Wee Hur - 5 key takeaways from SIAS Corporate Connect Webinar

Stocks

By Goh Lay Peng • 08 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We share five key takeaways from the SIAS Corporate Connect webinar with Wee Hur, including Singapore's construction sector, workers dormitory market, residential property cycle and Australia PBSA — and how capital from the A$1.6 billion Fund I exit is being redeployed into new growth opportunities.

What happened?

Wee Hur Holdings is a Singapore-listed company with an integrated business spanning four segments: building construction, workers dormitories, property development, and purpose-built student accommodation (PBSA) fund management.

Wee Hur recently participated in a Corporate Connect session organised by SIAS, supported by SGX Group, to share updates on its strategy and the market backdrop across each of its key businesses.

The session covered the construction sector outlook, the workers dormitory market, the Singapore residential property environment and Australia PBSA trends — and how Wee Hur is strategically positioned across all four. We spoke with Goh Wee Ping, Chief Investment Officer of Wee Hur, to understand how these developments could shape the company’s prospects and future returns for shareholders.

Watch the video to learn more about Wee Hur.

Key Takeaways from Corporate Connect Webinar with Wee Hur

Here are our five key takeaways from the discussion:

- Successfully monetised PBSA portfolio and redeployed capital into new Singapore and Australian opportunities

- Construction order book on track to exceed $1 billion, with revenue visibility through 2030

- Australian land subdivision business scaling significantly with a large pipeline in Southeast Queensland

- New investments in residential, education and hospitality underpinned upside potential to analysts’ valuation

- PBSA platform poised for Asia-Pacific growth, supported by a capital-light model and disciplined capital allocation

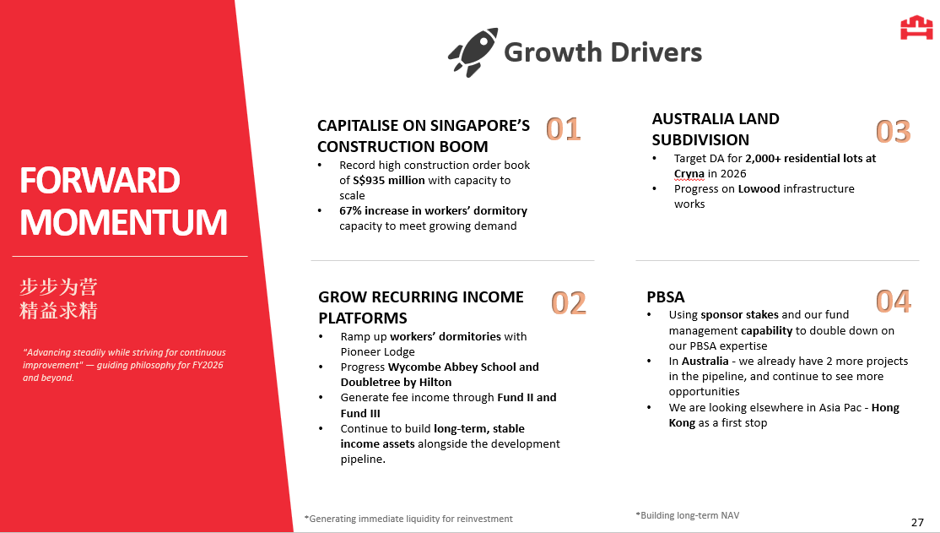

#1 – Capital recycled from PBSA into a diversified pipeline of new opportunities

The successful completion of Wee Hur’s PBSA monetisation cycle demonstrates management’s strong execution capabilities and ability to unlock value from its investments.

The company sold its Australian student housing assets to Greystar and GIC, completing a cycle that began in 2017, partial sale to GIC in 2022. The major milestone is a sale by Wee Hur and GIC to Greystar in 2025. The transaction returned net cash proceeds to the company and validated management’s asset-light approach to growing the PBSA business.

Rather than holding the Australian dollar proceeds, management chose to raise $205 million in Singapore dollars through a maiden medium-term note (MTN) programme at 4.8% over five years in November 2025. This allowed them to fund Singapore-based investments using local currency while keeping Australian capital deployed in Australia.

The redeployment resulted in three new Singapore project types being added to the portfolio: residential development through the Upper Thomson GLS and Springleaf sites totalling 596 units, an international school through a 60% stake in Wycombe Abbey School for 1,800 students, and a hospitality investment through a 20% minority stake in a DoubleTree by Hilton conversion from the former Hotel Mirama.

Management described this as a deliberate effort to diversify income streams and build a broader Singapore asset base over the next few years.

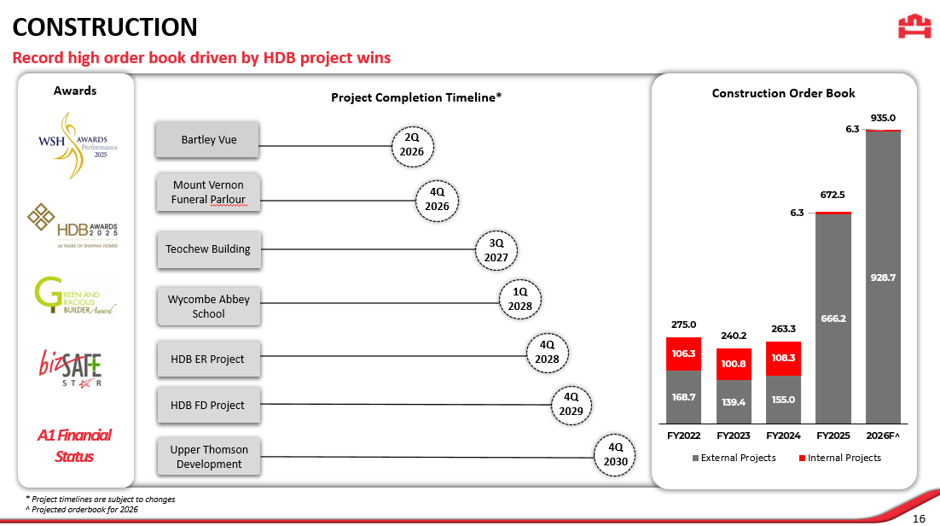

#2 – Construction order book on track to exceed $1 billion with visibility through 2030

Wee Hur’s construction business is entering a strong growth phase, with the order book standing at $672.5 million at end-2025 and expected to grow to $935 million in 2026 once the Springleaf GLS project is included.

Management expressed confidence in exceeding the $1 billion mark within six months, supported by active bidding activity across both public and private sector projects. Project completions are spread evenly from 2026 through 2030, providing multi-year revenue visibility.

Singapore’s construction boom is expected to persist for at least another two to three years, supported by a healthy pipeline of new tender awards. Importantly, projects secured during this period are typically executed over three to five years, providing sustained revenue visibility and potentially extending the construction upcycle well into 2030 to 2032.

Target construction margins are 8% to 10%, balancing competitiveness with profitability. To win HDB projects, which are evaluated 60% on price and 40% on quality metrics, management focused heavily on improving safety scores after COVID-19. This effort paid off with two HDB project wins last year.

One medium-term risk flagged was talent competition. Large upcoming projects such as the Marina Bay Sands Tower 2, estimated at $10 billion, could cause significant reshuffling of engineers across the industry. Management is preparing for this over a two to three year horizon.

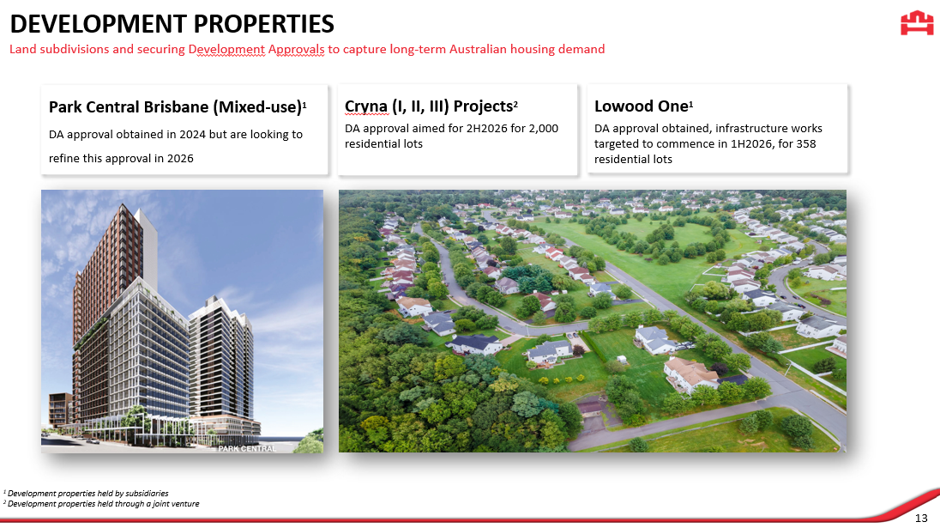

#3 – Australian land subdivision business scaling to over 2,000 lots in Southeast Queensland

In addition to doubling down on PBSA, Wee Hur has been building an Australian land subdivision business over the past three years, and management indicated it is now ready to scale significantly.

The business targets Australian homeowners who prefer 450 to 800 square metre lots for single or two-storey houses. Developers acquire agricultural land, obtain planning approvals for master-planned communities, install infrastructure including roads, sewerage and utilities, and then sell the lots.

The flagship project is Cryna in Southeast Queensland, where Wee Hur has accumulated sufficient land for approximately 2,000 residential lots under development application. This should be extremely accretive to bottom line. A smaller project in Lowood with around 400 lots is preparing to begin infrastructure works.

Management was careful to distinguish this from speculative land banking. The company only acquires land within urban planning zones already designated for low-density housing. Due diligence includes assessing the attitude of local city councils during the acquisition process.

Land parcels generate no income during the one to two year approval period, but this is factored into the business model upfront. Management noted that the experienced ground team’s track record to date shows timeframes have been managed well.

#4 – New investments not yet reflected in analyst consensus

A key message for investors was that several major value drivers are not yet captured in analyst estimates.

Management noted that the three significant Singapore investments — Springleaf residential, Wycombe Abbey School and the DoubleTree by Hilton — have not been incorporated into consensus estimates. Currently, the net asset value is at 73 to 75 cents per share, with the stock trading slightly below that level.

The Springleaf GLS site is expected to begin construction by end of Q2 2026 or early 2027, with a sales launch targeted for the first half of 2027. The residential market grew 2.3% in 2025 and management expects stable conditions to continue.

The DoubleTree by Hilton conversion targets opening by the time of the 2026 Singapore Formula 1 Grand Prix, with a light-touch renovation of rooms and internal amenities. Wycombe Abbey School construction targets completion by late 2027 or early 2028, with first students expected in September 2028.

Management plans to communicate more details over the coming months on the expected contributions from these assets, which they believe will help investors better value the company.

The workers dormitory business also offers a near-term earnings uplift. Pioneer Lodge in Jurong West, with 10,500 beds, is currently at 75% occupancy and is expected to reach 90% by year-end. The operating break-even is as low as 30% to 40% occupancy, making this a high-margin business already well past its break-even threshold.

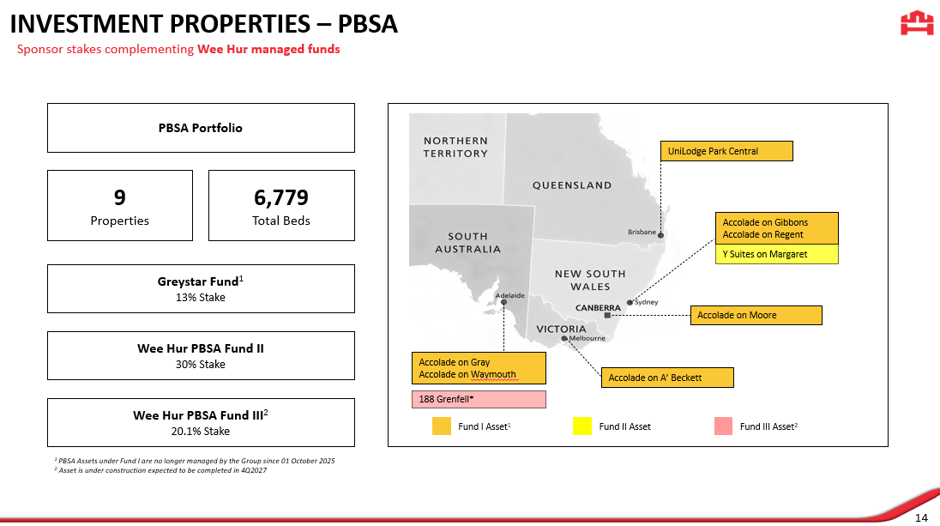

#5 – PBSA platform poised for Asia-Pacific growth, supported by a capital-light model and disciplined capital allocation.

Having completed the entire monetisation cycle of PBSA Fund I, Wee Hur plans to leverage on their PBSA expertise. With the demonstrated track record, Wee Hur is now able to attract institutional capital for partnership or co-invest in Wee Hur’s next phrase growth in Australia student housing.

Management sees the PBSA expertise built over 2016 to 2024 as a template for expansion into Hong Kong, Singapore and other Asia-Pacific markets. Future projects would require only 10% to 20% balance sheet allocation, with institutional capital partners providing the rest — a significant improvement on the capital intensity of the early PBSA years.

Wee Hur is mindful on a disciplined capital allocation policy. Management described pre-approved financial hurdles at both the group and board level, with a long-term target of 10% annual net tangible asset growth. This target has been achieved consistently from 2008 to 2025, spanning close to 20 years, and the second generation of management is aiming to improve on this track record.

The company does not have a formal dividend policy but has traditionally paid a yield of around 2% to 3% based on share price. As the share price has risen from the 20 to 30 cent range historically to the current 60 to 70 cent range, management has tried to maintain proportional dividends.

Hear directly from management of Wee Hur

Watch the full Corporate Connect webinar with Wee Hur on SIAS’s YouTube channel to catch the complete discussion and hear the insights straight from the company.

Follow us on Telegram, Youtube, Facebook and Instagram to get the latest financial insights.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments