AI is reshaping global markets. Here's what investors need to know.

Stocks

By Ng Hui Min • 17 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Artificial intelligence (AI) is driving renewed interest in global markets and tech stocks. Here’s what investors should know what is driving the AI boom.

What happened?

Artificial intelligence (AI) stocks are back in focus.

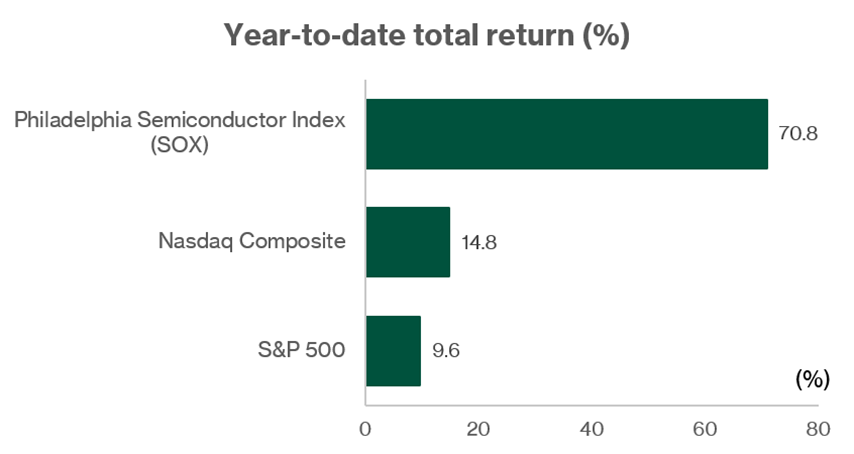

Year to date, the Philadelphia Semiconductor Index (SOX) has surged 70.9%, far outpacing the Nasdaq Composite’s 13.3% gain over the same period.

Nvidia’s rise to become the first listed company with a market capitalisation of US$5.5 trillion further underscores how deeply the AI theme has reshaped global markets.

Earlier we have also highlighted AI and data centres as a growing theme for Singapore stocks and also discussed if this AI rally has gone too far.

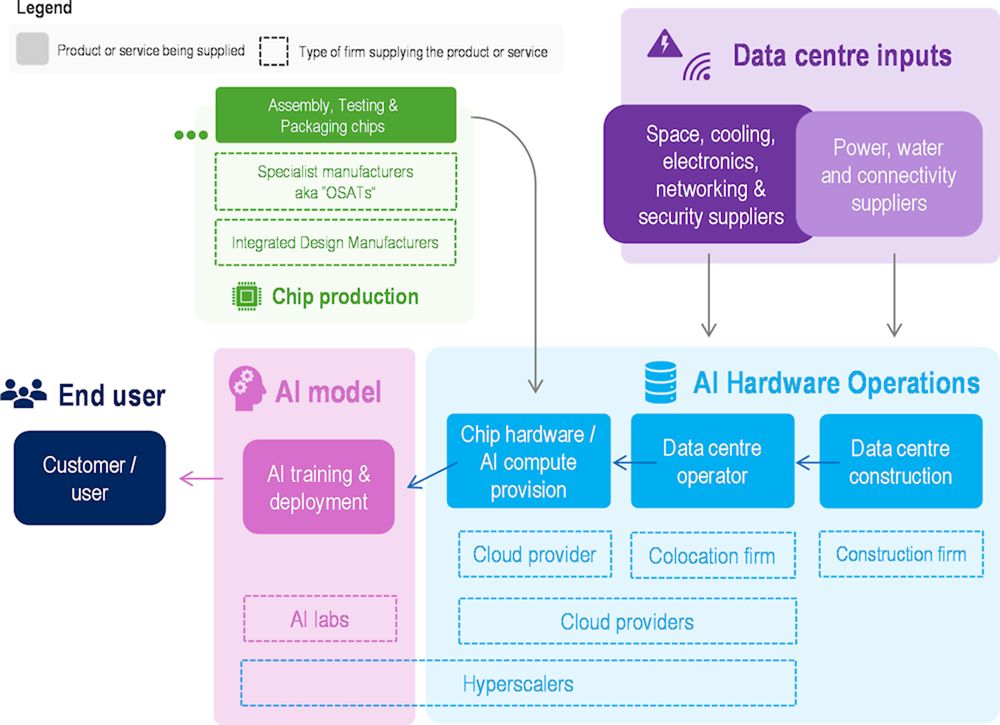

The AI boom is reshaping demand across the technology supply chain, from semiconductors and data centres to cloud computing, advanced manufacturing and precision engineering.

In this primer, we look at how the AI and technology value chain works, the growth drivers of the AI technology boom, and what investors should watch before jumping onto the AI wave.

What you need to know about the rally

#1 - AI is becoming the foundation of chip demand

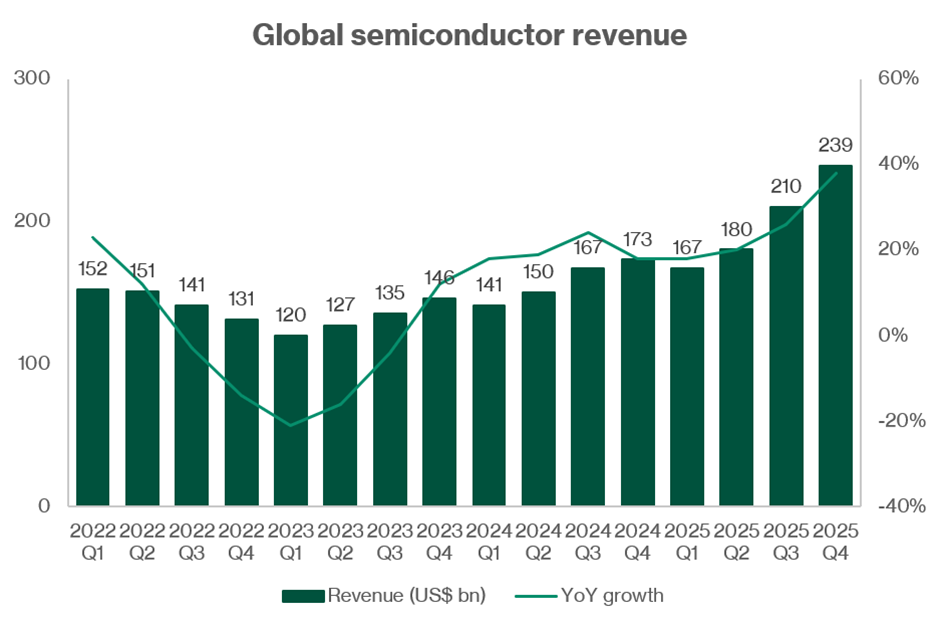

The global semiconductor industry is entering a new phase.

AI is no longer just one source of demand. It is increasingly becoming the key driver of growth across the chip industry.

Global semiconductor revenue reached around US$793 billion to US$800 billion in 2025, growing strongly from the year before. Looking ahead, industry forecasts suggest the market could continue expanding rapidly as demand for AI infrastructure drives spending on memory chips, processors and networking components.

The fastest-growing segment is AI chips. These include the accelerators, GPUs and specialised processors used to train and run AI models.

But the AI opportunity is not limited to companies selling AI chips directly. It also extends to high-bandwidth memory, networking silicon, CPUs, servers, storage and data centre infrastructure.

This matters because AI is creating a broader investment cycle across the semiconductor value chain. Suppliers of semiconductor equipment, precision components, testing services, advanced manufacturing and data centre infrastructure may also benefit from this structural growth trend.

#2 - Growth drivers behind the AI technology boom

The hyperscaler spending race

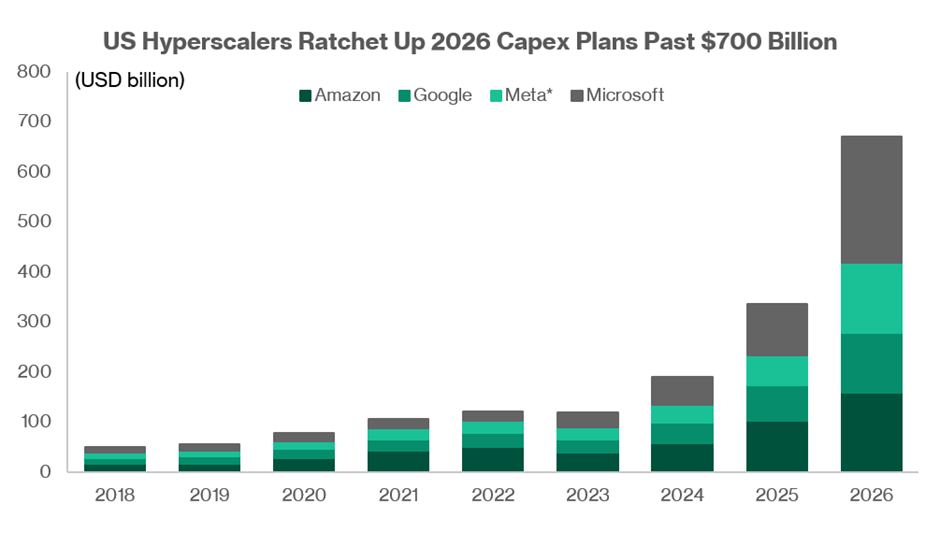

The biggest driver of AI semiconductor demand today is spending by the world’s largest technology companies.

Major hyperscalers such as Amazon, Alphabet, Microsoft and Meta Platforms are investing heavily in AI infrastructure, including data centres, GPUs, networking equipment and storage.

Source: Bloomberg, data as of 1 May, 2026

AI models require enormous computing power, and the infrastructure needed to support them continues to grow rapidly.

Collectively, the four major hyperscalers are now expected to spend up to US$725 billion in capital expenditure in 2026, nearly double what they spent in 2025.

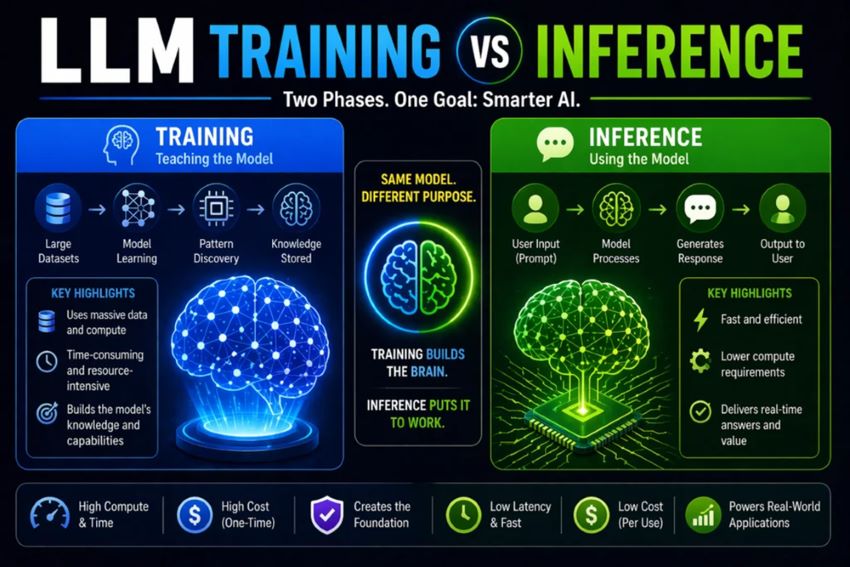

The rise of AI inference

The AI boom is also moving into a new phase.

The first wave focused on training large AI models. The next phase is inference, where these models are deployed at scale to millions of users and applications.

As AI becomes embedded into search, software, automation and digital assistants, demand for computing power could become more recurring and durable, rather than a one-off investment cycle.

The rise of AI agents, which are systems that can perform tasks or take actions on behalf of users, could increase compute demand even further.

High-bandwidth memory becoming a bottleneck

AI chips also require more advanced memory to perform efficiently.

High-bandwidth memory, or HBM, allows chips to process vast amounts of data at high speed, making it a critical part of the AI supply chain.

Demand has risen so quickly that industry forecasts are being revised upward.

Micron now expects the HBM market to reach US$100 billion in revenue by 2028, compared with around US$35 billion in 2025.

This is earlier than previous expectations for the industry to hit the US$100 billion milestone only by 2030.

This implies annual growth of almost 42%, well above Micron’s earlier estimate of 23%.

As a result, memory manufacturers and suppliers of advanced semiconductor components are becoming key beneficiaries of the AI investment cycle.

Rising complexity in chip packaging and testing

As semiconductors become smaller and more complex, packaging and testing requirements are increasing significantly.

AI chips require much more intensive testing because failures in large AI data centres can be extremely costly.

This trend benefits semiconductor equipment, testing and precision engineering companies, as chipmakers require more advanced tools and services to support increasingly complex production processes.

Governments pushing for sovereign AI

Governments are also investing heavily in domestic AI and semiconductor capabilities.

Initiatives such as the US CHIPS Act and semiconductor investments in the US, Japan, India and the Middle East are reshaping global supply chains.

More than US$250 billion in new fab investments have been announced, spanning TSMC’s Arizona facilities, Samsung’s Texas complex and Intel’s Ohio fabs.

This may create longer-term opportunities for contract manufacturers, precision engineering firms and semiconductor suppliers across Asia, including Singapore-listed companies linked to the global technology supply chain.

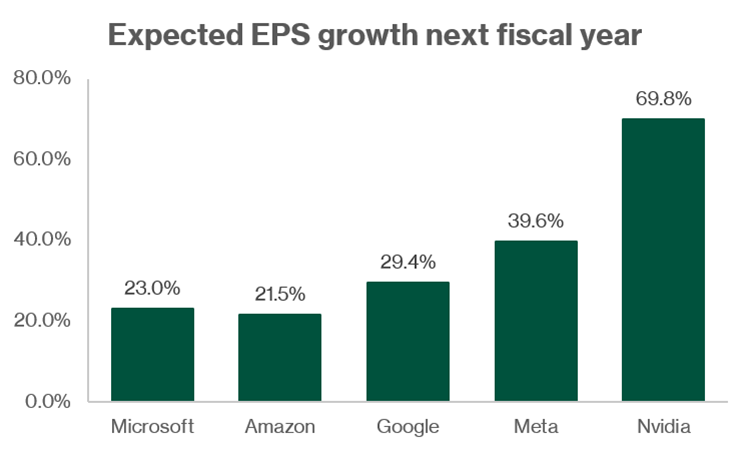

#3 - The rally is supported by a strong earnings outlook

Earnings momentum in the AI technology sector remains strong.

Semiconductor and equipment companies have been among the biggest beneficiaries, supported by rising demand for AI chips, memory, networking equipment and data centre infrastructure.

The strength is not limited to chipmakers. Cloud providers such as Microsoft, Amazon, Google, Oracle and Meta are also contributing meaningfully to earnings growth, as AI spending becomes a larger part of their long-term investment plans.

For 2026, the outlook remains supported by hyperscaler capex. This provides visibility for semiconductor equipment makers, memory suppliers and precision manufacturers.

For Singapore investors, this matters because some SGX-listed companies sit further down the same supply chain. They may not sell AI chips directly, but they can still benefit when global chipmakers and equipment manufacturers increase production.

The key risk is whether AI monetisation can keep pace with the massive infrastructure spending. If companies struggle to turn AI investment into revenue and profits, the market may start to question current valuations.

For now, earnings growth remains the main support for the AI technology rally. However, investors should watch whether revenue growth, margins and order books continue to justify the optimism.

What would Beansprout do?

The AI and technology sector is going through a major structural shift.

AI is becoming a key driver of growth across the semiconductor industry, supporting demand for chips, high-bandwidth memory, processors, networking components, servers, storage and data centre infrastructure.

This means the opportunity may extend beyond companies that sell AI chips directly. Suppliers of semiconductor equipment, precision components, testing services, advanced manufacturing and data centre infrastructure may also benefit from this investment cycle.

However, we would not chase the rally blindly. While earnings momentum remains strong, the key risk is whether AI monetisation can keep pace with the massive infrastructure spending.

Not all AI-related stocks offer the same risk-reward profile. We would focus on companies with growing revenue, stronger order books, improving margins and healthy cash flow, rather than those rising mainly on AI sentiment.

To find out if the rally can be sustained, check out our thoughts on whether the AI rally has gone too far.

To me, broad equity exposure can sit within the Growth Pot, while higher-conviction AI names can be sized within the Opportunity Pot so that I can participate without taking excessive concentration risk.

If you are looking for more Singapore stock ideas linked to AI growth theme, explore our high-conviction curated stock opportunities here.

Which part of the AI theme are you watching most closely now? Share with us in the comments below or in our Telegram group!

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

1 comments

- Jane • 18 May 2026 12:06 AM