3 Singapore blue chip stocks near all time highs. Are their yields attractive?

Stocks

By Gerald Wong, CFA • 24 Feb 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Here are three Singapore blue chip stocks trading near all time highs in February 2026. We find out if their dividend yields remain attractive after the rally in share prices.

What happened?

Singapore stocks have been pushing higher in early 2026.

The Straits Times Index has climbed to fresh records of above 5,000 points in recent weeks.

In January, the 3 best-performing Singapore blue chip stocks were companies in the property sector, including UOL, Hongkong Land and City Developments.

We have also seen other blue chip stocks reaching new all time highs, as sentiment towards Singapore stocks improve, and dividends continue to be raised.

This has led to questions in the Beansprout community about whether it is still worthwhile owning Singapore blue chip stocks for dividend income.

In this article, I will look at three Singapore blue chip stocks that are trading near all time highs in February 2026. I will also find out if their dividend yields remain attractive after the rally.

3 Singapore blue chip stocks near all time highs

#1 – Singtel (SGX: Z74)

Singtel is Singapore's largest telecommunications company and a leading communications technology group in Asia, with stakes in regional mobile operators including Bharti Airtel in India, Telkomsel in Indonesia, Globe Telecom in the Philippines, and AIS in Thailand.

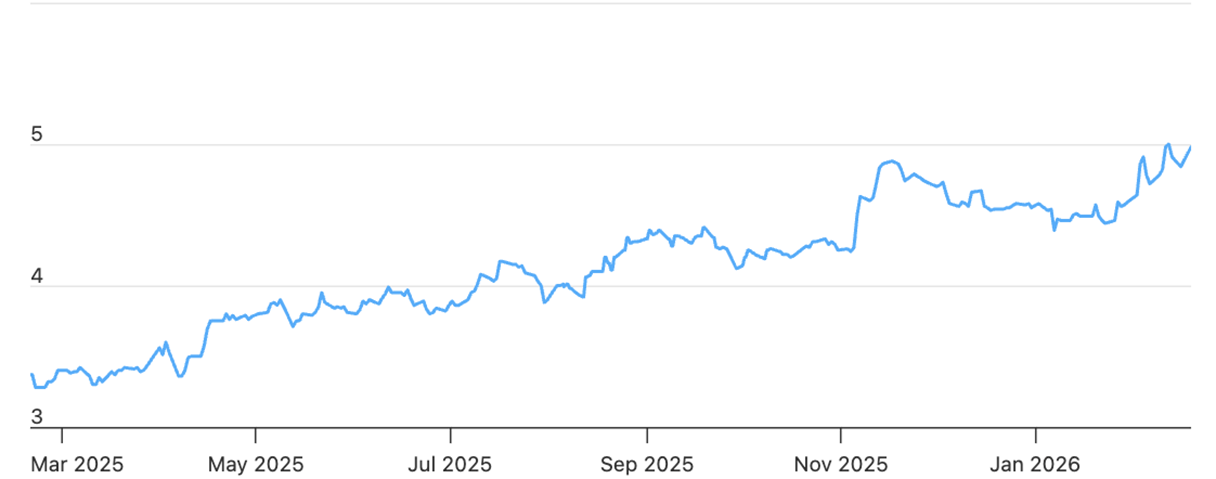

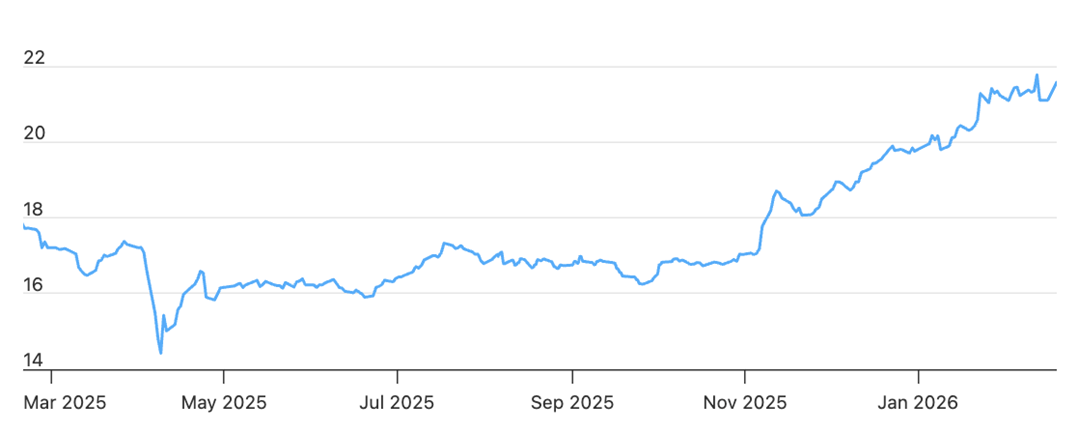

Singtel’s share price reached an all time high of S$5.10 before closing at S$5.04 on 20 February 2026.

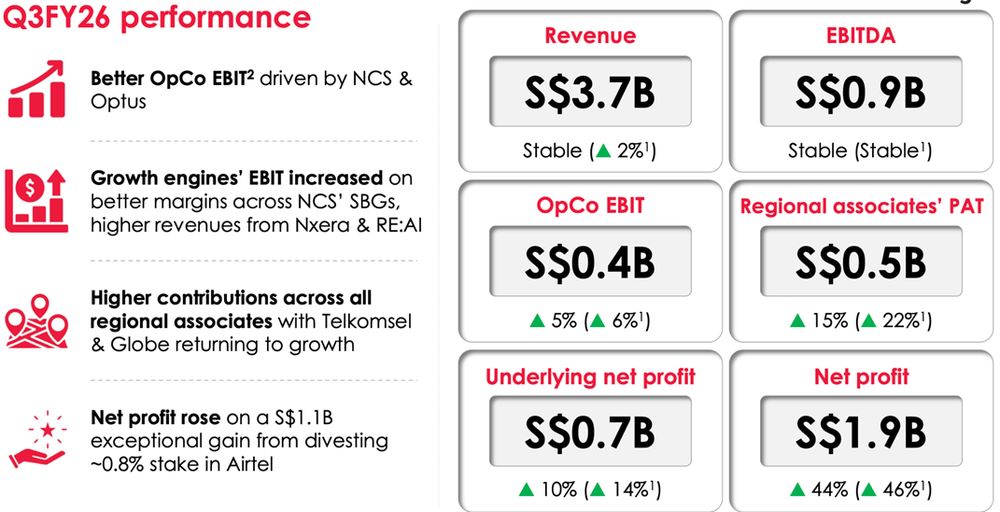

For the third quarter ended 31 December 2025, Singtel reported stable operating revenue of S$3.66 billion and stable EBITDA of S$939 million.

Operating company EBIT rose 5.3% to S$362 million, driven by stronger contributions from NCS and Optus, which helped offset weaker performance in Singtel Singapore.

Singtel’s underlying net profit increased 9.5% year on year to S$744 million, mainly due to stronger results from its regional associates led by Airtel and AIS.

Net profit rose more sharply to S$1.89 billion, as Singtel booked a net exceptional gain of S$1.15 billion. This was primarily from the sale of a partial stake in Airtel.

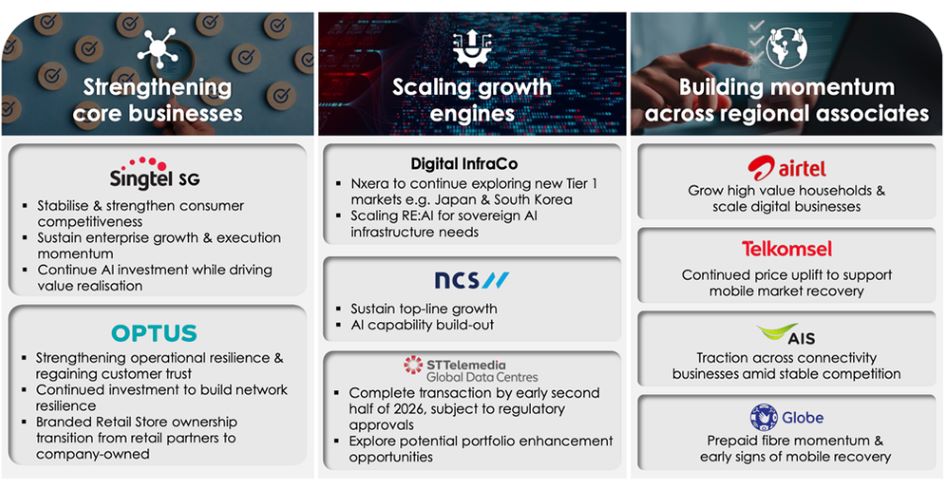

Singtel also highlighted continued progress in its growth engines.

NCS recorded stronger operating momentum, with revenue rising and profitability improving. Digital InfraCo continued to expand, supported by higher contributions from data centre services and its RE:AI business.

A key driver for the stock was Singtel's continued progress on its S$9 billion medium-term capital recycling target.

In November 2025, it sold a further 0.8% stake in Airtel for approximately S$1.5 billion, generating an estimated gain of S$1.1 billion. Its effective stake in Airtel fell to 27.3% after the transaction.

This transaction was part of Singtel’s broader medium-term asset recycling plan, and the company has already realised around S$5.6 billion since April 2024 toward its ~S$9 billion target.

Singtel also shared that Digital InfraCo secured 280MW of power commitment for a data centre in Johor, and that its Tuas data centre had more than 90% of capacity pre-sold, highlighting demand for AI-ready digital infrastructure.

In February 2026, Singtel announced a major transaction together with KKR, to take full control of data centre operator ST Telemedia Global Data Centres (STT GDC) in a deal that pegs STT GDC's enterprise value at S$13.8 billion.

Following completion, Singtel will hold a 25% stake in the enlarged entity.

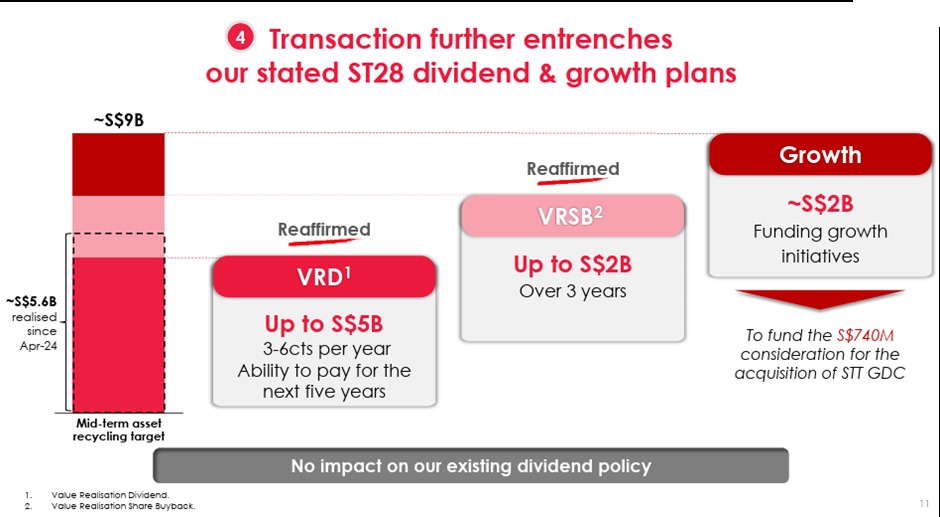

Management stated that there is no impact on its existing dividend policy from this acquisition, and reaffirmed its capital return and growth funding framework under Singtel28.

This includes a Value Realisation Dividend (VRD) of up to S$5 billion, which supports 3 to 6 cents per share per year and provides visibility for the next five years, as well as a Value Realisation Share Buyback (VRSB) of up to S$2 billion over three years.

Singtel also indicated that around S$2 billion is set aside for growth initiatives, including funding the S$740 million consideration for the STT GDC acquisition.

Singtel continues to return capital to shareholders through its dividend framework, supported by operating cash flows and capital recycling.

Based on Singtel’s share price of S$5.04 as of 20 February 2026, and a FY2026 dividend estimate of S$0.181 per share according to Factset, Singtel offers a forward dividend yield of approximately 3.6%.

Find out how much dividends you would have received as a shareholder of Singapore Telecommunication Limited (Singtel) in the past 12 months with the calculator below.

Related Links:

#2 – OCBC (SGX: O39)

OCBC is one of Singapore’s largest banks, offering a full range of consumer, corporate and wealth management services across the region.

OCBC’s share price has been trading near its recent highs, supported not just by resilient earnings, but also by confidence in OCBC’s longer-term strategy.

A key part of that strategy is its “One Group” approach — integrating the bank, Bank of Singapore, Great Eastern and Lion Global Investors more closely so it can deepen customer relationships across banking, wealth and insurance.

OCBC also continues to focus on growth areas such as wealth, digitalisation and higher-growth industries as part of its broader corporate strategy.

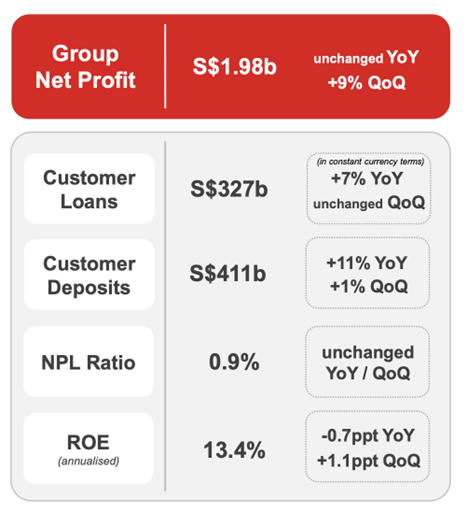

For 3Q 2025, OCBC reported net profit of S$1.98 billion, up 9% quarter-on-quarter, supported by a pickup in non-interest income which helped cushion the impact of lower net interest income in a softer rate environment.

Total income rose 7% quarter-on-quarter to S$3.80 billion, underpinned by record non-interest income.

Non-interest income increased 24% quarter-on-quarter to S$1.57 billion, led by stronger fee, trading and insurance income.

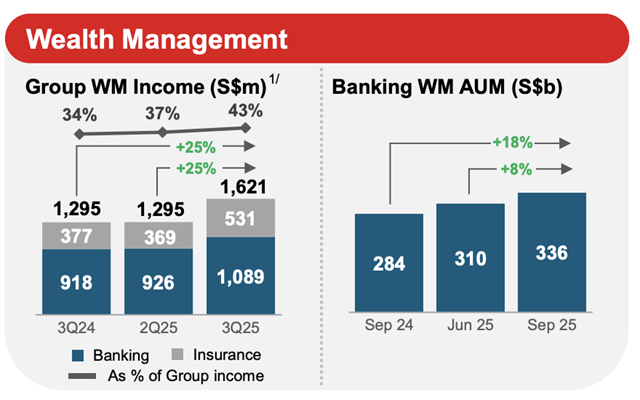

Wealth management was a key bright spot.

Wealth management income reached a record S$1.62 billion, up 25% quarter-on-quarter, and accounted for 43% of OCBC’s total income.

Banking wealth management assets under management rose 8% quarter-on-quarter to a record S$336 billion, supported by net new money inflows and positive market valuation.

This strength in wealth and insurance is also why investors are watching developments around Great Eastern.

Great Eastern remains a strategic pillar within OCBC’s wealth and insurance ecosystem, and management has consistently framed the insurer as important to the group’s integrated model.

In 2025, OCBC backed a voluntary exit offer for Great Eastern and later clarified that the offer was final, with no intention to launch another offer in the foreseeable future.

OCBC also said delisting Great Eastern remains a long-term strategic goal, while indicating it is comfortable with its current economic interest in the insurer.

OCBC’s asset quality remained sound. Its non-performing loan ratio stayed at 0.9%, marking the sixth consecutive quarter at this level.

Looking ahead, OCBC reiterated its 2025 targets, including net interest margin around 1.90%, and a 60% total dividend payout ratio and share buybacks, which reflects its focus on shareholder returns while continuing to invest for growth.

For dividends, OCBC’s interim dividend declared for 2025 was S$0.41 per share. According to consensus forecasts, OCBC is expected to pay a total dividend of S$0.99 per share in 2025.

Based on OCBC’s share price of S$21.72 as of 20 February 2026, this implies a potential dividend yield of about 4.6%.

Find out how much dividends you would have received as a shareholder of OCBC in the past 12 months with the calculator below.

Related links:

- OCBC reports 3% rise in net profit and higher final dividend: Our Quick Take

- Oversea-Chinese Banking Corporation Ltd share price history and share price target

- Oversea-Chinese Banking Corporation Ltd dividend history and dividend forecast

#3 – ST Engineering Ltd (SGX: S63)

ST Engineering is a global technology, defence and engineering group with businesses spanning Commercial Aerospace, Defence and Public Security, as well as Urban Solutions and Satcom.

ST Engineering’s share price has been supported by steady earnings growth and a strong order book that provides visibility for future revenue.

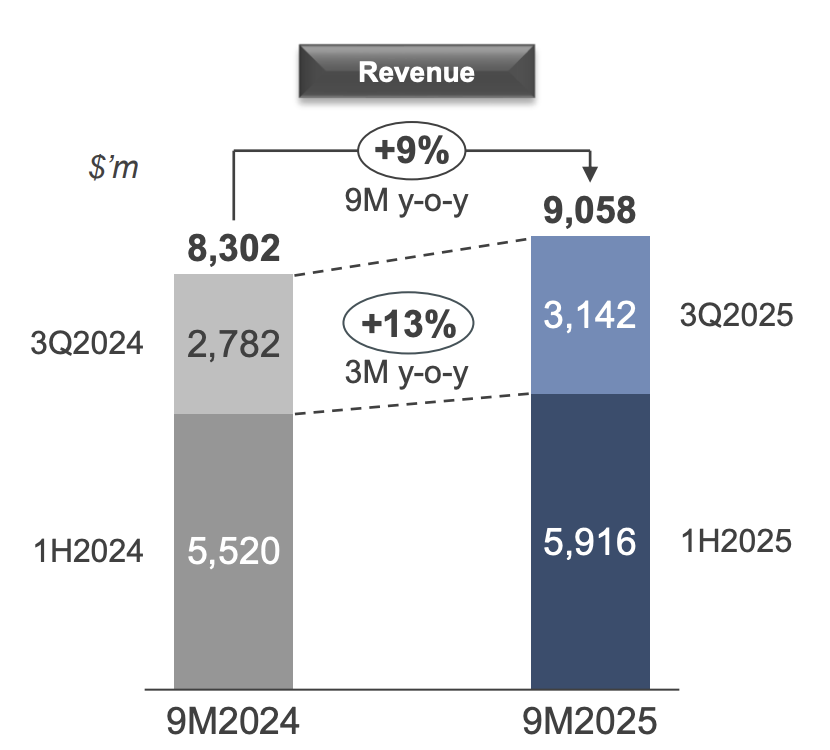

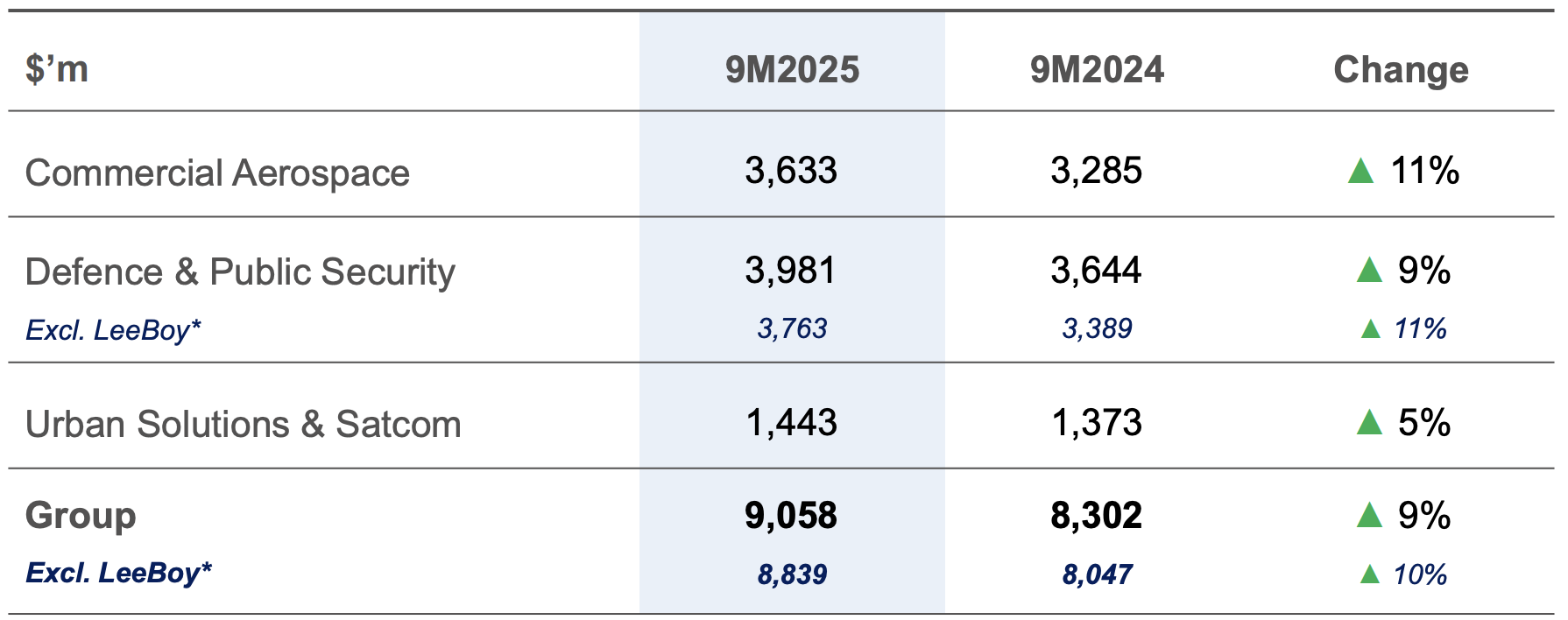

For the first 9 months of 2025 ended 30 September 2025, ST Engineering reported revenue of S$9.1 billion, up 9% year on year. Growth accelerated in the third quarter, with revenue rising 13% to S$3.1 billion.

Growth was broad based across segments.

Commercial Aerospace revenue rose 11% to S$3.6 billion, driven by strong engine MRO and nacelles performance.

Defence and Public Security revenue increased 9% to S$4.0 billion, supported by contributions from all sub segments.

Urban Solutions and Satcom revenue grew 5% to S$1.4 billion, driven by Urban Solutions, with growth picking up in the third quarter.

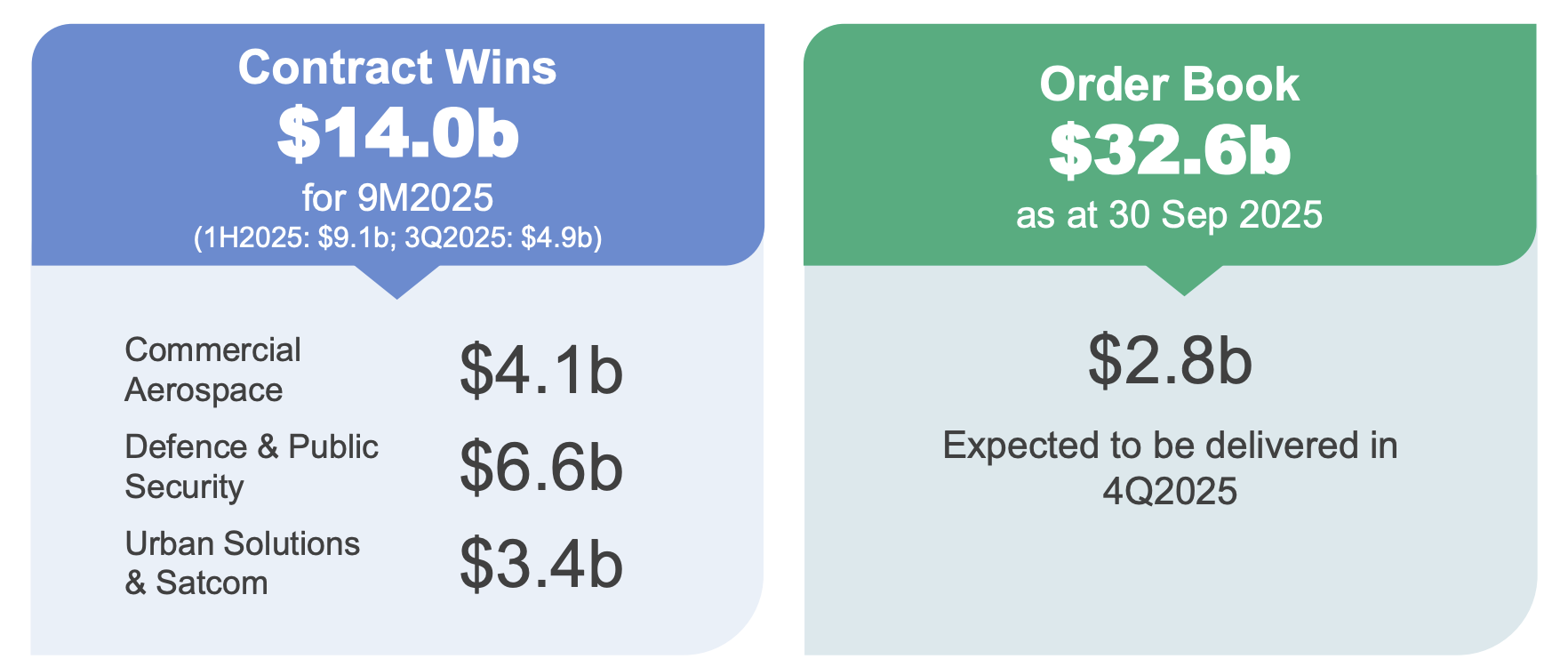

A key positive has been contract momentum.

ST Engineering secured S$14.0 billion of new contracts in the first nine months of 2025, including S$4.9 billion in the third quarter.

This lifted its order book to a record S$32.6 billion as at 30 September 2025. This supports earnings visibility as projects are delivered over time.

At the recent Singapore Airshow 2026, ST Engineering showcased a broad range of capabilities across aviation, defence, public safety and smart city solutions, underlining its positioning as a multi-domain engineering player.

Management highlighted new products launched at the airshow, including the DrN-600, a next-generation medium-lift cargo drone, alongside other aviation and defence technologies.

ST Engineering’s AirX joint venture also announced partnerships to commercialise the AirFish Voyager, a 10-passenger wing-in-ground craft for high-speed over-water transport, which adds another layer to its growth optionality beyond traditional aerospace MRO.

At the same time, the airshow also reinforced ST Engineering’s strength in its core aerospace franchise.

The group announced an integrated airframe and nacelle MRO service centre in Singapore, the first such integrated setup in its global network, aimed at improving turnaround times and efficiency for airline customers.

The group also continued portfolio rationalisation.

Management highlighted the planned divestments of LeeBoy and SPTel, which are expected to generate around S$450 million of net cash proceeds and an estimated one off divestment gain of around S$180 million, subject to regulatory approvals and completion.

For dividends, ST Engineering has committed to a total dividend of 23.0 cents per share for FY2025. This includes the quarterly interim dividends, a proposed final dividend, and a proposed special dividend announced in conjunction with its dividend policy.

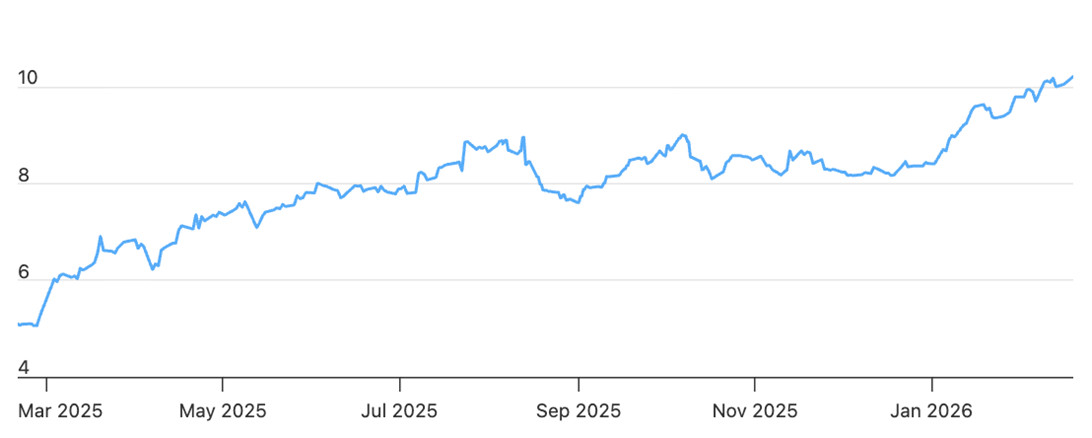

Based on ST Engineering’s share price of S$10.23 as of 20 February 2026, the FY2025 total dividend of 23.0 cents implies a dividend yield of approximately 2.3%.

Find out how much dividends you would have received as a shareholder of ST Engineering in the past 12 months with the calculator below.

Related links:

- ST Engineering share price history and share price target

- ST Engineering dividend history and dividend forecast

What would Beansprout do?

| Company | The Good | The Bad |

| Singtel | • Dividend supported by operating cash flows • Capital recycling unlocks balance sheet value • Buybacks and Value Realisation Dividend (VRD) reinforce shareholder returns | • Yield lower than OCBC • Competitive telco pressures in Singapore • Execution risks in digital infrastructure investments |

| OCBC | • Highest dividend yield among the three • Clear payout ratio plus share buybacks • Diversified earnings via One Group strategy | • Sensitive to falling net interest margins • Earnings pressured if rates fall faster • Price-to-book valuation near highs |

| ST Engineering | • Large order book supports earnings visibility • Strong aerospace MRO demand • Growth optionality in autonomous systems | • Lowest dividend yield at current prices • Price-to-book valuation stretched after rally • Dependent on project execution and margins |

Verdict: Singapore blue chip stocks remain a critical part of our portfolio as income anchors, even though dividend yields are less attractive after the recent rally. • OCBC currently offers yield + capital return combination | ||

Singtel, OCBC and ST Engineering have been trading near their all time highs in February 2026. This reflects improving sentiment and resilient business performance.

Following the rally in their share prices, OCBC now offers the highest potential dividend yield of 4.6%.

This is followed by Singtel which offers a potential dividend yield of 3.6%. ST Engineering offers the lowest dividend yield of 2.3%.

Apart from having the highest dividend yield, management of OCBC has also maintained a clear shareholder return framework with a 60% total payout ratio plus share buybacks.

On top of that, OCBC’s “One Group” strategy and its wealth and insurance ecosystem (including Great Eastern) provide additional support to earnings diversification.

The key thing to watch is whether net interest margins hold up as interest rates ease, since that can affect future profit growth and dividend capacity.

Singtel's dividend is supported by its operating cash flows, as well as its capital recycling programme and value realisation framework.

Importantly, management has reiterated that the STT GDC transaction does not affect its existing dividend policy, while reaffirming its VRD and share buyback plans under Singtel28.

This gives investors some confidence that Singtel is trying to fund growth in digital infrastructure while continuing to return capital to shareholders.

ST Engineering offers the lowest headline yield at current prices among the three, but has a large order book that supports earnings visibility, and its recent Singapore Airshow announcements highlighted both continued strength in core aerospace MRO and optionality in newer areas such as autonomous systems and next-generation mobility.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, S$1,380 CapitaVouchers to be won in our exclusive Huat Together Lucky Draw. Promo ends on 28 February 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Check out the best stock trading platforms in Singapore with the latest promotions to invest in Singapore blue chip stocks.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments