UOB reports 7% decline in 4Q25 profit and lowers final dividend: Our Quick Take

Stocks

By Gerald Wong, CFA • 24 Feb 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

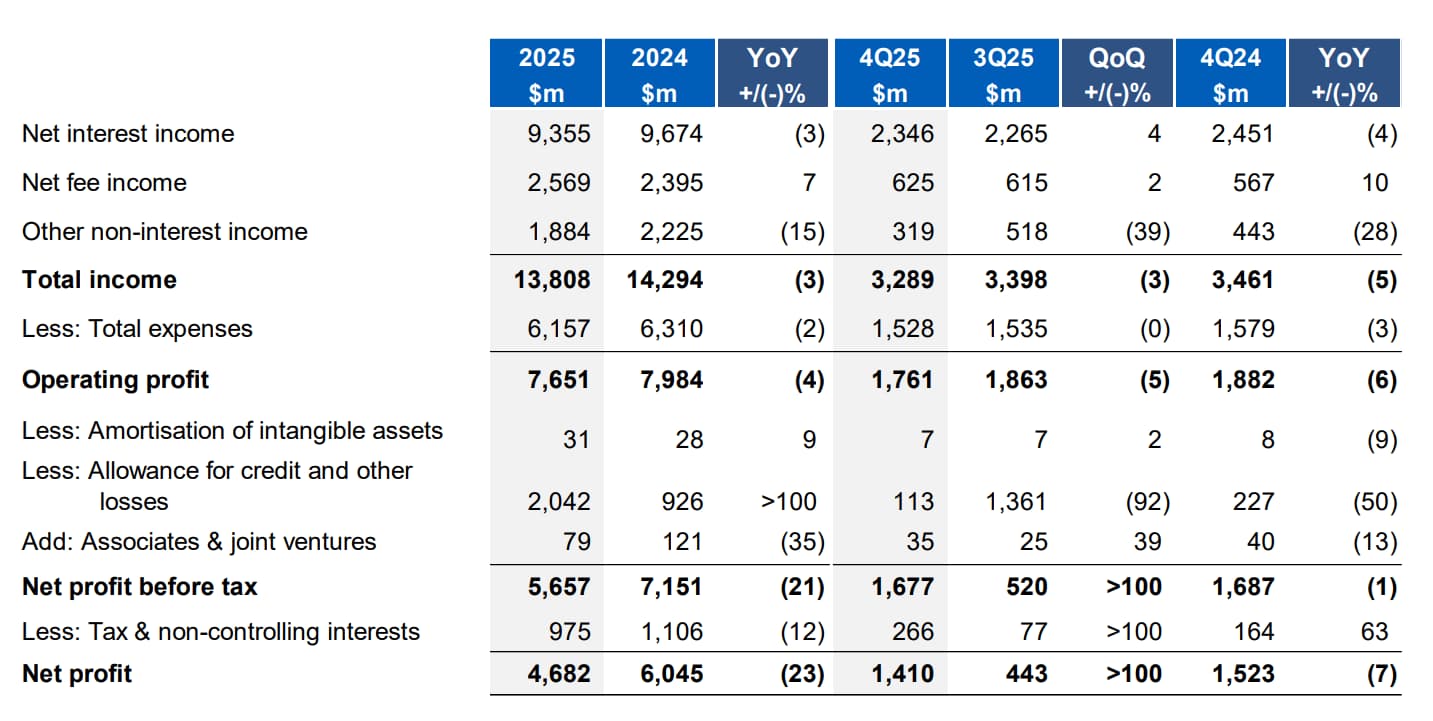

UOB reported a 7% drop in 4Q25 net profit and a lower final dividend of S$0.71.

UOB 4Q25 earnings highlights

UOB Group announced its earnings for the fourth quarter of 2025. Key highlights include:

- Net profit of S$1.41 billion in 4Q 2025, down 7% year-on-year

- Net profit of S$4.68 billion in FY 2025, down 23% year-on-year

- Final dividend of S$0.71 per ordinary share

What you need to know about UOB 4Q25 results

UOB Group has reported net profit of S$1.41 billion for 4Q25. This represents a 7% decrease compared to the previous year.

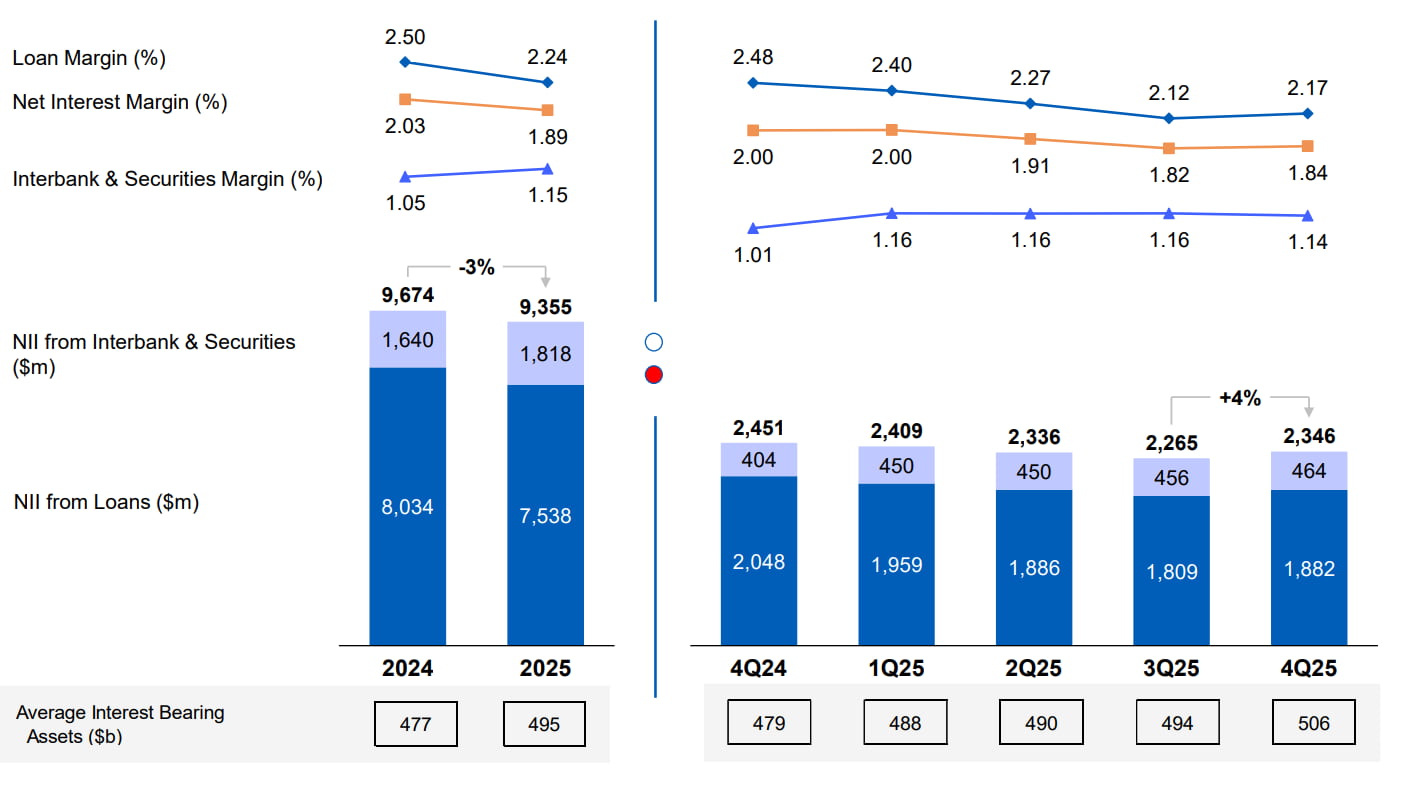

#1 - Net interest margin improved quarter-on-quarter

Net interest income fell 4% year-on-year to S$2.3 billion as margin headwinds outweighed healthy loan growth of 4%. 3-month SORA rate declined by 43 basis points in 4Q25.

Net interest margin improved from 1.82% in 3Q25 to 1.84% in 4Q25, supported by proactive funding cost management.

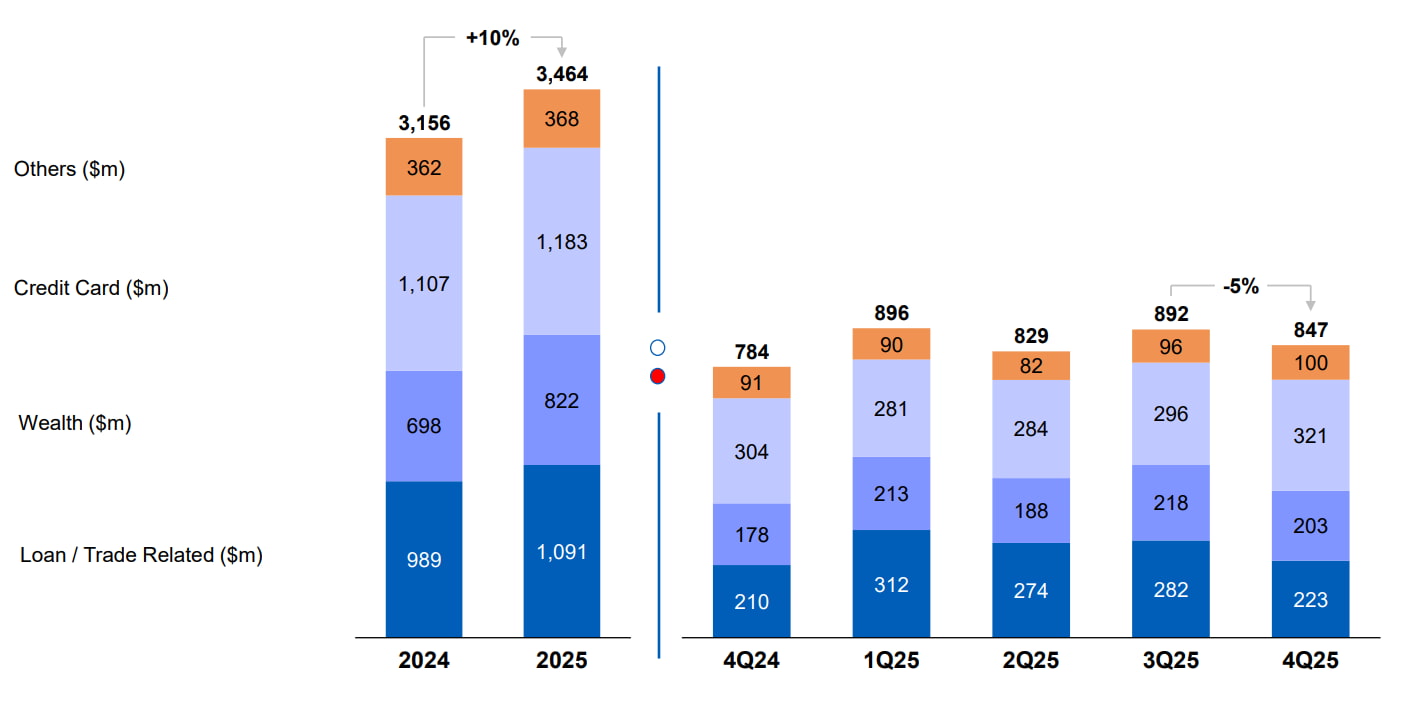

#2 - Fee income grew in 4Q25

Fee income reached S$625 million in 4Q25, representing a growth of 10% compared to 4Q24 as wealth management and loan-related fees reached new heights amid favourable market conditions and rising consumer confidence.

Other non-interest income fell 28% on lower trading and investment income to S$319 million in 4Q25.

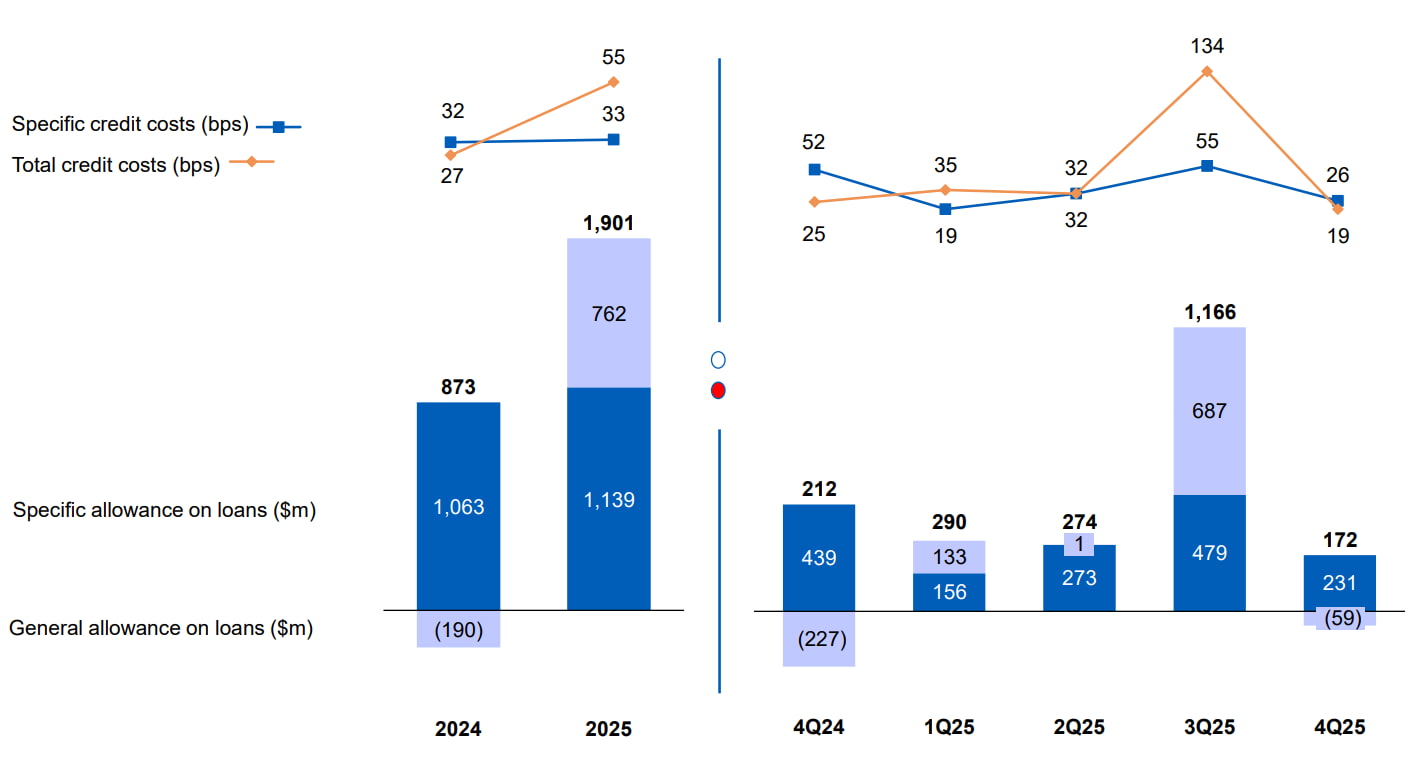

#3 - Lower specific allowance

Total allowance normalised to S$113 million in 4Q25 following last quarter's pre-emptive general allowance, and lower specific allowance to S$231 million in 4Q25 (from S$479 million in 3Q25).

This lowered total credit costs on loans to 19 basis points (0.19%).

The performing loan coverage was stable at 1.0% as of end-December 2025, unchanged from last quarter.

The asset quality remained healthy as non-performing loan (NPL) ratio improved to 1.5% from 1.6% in 3Q25, with non-performing assets (NPA) coverage adequate at 97% or 254% after taking collateral into account.

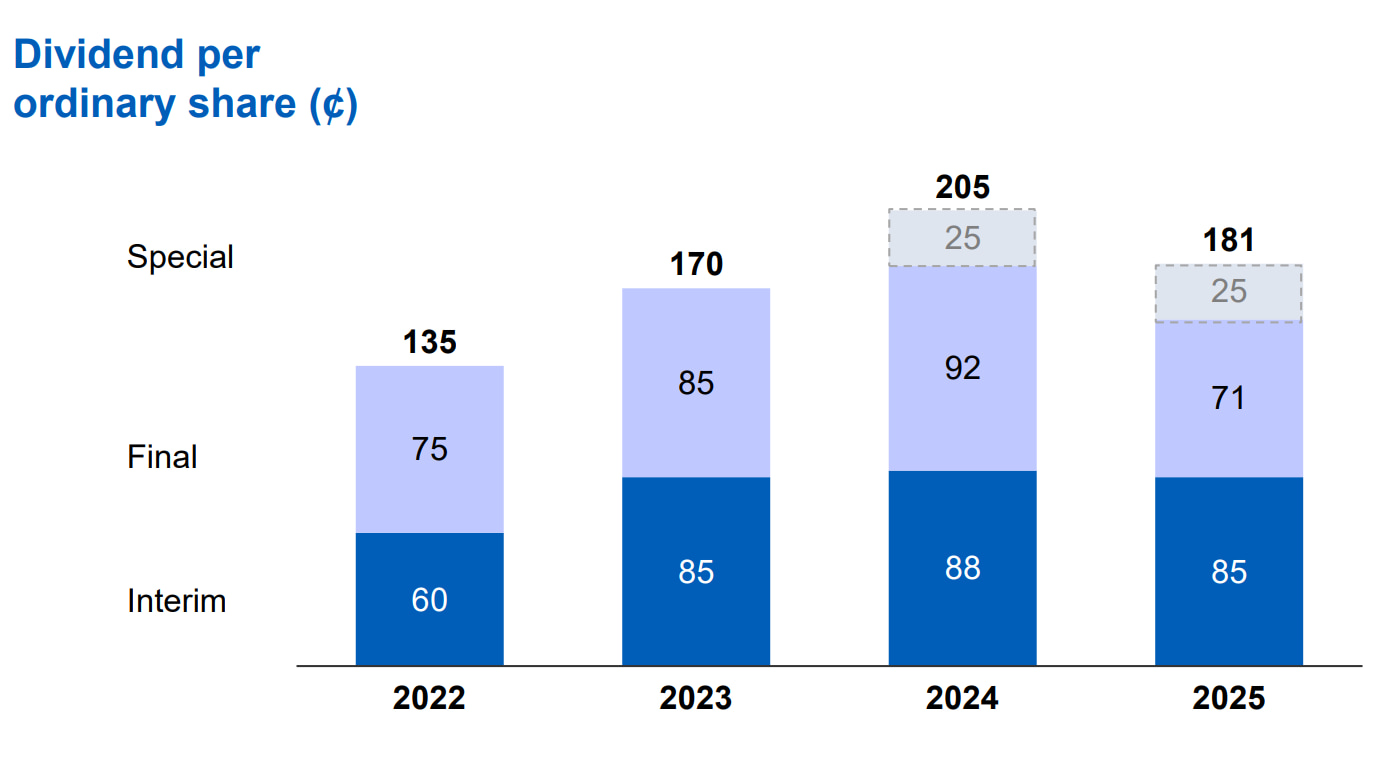

#4 - Final dividend of S$0.71 per share

UOB proposed a final dividend of S$0.71 per share, together with the interim dividend of S$0.85 per share, the total dividend for FY25 will be S$1.56 per share, representing a payout ratio of approximately 50%.

In addition to the regular dividends, the Group returned surplus capital to shareholders through a special dividend of 50 cents per ordinary share, which was paid over two tranches during 2025.

#5 - 2026 outlook

For 2026 outlook, UOB expects low single-digit loan growth, net interest margin of 1.75% to 1.80% and high single-digit fee income growth.

Operating cost is expected to increase at low-single digit while total credit costs will normalise are expected to be benign in the 25-30 basis points (0.25-0.3%) range.

Beansprout’s Quick Take on UOB earnings

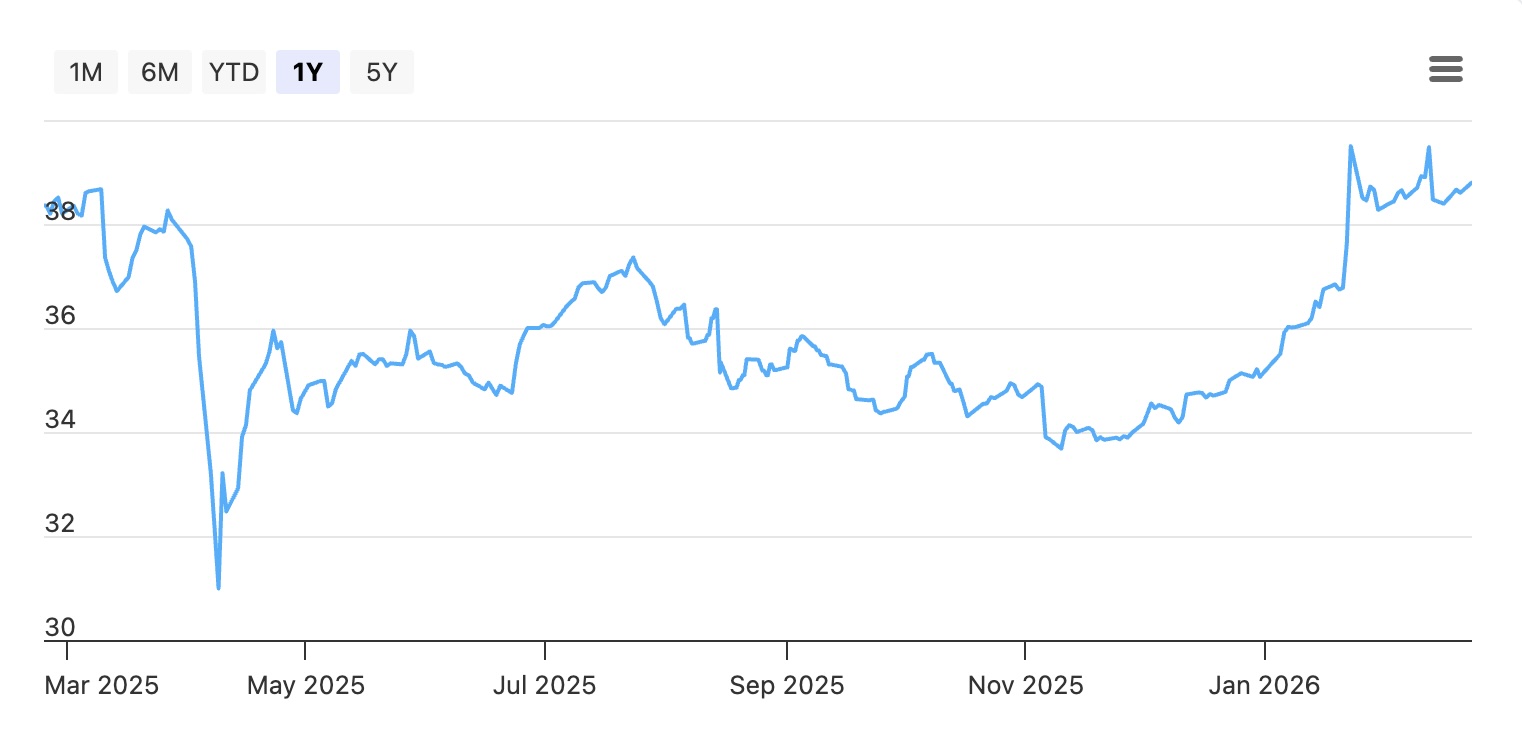

UOB share price has done well year-to-date, up 10.7%, leading OCBC’s 9.8% and 3.2%.

UOB’s share price recovery year-to-date suggests investors are looking past the 3Q25 earnings shock, recognising that the sharp drop in quarterly profit was driven primarily by proactive general provisions rather than deterioration in the core franchise.

Looking ahead to 2026, UOB’s guidance points to steady but modest growth, with low single-digit loan growth and a full-year net interest margin of 1.75%–1.80% signalling some margin pressure as rates normalise.

The bank is targeting high single-digit fee growth and low single-digit operating cost growth, which suggests it will lean more on wealth and fee-based income while keeping a tight lid on expenses to support profitability. Total credit costs expected to normalise at 25–30 basis points.

However, the decision to declare a lower final dividend of S$0.71 per share for FY25, a 23% decline from the S$0.92 final dividend in FY24, stands in contrast to DBS, which reported a 10% decline in net profit but still raised its dividend.

This is likely to reinforce the perception that UOB is taking a more conservative stance on capital returns.

According to consensus expectations, UOB is expected to offer a total dividend per share of S$1.72 in 2026. This would represent a potential dividend yield of 4.4% based on its closing price of S$38.80 on 23 February.

This would be lower than the dividend yield for DBS (including capital return dividend).

UOB currently trades at a price-to-book valuation of 1.36x, above its historical average of 1.0x.

Related links:

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in UOB.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments