UOB reports 4% decline in 1Q26 profit: Our Quick Take

Stocks

By Gerald Wong, CFA • 07 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

UOB reported a 4% drop year-on-year in 1Q26 net profit.

UOB 1Q26 earnings highlights

UOB Group announced its earnings for the first quarter of 2026. Key highlights include:

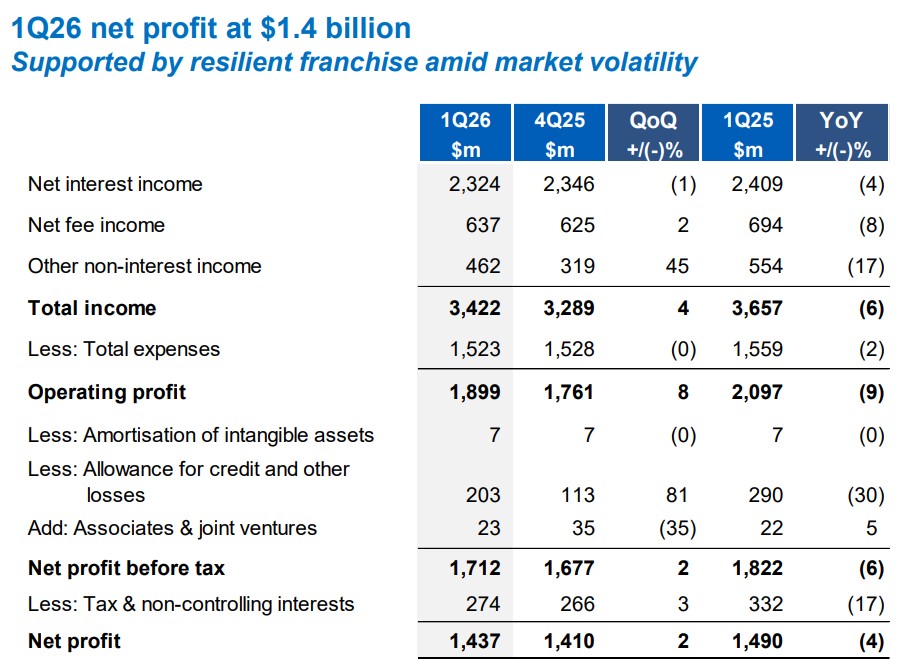

- Net profit of S$1.44 billion in 1Q26, down 4% year-on-year

- Net interest margin of 1.82%, down from 1.84% in 4Q25

- Asset quality stable with NPL ratio unchanged at 1.5%

What you need to know about UOB 1Q26 results

UOB Group has reported net profit of S$1.44 billion for 1Q26. This represents a 4% decrease compared to the previous year, but a 2% increase from the prior quarter.

#1 - Net interest margin narrowed slightly

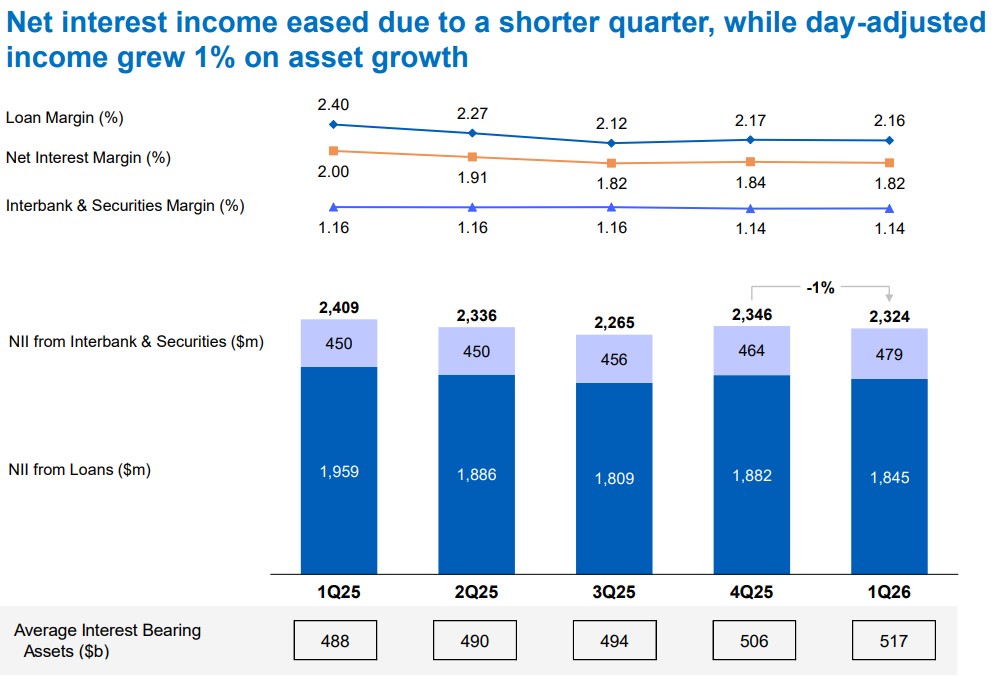

Net interest income declined 1% quarter-on-quarter (QoQ) and 4% year-on-year (YoY) to S$2.32 billion, weighed down by a shorter quarter and continued margin pressures from a lower interest rate environment. Healthy loan growth of 4% year-on-year provided some cushion.

Net interest margin narrowed by 2 basis points (0.02%) to 1.82% in 1Q26 from 1.84% in 4Q25, as asset repricing pressures were partially offset by active funding cost management. The 3-month SORA average fell 16 basis points (0.16%) during the quarter, while 1-month HIBOR average dropped 72 basis points (0.72%).

#2 - Fee income up QoQ but lower YoY against record base

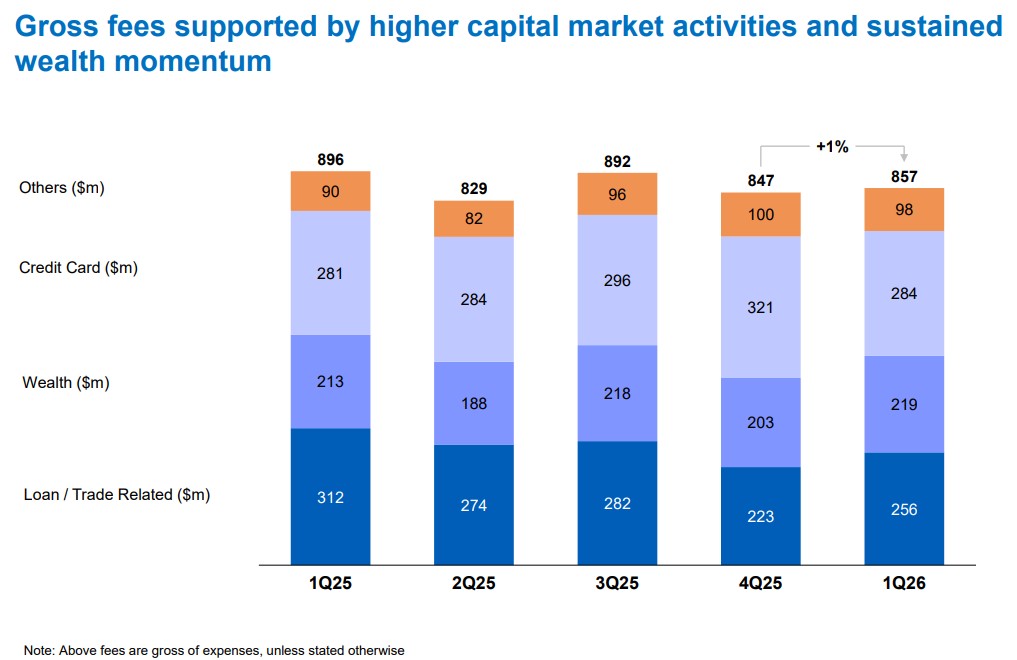

Net fee income reached S$637 million in 1Q26, up 2% quarter-on-quarter, supported by stronger capital market activities and sustained momentum in wealth management.

Compared to the year before, fee income declined 8% from last year's record high, as investment banking and loan-related activities moderated amid a more cautious, risk-off market sentiment.

Other non-interest income rebounded 45% quarter-on-quarter to S$462 million, lifted by stronger customer treasury income and trading activities that benefitted from market volatility. On a year-on-year basis, this line was 17% lower.

#3 - Credit costs within guidance, asset quality stable

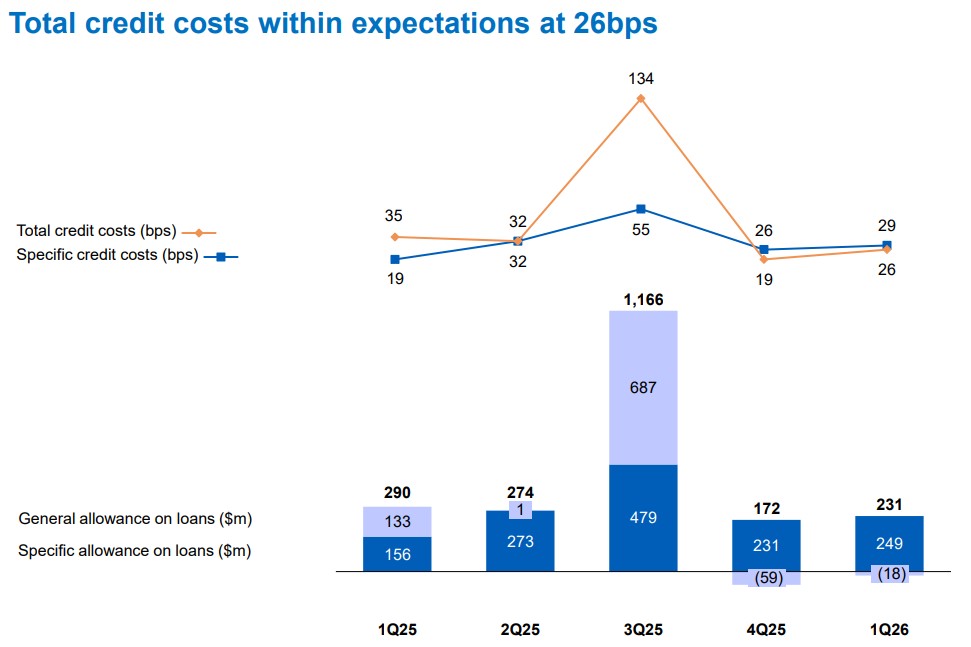

Total allowance increased to S$203 million in 1Q26 (from S$113 million in 4Q25), mainly due to a smaller write-back of general allowance. This translated to total credit costs on loans of 26 basis points, well within UOB's full-year 2026 guidance of 25–30 basis points.

Asset quality remained stable, with the non-performing loan (NPL) ratio unchanged at 1.5%. Non-performing assets (NPA) coverage strengthened to 100% (or 272% after taking collateral into account), up from 97% in the prior quarter. Performing loans coverage was steady at 1.0%.

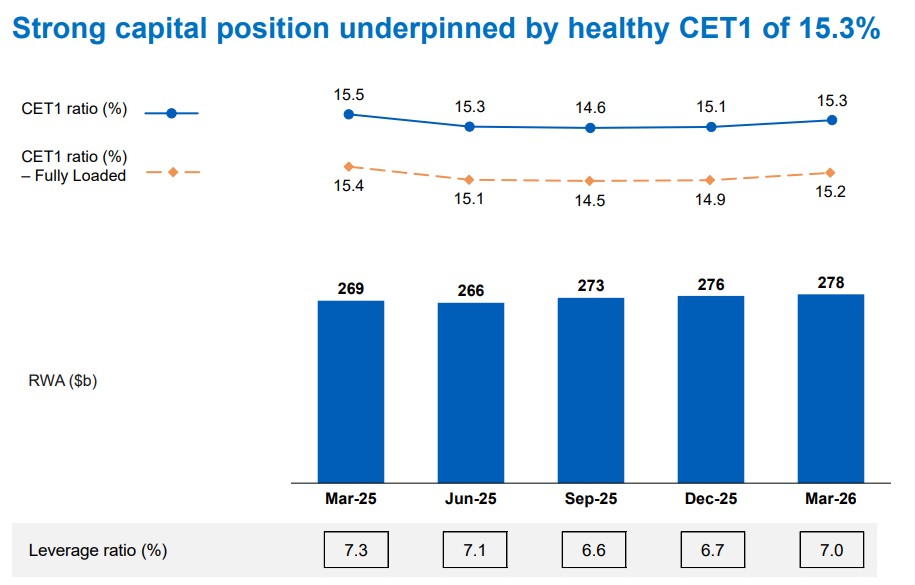

#4 - Strong capital and liquidity position maintained

The Group's capital position strengthened, with the Common Equity Tier 1 (CET1) ratio rising to 15.3% in 1Q26 from 15.1% in 4Q25. Liquidity metrics stayed robust, with the all-currency liquidity coverage ratio at 144% and net stable funding ratio at 115%, both comfortably above regulatory requirements.

Cost-to-income ratio improved to 44.5% from 46.4% in 4Q25, reflecting ongoing cost discipline, with total expenses broadly unchanged at S$1.5 billion.

UOB does not declare a dividend at the first-quarter mark, with interim dividends typically announced alongside half-year results.

#5 - 2026 outlook unchanged

UOB kept its full-year 2026 guidance unchanged.

The bank expects low single-digit loan growth, net interest margin of 1.75% to 1.80%, high single-digit fee income growth, and low single-digit growth in operating costs.

It also expects total credit costs to remain within the 25 to 30 basis points range.

UOB added that its exposure to the Middle East is limited, and that these exposures have been stress-tested.

Management said the bank’s capital and provision buffers remain resilient.

Beansprout’s Quick Take on UOB earnings

While UOB 1Q26 net profit dipped 4% year-on-year due to a stronger base last year, the bank continued to show resilient margins, stable credit costs, and healthy growth in its wholesale banking franchise.

As interest rates normalise, net interest income growth is slowing, with fee and trading income becoming more important drivers of performance.

Trading income rebounded strongly during the quarter, although fee income remained softer amid weaker investment banking and loan-related activity.

Looking ahead to 2026, UOB maintained its guidance of steady but modest growth, with low single-digit loan growth and a full-year net interest margin of 1.75%–1.80%.

UOB is currently trading at 4.6% forward dividend yield, lower than its historical average of 4.8%. In comparison, DBS is trading at a higher forward dividend yield of 5.5% while OCBC is lower at 4.4% forward dividend yield.

Its current price-to-book ratio of 1.25x is also slightly above historical average of 1.14x.

Related links:

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in UOB.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments