UI Boustead REIT - Gateway to Asia Pacific Industrial Real Estate

REITs

By Goh Lay Peng • 27 Mar 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

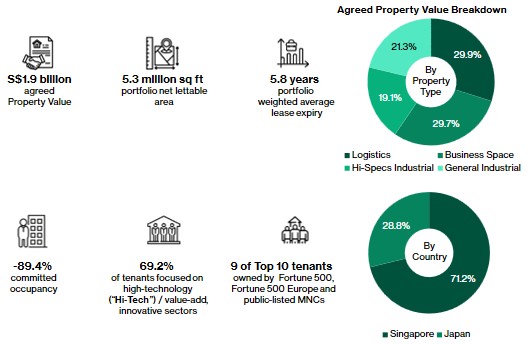

UI Boustead REIT is an industrial REIT focused on logistics, industrial, high-specifications industrial and business space assets. The initial portfolio, valued of S$1.9 billion, consists of 23 properties located in Singapore and Japan.

About UI Boustead REIT

UI Boustead REIT is a real estate investment trust established with the mandate to invest in logistics, industrial, high-specifications (“Hi-Specs”) industrial and business space assets across the Asia Pacific region. Its initial focus is on Singapore and Japan.

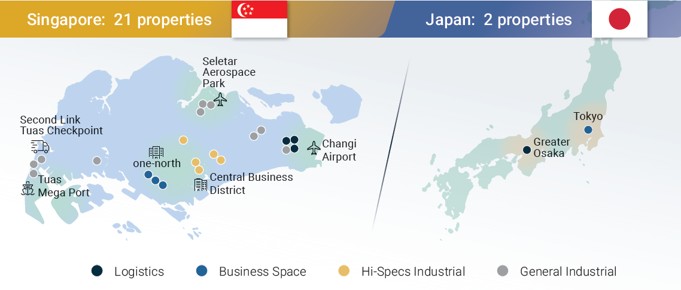

The initial portfolio consists of 23 properties, of which 21 assets in Singapore and 2 assets in Japan. The portfolio is concentrated in Singapore, which accounts for 71.2% of the total portfolio value, with the remaining 28.8% comprising properties located in Japan.

The IPO portfolio has a total gross floor area (GFA) of approximately 5.9 million sq ft and a net lettable area (NLA) of approximately 5.3 million sq ft. As at 30 September 2025, the agreed property value was S$1.9 billion, with a committed occupancy rate of 89.4%, providing a stable recurring rental income.

A portfolio providing a base of stable income, the portfolio is well-diversified across asset classes, including logistics facilities, business parks, high-specs industrial and general industrial buildings. The tenant profile is unique with 69.2% of the tenants in high-technology and value-add innovative sectors. These industries typically require purpose-built or specialised facilities, which makes tenants more anchored to the properties and results in stronger tenant retention.

Key portfolio highlights, as at 30 September 2025

Focused on high-technology and innovative sectors in Singapore

UI Boustead REIT is formed through a partnership between Unified Industrial and Boustead Projects Limited. UI Boustead REIT was listed on the Mainboard of SGX on 12 March 2026 at S$0.88 per unit. The Sponsor of the REIT, UIB Holdings, is 80% owned by Unified Industrial and 20% owned by Boustead Projects Limited.

Unified Industrial is a real estate investment, development, and asset management firm focused on industrial and logistics properties in North Asia. It operates in Japan and China, targeting logistics facilities, warehouses, and industrial parks.

Boustead Projects Limited is the real estate solutions division of Boustead Singapore Limited (F9D), an infrastructure-related engineering and technology group listed on the Mainboard of SGX with a market capitalisation of S$943.8 million.

The portfolio has a total net leasable area (NLA) of approximately 5.3 million square feet (sq ft) and a portfolio value of S$1.90 billion as at 30 September 2025. The initial portfolio comprises 23 properties across Singapore and Japan.

Singapore – 21 leasehold properties strategically located near Changi Airport, one-north, Seletar Aerospace Park, and the Tuas industrial corridor.

Japan – UIB Konan Phase 2, a large-scale institutional-grade logistics facility in Shiga Prefecture, and Toyo MK Fuso Building, a business space property in Tokyo's Koto Ward.

About 69.2% of the portfolio’s gross rental income is derived from tenants operating in high-technology, value-added, and innovative sectors. These include electronics and IT, automotive, aerospace and avionics, life sciences, precision engineering, and technology, media and telecommunications.

Properties are strategically located near designated hubs

Strategy

Asset management and asset enhancement initiative (AEI)

The REIT Manager adopts a proactive asset management approach, focusing on lease management, occupancy uplift, and value-enhancing AEIs.

Key near-term AEI opportunities include the AUMOVIO Building Phase 3 and the potential redevelopment of Toyo MK Fuso Building

AUMOVIO Building Phrase 3 will become vacant from 29 May 2026. The REIT has a planned $3.0 million AEI to convert the property from single-tenanted to multi-tenanted. The downtime of 12 months from June 2026 includes the AEI completion and the progress to achieve a stabilised occupancy.

Toyo MK Fuso Building could be redeveloped into a data centre with up to 20-megawatt capacity, subject to obtaining approvals from Tokyo Electronic Power Company Holdings.

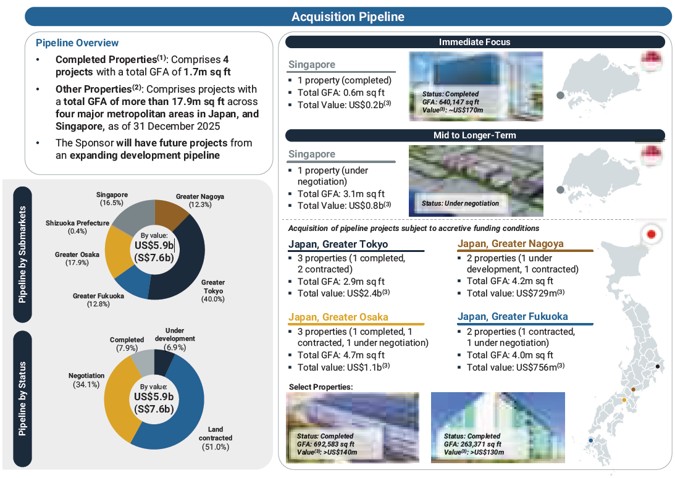

Acquisitions and Co-Development Pipeline

UI Boustead REIT benefits from rights of first refusal (ROFR) of the sponsor’s stabilised Pan-Asian logistics and industrial assets pipeline of over US$5.9 billion. The sponsor has a sizeable pipeline of approximately 19.6 million sq ft of GFA, including 1.7 million sq ft across four completed projects that are still in the lease-up phase or at an early stage of fund life. The balance of c.17.9 million sq ft comprises projects under development, on secured land, or currently under exclusive negotiation, providing potential visibility for future growth.

The near-term acquisition visibility includes a pre-committed logistics facility at 36 Tuas Road.

36 Tuas Road is a five-storey ramp-up logistics facility with a gross floor area of 640,147 sq ft. Completed in February 2025, the asset features modern logistics specifications including high floor loading, efficient floor plates, direct ramp access, and high ceiling clearance. The property is leased to tenants including a leading global apparel brand and a multinational shipping and logistics solutions provider and was valued at approximately S$220.0 million as at 31 March 2025.

Co-development opportunities, includes, a built-to-suit facility in Singapore for an existing tenant in Singapore, and a two-storey logistics facility in Greater Osaka.

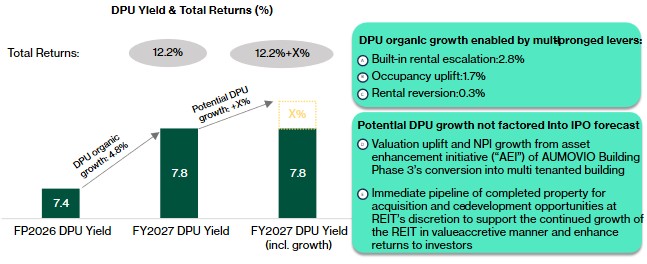

DPU growth not factored into IPO forecast

Portfolio performance metrics

Built-in rental escalations and property expense pass-through

The Singapore Properties are well positioned to deliver healthy organic growth, supported by built-in rental escalations in committed leases. For Forecast period 2026 and Projection Year 2027, 72.3% and 70.3% of leases have built-in rental escalations of 3.3% and 2.3%, respectively.

In addition, approximately 34.0% of leases (by NLA) include cost pass-through arrangements for property expenses such as property tax, utilities, and land rent. Leases in multi-tenanted buildings typically include service charge review clauses, allowing adjustments in the event of increases in operating costs.

These contractual features provide income visibility and protection for unitholders, supporting stable and predictable cash flows.

Occupancy rates uplift

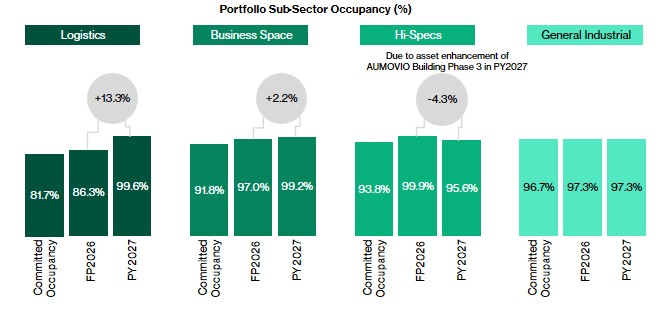

Occupancy rates of IPO properties by property type, as at 30 September 2025

As at 30 September 2025, the occupancy rates for the business space, Hi-Specs industrial were 91.8% and 93.8%, respectively.

The logistics properties are expected to see committed occupancy increase from 81.7% as at 30 September 2025 to 99.6% in Projection Year 2027, driven by the lease-up of the recently completed Japan property, UIB Konan Phase 2. As at 30 September 2025, UIB Konan Phase 2 recorded a committed occupancy rate of 76.7%, which is projected to increase to 99.4% by Projection Year 2027, supported by healthy leasing enquiries and activity.

However, as the leases are still under negotiation, the vacancies may not be filled as projected. This is particularly relevant in Japan, where the leasing lead time tends to be longer. Based on our research on industrial REITs in Japan, the competitive landscape is also relatively more intense.

Business space will also record occupancy uplift from 91.8% as at 30 September 2025, to 97% as of FP2026, driven by Toyo MK Fuso Building. Toyo MK Fuso Building’s major tenant recently vacated the property following a corporate restructuring exercise, resulting in the committed occupancy rate declining to 76.5% as at 30 September 2025. Leasing momentum has since improved, with committed occupancy recovering to 100.0% as at 20 February 2026.

The Hi-Specs industrial are expected to see committed occupancy increase from 93.8% as at 30 September 2025 to 99.9% in the Forecast Period 2026, driven by the lease-up of 26 Tai Seng Street. As at 30 September 2025, the property recorded a committed occupancy rate of 81.6%, with a further 14.4% of NLA under various stages of negotiations with prospective tenants.

Overall leasing momentum remains positive with occupancy uplift across the sub-sectors, in the next 12 to 18 months.

Tenant profile

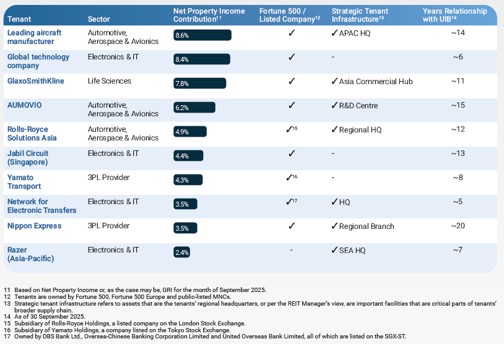

The REIT has a highly diversified tenant base. The top 10 tenants account for approximately 53.9% of Net Property Income (NPI). Largest tenant accounted for 8.6% of the net property income.

Nine of the top 10 tenants are owned by Fortune 500, Fortune 500 Europe, or public-listed MNCs, with an average relationship of approximately 11.4 years with the Sponsor. The relationship with a portfolio of high quality tenants strengthens the REIT’s position as a provider of reliable tenant infrastructure.

Key tenants include a leading aircraft manufacturer (APAC HQ, 8.6% NPI contribution), a global technology company (8.4%), GlaxoSmithKline (Asia Commercial Hub, 7.8%), AUMOVIO (R&D Centre, 6.2%), and Rolls-Royce Solutions Asia (Regional HQ, 4.9%).

Top 10 tenants

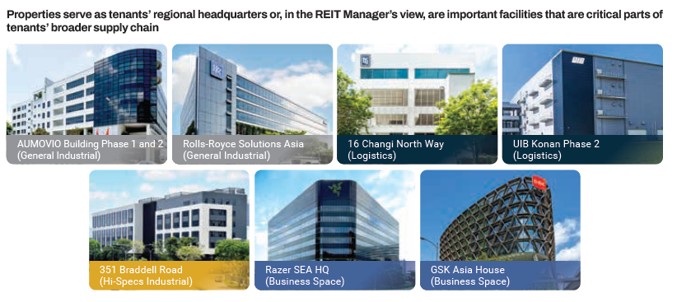

65.1% of the portfolio by Gross Rental Income comprises assets serving as strategic tenant infrastructure — properties that serve as tenants' regional headquarters or are critical parts of tenants' broader supply chains, enhancing "tenant stickiness" and income resilience.

Strategic tenant infrastructure in the REIT Manager’s view

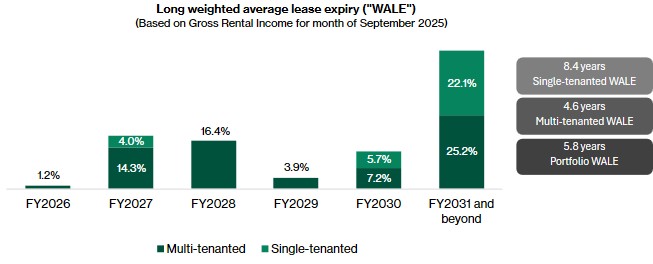

Long weighted average lease expiry

To the extent that the portfolio WALE stands at 5.8 years by Gross Rental Income, investors have reasonable visibility on the mid-term income stream. Furthermore, 61.5% of tenants are holding balance leases of three years or more.

Weighted average lease expiry at 5.8 years

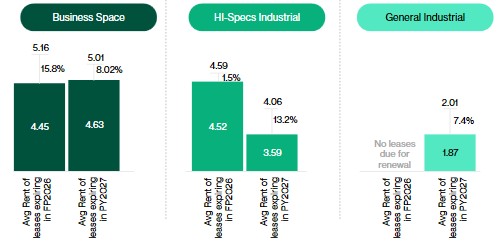

Positive rental reversion from lease renewal

As the passing rents on leases due for renewal in Forecast Period 2026 and Projection Year 2027 are below current market rents, there is room for potential positive rental reversion. For example, the lease at one Property was renewed in the first half of the financial year ending 31 March 2026 with a 20.0% increase in newly signed rental rates.

In Forecast Period 2026 and Projection Year 2027, rents of expiring leases at business space are 15.8% and 8.2% below current market rents, respectively. In Forecast Period 2026 and Projection Year 2027, passing rents of expiring leases at Hi-Specs industrial properties are 1.5% and 13.2% lower than current market rents, respectively.

We expect the renewal to be set at a rent near to the passing rent, bringing positive rental reversion to the portfolio.

Positive rental reversion opportunities

Industry outlook

Singapore industrial and logistics market

Singapore's industrial and logistics market is underpinned by robust structural demand drivers. The government has designated several sectors — electronics, precision engineering, energy and chemicals, aerospace, and logistics — as strategic growth areas under its Industry Transformation Maps, targeting a 50% increase in manufacturing value-add between 2020 and 2030.

Supply remains constrained across Singapore's industrial sub-sectors. For business space in the Central region, there are no new projects in the pipeline between 3Q 2025 and 2028. For logistics in the East region, limited new supply is expected over the next two years, while Hi-Specs industrial supply is expected to remain tight through 2028. This supply scarcity should continue to support occupancy and rental growth across the portfolio.

Japan Logistics Market

Japan's logistics sector is undergoing structural change driven by the "2024 issue" — a regulation capping truck driver overtime hours to 960 hours annually and driving time to four hours between rest periods — which is reshaping logistics footprints and driving demand for strategically-located, modern distribution facilities.

UIB Konan Phase 2, located in Shiga Prefecture in the Kansai region, is well-positioned to benefit. The asset is the only double-rampway facility in Shiga Prefecture, which provides access to approximately 30% of Japan's population and has 20 prefectures and cities within a four-hour driving radius. The Greater Osaka logistics rental market has grown approximately 1.8 times between 2020 and 3Q 2025, exhibiting stronger rental growth compared to Greater Tokyo.

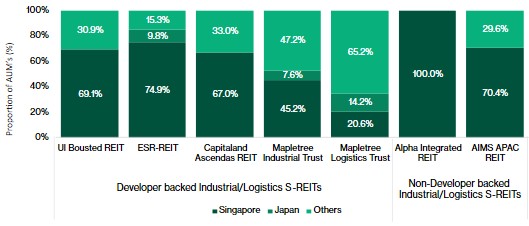

Competitors

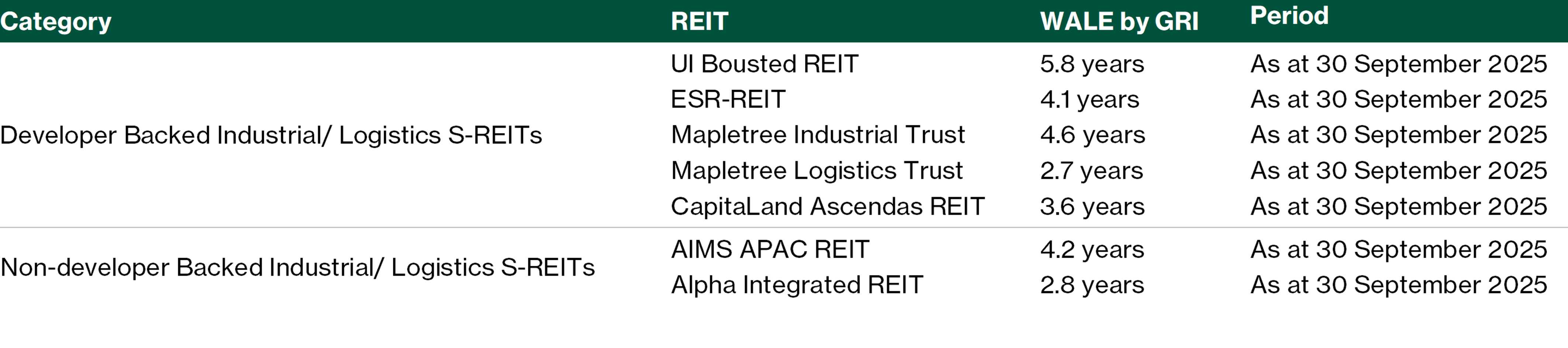

There are six REITs listed on the SGX that have industrial and logistics properties within their portfolio. They include developer-backed or non-developer backed industrial/logistics REITs.

The REIT sits mid-pack among the S-REIT peers. It is roughly twice the size of Alpha Integrated REIT and about one-fifth that of Mapletree Industrial Trust. We think the REIT is not at optimal scale.

Competitor’s assets under management by country

The weighted average lease to expiry (WALE) for UI Boustead REITs portfolio was 5.8 years, the longest among its competitors (2.7 to 4.6 years) as at 30 September 2025.

Competitors’ WALE by GRI

The Sponsor

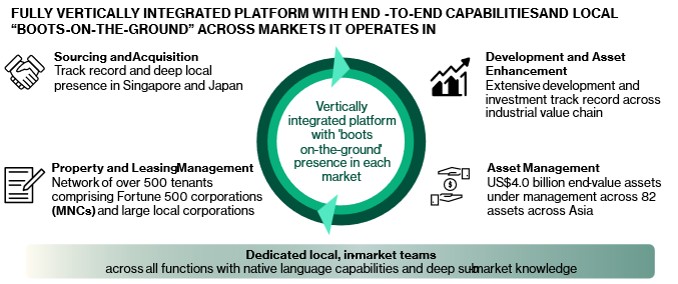

The Sponsor is a fully vertically integrated Pan-Asian logistics and industrial real estate platform with end-to-end capabilities and experience across markets it operates in. It is ability to source and access real estate opportunities in its key focus markets of Singapore and Japan.

This is particularly important when the REIT embarks on co-development projects. The REIT will be able to benefit from a higher yield on costs from these projects.

Sponsor operates a fully vertically integrated platform

The Sponsor has granted UI Boustead REIT a voluntary right of first refusal over its stabilised income-producing logistics, industrial, Hi-Specs industrial, and business space assets across the Asia Pacific region. The UIB ROFR gives the REIT potential access to a pipeline of over US$5.9 billion in relevant assets, supporting responsible, value-enhancing growth. The properties in the acquisition pipeline are mostly located in Japan. Of the US$5.9 billion in relevant assets, US$4.99 billion or 84% are properties located in Japan while the remaining are located in Singapore.

Separately, BPL has granted a ROFR to UI Boustead REIT (the “BPL ROFR”), providing potential additional access to relevant assets.

Following the listing, the Sponsor and BPL will hold 19% in combined stake in UI Boustead REIT. While this reflects the alignment of interest with unitholders, we prefer that the Sponsor and BPL own a higher stake in UI Boustead REIT.

Acquisition pipeline

Financial performance

Robust Distribution Profile

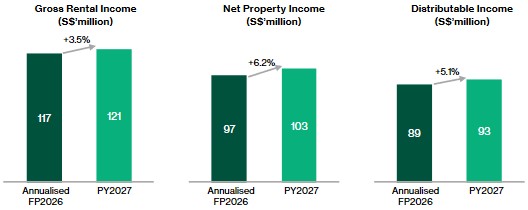

UI Boustead REIT offers an annualised distribution yield of 7.4% for the Forecast Period 2026 (FP2026, two months from 1 February 2026 to 31 March 2026) and 7.8% for PY2027, with approximately 98.1% and 87.0% of Gross Rental Income derived from in-place contracted leases in FP2026 and PY2027, respectively.

Organic DPU growth of 4.8% from annualised FP2026 to PY2027 is driven by built-in rental escalations (2.8%), occupancy uplift (1.7%), and positive rental reversions (0.3%).

Financial performance to underpin unitholder returns

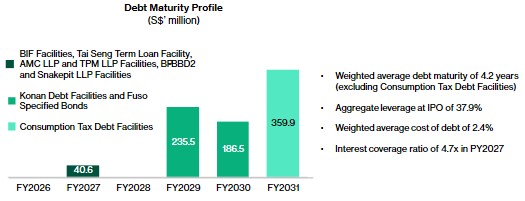

Disciplined capital management

As at IPO, the REIT's aggregate leverage stands at 37.9%, well within the MAS regulatory limit of 50%. This leaves a debt headroom of about S$230 million.

The weighted average debt maturity is 4.2 years (excluding Consumption Tax Debt Facilities), with a weighted average cost of debt of 2.4% and interest coverage ratio of 4.7x in FY2027.

Approximately 80% of borrowings are on fixed rates, limiting near-term interest rate sensitivity.

Debt maturity profile

Initiate at Neutral

We initiate coverage on UI Boustead REIT with a Neutral rating and a target price of S$0.91 per unit. UI Boustead REIT is relatively attractive compared to other industrial REITs, in our view.

The REIT has developed a network of high-quality tenants to support a visible income stream with modest positive rental reversion. In the near term, there are organic growth from built-in positive rental reversion and asset enhancement initiatives. In the medium term, the REIT is looking at new asset acquisition and property development projects for inorganic expansion.

Target price of S$0.91

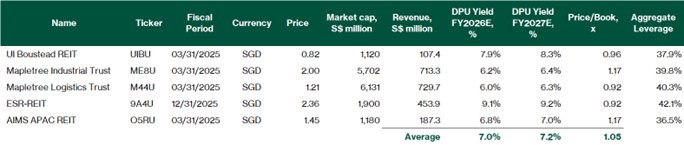

Currently, UI Boustead REIT is trading at S$0.81, implying FY2026E annualised distribution yield of 8.0% and FY2027E distribution yield of 8.4%. This is higher than the peers’ average FY2026E distribution yield of 7.0% and FY2027E distribution yield of 7.2%. Our target price at S$0.91 is based on the dividend discount model. At S$0.91, UI Boustead REIT is trading at FY2027E distribution yield of 7.5%. While the dividend yield appears high, this is offset by the shorter lease tenures; sponsor’s relatively low stake, the longer lead time needed to fill vacant space in Japan, and the REIT’s smaller scale compared to peers.

Projected dividend yield at IPO price

Peer comparison

Key risks

Key risks include concentrated two-market exposure, foreign exchange risk, lease expiry and tenant concentration risk, and regulatory exposure.

Concentrated asset type and geographic exposure

UI Boustead REIT's portfolio is exclusively comprised of industrial, logistics and business space assets in Singapore and Japan. While both are developed markets which offer attractive fundamentals, the REIT's financial performance is exposed to risks specific to these two markets and sectors.

Limited duration of lease tenures

The lease tenures of industrial land of Singapore are typically limited to 30 years, relatively short compared to other commercial land use. For UI Boustead REIT, 13 of the 21 Singapore Properties have lease tenure of less than 30 years. A significant portion of operating profits is generated from these properties of limited duration. The 13 properties account for 61.4% of the portfolio’s operating profits in FY2025. Besides the loss of income, the decay in lease terms will also adversely affect the valuation of the portfolio.

Lease expiry and tenant concentration risk

While the portfolio has a healthy WALE of 5.8 years, approximately 38.5% of tenants by Gross Rental Income have balance leases of less than three years. Any failure to renew leases at favourable terms or the early departure of a major tenant — such as AUMOVIO, which has already issued a notice of termination of its lease at AUMOVIO Building Phase 3 — could adversely affect the REIT's distributable income.

Foreign exchange risk

28.8% of the IPO Portfolio by Agreed Property Value is in Japan. Distributions from the Japan Properties will be impacted by fluctuations in the SGD/JPY exchange rate. The REIT may employ hedging strategies to mitigate this risk, though there is no assurance that these will fully offset currency movements.

Interest rate risk

While approximately 80% of borrowings are on fixed rates, rising interest rates could increase refinancing costs upon debt maturity, reduce distribution coverage, and compress the yield spread relative to risk-free rates, affecting unit price performance.

Regulatory and planning risk

Industrial and logistics properties in Singapore are subject to JTC land lease conditions, URA zoning requirements, and evolving environmental regulations. In Japan, ongoing regulatory changes affecting logistics operations may affect the operating environment

Related links:

Check out Beansprout guide to the best stock trading platforms in Singapore with the latest promotions to UI Boustead REIT.

Download the full report here.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments