United Hampshire US REIT: Defensive yield from America’s everyday essentials

REITs

By Goh Lay Peng • 30 Jun 2026

Global Wealth Technology Pte. Ltd. is regulated by the Monetary Authority of Singapore (MAS) as a licensed Financial Adviser.

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

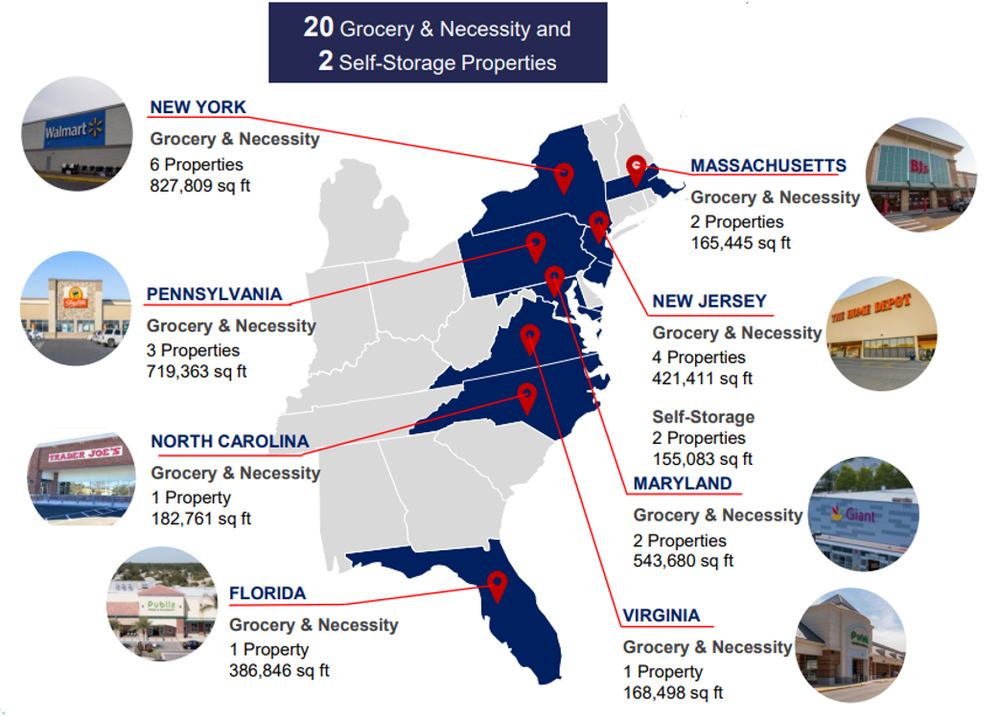

United Hampshire US REIT (UHREIT) invests in a diversified portfolio of stabilised, income-generating U.S. grocery-anchored and necessity-based retail assets, complemented by modern climate-controlled self-storage facilities. As at 31 Dec 2025, United Hampshire US REIT owns a portfolio of 20 Grocery & Necessity and two Self-Storage properties, with a total appraised value of US$774.3 million.

Defensive yield from America’s everyday essentials

About United Hampshire US REIT

Listed on the Singapore Exchange on 12 March 2020, United Hampshire US REIT (UHREIT) invests in a diversified portfolio of stabilised, income-generating U.S. grocery-anchored and necessity-based retail assets, complemented by modern climate-controlled self-storage facilities. As of 2 Jun 2026, the market capitalisation was S$0.32 billion.

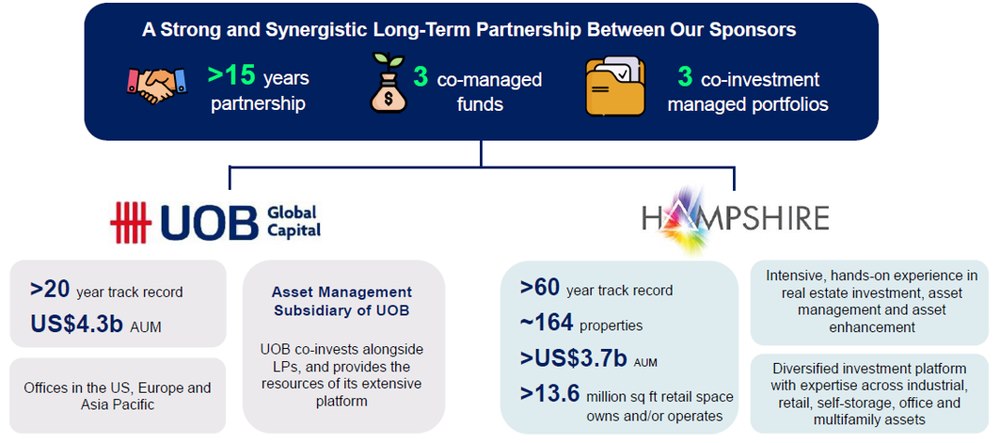

The two key shareholders are United Overseas Bank Limited (UOB, U11.SI) and The Hampshire Generation Fund LLC, who own shareholdings of 8.23% and 7.33%, respectively.

United Hampshire US REIT is jointly sponsored and managed by UOB Global Capital LLC, a wholly owned subsidiary of UOB, and The Hampshire Companies LLC. The REIT Manager is equally owned (50:50) by the two sponsors. The two sponsors are invested across three U.S. real estate funds with a combined AUM of US$1.3 billion, providing a healthy pipeline of assets.

Portfolio

United Hampshire US REIT owns a portfolio of 20 Grocery & Necessity and two Self-Storage properties, with a total appraised value of US$774.3 million and aggregate net lettable area (NLA) of 3.6 million square feet. The portfolio consists 22 properties valued at about US$774.3 million as at 31 December 2025.

Following the acquisition of Wallingford Fair Shopping Centre in January 2026, the portfolio expanded to 23 assets.

Strategy

United Hampshire US REIT’s investment mandate is focused on U.S. grocery-anchored and necessity-based retail properties, with selective exposure to the self-storage sector. The REIT targets tenant resilient to the e-commerce threat: grocers and wholesalers, home improvement stores, fitness centres, pharmacies, convenience stores, and off-price retailers operating strong omnichannel platforms.

The REIT’s strategy has three pillars:

(i) stable organic income through high-quality triple-net leases with built-in escalations;

(ii) inorganic growth via yield-accretive acquisitions in the grocery & necessity segment where cap rates remain at approximately 7.5%; and

(iii) disciplined capital recycling, selling mature or non-core assets at or above valuation and redeploying proceeds into higher-return opportunities.

In 2025, United Hampshire US REIT divested Albany Supermarket for US$23.8 million, representing a 4.2% premium to its purchase price. It then successfully recycled capital into higher-yielding assets. It completed two yield-accretive acquisitions - Dover Marketplace in Pennsylvania in August 2025 for US$16.4 million, at a 4.8% discount to its independent valuation, and Wallingford Fair Shopping Center in January 2026 for US$21.4 million, at an 8.2% discount to its independent valuation.

Reputable sponsors with sizeable inventory of assets

UOB Global Capital LLC is founded in 1998, it manages US$4.3 billion in AUM as at 31 December 2025, with offices in New York, Paris, and Singapore. UOB Global Capital LLC is the global asset management subsidiary of United Overseas Bank. UOB is listed on the Singapore Exchange, with market capitalisation of around S$64 billion.

The Hampshire Companies LLC (THC) is a privately held, fully integrated U.S. real estate firm with over 60 years of operating experience across acquisition, development, leasing, repositioning, and management of real estate. THC owns and/or operates approximately 164 properties totalling 13.6 million square feet across the U.S., with AUM of approximately US$2.9 billion. THC serves as the U.S. Asset Manager for UHREIT, bringing on-the-ground operational expertise and deep market relationships across the East Coast.

Portfolio performance

Est. 2020, United Hampshire US REIT owns 23 assets – 21 in Grocery & necessity retail and two in Self-storage. This includes an acquisition in Jan 2026 when it acquired Wallingford Fair at Connecticut, at US$21.4 million.

The portfolio comprises 97.9% freehold properties, based on appraised value of investment properties as at 31 December 2025.

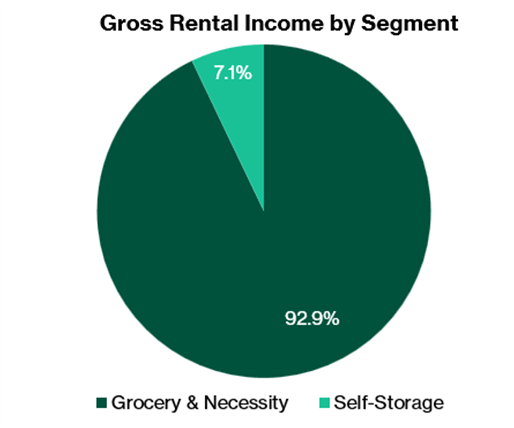

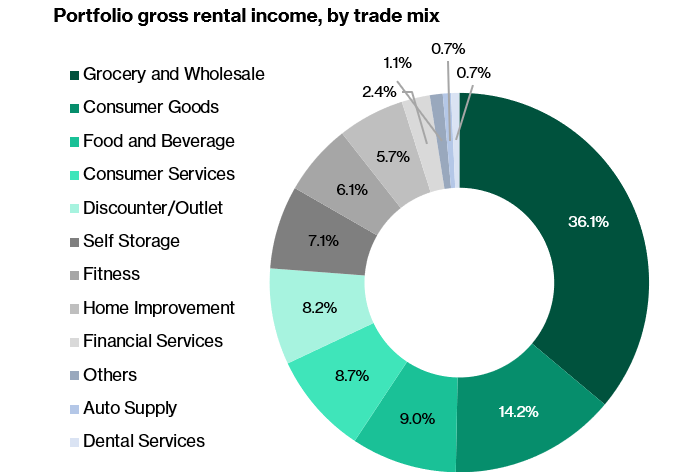

Grocery & necessity retail is the main income contributor, around 95%. Self-storage accounts for around 5%. As of 31 December 2025, the portfolio is valued at US$774.3 million.

Resilience in grocery and necessity retail

The U.S. grocery-anchored retail segment remains resilient, supported by the non-discretionary nature of grocery spending. Although retail sales growth moderated towards the end of 2025, both retail and grocery sales remained positive, demonstrating consumers' continued spending on essential goods despite inflationary pressures and economic uncertainty.

This resilience is reflected in the healthy sales performance of major tenants such as Walmart, Publix and BJ's Wholesale Club. They reported positive comparable sales growth. Strong tenant fundamentals continue to support stable occupancy, recurring rental income and favourable leasing demand for grocery-anchored retail assets.

Anchor tenants are financially resilient retailers

The portfolio’s anchor tenants are among the largest and most financially resilient retailers in the United States. BJ’s Wholesale Club Holdings (10.7% of income), Ahold Delhaize / Stop & Shop (8.4%), and Wakefern Food Corporation / ShopRite (8.3%) collectively represent the three largest warehouse club, supermarket cooperative, and supermarket group operators in the Northeast U.S. Their combined WALE exceeds 9 years.

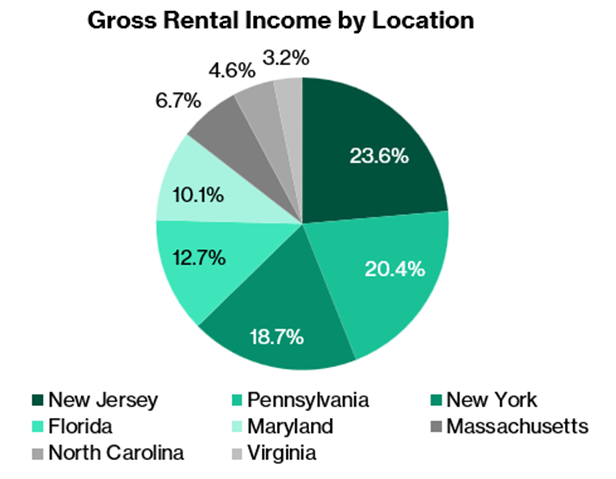

United Hampshire US REIT’s 23-asset portfolio is geographically concentrated along the U.S. East Coast, spanning eight states: New York, New Jersey, Maryland, Massachusetts, North Carolina, Florida, Virginia, and Pennsylvania.

This regional concentration is a deliberate strategy that enables the Manager to capitalise on the Hampshire sponsor's extensive local market knowledge and strong property management network.

St. Lucie West in Florida is United Hampshire US REIT’s single largest asset at US$101.0 million (13.1% of portfolio by value), a 381,648 sq ft community power centre anchored by Burlington Stores, LA Fitness, and Publix Super Markets.

Upland Square in Pennsylvania (US$91.5 million, 11.8% of portfolio) and Penrose Plaza (US$56.2 million) represent the REIT’s newest and largest market entries, providing significant geographic diversification into the Greater Philadelphia market.

Triple-net leases and built-in escalations protect the profit margins

All leases are triple-net (NNN), including the car parks. Tenants bear their pro-rata share of property taxes, insurance, property expenses, and common area maintenance.

This structure limits its operational responsibilities to carpark and common area maintenance — both with minimal utility costs and generally reimbursable by tenants.

Most leases include built-in rental escalations of 1–3% per annum for inline tenants and 5–10% every five years for anchor tenants, providing embedded organic income growth.

In the current environment of elevated oil prices and fuel shortages, this leasing clause protects its profit margins during the leasing period.

High occupancy

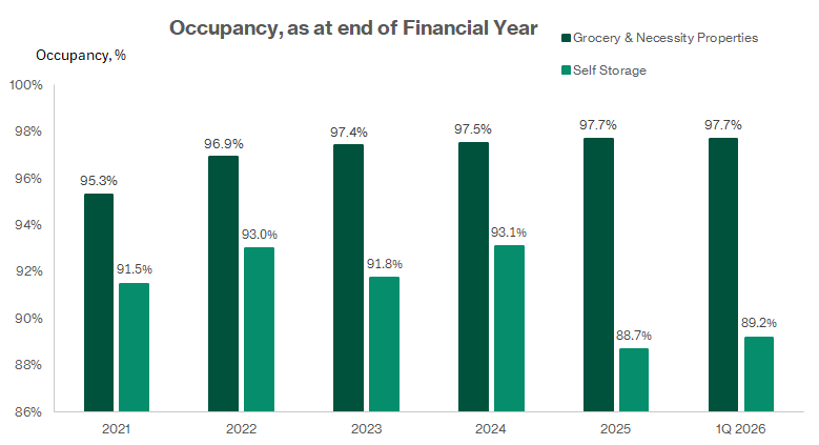

Grocery & Necessity portfolio has maintained committed occupancy above 94.7% in every reporting period since its March 2020 listing. As at 31 March 2026, grocery & necessity occupancy was 97.7%.

This exceptional track record through COVID lockdowns, inflation, and a significant interest rate cycle reflects both the essential nature of the portfolio’s tenants and the structural strength of open-air strip centre formats.

Income visibility from long-dated tenant leases

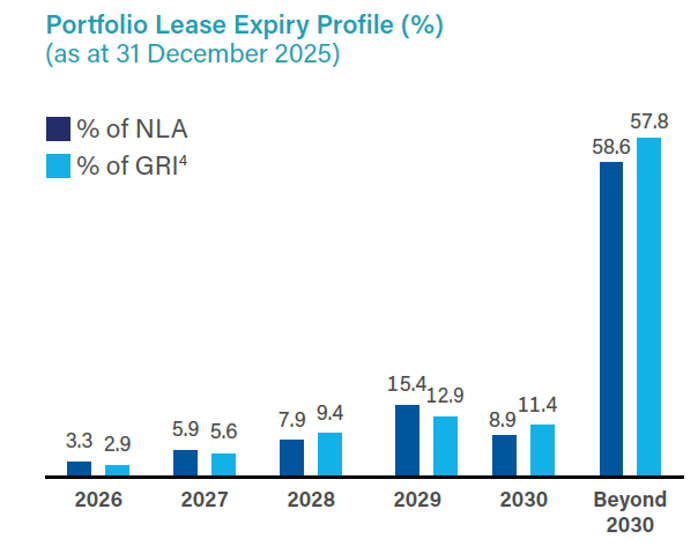

The portfolio provides strong income visibility, underpinned by long-dated leases. As at 31 March 2026, the portfolio is supported by long weighted average lease expiry (WALE) of 8.0 year. Such long dated leases provides visibility to cashflow and thus distribution income.

As at 31 March 2026, the top 10 tenants had a WALE of 10.6 years by gross rental income, supporting the portfolio's long-term income stability.

Extended weight average lease expiry

United Hampshire US REIT benefits from a highly defensive lease profile, with a portfolio WALE of 8.0 years as at 31 March 2026 and a top-10 tenant WALE of 10.6 years based on gross rental income.

As at 31 December 2025, lease expiries are well staggered, with only 2.9% and 5.9% of leases due for renewal in 2026 and 2027, respectively. Coupled with a consistently strong tenant retention rate of 90% since listing, these metrics provide good earnings visibility and support the resilience of the REIT's income stream.

Leasing risk is minimal. As at 4Q2025, less than 10% of leases by rental income were due for renewal through 2027.

In FY2025, tenant retention rate was 90% and it executed 30 new and renewal leases totalling 422,032 sq ft in FY2025, attracting tenants including Walmart, HomeGoods, Dollar Tree, M&T Bank, and CAVA.

Asset enhancement works

At St. Lucie West, construction is underway for a new 5,000 sq ft standalone store on excess land, which has been pre-leased to Florida Blue under a 10-year lease. This builds on the successful redevelopment completed in 2023, when a 63,000 sq ft store was developed for Academy Sports + Outdoors and secured on a 15-year lease.

These initiatives demonstrate the manager's ability to unlock value from existing assets while enhancing long-term income visibility.

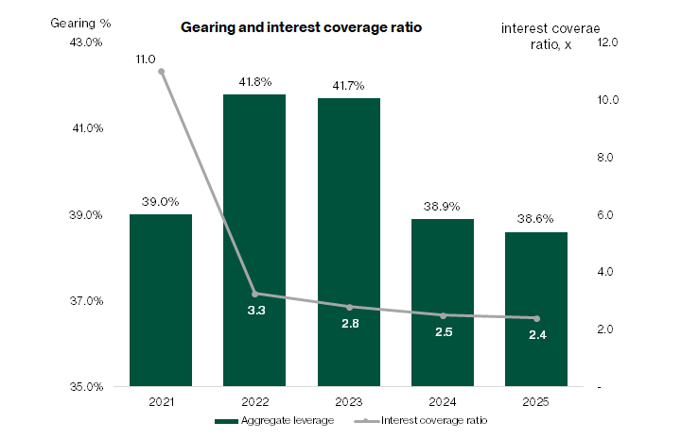

Capital Management

As at 31 March 2026, the aggregate leverage was 41.1%, within MAS’s 50% regulatory limit and leaving around US$70 million of debt headroom.

In November 2025, it has upsized its secured overnight financing rate (SOFR) and revolving credit facilities to US$350 million. It has also extended the debt maturity to 2029 and beyond. The facility incorporates a delayed-draw component that can be used to refinance the US$41 million Upland Square fixed-rate mortgage maturing in November 2026. It does not have any refinancing requirement till February 2028.

As of 1Q26, the weighted average debt maturity was 3.2 years, from 3.4 years in 4Q25. Weighted average interest rate declined for the fourth consecutive period to 4.91%.

Interest coverage remained healthy at 2.4x, versus the regulatory minimum of 1.5x.

Based on these credit metrics, we think it has adequate financial flexibility to grow the portfolio through inorganic accretive acquisitions.

Average interest cost was 4.91% in 1Q26, from 5.01% in 4Q25. United Hampshire US REIT has benefitted from the gradual decline in SOFR in 2025.

70% of total debt is on fixed or swapped-to-fixed rates, providing near-term income certainty. If the benchmark interest rate declines modestly, it will benefit when rolling over fixed-rate hedges at lower prevailing rates.

FY2025 Financial Results

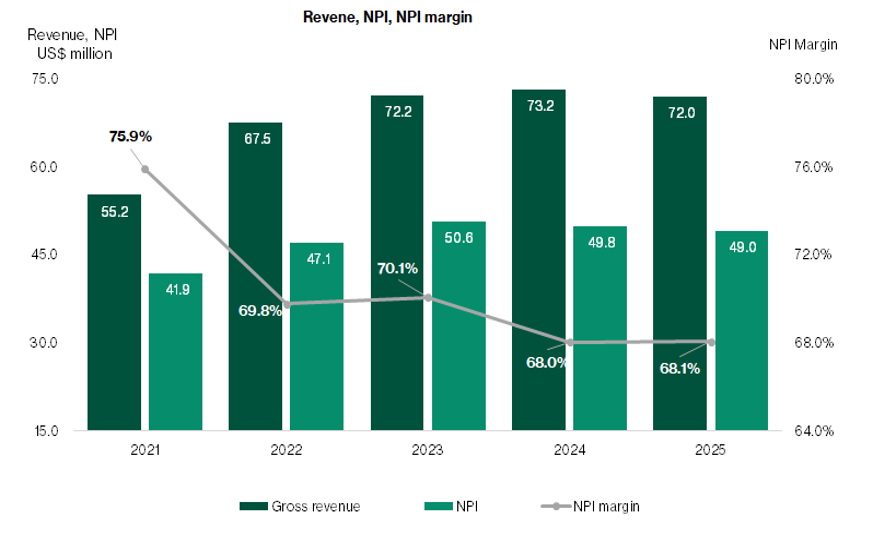

Revenue and net property income

FY2025 gross revenue was US$72.0 million, a decline of 1.7% year-on-year, primarily due to the absence of contributions from three divested properties: the freestanding Lowe’s and Sam’s Club units within Hudson Valley Plaza (divested August 2024) and Albany Supermarket (divested January 2025).

Excluding these divestments, same-store gross revenue would have grown 2.3% year-on-year, driven by new lease commencements, built-in rental escalations, and the initial contribution from Dover Marketplace.

Net property income of US$49.0 million (NPI margin: 68.1%) was similarly impacted by the divestments, declining 1.7% year-on-year. On a same-store basis, NPI would have increased 4.1%, reflecting the leverage advantage of triple-net leases as operating cost growth is largely passed through to tenants.

Distributable income and Distribution per unit (DPU)

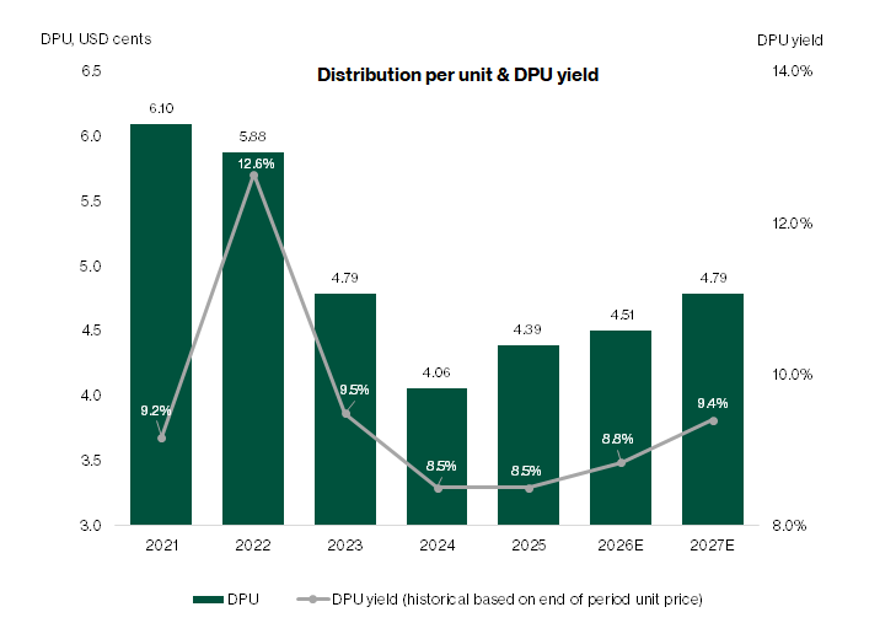

FY2025 distributable income increased by 5.7% year-on-year to US$26.9 million, notwithstanding the revenue decline, as lower finance costs from the Fed’s 175 basis points of rate reductions since September 2024 and partial loan repayments from divestment proceeds drove a meaningful reduction in net interest expense.

It declared a distribution per unit (DPU) of 4.39 US cents for FY2025, increased by 8.1% year-on-year, delivering the third consecutive period of DPU growth. This also represents the third consecutive year of DPU growth.

At the current unit price of US$0.51 as at 4 June 2026, UHREIT offers a FY2025 distribution yield of 8.6%, 410 basis points above the U.S. 10-year Treasury yield.

Portfolio valuation

UHREIT’s portfolio valuation increased 3.8% on a like-for-like basis (excluding acquired and divested properties) to US$774.3 million as at 31 December 2025, the fifth consecutive year of like-for-like valuation gains since listing. Total AUM has grown 32.4% from US$584.6 million at IPO, reflecting both the quality of the portfolio and the effectiveness of the capital recycling strategy.

Net asset value per unit was US$0.73 as at 31 December 2025, broadly stable from US$0.75 at IPO despite five years of distribution payments, reflecting the portfolio’s appreciation in value. UHREIT currently trades at 0.71x P/NAV, a 29% discount to book value — the widest discount among SGX-listed REITs with comparable portfolio quality and income stability.

Industry outlook

United States: grocery-anchored strip centres

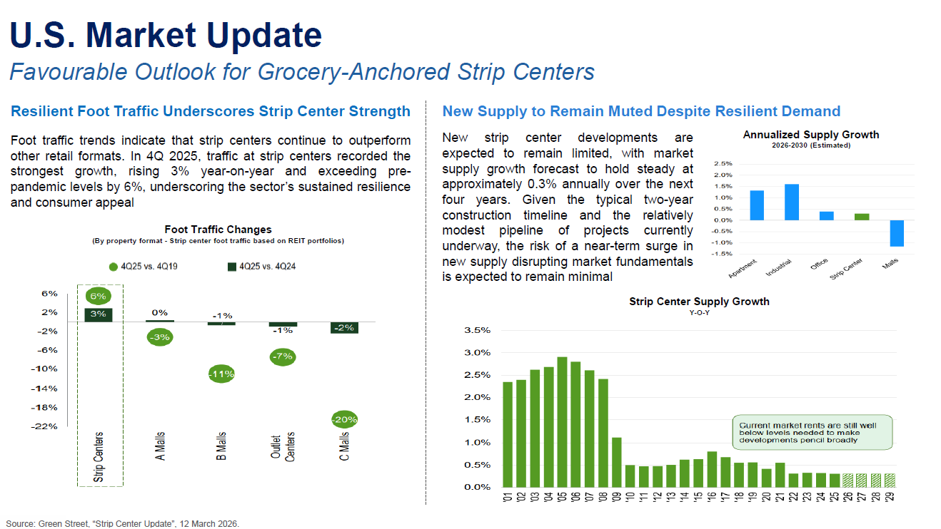

The U.S. retail real estate sector is undergoing a bifurcation: higher-quality, necessity-anchored formats continue to outperform, while discretionary and enclosed mall formats face structural headwinds from e-commerce and changing consumer behaviour.

Grocery-anchored strip centres sit firmly in the outperforming cohort, benefiting from non-discretionary consumer spending, limited new supply, and growing demand for physical fulfilment infrastructure.

Strip centre market fundamentals entering 2026 are the strongest in at least two decades. Market leased occupancy is approximately 95%, with asking rents growing mid-single digits year-on-year.

New supply is structurally constrained by elevated construction costs, which compress development returns below acquisition yields — a self-reinforcing dynamic that should sustain occupancy and rent growth well into the decade.

For U.S. grocery-anchored REITs, this backdrop is constructive.

United States: self-storage

The U.S. self-storage sector continues to benefit from structural demand drivers: an increasingly mobile population, the shift to smaller urban and suburban housing, and the impact of remote and hybrid work arrangements on residential space utilisation.

The New York Metropolitan Area, where United Hampshire US REIT’s two self-storage properties are located, remains among the most undersupplied major U.S. markets, with 2,616 sq ft of supply per 1,000 inhabitants versus a national average of 5,365 sq ft.

Self-storage sector same-store net operating income (NOI) has grown at a 4.6% CAGR over 24 years, outperforming inflation, and major U.S. property sectors by 2.4% and 1.8% respectively, with outperformance achieved in 18 out of 24 years.

Despite a sector-wide occupancy normalisation through 2024–2025 following exceptional pandemic-era demand, the supply-demand backdrop for the New York Metro Area remains supportive of sustained above-average rent growth.

Initiate at Buy with target price of US$0.62

United Hampshire US REIT provides a defensive cash flow profile anchored by grocery and necessity-based retail properties on the U.S. East Coast. Its portfolio consists 21 strip centres that focused on grocery and necessity retail. It trades at an attractive yield and provide long-term asset value stability. All the properties are freehold and leases are on triple net basis, making it an attractive proxy to US consumer spending.

We initiate coverage on United Hampshire US REIT with a BUY recommendation and a target price of US$0.62, based on the Dividend Discount Model (DDM) with a cost of equity of 10% and a terminal growth rate of 2.0%.

Our COE of 10% reflects the REIT’s U.S. dollar-denominated income base, the relatively small market capitalisation and associated liquidity premium, and the current S-REIT sector discount environment. We like United Hampshire US REIT for the disciplined approached towards capital management and long WALE. A long WALE provides earnings stability and reduces near-term leasing risk, while improving retail fundamentals across its key markets support a constructive outlook.

Our terminal growth rate of 2.0% is anchored on built-in lease escalations, the organic rent reversion potential of a 95%+ occupied portfolio, and the REIT’s demonstrated ability to recycle capital into higher-yielding assets.

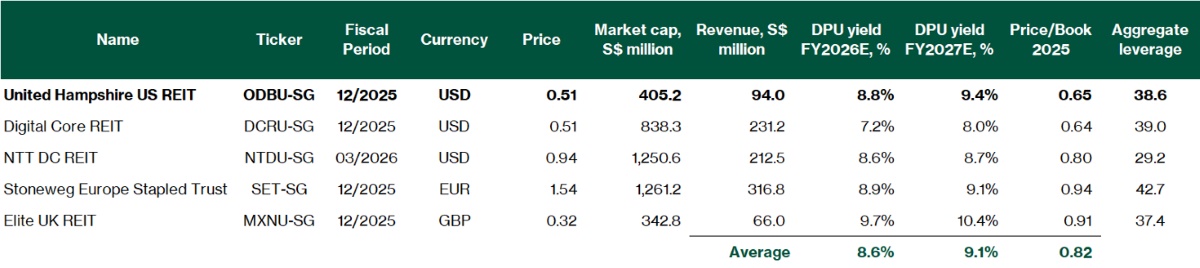

Currently, it is trading at US$0.51, implying FY26E distribution yield of 8.8%, FY27E distribution yield of 9.4%. This is attractive relative to peer valuation of FY26E and FY27E distribution yield of 8.6% and 9.1%, respectively.

We forecast gross revenue of US$74.1 million for FY2026E and US$77.1 million for FY2027E, reflecting 3.9% and 3.4% growth respectively, driven by commencement of new leases at recently acquired properties, built-in escalations across the existing portfolio, and the full-year contribution of Wallingford Fair Shopping Centre.

We project NPI margins to be broadly stable at 67% across the forecast period given the triple-net lease structure.

Distributable income is forecast at US$27.3 million in FY2026E and US$29.1 million in FY2027E, underpinned by NPI growth.

We project DPU of 4.51 US cents in FY2026E and 4.79 US cents in FY2027E, representing distribution yields of 8.8% and 9.4% at the current price. This is slightly higher than other listed REIT denominated in USD.

United Hampshire US REIT maintains a payout ratio of around 95%.

The broader S-REIT sector is well positioned entering 2026, with easing global interest rates reducing refinancing costs and supporting sector-wide P/NAV re-rating.

U.S.-focused S-REITs have been among the most affected by the rate cycle, with average sector discounts to NAV widening to 60–70%.

As rate headwinds abate and distributable income growth resumes, we expect sector discounts to narrow. UHREIT’s combination of a defensive grocery-anchored portfolio, improving DPU trajectory, and healthy balance sheet positions it as a compelling re-rating stories within the U.S. S-REIT subset.

Key risks

Key risks include concentrated exposure to single tenant, low trading liquidity, exposure to economic cyclicality.

Concentrated exposure to anchor tenants

As at 31 March 2026, the top 10 tenants accounted for 52% of gross rental income. The largest single tenant, BJ’s Wholesale Club Holdings, represents approximately 10.1% of portfolio gross rental income. Any material deterioration in BJ’s financial health, closure of stores, or failure to renew leases could have an adverse impact on United Hampshire US REIT’s income. However, BJ is an established company and publicly listed company (NASDAQ: BJ) with a market capitalisation of US$11.3 billion. We think this mitigates near-term risk on the portfolio income.

Currency risk

United Hampshire US REIT’s income and NAV are denominated in U.S. dollars. Singapore-based investors are therefore exposed to SGD/USD fluctuations, which could affect the Singapore-dollar value of distributions. Management partially mitigates this by offering distributions payable in USD, SGD (at the prevailing exchange rate), or via the Distribution Reinvestment Plan. The DRP take-up rate has historically ranged from 6% to 32%, with an average of approximately 20%.

Interest rate risk

While the current environment is characterised by declining interest rates, an unexpected reversal — driven by persistent inflation or exogenous shocks — could compress UHREIT’s distributable income. With 21.5% of borrowings on floating-rate SOFR, each 100 basis point increase in rates reduces annual distributable income by approximately US$0.7–0.8 million, equivalent to roughly 0.1–0.13 US cents per unit on current unit count.

Macro-driven consumer spending softness

Grocery-anchored strip centres are not entirely immune to macroeconomic deterioration. A sustained consumer spending downturn — whether driven by tariff-related price increases, employment deterioration, or global financial shocks — could affect tenant sales and, ultimately, the ability of inline tenants to absorb built-in rent escalations upon renewal. UHREIT’s exposure to this risk is partially mitigated by the essential, non-discretionary nature of its anchor tenants, but the tail risk exists.

Trading liquidity

UHREIT’s market capitalisation of approximately US$324 million (S$439 million) and three-month average daily turnover of approximately US$0.19 million place it at the smaller end of the SGX REIT universe. This may limit institutional ownership and result in a structural liquidity discount relative to larger-capitalisation peers. Investors should factor liquidity considerations into position sizing.

Related links:

- United Hampshire US REIT share price and share price target

- United Hampshire US REIT dividend history and forecast

Download the full report here.

Check out Beansprout guide to the best stock trading platforms in Singapore with the latest promotions to invest in United Hamsphire US REIT.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments