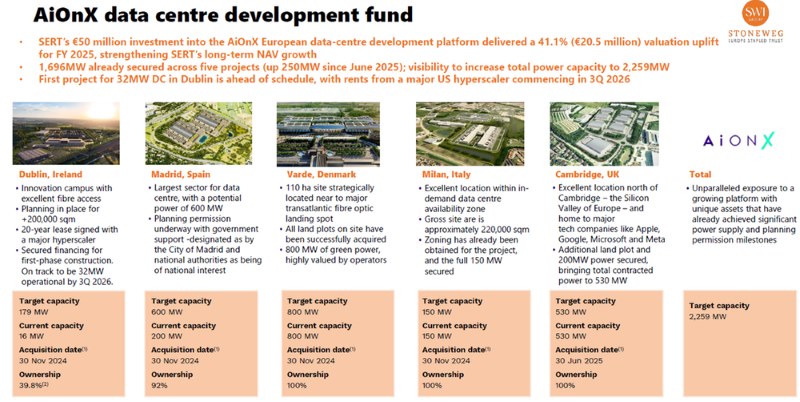

On 23 June 2025, Stoneweg European BT (the business trust arm of the SERT stapled structure) invested €50 million to acquire a 6.65% stake in AiOnX. AiOnX is a subsidiary of the REIT’s sponsor. The REIT made a second €50 million investment in AiOnX in late March 2026, bringing its total committed capital to the platform to €100 million. The second tranche was structured differently from the initial equity investment. It was made via a mandatory convertible loan carrying a coupon of 7.25% per annum with a seven-year tenure

Shift toward logistics and data centres through active capital recycling

Stoneweg Europe Stapled Trust focuses on raising the exposure to logistics, light industrial and data centres to a vast majority weighting over the medium term. Structural tailwinds — e-commerce penetration, supply chain reconfiguration, and accelerating AI and cloud adoption across Europe — are driving sustained demand for logistics and data centre assets, supporting occupancy, rental growth, and long-term asset values.

The focus on Western Europe is driven by the logistics segment, where structural demand from e-commerce, supply chain reconfiguration and inflation-linked lease structures, support resilient occupancy and rental growth.

On the other hand, office assets were underperforming. In FY2025, the Polish office portfolio was a notable drag with negative rent reversion across the portfolio. This explains the why the management is actively divesting non-core office assets and recycling into logistics and data centres

The strategy centres on active capital recycling, with non-core office assets divested and proceeds redeployed into higher-conviction opportunities. In FY2025, it sold eight properties for €120 million, including its entire Slovakia portfolio. Disposals have been well-timed, exemplified by the Rome Maxima office sale at a 32% premium to valuation.

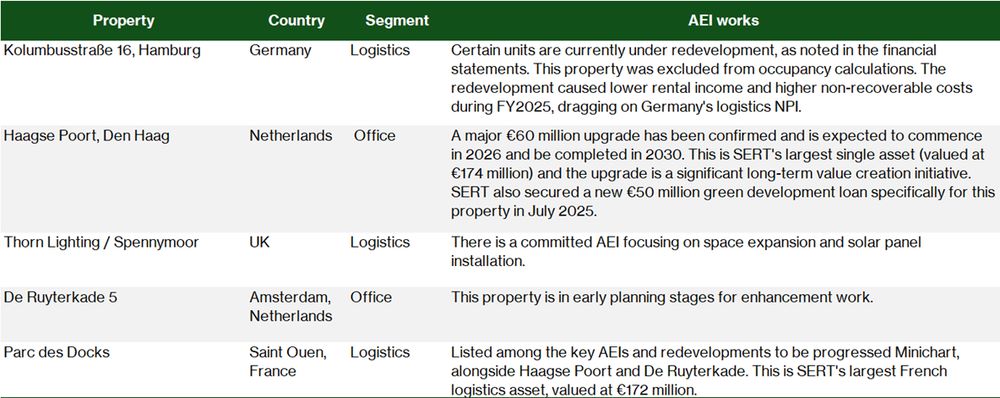

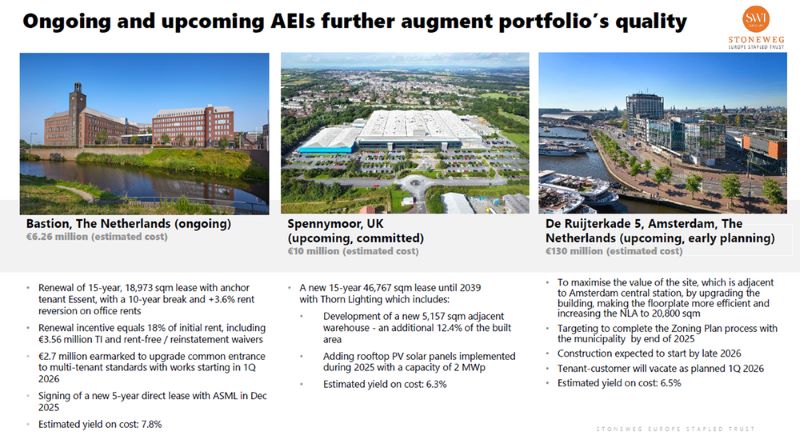

When implementing asset enhancement initiatives, it selectively pursues redevelopment of existing assets to enhance quality and earnings. Examples include the completed Nervesa21 office redevelopment in Milan (which achieved full occupancy) and Via dell'Industria 18 in Italy. There's also an ongoing redevelopment at Kolumbusstraße 16 in Hamburg.

The management aims to increase the exposure to logistics/light industrial/data centre from the current 59% to closer to 70% by 2027.

Strong sponsor with proven expertise in European real estate

The sponsor is SWI Group - a global alternative investment platform managing €11 billion in assets and operates in 18 countries. SWI Group is based in Geneva. SWI Group is also the largest unitholder, holding 28% stake in Stoneweg Europe Stapled Trust, which provides meaningful alignment with stapled securityholders. .

The sponsor has also strengthened its platform following its public listing. In February 2026, SWI Capital Holding completed its IPO on Euronext Amsterdam under the ticker “SWICH”, achieving a market capitalisation of €2.55 billion.

Industry outlook

The macroeconomic backdrop in the Eurozone is expected to remain resilient. According to Oxford Economics, GDP growth in the Eurozone outperformed consensus at 1.5% in 2025, up from 0.8% in 2024. For 2026, GDP growth is projected to remain modest at 1.1% and inflation of around 1.7%. Growth is expected to rise to 1.6% in 2027, supported by higher public infrastructure and defence spending, alongside recent 200bps rate cuts, despite tariff uncertainty and a stronger euro.

Inflation has moderated through 2025 to 1.7%, close to the European Central Bank’s 2% target. Further easing in core inflation could provide a more supportive backdrop for real estate and credit markets.

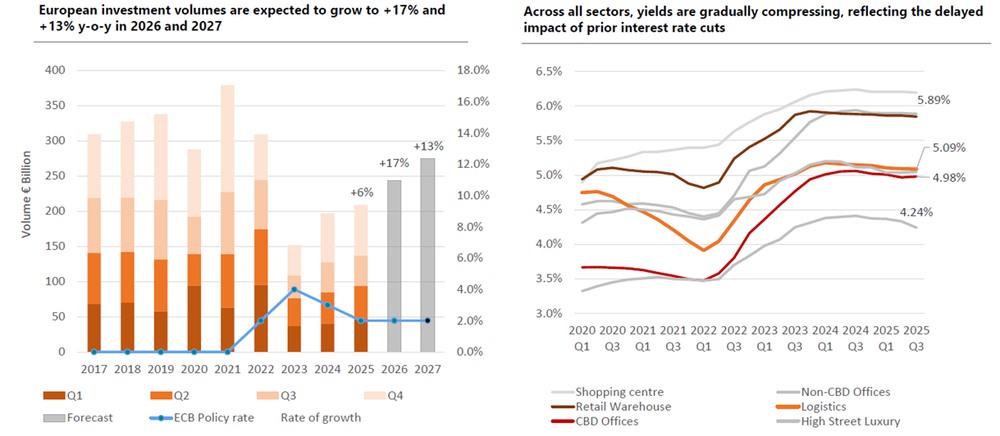

Investment volumes are rising and expected to grow at 17% and 13% year-on-year in 2026 and 2027, respectively. Cap rates have started to compressing to reflect the current rate cut cycle.

The European real estate market remains bifurcated, with logistics and data centres showing structural growth, while office assets face ongoing pressure—supporting SERT’s pivot towards logistics and alignment with data infrastructure themes.

Logistics stays resilient as demand improves and vacancies stabilise

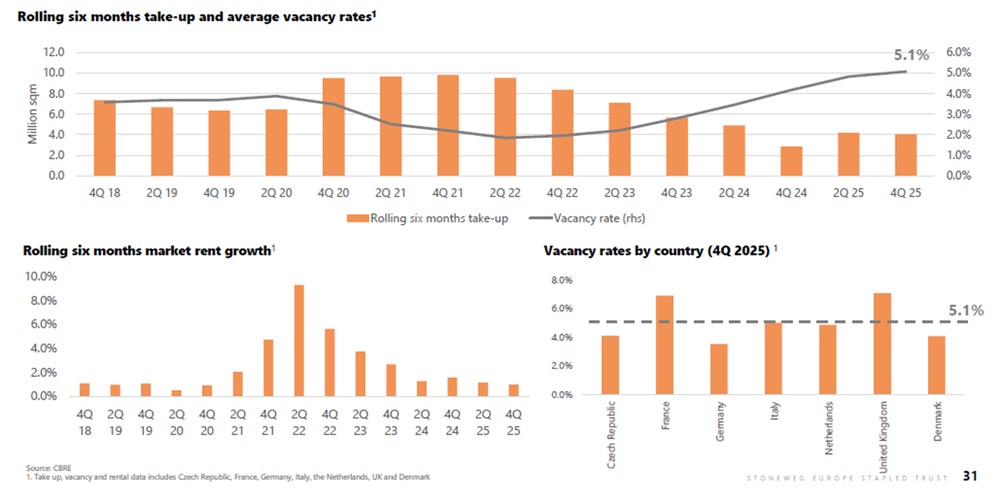

Logistics and light industrial assets remain resilient, supported by structural tailwinds such as e-commerce growth, supply chain reconfiguration, and nearshoring.

In 2025, European logistics leasing activity strengthened and pointing to a possible inflection. Take-up is expected to reach the low-20s million sqm for the full year, compared with about 19 million sqm in 2024. Logistics vacancy rates began to stabilise in the second half of 2025 and are expected to moderate to 5.0–6.0% by 4Q 2025.

SERT shifts to prime offices amid flight-to-quality demand

The office sector continues to face structural headwinds, particularly for older or non-core assets. Hybrid work trends and tenant downsizing have weighed on demand. But prime office assets in key locations with strong ESG credentials continue to see relatively stable demand, reinforcing a flight-to-quality dynamic.

SERT’s strategy of divesting weaker office assets while enhancing retained properties helps mitigate these risks. For retained office assets, the focus is on prime or core locations in key gateway cities, where demand tends to be more stable.

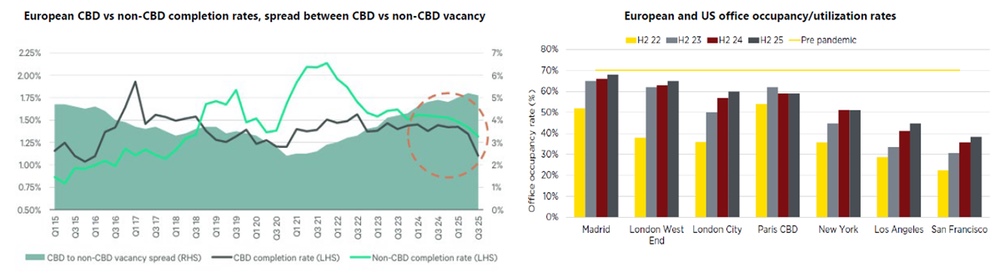

European office utilisation is recovering, with tight supply and a clear flight to quality supporting ~2.1% prime rental growth in 2026. CBD assets are leading. CBRE highlights a widening vacancy gap versus non-CBD offices, driven by stronger demand for well-located Grade A space, consistent with SERT’s positioning.

Demand is firming. Savills data shows utilisation in cities like Madrid, London and Paris nearing 70% in 2025, ahead of U.S. markets. Looking ahead, Oxford Economics expects ~605,000 new office-based jobs across the EU, supporting absorption.

Data centre demand stays strong as supply remains constrained

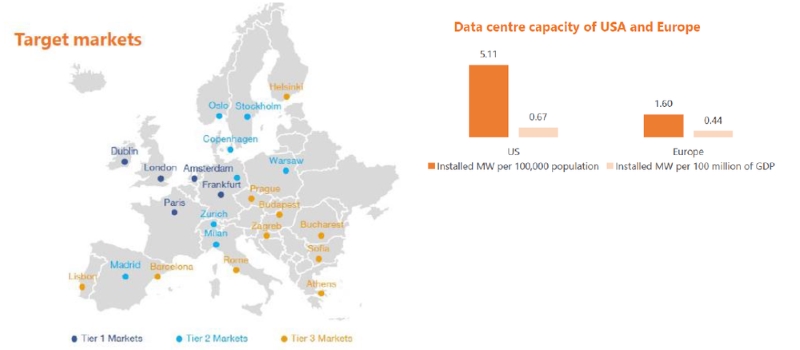

Demand for data centres remains strong, particularly in major tech hubs, driven by the increasing reliance on cloud computing, artificial intelligence, and data-intensive industries. To support data resilience, capacity is expected to grow at a double-digit pace over the coming decade, yet near-term supply remains constrained.

Limited availability of land, especially in dense urban areas, alongside energy constraints and strict environmental regulations, continues to restrict new developments and delay approvals. As a result, already secured and powered sites are highly sought after by hyperscalers and investors.

Despite this demand, Europe still lags the US in data centre capacity and will need to significantly scale up, potentially tripling capacity over the next few years to meet requirements. This growth is further underpinned by the rapid expansion of the global AI market, which is expected to reach US$1.8 trillion by 2030. Data generation is forecasted to grow by 28% CAGR, from 175 zetabytes in 2025 to 2,142 ZB in 2035.

Focused on stable distributions and long-term NAV growth

Its goal is to provide unitholders with stable and growing distributions and net asset value per unit over the long term, while maintaining an appropriate capital structure.

Portfolio grew since IPO as active recycling shifted exposure toward logistics

Portfolio valuation declined by €73.4 million or 3.3% year-on-year, to €2,152.5 million at 31 December 2025. This decline was primarily driven by asset divestments during the year. In FY2025, the REIT sold eight properties, including the entire Slovakia portfolio.

The REIT recorded a net fair value gain of €11.3 million on its remaining investment properties in FY2025, led by the logistics assets. On a like-for-like basis, portfolio valuation gained 2.15% year-on-year, or €45.4 million in FY2025.

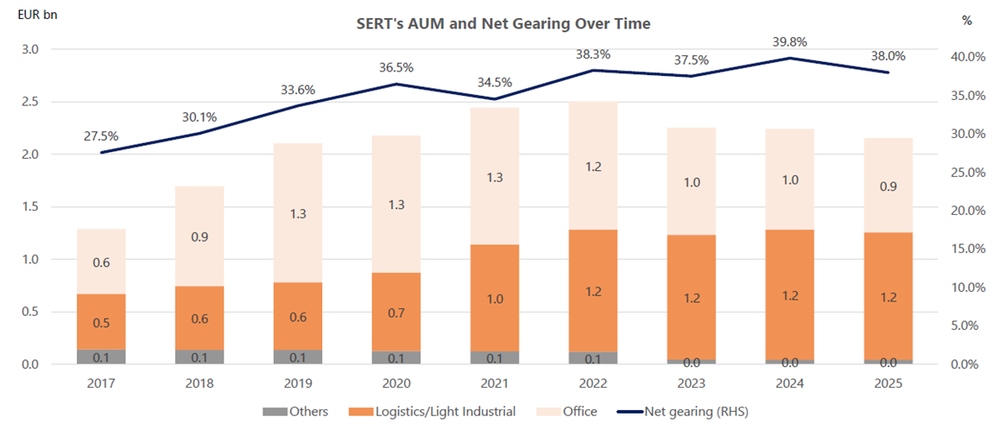

Since IPO in 2017, the portfolio has grown from €1.3 billion to €2.2 billion, up by 67%. Meanwhile, the REIT has proactively preserved its balance sheet, with net gearing maintained below 40%. To position the portfolio of sustainable and stable income streams, the REIT has shifted the weighting to logistics/ light industrial from 33% in 2020 to 60% in 2025. To fund the acquisitions, the REIT has disposed €400 million of non-core and non-strategic assets since 2022.

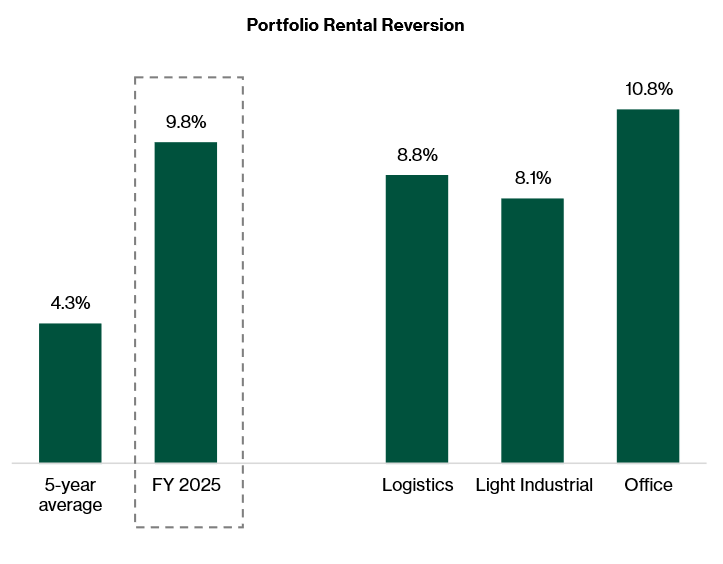

Strong leasing and rental reversions supported portfolio income growth

Portfolio rental reversion for FY2025 came in at 9.8%, significantly higher than the five-year average of 4.3%. It reported strong leasing success with approximately 300,000 square metres ("sqm") of new leases and re-leasing secured, representing around 20% of the portfolio. Offices delivered the strongest reversion at 10.8%, followed by logistics at 8.8% and light industrial at 8.1%.

Notable lease deals driving reversions include :

- a 20-year lease with NN Group NV in The Hague at a +50% rent reversion

- long-term renewals in Italy and Denmark at greater than +20% rent reversion

- The Nervesa21 office in Milan contributed strongly after the redevelopment was completed and fully leased.

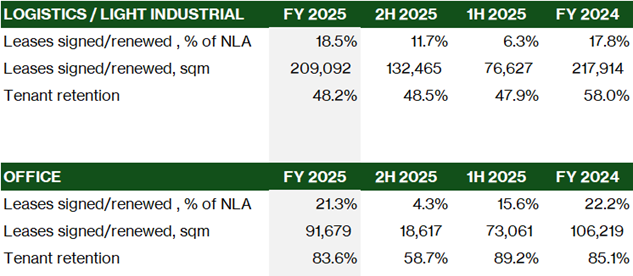

Leasing activity remained robust, with 18.5% of logistics NLA and 21.3% of office NLA signed or renewed in FY2025. Logistics momentum strengthened into 2H2025, accounting for 11.7% of activity versus 6.3% in 1H, while office leasing was front-loaded, with 15.6% completed in 1H compared to 4.3% in 2H.

Tenant retention in logistics dropped to 48.2% from 58.0% in FY2024, meaning more than half of expiring logistics tenants departed. However, this was offset by the high rental reversion of close to 9%. Office retention was broadly stable at 83.6%.

By geographical segment, assets with high occupancy include those in Italy (100%), Netherland (96.2%), UK logistics (100%) and Germany logistics (95.7%). Occupancy of office assets was weak, in Poland (83.2%), Finland (71.6%) and France (66.2%).

Stable weight average lease expiry

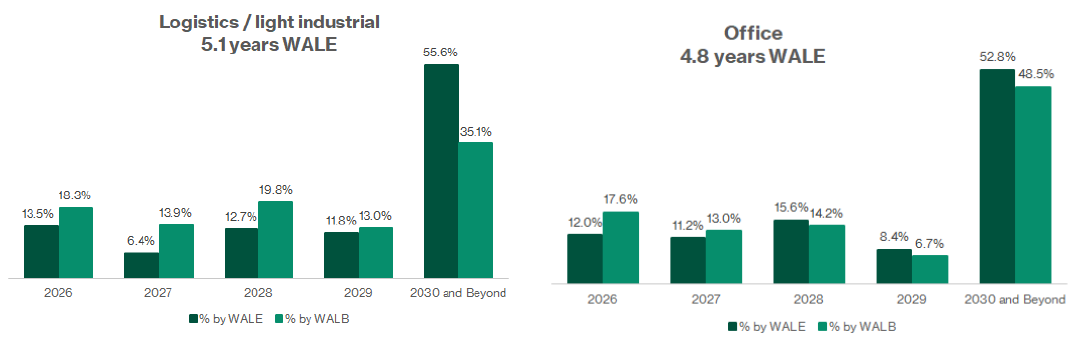

As at 31 December 2025, portfolio weighted average lease expiry (“WALE”) of 4.9 years was marginally lower from 5.1 years at 31 December 2024.

The portfolio provides reasonable cash flow visibility on commercial assets, in our view. Active asset management on leasing activities is key to manage the lease expiry profile.

By segment, logistics reported WALE of 5.1 years as at 31 December 2025, from 5.3 years as at 31 December 2024. Office segment reported WALE of 4.8 years as at 31 December 2025, from 4.9 years as at 31 December 2024.

Asset enhancement initiatives and organic growth drivers support future NPI upside

Stoneweg Europe Stapled Trust sees potential NPI growth driven by occupancy, under-renting, indexation, and its three-year asset enhancement initiatives (AEI) and development pipeline. The AEI programme is a key part of the strategy to enhance portfolio quality and drive organic growth without relying solely on acquisitions — particularly important given the current higher interest rate environment.

Early data centre exposure adds a new long-term growth driver

To drive the portfolio towards higher quality income, the REIT made the first move into the data centre space in 2025. On 23 June 2025, the REIT invested €50m into AiOnX data centre fund. AiOnX is an unquoted fund that owns a portfolio of five early-stage data centre development sites. When fully developed, these sites could have up to 2.3 gigawatts (GW) of total power capacity — which is a very substantial scale. The investment booked a fair value gain of €20.5m in FY2025.

Stoneweg Europe Stapled Trust made a second tranche investment in March 2026, investing another €50 million in AiOnX via a mandatory convertible loan carrying a coupon of 7.25% per annum with a seven-year tenure, which can be converted into AiOnX shares at maturity at a discount.

We are positive on the REIT’s pivot towards this fast-growing asset class. It has secured early-stage exposure through its sponsor relationship. SWI Group is the manager of AiOnX. When completed, AiOnX will be one of the largest data centre owners in Europe. This asset will drive the capital appreciation and income generation potential of the REIT in future.

Note : 1. Acquisition date is the date in which the assets were transferred/ acquired by the IDC Fund (ICF SPC)2. Shareholding was increased in Q2 2025 following an opportunistic restructuring with other exiting shareholders

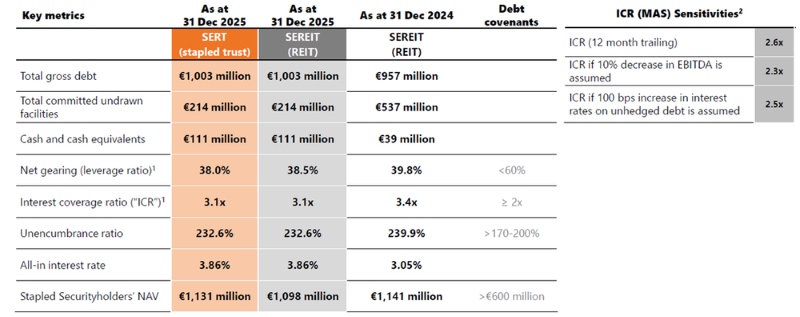

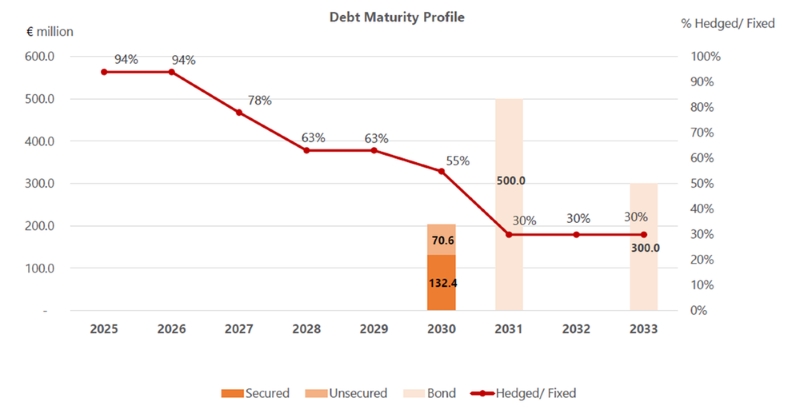

Elevated leverage but stable, well-hedged debt profile

As of 31 December 2025, aggregate leverage increased to 42.4%, from 41.2% as at 31 December 2024. Management expects the leverage to remain at the upper end of the policy range of 35-40%.

94% of the total debt is fixed or hedged using interest rate cap or swaps contracts.

All-in interest rate increased to 3.85% in FY2025, from 3.05% in FY2024. This was due to the bond refinancing in January 2025 when it issued €500 million of fixed rate senior unsecured notes at a coupon of 4.25%.

This increase was partially offset by lower interest expense on the unhedged portion of floating-rate borrowings, following declines in 3M Euribor and the Euro short-term rate (€STR). 3-month Euribor fell by 80 basis points in 1H 2025 to 1.94% and remain in the 2% range in 2H 2025. The remaining facilities, totalling €422 million, were refinanced at lower margins later in the year.

Following the refinancing activities in 2025, it does not have any debt maturities till 2030.

Interest coverage ratio of 3.1 times is broadly in line with S-REIT peers and sits comfortably above the regulatory minimum of 1.5 times.

Weighted debt to maturity improved to 5.6 years as at 31 December 2025, from 4.2 years as at 31 December 2024.

In October 2025, Fitch Ratings upgraded Stoneweg Europe Stapled Trust’s credit rating to BBB, from BBB-, with a stable outlook, reflecting its improved portfolio quality and stable financial leverage metrics.

FY2025 financial results

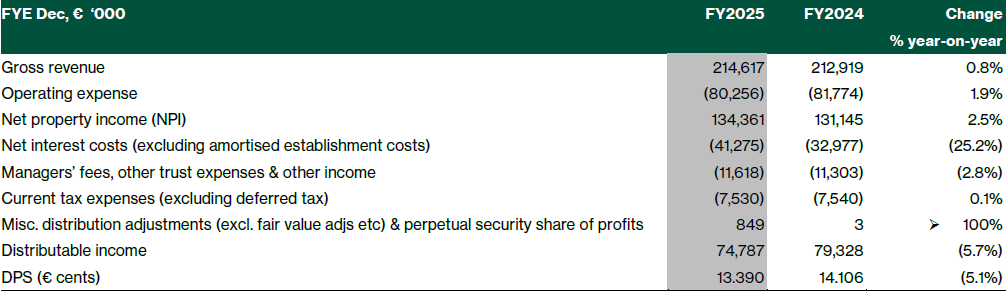

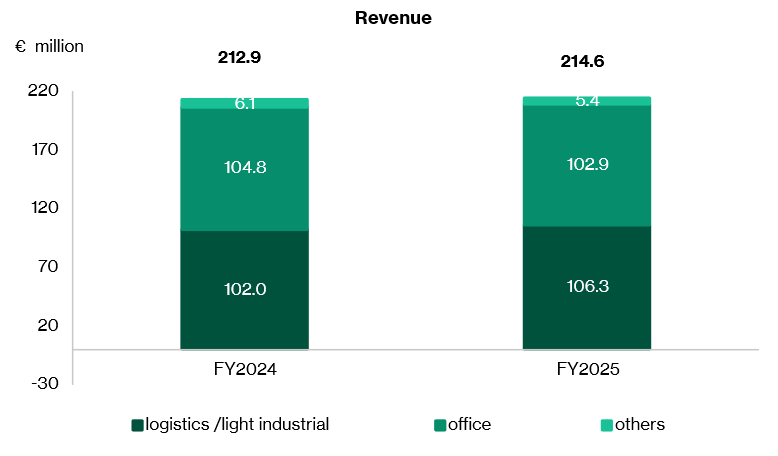

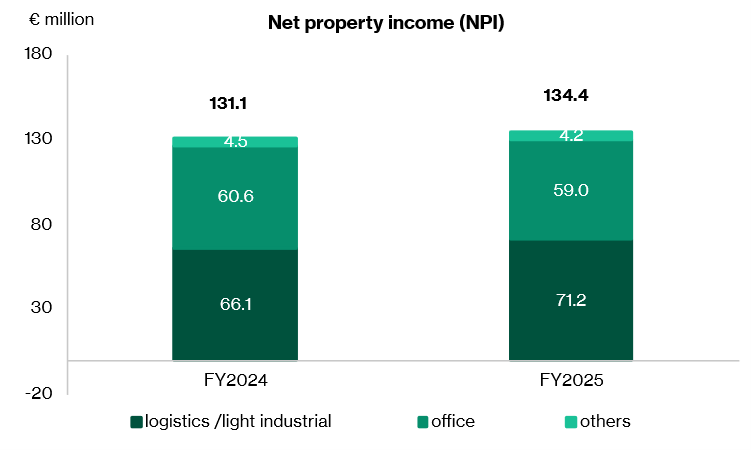

Revenue increased by 0.8% year-on-year to €214.62 million in FY2025. Net property income (NPI) rose 2.5% year-on-year to €134.36 million. Excluding the impact of divestments, net property income grew by 5.0% year-on-year in FY2025 on a like-for-like basis. The REIT recorded higher income from redevelopments and growth in the logistics/light industrial sectors.

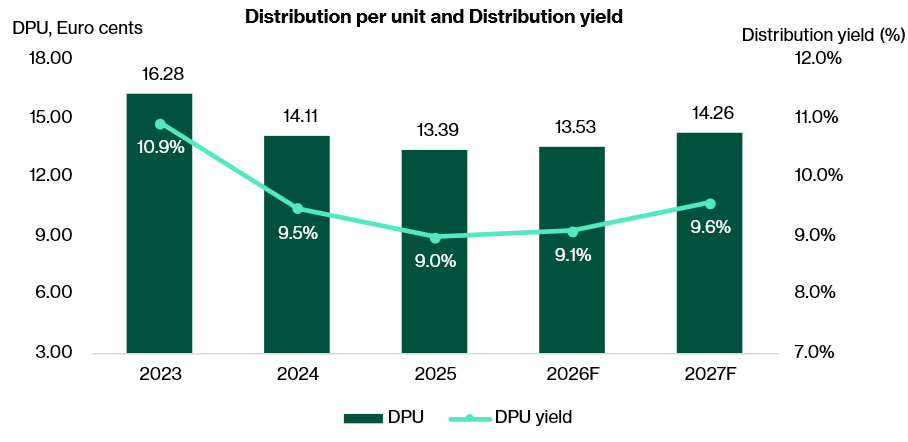

FY2025 distributable income declined 5.7% year-on-year to €74.8 million, driven by higher interest expense. Interest expense increased by 15.2% year-on-year to €44.0 million. This was mainly attributed to the €500 million green bonds issued in January 2025, at a higher coupon of 4.25% p.a. However, this was partly offset by lower refinancing costs later in the year as 3M Euribor and the Euro short-term rate decreased. Further, the €10.0 million buyback was 1.1% accretive.

Stoneweg Europe Stapled Trust delivered FY2025 distribution per security (DPS) at 13.39 € cents, declined by 5.1% year-on-year. Management expects FY2026 DPS to be similar to FY2025, implying 8.9% distribution yield at the current security price.

Note : Distribution per stapled security (“DPS”) is based on applicable stapled securities entitled to distribution at record date of each distribution

Logistics and light industrial delivered solid growth

Logistics/light industrial reported revenue at €106.3 million in FY2025, up 4.2% year-on-year. Net property income increased by 7.7% year-on-year to €71.2 million.

Key contributors included stronger contributions from the Italian portfolio, especially Via dell'Industria 18, following the completion of its redevelopment and the start of new leases. Net property income from Italy rose 27 per cent year on year, supported by both higher rental income and lower operating expenses.

Performance in France also improved, helped by lower provisions for doubtful debts and higher rent from annual inflation indexation.

Across the wider portfolio, income was further supported by annual rent indexation and better occupancy, including in markets such as the Netherlands and Denmark.

Office income was broadly stable

Office portfolio reported revenue at €102.9 million in FY2025, declining by 1.8% year-on-year. Net property income decreased by 2.7% year-on-year to €59.0 million, due to the impact of divestments made in FY2024 and 2025.

Stoneweg Europe Stapled Trust divested four properties in FY2024 and seven properties in FY2025. In total, these divestments reduced net property income by €1.6 million. On a like-for-like basis, net property income was mostly stable.

The Italian portfolio recorded higher income from Nervesa21 in Italy following the completion of the redevelopment. On a like-for-like basis, the Italian portfolio’s net property income grew 31.3% year-on-year, reflecting strong underlying performance.

In France, NPI rose by 38.3% year-on-year on a like-for-like basis, driven mainly by lower provisions for bad debts at Cap Mermoz following tenant settlements, as well as reduced portfolio-level maintenance expenses.

Initiate at Buy

We initiate coverage on Stoneweg Europe Stapled Trust with a 12-month target price of €1.73 per security. The target price is based on dividend discount model with a 10% discount to reflect the current heightened geopolitical risks. We are concerned that if the US-Iran war led to prolonged period of elevated oil price, Eurozone Central Bank may hike benchmark interest rates.

That said, Stoneweg Europe Stapled Trust has reconstituted the portfolio towards income generation and growth potential.

A long WALE provides earnings stability and reduces near-term leasing risk, while improving demand fundamentals a constructive outlook.

Target price of €1.73 offers FY2026E distribution yield of 7.8%

Currently, the REIT is trading at €1.49, implying FY26E distribution yield of 9.0%, FY27E distribution yield of 9.5%. Based on the reported NAV per security of €2.03 per security, the REIT is trading at price-to-book of 0.73x.

Currently trading at €1.49, Stoneweg Europe Stapled Trust offers FY26E distribution yield of 9.0%. In comparison, Elite UK REIT and IREIT Global are trading at consensus forecast FY2026f distribution yield of 9.0% and 6.2%, respectively.

Stoneweg Europe Stapled Trust is trading at FY2025 price-to-book 0.73x, in versus Elite UK REIT’s FY2025 price-to-book 0.91x and IREIT Global’s FY2025 price-to-book 0.57x. Given the larger scale and established track record, we think Stoneweg Europe Stapled Trust will trade closer to the upper end of the range.

Key risks

Key risks include interest rate risk, weak office demand, limited debt headroom, execution risk and macroeconomic risk.

Interest rate and refinancing risk

It is exposed to movements in European interest rates which have remain elevated relative to the low-rate environment seen in prior years. Higher all-in funding costs directly increases interest expense and reduces distributable income.

What this really means is that even if the underlying property income remains stable, distributions can still come under pressure due to financing costs alone. The pace and timing of rate cuts, as well as its ability to manage its debt maturity profile and hedging strategy, will be key in determining the extent of this impact.

It actively manages its debt profile through a mix of fixed and hedged borrowings and maintains a well-staggered debt maturity profile.

Office sector weakness

Office assets is a segment facing structural and cyclical headwinds across Europe. Demand for office space has softened in certain markets due to hybrid work trends, corporate cost rationalisation, and tenant downsizing. This has resulted in lower occupancy rates and weaker rental reversions compared to logistics assets.

Stoneweg Europe Stapled Trust is gradually reducing its exposure to office assets through selective divestments, while increasing allocation to logistics and light industrial properties. This strategic shift helps rebalance the portfolio towards sectors with stronger demand fundamentals and more resilient occupancy.

Leverage and limited debt headroom

Its gearing remains in the low-40% range, which is below regulatory limits but leaves only moderate headroom for additional borrowing. This constrains financial flexibility, particularly in a rising rate environment where maintaining balance sheet discipline is critical. This limits its ability to pursue acquisitions or fund large-scale redevelopment without raising equity. Ongoing divestments of non-core assets can free up capital and create additional headroom. The REIT also has access to multiple funding channels, including bank debt and capital markets, allowing it to optimise its capital structure.

Execution risk in portfolio repositioning

The REIT is actively repositioning its portfolio while undertaking asset enhancement initiatives and redevelopment projects to improve asset quality and ESG credentials. We think the execution risk is mitigated by the strong support from an experienced sponsor, SWI Group, which has an established track record. This provides operational expertise and access to deal flow. For instance, the REIT has invested into the data centre platform at the early development stage.

Macroeconomic and valuation risk

SERT’s portfolio is concentrated in Europe, exposing it to regional macroeconomic conditions including GDP growth, inflation, and monetary policy. A weaker economic outlook could dampen tenant demand, reduce leasing activity, and put downward pressure on rents across certain markets.

Related links:

- Stoneweg Europe Stapled Trust share price history and share price target

- Stoneweg Europe Stapled Trust history and dividend forecasts

Download the full report here.

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in Stoneweg Europe Stapled Trust.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments