Wee Hur Holdings: Strong performance across core segments

Stocks

By Goh Lay Peng • 23 Mar 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Wee Hur reported robust performance across core segments in 2H2025. Wee Hur also reported record order book and income visibility till 2031.

Robust performance across core segments in 2H 2025

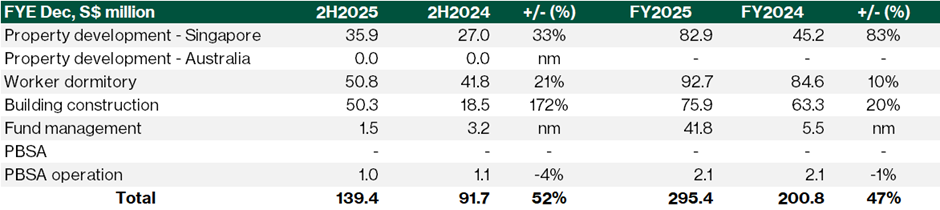

Revenue increased by 52% year-on-year in 2H2025, led by strong performance across its property, building construction, workers’ dormitory and management segments.

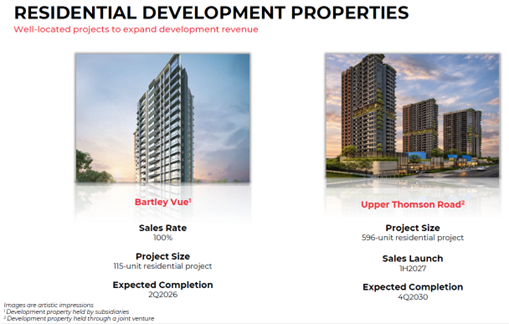

Property development (Singapore) segment reported 33% year-on-year increase in revenue, following higher progressive revenue recognition from Bartley Vue, which reached 84.9% completion in FY2025.

Workers’ dormitory reported revenue of S$50.8 million in 2H2025, an increase of 21% year-on-year, underpinned by robust performance from Tuas View Dormitory and Pioneer Lodge. Pioneer Lodge obtained Temporary Occupation Permit in 4Q2025. This is the second workers dormitory with a capacity of 10,500 beds. With Pioneer Lodge, raising Wee Hur’s total capacity to 26,244 beds, +66.7% year-on-year.

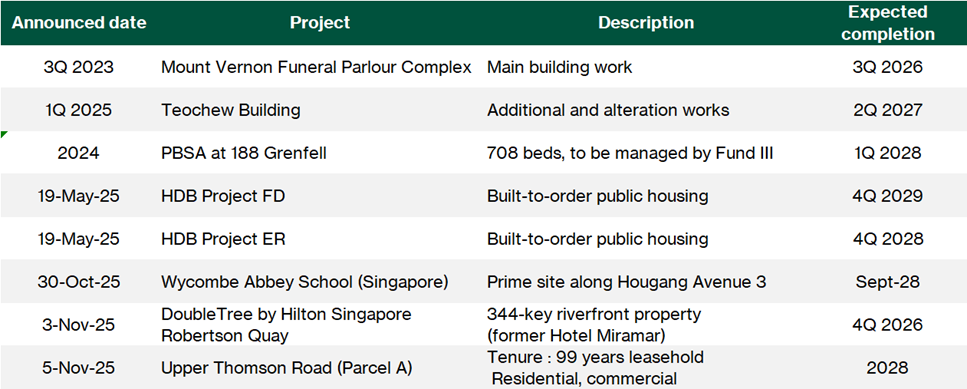

Building construction recorded revenue of S$50.3 million in 2H2025, an increase of 172% year-on-year. Higher revenue was led by progressive recognition from Mount Vernon Funeral Parlour and Teochew Building. In addition, two new projects have started to record revenue – Wycombe Abbey School and HDB ER Project.

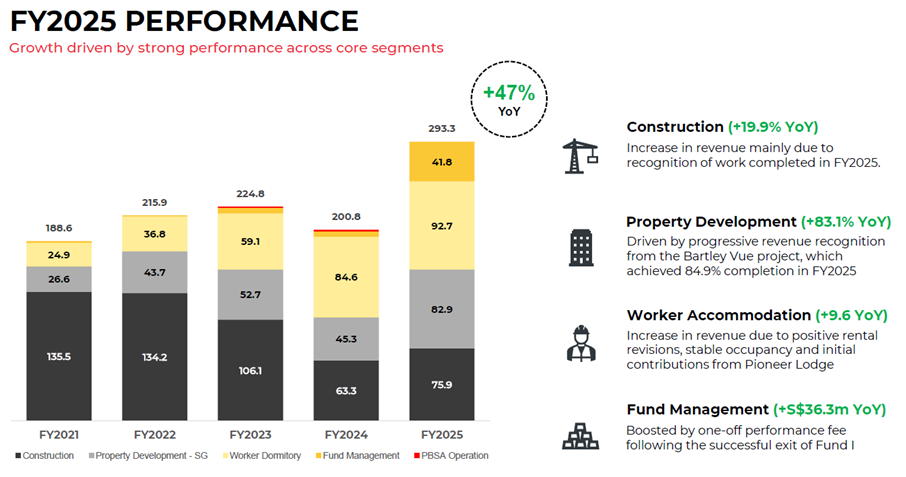

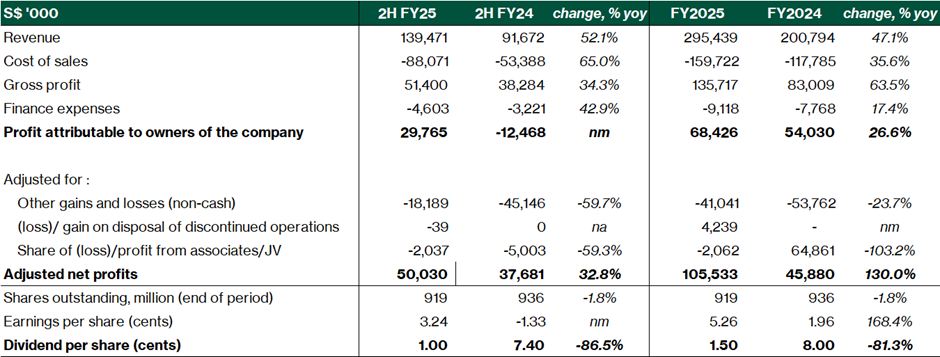

Revenue in FY2025 grew 47% year-on-year to S$295.4 million.

Gross profit grew faster at 63% to S$135.7 million, lifting gross profit margin to 45.9% from 41.3% a year earlier. The margin expansion was partly supported by a one-off performance fee of S$41.8 million from the partial sale of Fund I units. Construction and property development segments also recorded higher contributions.

Net profit attributable to equity holders increased 27% to S$68.4 million, while overall net profit rose 17% to S$66.7 million. However, share of results from associates and joint ventures declined sharply to a loss of S$2.1 million compared with a profit of S$64.9 million in FY2024, following the partial disposal of Fund I which reduced the remaining stake to about 13%.

After adjusting for non-cash items and one-off gains, adjusted net profit surged to S$105.5 million from S$45.9 million in the previous year. The improvement reflects stronger underlying performance across the group’s core business segments, particularly construction and property development, which more than offset the reduced contribution from associates and joint ventures.Top of Form

Record order book and income visibility till 2031

Building Construction

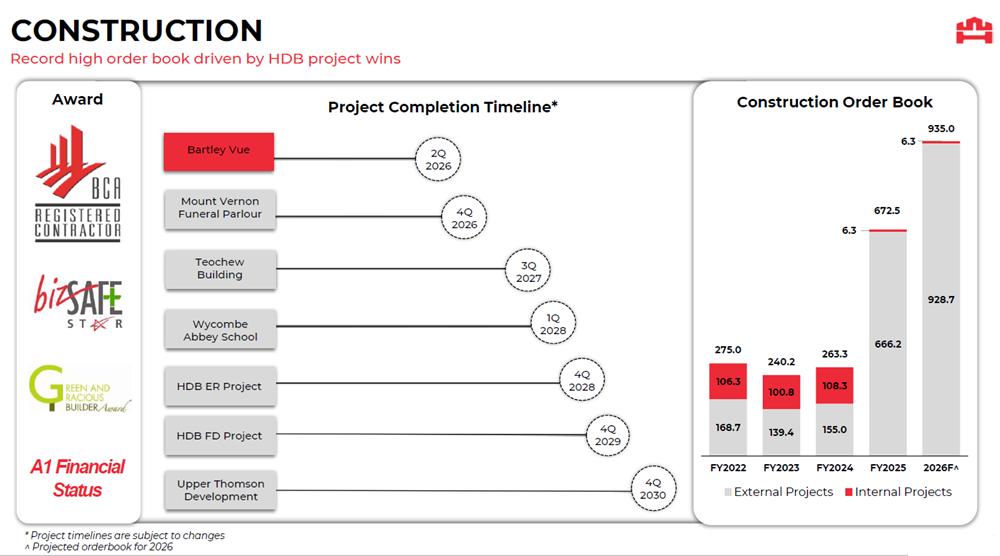

Building construction segment continues to perform strongly, supported by new project wins and a growing pipeline.

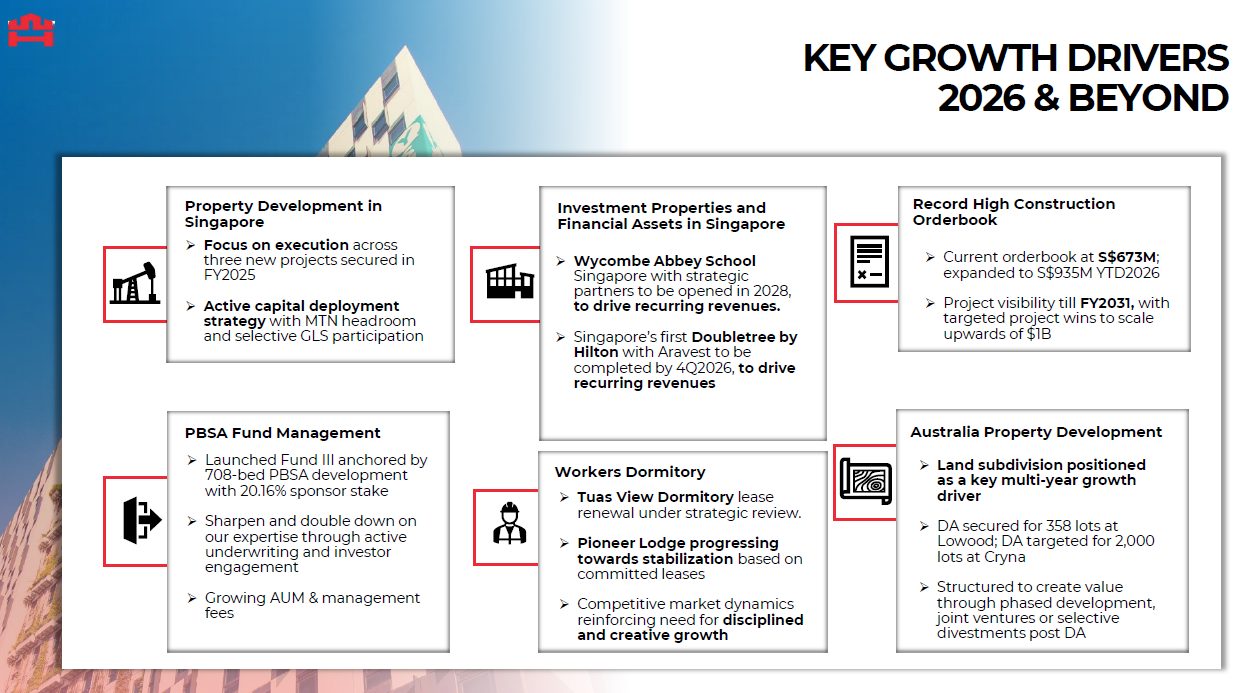

In FY2025, Wee Hur won three construction contracts, including two HDB build-to-order contracts worth S$439.4 million. In addition, it has a significant joint-venture stake in Wycombe Abbey International School. The construction project amount of Wycombe Abbey is S$148.5 million. As at FY2025, the construction order book increased to S$672.5 million, up 155% year-on-year.

The development at Upper Thomson will be added to the orderbook in FY2026. Order book is projected to rise further to around S$935.0 million in FY2026, providing strong revenue visibility over the next few years. The majority of projects are external contracts, reflecting its ability to secure work beyond its internal developments.

Current pipeline of projects is scheduled for completion between 2026 and 2030, including developments such as Bartley Vue, Wycombe Abbey School, and several HDB projects. This diversified project timeline supports sustained construction activity and underpins its medium-term earnings visibility.

Development and investment properties in Singapore

Wee Hur entered into joint venture to develop Wycombe Abbey School Singapore, representing a strategic entry into the premium international education sector. With a planned capacity of 1,800 students, the school will be an extension of the prestigious UK-based Wycombe Abbey brand, catering to growing demand from both local and expatriate families seeking world-class education. This investment diversifies the portfolio beyond traditional real estate, tapping into Singapore's position as a regional education hub.

In FY2025, Wee Hur made significant advancement in development and investment properties pipeline. Wee Hur has been awarded the Upper Thomson Government Land Sales development (Parcel A). This 596- unit project is expected to be launched in the first half of 2027 and completed by the first half of 2031. Wee Hur holds a 50% stake in this development through an investment in joint venture. Given the limited upcoming supply and strong take-up of existing developments in the vicinity, it believes it is well-positioned to benefit from sustained demand in the area.

Wee Hur invested in the redevelopment of DoubleTree by Hilton Singapore. The targeted launch is in the fourth quarter of 2026, signals a bullish outlook on Singapore's hospitality sector. The redevelopment is expected to modernise the property and enhance its competitive positioning as tourism and business travel continue to recover and grow. This project strengthens the company's presence in the hotel and hospitality segment, capitalising on Singapore's strong appeal as a global travel destination.

Development and investment properties in Australia

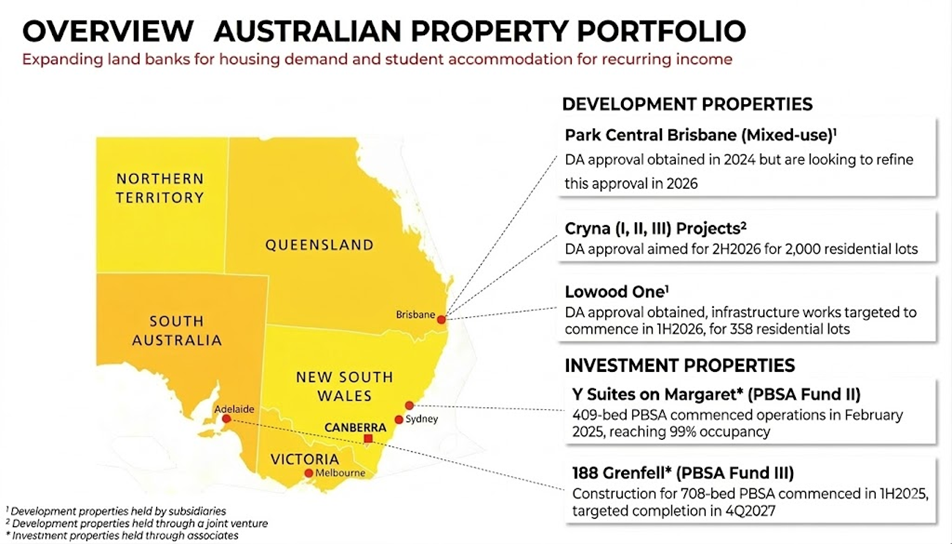

For the development properties, Wee Hur is building a substantial land bank and securing Development Approvals to capture long-term Australian housing demand.

Park Central Brisbane is a mixed-use project that secured development approval in 2024, with plans to refine the approval in 2026 to optimise the project's scope.

The Cryna (I, II, III) Projects represent a sizeable pipeline of approximately 2,000 residential lots, with development approval targeted for the second half of 2026.

Lowood One has already obtained its development approval for 358 residential lots, with infrastructure works expected to commence in the first half of 2026. These three projects collectively position the company to benefit from Queensland's sustained population growth and housing undersupply.

Investment properties are two projects in Purpose-Built Student Accommodation Fund II and Fund III (PBSA Fund II and Fund III). Wee Hur’s stake in Fund II and Fund III are 30% and 20.1%, respectively.

Y Suites on Margaret, held under PBSA Fund II, is a 409-bed facility located in Brisbane that commenced operations in February 2025 and has already achieved an impressive 99% occupancy rate, demonstrating strong demand for quality student housing.

188 Grenfell under PBSA Fund III, a larger 708-bed PBSA development in Adelaide where construction began in the first half of 2025 and is targeted for completion by the fourth quarter of 2027

Healthy liquidity and financial flexibility

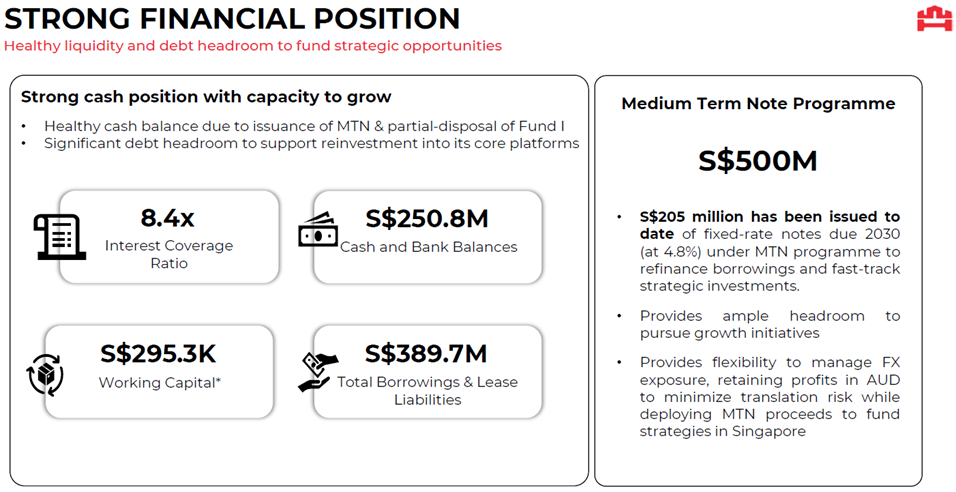

It maintains a strong financial position, supported by healthy liquidity and ample debt headroom to pursue strategic growth opportunities.

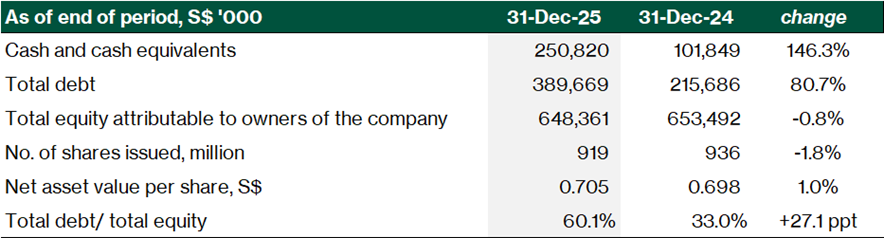

Cash and bank balances stood at S$250.8 million, bolstered by the issuance of Medium Term Notes (MTN) and proceeds from the partial disposal of Fund I. The Group also reported a robust interest coverage ratio of 8.4 times, reflecting its strong ability to service debt obligations.

Total borrowings and lease liabilities amounted to S$389.7 million, while working capital remained positive. The balance sheet strength provides flexibility for the Group to reinvest into its core platforms and support future expansion initiatives.

The Group has established a S$500 million MTN programme, of which S$205 million of fixed-rate notes due 2030 have been issued at an interest rate of 4.8%. The programme provides additional funding capacity to refinance existing borrowings, pursue growth opportunities, and manage foreign exchange exposure while deploying capital across its investment strategies.

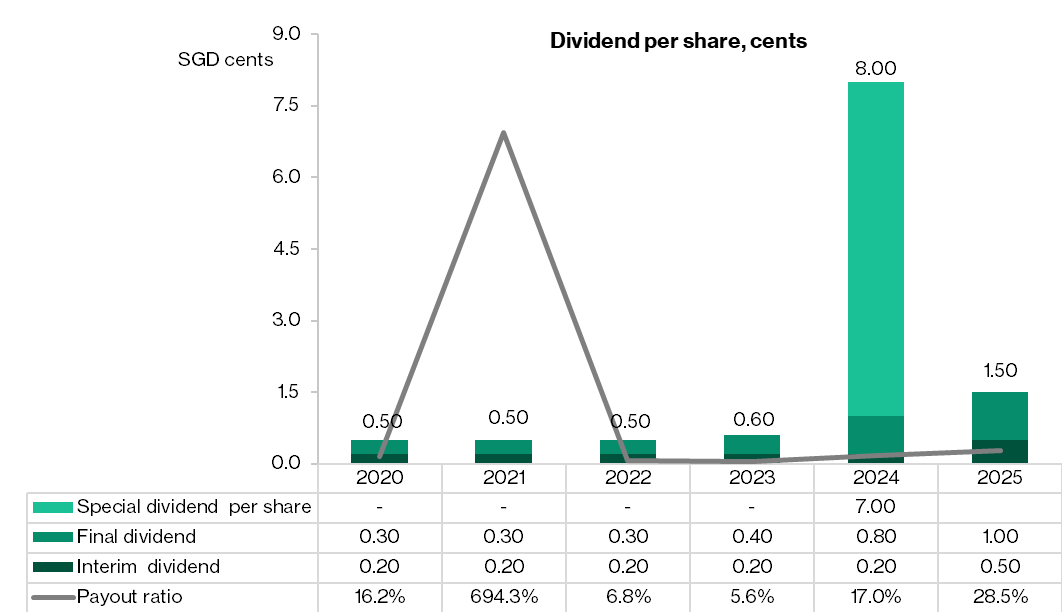

2H FY25 dividend per share rose by 25% year-on-year

Wee Hur recommended DPS of 1.00 cents for 2H FY2025, an increase of 25% year-on-year. The higher dividend per share was driven by strong revenue growth across the segments.

Total dividend per share in FY2025 of 1.50 cents translates to dividend payout ratio of 28.5% of profit after tax and non-controlling interests. Management continues to reinvest earnings in order to generate higher shareholders’ returns.

Outlook

Wee Hur continues to strengthen the core businesses with record order book and income visibility till 2031. To recap, order book of construction segment was S$673 million in FY2025 and expected to reach S$935 million in FY2026. Property development will be driven by the three new projects secured in FY2025. The debt headroom will be deployed into selective government land sales (GLS) participation.

Wee Hur is steadily building a portfolio of assets designed to secure long-term recurring income. These include the workers’ dormitory and purpose-built student accommodation (PBSA). In FY2025, it has also diversified into education and hospitality through The Wycombe Abbey School Singapore and the DoubleTree by Hilton Singapore. On the PBSA front, it has pared down a substantial stake in Fund I and actively rebuild scale with the launch of Fund III. These assets provide defensive earning streams that are relatively stable.

In Australia, it is actively securing Development Approvals (DA) to capture long-term housing demand. Wee Hur has assembled a sizeable residential land bank in Queensland. It has secured DA for 358 lots at Lowood and a further 2,000 lots targeted at Cryna,. Management retains flexibility to monetise these assets through phased development, joint ventures, or selective divestments.

Maintain at Buy

Maintain at Buy with target price S$1.00. Currently trading at FY2025 PE 9.8x and PB 0.94x, Wee Hur's share price has not fully reflected potential upside drivers, in our view. These include successful stabilisation of Fund III, contribution from international school at Hougang and land rezoning projects in Australia. As the projects develop, the potential contribution from these businesses will become clearer. Cash flows from PBSA and PBWA will remain resilient against economic uncertainty.

Our target price at S$1.00 is based on sum-of-parts on the core business and growth engines. At S$1.00, Wee Hur is trading at FY2026E PE of 13.7x and FY2026E dividend yield 1.5%. The higher valuation compared with the companies in the construction industry reflects the potential upside drivers, diversified source of income and exposure to stable cashflows.

Wee Hur is an attractive investment with quality assets to support steady cashflow from diversified sources. By recycling capital, management aims to pursue new revenue streams in order to achieve a higher return on equity for the shareholders.

Key risks

Key risks include economic, regulatory, interest rate, execution, and concentration.

Economic and demand risk

A slowdown in economic activity, changes in employment conditions, or weaker student inflows could reduce demand for worker and student accommodation, affecting occupancy and rental growth. Currently, the elevated tariffs imposed by the United States, trade tensions between the United States and China and other geopolitical conflicts have led to heightened economic uncertainty. The company’s financial position may be affected if the demand for purpose-built accommodation is adversely affected, slowdown in new customers acquisition and longer receivables days, amongst others.

Regulatory and policy risk

Worker dormitories and student accommodation are subject to evolving regulations on zoning, operating standards, levies, and foreign student policies. Any tightening could raise compliance costs or limit capacity and returns. The company has to be mindful of the regulatory and policy risk in Singapore and Australia, the two key markets which they operate in. For example, in 2024, Australia implemented a cap on international students in order to reduce the overall migration to pre-pandemic levels. The average occupancy rate fell to 82.7% in 2024, from 90% in 2023. However, the proposed cap on international students did not pass into legislation, resulting in a surge in demand for Semester 1 of 2025.

Interest rate and financing risk

Higher interest rates increase borrowing costs and may pressure earnings, especially during development phases when gearing is elevated. Refinancing risk could also arise in volatile credit markets. Higher interest rates also raise the cost of acquisition, restricting the options to pursue opportunistic acquisitions.

Execution and development risk

Construction delays, cost overruns, or delays in achieving stabilised occupancy could defer cash flow generation and impact project returns, particularly for assets under development. In Australia, the company has obtained the development approval for Buranda Plot 2, Brisbane in 2024. However, the project is not viable for development due to the high construction costs. The company is exploring alternative options for the land parcel.

Concentration and operational risk

Earnings are exposed to specific asset types and geographies. Operational disruptions, tenant concentration, or weaker-than-expected leasing performance at key assets could have a disproportionate impact on results. The company’s recurring income are mainly generated from workers’ dormitories in Singapore and students’ accommodation in Australia. In order to diversify the source of recurring income, the company is entering the hospitality business by acquiring Hotel Miramar at Robertson Quay. The company plans to upgrade and rejuvenate the asset with the launch of DoubleTree by Hilton in 2026.

Check out Beansprout guide to the best stock trading platforms in Singapore with the latest promotions to Wee Hur Holdings.

Download the full report here.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments