OCBC reports 3% rise in net profit and higher final dividend: Our Quick Take

Stocks

By Gerald Wong, CFA • 25 Feb 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

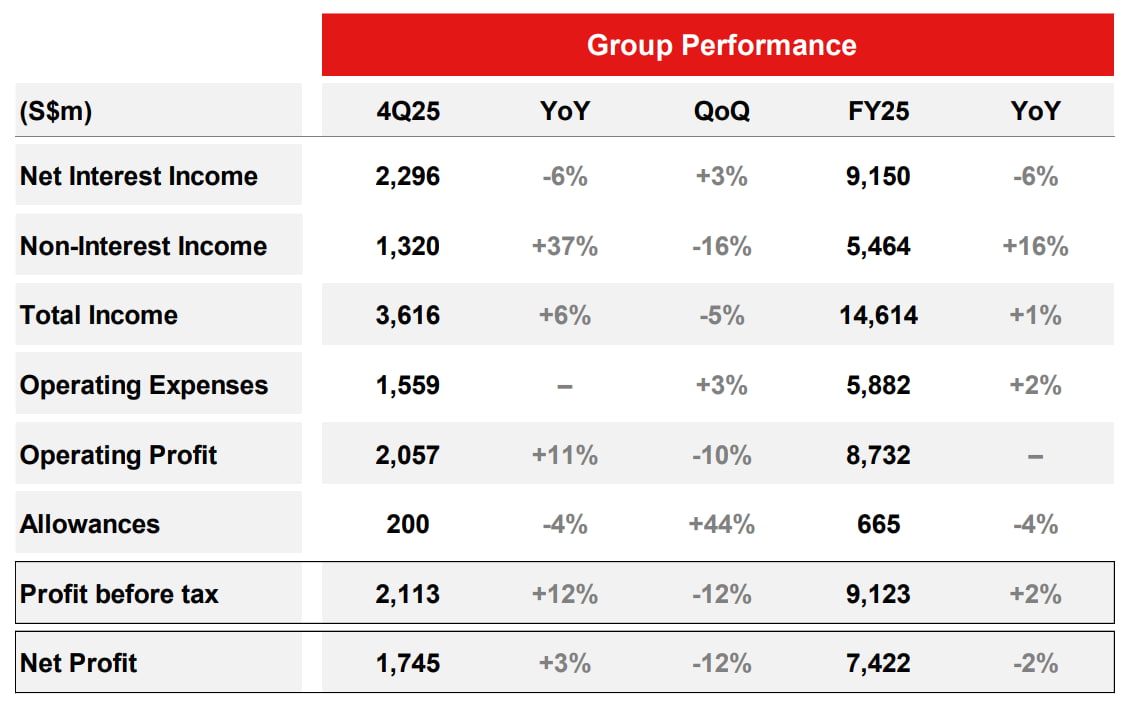

OCBC Group has reported net profit of S$1.75 billion for 4Q25, a 3% increase compared to the previous year and a higher final dividend of S$0.42 per share.

OCBC 4Q25 earnings highlights

OCBC announced its earnings for the fourth quarter of 2025 (4Q25). Key highlights include:

• Net profit of S$1.75 billion in 4Q25, 3% higher compared to the previous year, and higher than Factset consensus forecasts of S$1.73 billion. Net profit reached S$7.42 billion in FY25, down 2% year-on-year

4Q25 consensus forecast 1.73 billion 7.43 billion FY2025

FY25 consensus DPS 0.991, FY26 consensus DPS 0.978

• Final dividend of S$0.42 per share, slightly higher compared to the previous year’s S$0.41 per share. Special dividend of S$0.16 per share.

• Committed to complete S$2.5 billion capital return plan by FY26

What you need to know about OCBC 4Q25 results

OCBC Group has reported net profit of S$1.75 billion for 4Q25. This represents a 3% increase compared to the previous year.

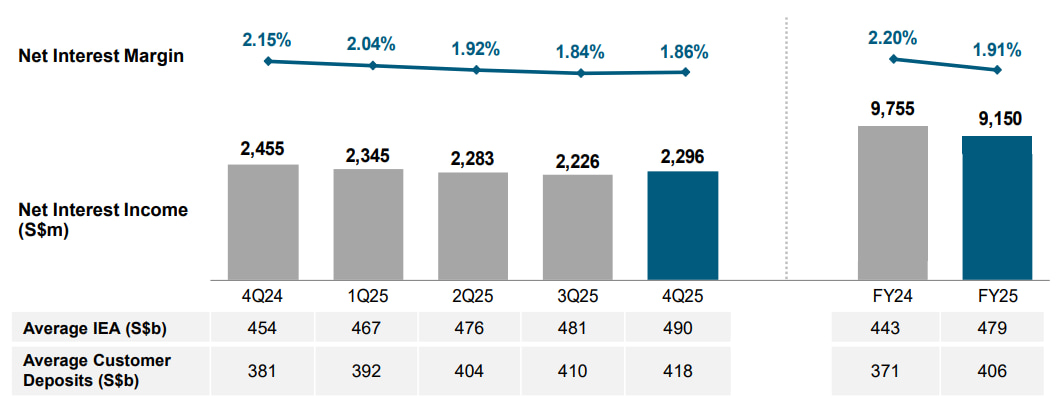

#1 - Net interest margin improved quarter-on-quarter

OCBC's total income for the fourth quarter of 2025 rose to S$3.62 billion, marking a 6% increase from the same period last year.

OCBC’s net interest income for 4Q25 fell 6% year-on-year to S$2.30 billion, as asset yields declined faster than deposit costs in a lower interest rate environment. The impact was partly offset by 8% growth in average assets.

OCBC's net interest margin improved to 1.86% in 4Q25 from 1.84% in 3Q25.

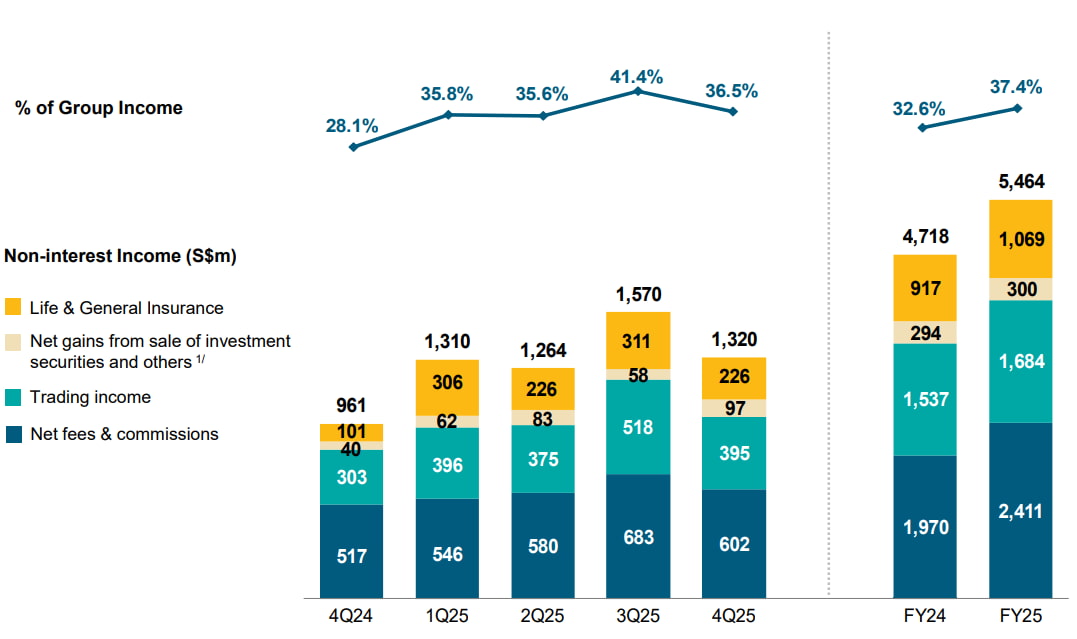

#2 - Non-interest income grew in 4Q25

Non-interest income rose 37% year-on-year to S$1.32 billion, supported by broad-based growth across fee, trading and insurance income.

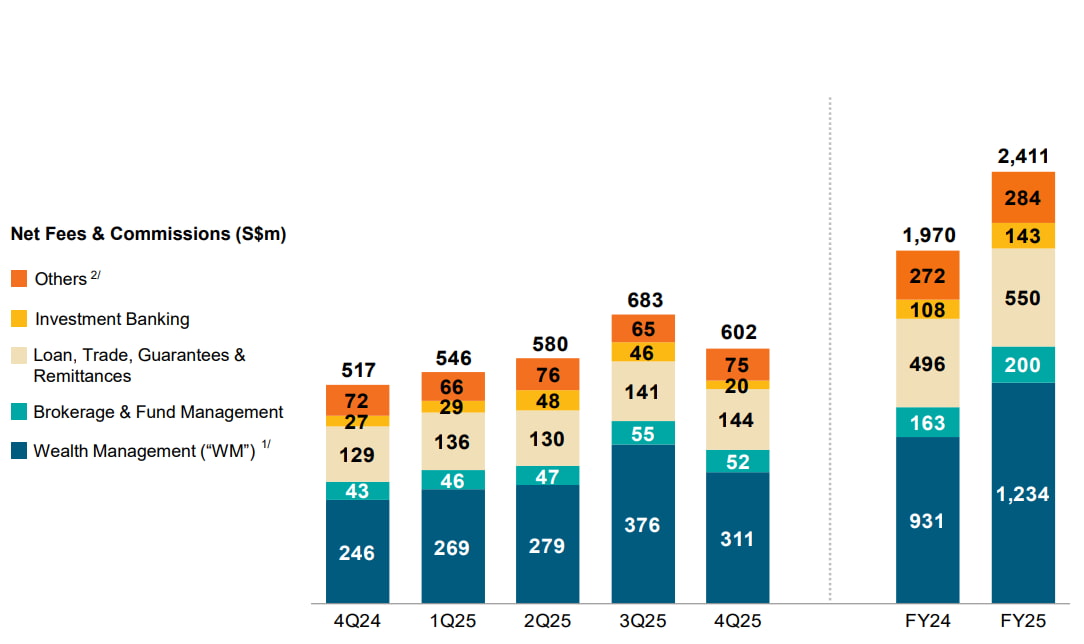

- Net fee income increased 16% to S$602 million (from S$517 million a year ago), mainly driven by a 26% rise in wealth management fees, alongside higher loan-related, brokerage, fund management and credit card fees.

- Net trading income rose 30% to S$395 million, boosted by stronger customer flow income from both the wealth and corporate segments.

- Insurance income more than doubled to S$226 million (from S$101 million a year ago), supported by better insurance and investment performance, and partly due to a negative adjustment related to changes in the medical insurance environment in the previous year.

OCBC's wealth management fee income grew to S$311 million in 4Q25 from S$246 million in 4Q24, though it declined quarter-on-quarter due to typical year-end seasonality.

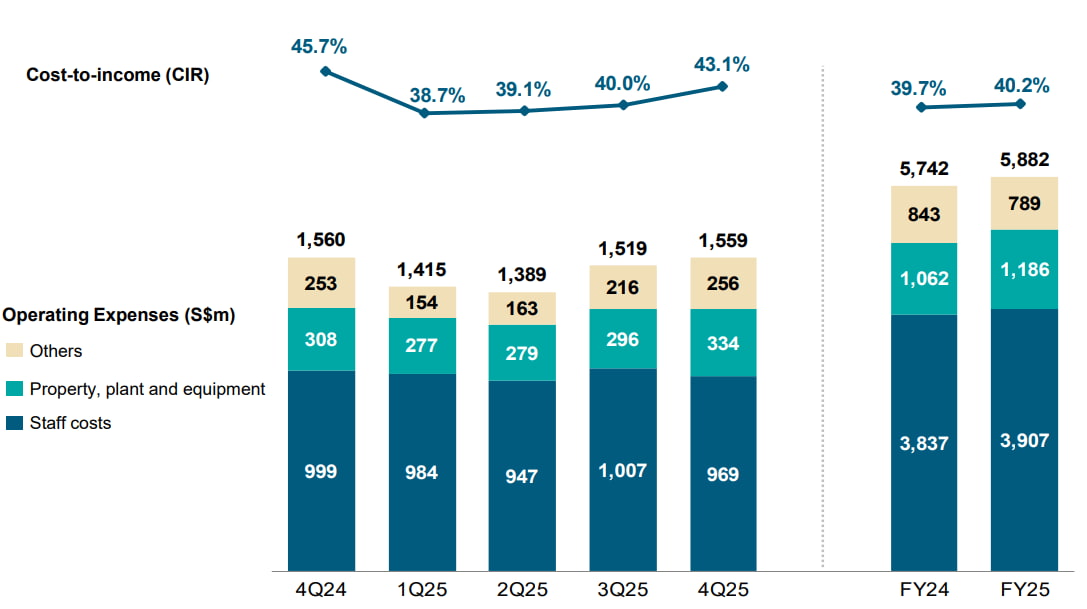

#3 - Lower cost-income ratio in 4Q25 compared to previous year

OCBC maintained cost discipline, with operating expenses broadly flat year-on-year at S$1.56 billion. As a result, the cost-to-income ratio (CIR) improved to 43.1%, from 45.7% a year earlier.

On a quarter-on-quarter basis, however, operating expenses rose 3%, mainly due to higher technology-related costs and professional fees, as OCBC continued to invest in strategic initiatives as part of its digitalisation journey.

Total allowances came in at S$200 million, down 4% year-on-year from S$208 million. Credit costs were 20 basis points (0.20%) of loans (annualised), compared with 21 basis points (0.21%) in 4Q24.

Compared with the previous quarter, total allowances were 44% higher, mainly due to higher allowances for impaired assets, partly offset by a net write-back of allowances for non-impaired assets.

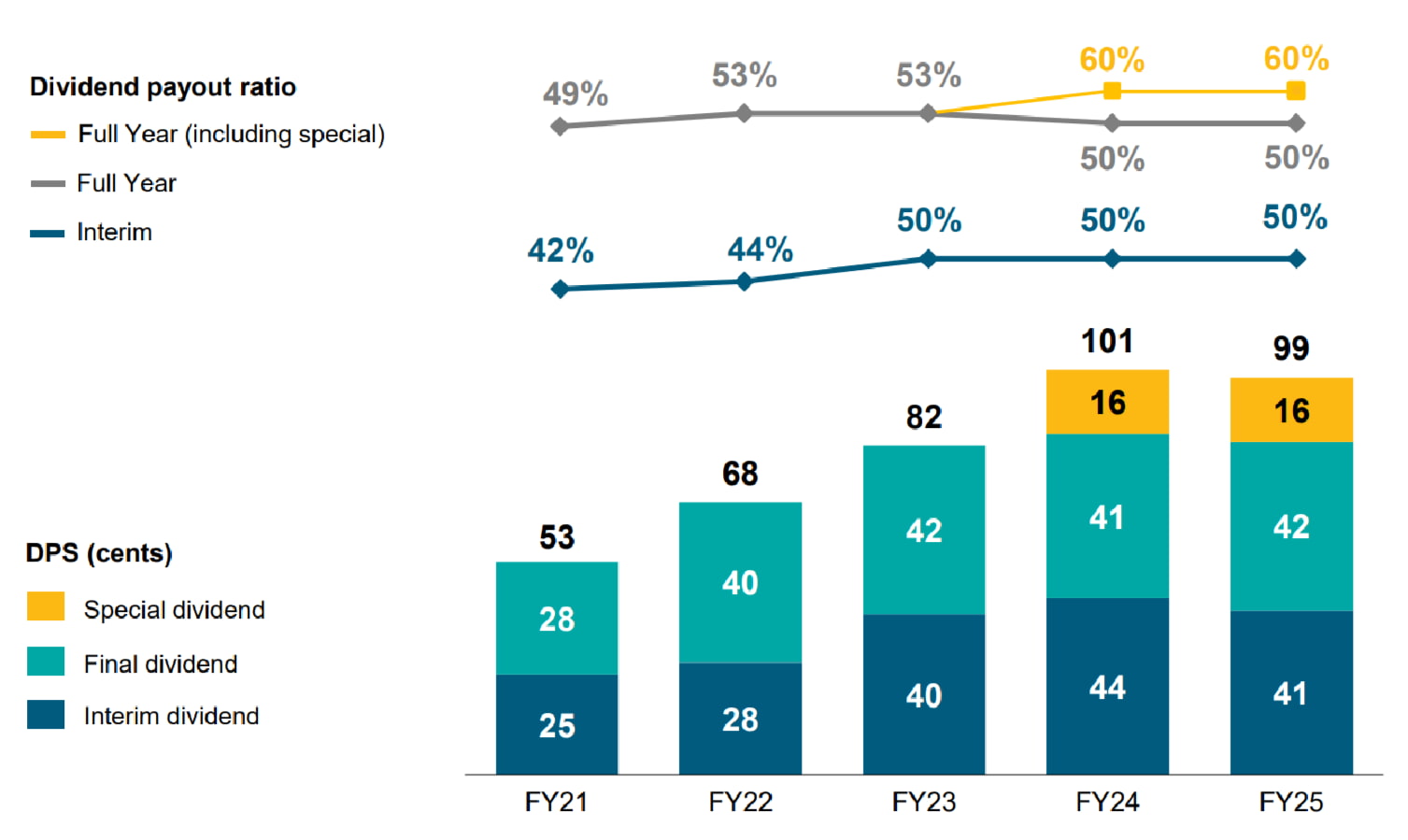

#4 - Final dividend of S$0.42 per share

The board has proposed a final ordinary dividend of 42 cents per share for FY25, slightly higher than 41 cents per share for FY24.

This would bring the total ordinary dividend for FY25 to 83 cents per share with a payout ratio of 50%.

A special dividend of 16 cents per share is recommended, raising the total dividend payout for FY25 to 60% of net profit.

The S$2.5 billion capital return plan is targeted to be completed by FY26.

Find out how much dividends you will potentially receive as a shareholder of OCBC with the calculator below. Note that this is based on latest average forecasts of analysts, which may not have included the special dividends announced.

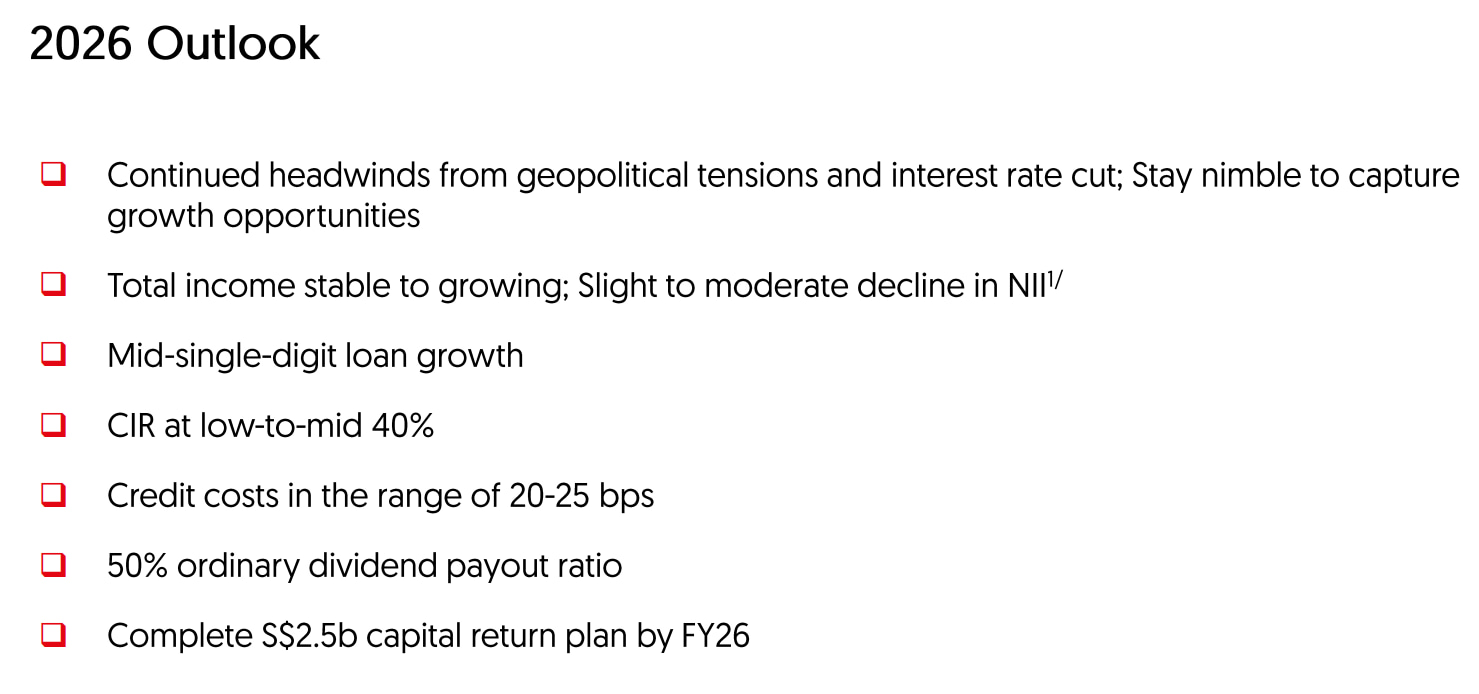

#5 - 2026 outlook

OCBC expects the operating environment in 2026 to remain challenging, with continued headwinds from geopolitical tensions and lower interest rates, while staying nimble to capture growth opportunities.

Management guided for total income to be stable to growing, although net interest income is expected to see a slight to moderate decline, assuming 3M SORA of ~1.4%, Fed Fund Rate of ~3.5% and 3M HIBOR of ~2.8%.

The bank is targeting mid-single-digit loan growth, while keeping its cost-to-income ratio (CIR) in the low-to-mid 40% range.

On asset quality, credit costs are expected to come in at 20–25 basis points.

OCBC also maintained its 50% ordinary dividend payout ratio and expects to complete its S$2.5 billion capital return plan by FY26.

Beansprout’s Quick Take on OCBC earnings

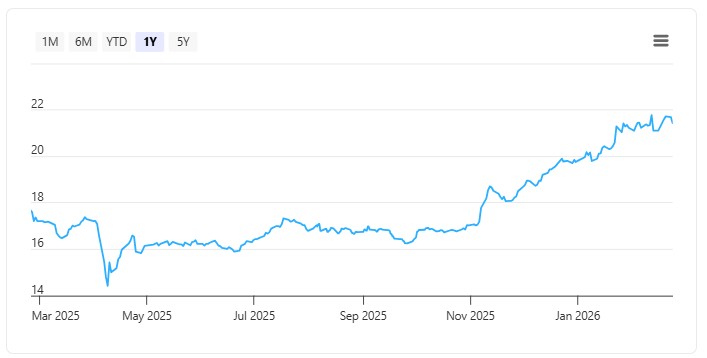

OCBC has seen the strongest share price performance year-to-date amongst the Singapore banks, with a gain of 8.5% versus UOB’s 6.1% and DBS’s 2.7%.

On the positive side, OCBC's results stand out as it the only Singapore bank to report a year-on-year profit increase in 4Q25. Its net profit rose 3% YoY to S$1.75 billion, supported by a quarter-on-quarter bounce in its net interest margin, and strong growth in non-interest income. This also exceeded consensus forecast of S$1.73 billion.

With the higher profit, OCBC also announced an increase in in its final ordinary DPS to S$0.42, as well as a special dividend of S$0.16. This would bring its total dividend per share in 2025 to S$0.99.

Looking ahead, OCBC expects a stable-to-growing total income in 2026.

On the flip side, we will be looking out for whether Singapore banks will continue to see further pressure on net interest margins in 2026.

OCBC has also guided for a 50% ordinary dividend payout ratio in 2026, compared to its 60% total dividend payout ratio in 2025. This may mean a potential decline in its total dividend payout in 2026 compared to 2025.

OCBC is currently trading at 1.66x price-to-book, above its historical average of about 0.94x.

| Bulls say | Bears say |

| 4Q25 net profit up 3% YoY to S$1.75b, beating consensus S$1.73b. | Net interest margin pressures remain a broader sector risk |

| Stronger non-interest income drove earnings | Guidance for 50% ordinary dividend payout ratio in 2026, vs 60% total dividend payout ratio in 2025 |

| Final DPS S$0.42 (up from S$0.41) + S$0.16 special dividend. | Price-to-book ratio of 1.66x above historical average valuation |

| Stable-to-growing total income expected in 2026 | |

For income investors, OCBC is expected to offer a total dividend per share of S$0.978 in 2026, according to consensus forecast. This would represent a potential dividend yield of 4.6% based on its closing price of S$21.43 on 25 February.

This would be lower than the dividend yield for DBS (including capital return dividend) and comparable to UOB’s dividend yield.

Read also: 3 Singapore blue chip stocks near all time highs. Are their yields attractive?

Related links:

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in OCBC.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments