With residential prices rising, are property stocks still a good buy?

Stocks

By Gerald Wong, CFA • 29 Nov 2025

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

With residential prices continuing to rise, we examine whether it is worthwhile investing in Singapore property stocks.

What happened?

Recently, I spoke at a seminar on “Property vs stocks - What is more attractive?”.

One of the questions that was asked as the panel was whether the Singapore property sector is in a bubble, and if it is still worthwhile buying property stocks.

Recently, we have seen Singapore stocks rallying, with several blue chip stocks reaching new all-time highs.

Singapore property stocks have also rebounded strongly from the lows, supported by improving sentiment with a pickup in sales volumes.

In this article, I will look at the latest trends in the residential property market, and find out if property stocks still look attractive on valuation.

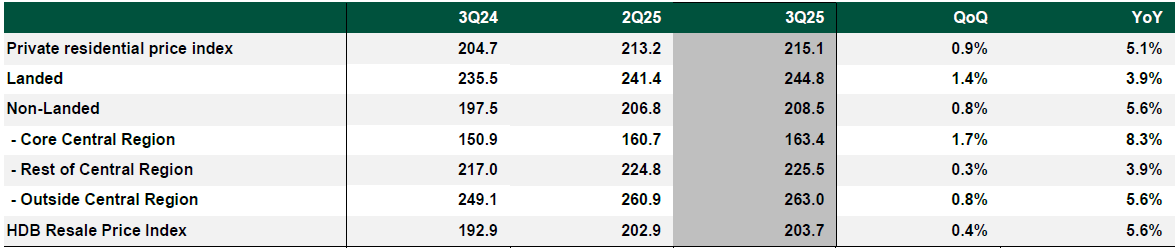

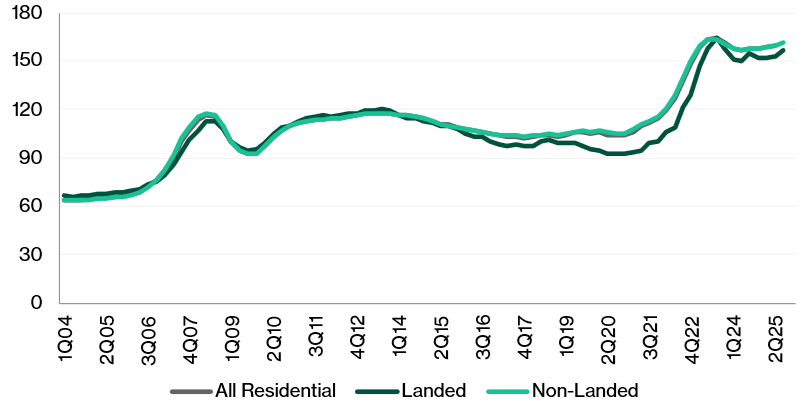

Private residential prices were up 0.9% in 3rd quarter 2025

Private residential prices were up 0.9% quarter-on-quarter in third quarter of 2025, marginally lower than the 1.0% quarter-on-quarter increase in 2Q25.

On a year-on-year basis, private residential prices increased 5.1% in 3Q25, above that of estimated headline inflation rate of 0.62% year-on-year in 3Q25.

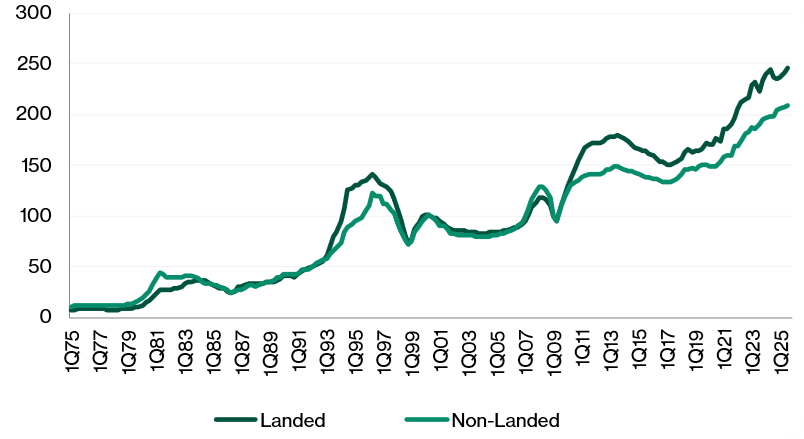

This quarter’s private residential price increases continued to be led landed properties which rose 1.4% quarter-on-quarter in 3Q25.

Non-landed properties reported price increased by 0.8% quarter-on-quarter in 3Q25.

Year-to-date, private home prices have increased by 2.7% for the period 9M 2025.

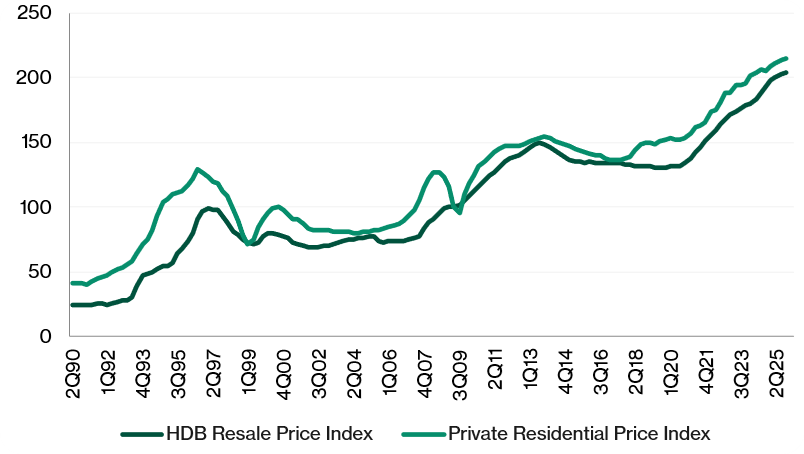

The sequential increase in HDB resale prices continued to ease, with 3Q25 prices up 0.4% quarter-on-quarter, the smallest quarterly price increase since 2Q20.

HDB resale prices have stabilised but there are more million-dollar resale transactions.

In 3Q 2025, there were 480 resale transactions of more than S$1.0 million, compared to 415 of such transactions in 2Q 2025.

On a year-on-year basis, HDB resale prices have continued to outpace that of private residential prices, with a 5.6% year-on-year increase.

Year-to-date, HDB resale prices have risen by 2.9% in 9M 2025.

HDB resale volume was 7,221 in 3Q25, +1.7% quarter-on-quarter and -11.3% year-on-year.

The year-on-year slowdown in HDB resale transactions could be due to the steady supply of attractively located built-to-order flats.

In October 2025, HDB launched the final Build-To-Order (BTO) sales exercise for the year, offering 9,144 flats across ten projects in Ang Mo Kio, Bedok, Bishan, Bukit Merah, Jurong East, Sengkang, Toa Payoh and Yishun.

This includes HDB’s fifth Community Care Apartment (CCA) project in Sengkang.

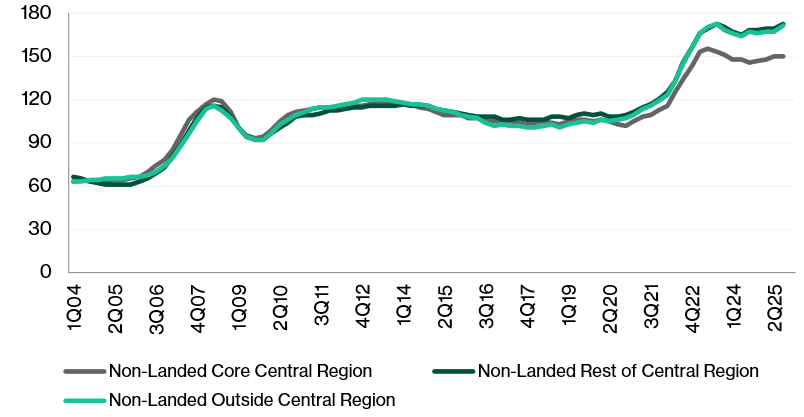

Robust price increases across the segments

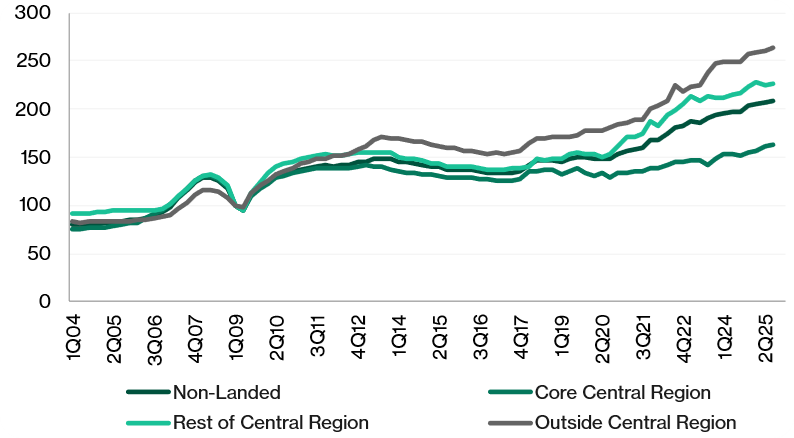

Despite the record high launches in the city region, prices of non-landed properties in the Core Central Region (CCR) continued to climb steadily, increased by 1.7% quarter-on-quarter in 3Q25, compared to +3.0% quarter-on-quarter in 2Q25.

In the Rest of Central Region (RCR), and Outside Central Region (OCR) segments, price increases at a more measured pace, +0.3% quarter-on-quarter and +0.8% quarter-on-quarter, respectively.

The moderation in the RCR was likely due to pricing at new launches like Lyndenwoods (336 units sold at a median price of $2,462 psf).

On the other hand, volume and prices in CCR were driven by three key projects which sold total of 835 units – Robertson Opus (171 units sold at $3,356), Upperhouse at Orchard Boulevard (202 units sold at $3,304) and River Green (465 units sold at $3,120).

CCR recorded overall new home sales of 903 units in 3Q 2025, the highest quarterly CCR sales since 4Q 2010.

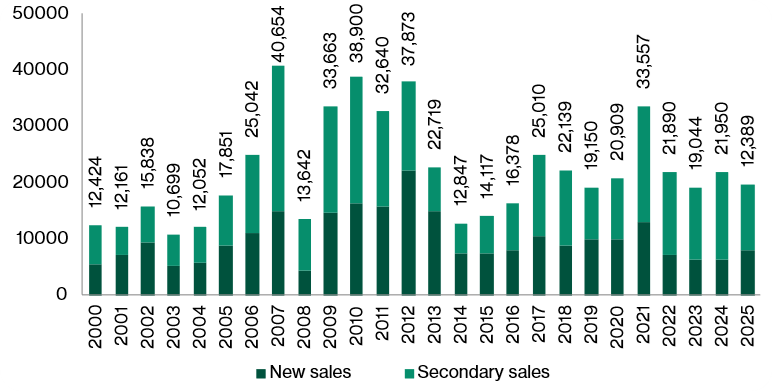

Year-to-date till end-September 2025, developers’ new homes sales totalled 7,875 units, surpassing full year 2024 new home sales of 6,469 units.

We believe the strong momentum in new homes sales to continue in 4Q 2025. In October, 2,424 new private homes were sold, making this the strongest monthly sales since 2024.

The stellar performance was led by four new projects launched in October – Skye at Holland, Faber Residence, Penrith and Zyon Grand. The four projects achieved take up rate of between 84% to 99% during the launch.

For the full year 2025, new private residential sales will likely surpass 11,000 units, up from the initial consensus forecast of 10,000 units.

Strong growth in transaction volumes

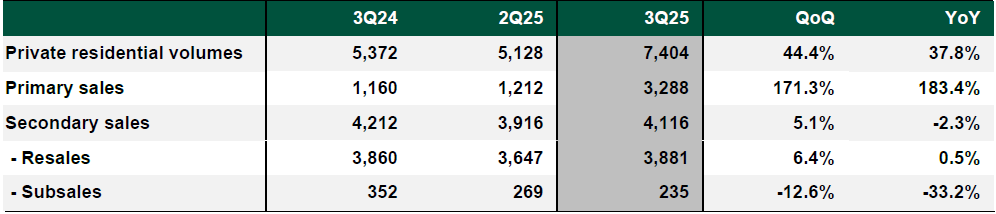

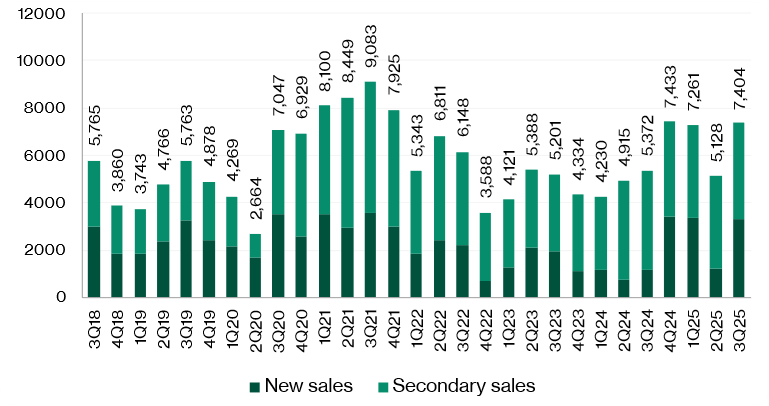

Overall private residential volumes surged 38% year-on-year to 7,404 units for 3Q25, or +44% quarter-on-quarter. 3Q25 volume was a strong recovery from a weak 2Q25 which recorded overall private residential volumes of 5,128.

Primary sales activity was robust with volume increased by 171% quarter-on-quarter and 183% year-on-year. In 3Q25, eight projects were launched with total 4,191 units, compared with 1,520 units launched in 2Q2025.

As a result, secondary sales continued to fall year-on-year, to 4,116 units—extending the downtrend since 3Q24 as buyers increasingly favoured the attractive locations of new launches.

Lower mortgage rates boost demand

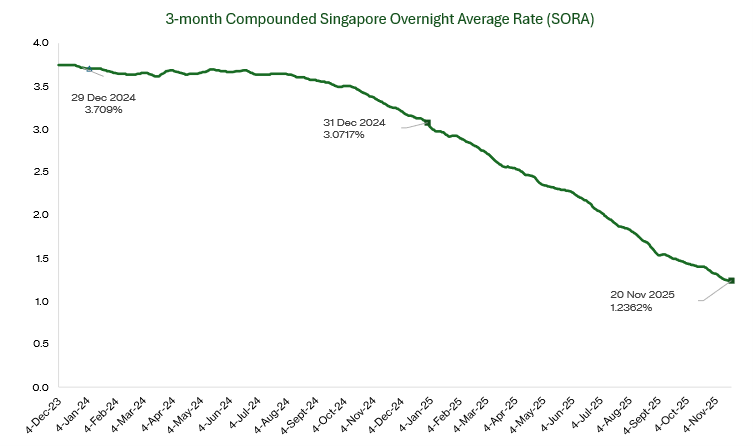

SGD interest rates continue to slide in tandem with the U.S. Fed’s rate cut actions. U.S. Fed cut interest rate by 25 basis points in October.

Year-to-date, U.S. Fed has lowered interest rate by 50 basis points.

The 3-month compounded SORA, the key benchmark for floating-rate mortgages in Singapore, has fallen by about 180 basis points in 2025. That drop has pulled mortgage rates lower and improved affordability for borrowers.

New launches in 3Q25 reported healthy take-up rates, including Wing Tai’s River Green (89%), CapitaLand’s LyndenWoods (98%) and GuocoLand’s Springleaf Residence (94%).

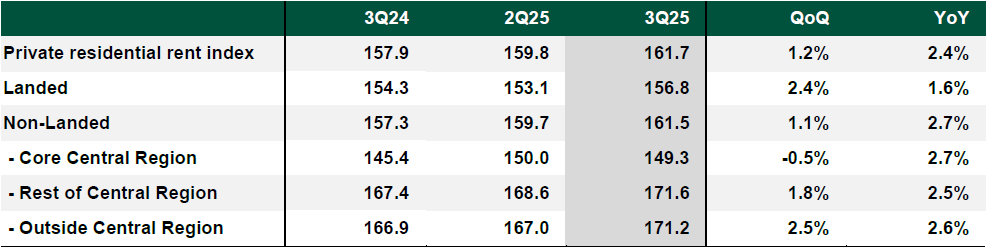

Rental rates outside central core region remains firm

Private residential rents increased in 3Q25, with the overall rent index rising 1.2% quarter-on-quarter and 2.4% year-on-year to 161.7.

Non-landed rents grew 1.1% quarter-on-quarter and 2.7% year-on-year, supported by a 2.5% quarter-on-quarter and 2.6% year-on-year in the OCR.

In contrast, the CCR saw a decline of 0.5% quarter-on-quarter, the only segment to record negative growth from previous quarter.

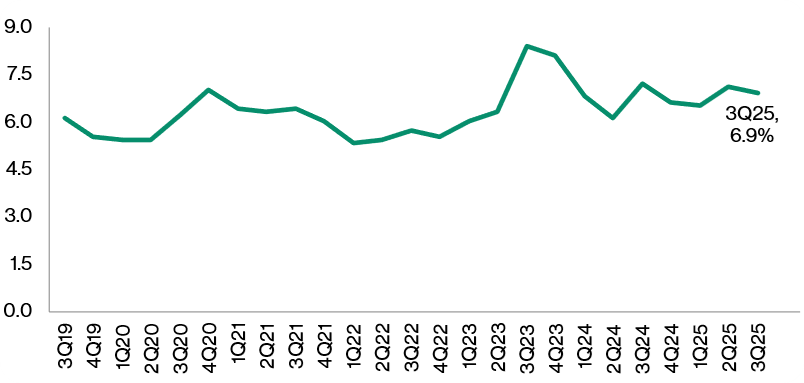

Vacancy rate marginally lower

Private residential vacancy rate edged down by 0.2 percentage points (pp) to 6.9% in 3Q25, extending the decline from 7.1% in 2Q25.

Vacancy levels are now broadly in line with the historical average of 6.3%, after peaking at 8.4% in 3Q23.

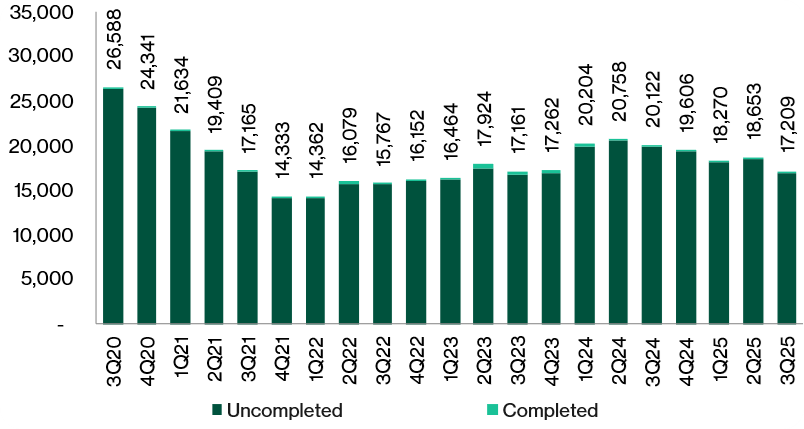

Given the pick-up in primary sales momentum, albeit with additional new supply coming onstream, the overall number of unsold private residential units continued to slide, down to 17,209 units, a 7.7% quarter-on-quarter decrease in 3Q25 from 18,653 units in 2Q25.

In 3Q25, 1,776 units were completed, bringing total supply completed in 9M 2025 to 4,105 units.

For 2025, 5,846 units are expected to be completed which marks a significant 31% decrease from the total of 8,460 units completed in 2024. For 2026, the projected units of completion is 7,810 units.

The Government is keeping private housing supply elevated under the Government Land Sales (GLS) programme, with close to 10,000 Confirmed List units in 2025 — about 50 percent above the average annual supply from 2021 to 2023.

It also signalled that it will keep tracking economic and property market conditions to ensure there is sufficient private housing and commercial space to meet the needs of the population.

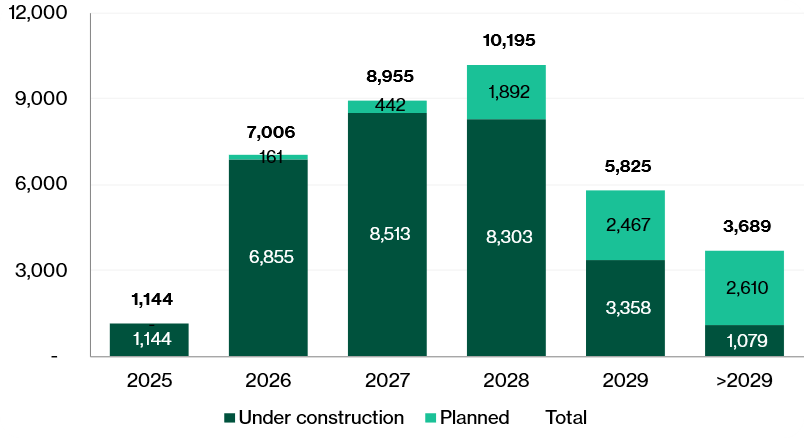

As of end-3Q 2025, there are a total supply of 36,814 private residential units (excluding Executive condominiums) in the pipeline, of which 17,029 units remained unsold.

Based on the expected completion dates, about 27,300 units are expected to be completed by 2029.

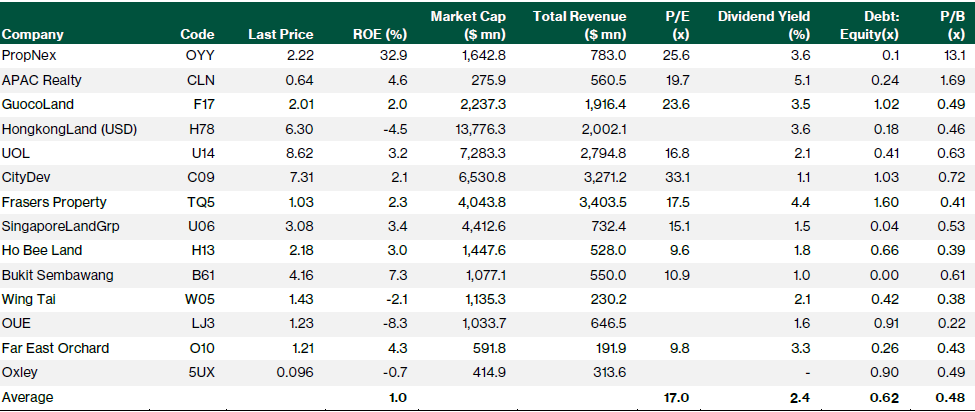

Singapore listed developers trade at average price-to-book ratio of 0.48x

We believe the listed real estate brokers represent the most direct proxies to the resilient residential market, with earnings directly leveraged to robust residential volume growth.

Despite a strong share price re-rating of more than 100% YTD, PropNex and APAC Realty (both Neutral rated) offer dividend yields of 3.6% and 5.1%, respectively.

In addition, the Singapore real estate developers trade at deep discounts to NAV amid a broad-based re-rating in the Singapore market.

Singapore-listed property developers currently trade at an average price-to-book (P/B) ratio of 0.48x, reflecting the relatively low returns they are generating.

At the same time, many have diversified geographically and shifted focus away from the local property market and residential developments.

Among them, GuocoLand has significant exposure to the Singapore residential market, concentrating on premium developments.

The company also generates recurring income through its investment properties. Its stock trades at a P/B ratio of 0.49x, in line with the sector average.

If you are interested in Singapore REITs, check out our analysis on whether Singapore REITs are more attractive with interest rates falling.

Download the full report here.

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in Singapore property stocks in Singapore.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments