Has the AI rally gone too far?

Stocks

By Gerald Wong, CFA • 15 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Is AI a bubble or a real revolution? I look at 5 reasons why the AI rally may be real, 5 warning signs to lookout for, and what investors may watch before buying AI stocks.

What happened?

AI stocks are back in focus.

Some investors see AI as a long-term growth theme, while others are asking if valuations are starting to look like a bubble.

The debate has grown louder after the Nasdaq reached an all-time high, supported by continued optimism around AI and large US technology stocks.

This is not just a US market story as the AI theme has also extended to Asia.

We recently highlighted AI and data centres as one of the 3 growth themes to watch in Singapore, while Taiwan and South Korea remain key parts of the global semiconductor supply chain.

Against this backdrop, I thought it would be useful to ask a bigger question: is the AI rally a real technological revolution, or are investors paying too much for future growth?

In this article, I look at five reasons the AI rally may have real substance, five warning signs that look bubble-like, and the signals I would watch before adding more exposure.

Has the AI rally gone too far?

Every revolution starts with a bubble.

Railways had their boom. Electricity had one too. So did the internet.

In each cycle, investors rushed in before the full impact of the technology was clear. Valuations climbed, expectations stretched, and speculation eventually took over.

Many of those bubbles burst. But the story did not end there.

Railways changed trade. Electricity transformed how economies worked. The internet reshaped communication, commerce and productivity.

The bubble eventually faded; the revolution did not.

As artificial intelligence captures the world's attention today, investors are asking the same question:

Are we witnessing another bubble, or the early stages of the next technological revolution?

The honest answer is that both stories can be true at the same time.

AI may still transform the way businesses operate. At the same time, some AI-related stocks may already be pricing in very high expectations.

So, before we dismiss AI as another bubble, let’s start with the case for why this rally may still be supported by real fundamentals.

Five reasons the AI rally may not be a bubble

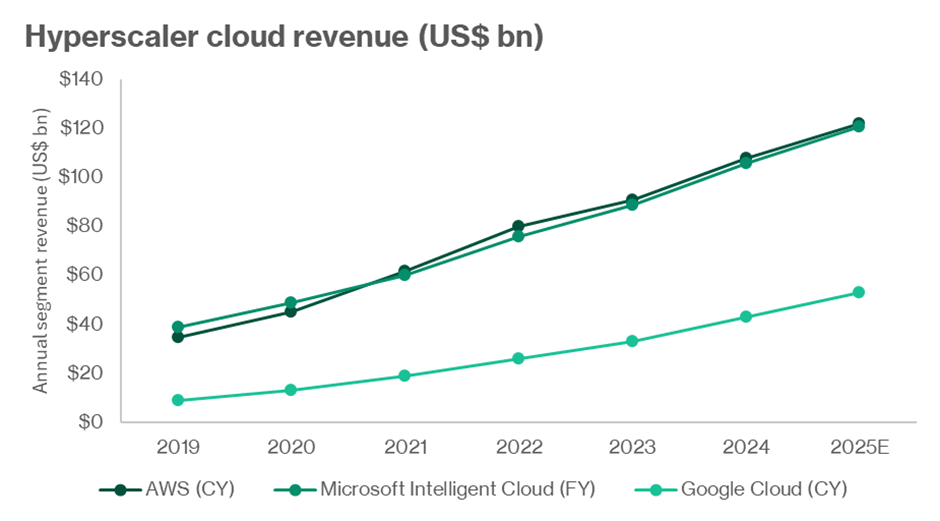

#1 - The revenue is real, and growing rapidly

One reason AI may not be a bubble is that the revenue is already showing up.

The large cloud companies are not just selling a future promise. They are already generating revenue from cloud computing, AI model training, inference capacity, and software subscriptions.

This is supported by rising corporate spending on AI. Businesses are using AI to improve customer service, automate workflows, analyse data, and support software development.

Cloud revenue across the major hyperscalers has continued to grow steadily, showing that demand is being backed by real spending rather than just market excitement.

This makes today’s AI boom quite different from the dot-com bubble in 2000. Back then, many internet companies had little revenue and unproven business models.

Today, many of the biggest AI beneficiaries are large, profitable companies with existing customers, strong cash flow, and the ability to invest heavily in infrastructure.

More importantly, much of the spending is going into assets that could remain useful even if the hype fades.

Data centres, GPUs, fibre networks, and power infrastructure are not speculative collectibles. They are long-term assets that support the digital economy.

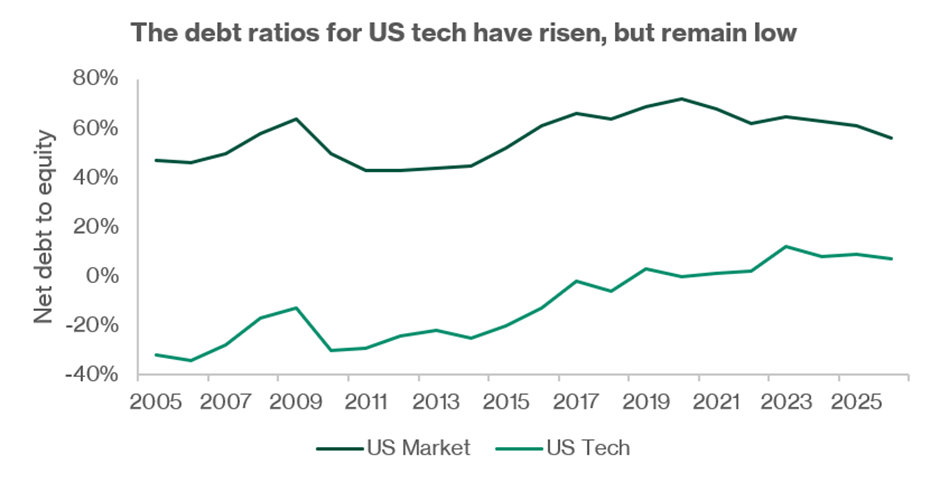

#2 - AI spending is being funded by cash, not just optimism

Another reason AI may not be a bubble is that the spending is being funded from real cash flows.

This is an important difference.

During the late-1990s telecom boom, many companies built infrastructure aggressively based on optimistic demand forecasts. Some relied heavily on debt to fund expansion before the cash flows were fully proven. When demand failed to meet expectations, balance sheets came under pressure.

The AI build-out today looks different.

The major hyperscalers are spending heavily on data centres, chips and cloud infrastructure. But much of this capital expenditure is being funded by strong operating cash flows from existing businesses such as search, advertising, cloud and software.

This does not mean there is no risk. AI spending could still disappoint if future demand falls short of expectations.

However, the funding base appears stronger than in past bubble-like cycles. Many large US technology companies have strong cash positions and lower debt levels compared to the broader market.

This gives them more room to invest through the cycle without relying too heavily on borrowed money.

The two charts below help explain why this matters. US technology companies generally carry lower debt ratios than the wider market, which suggests that much of the current AI investment is being supported by internal cash generation rather than excessive leverage.

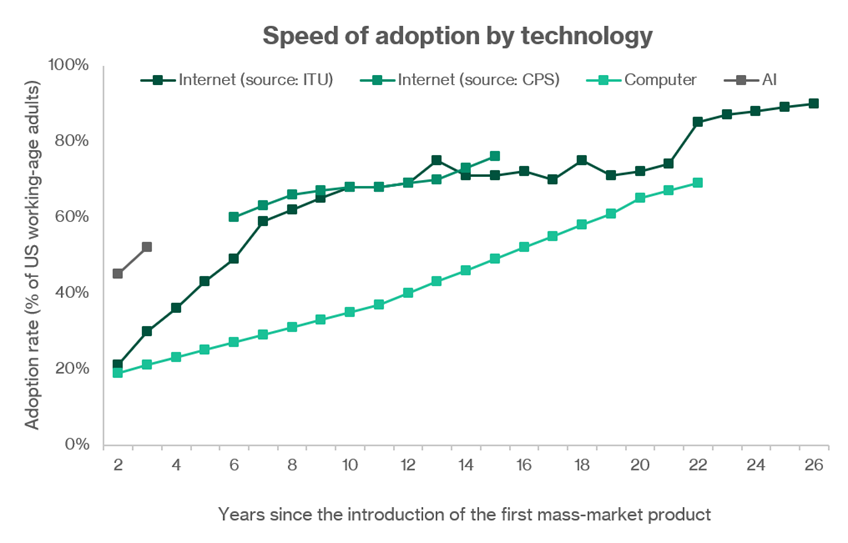

#3 - AI is moving from theory into real-world use

Unlike some past technology booms, AI is already being tested and used across actual business workflows.

AI is no longer just a concept discussed by researchers or technology companies. It is already being used in areas such as coding, customer support, marketing content, drug discovery, insurance claims processing, and data analysis.

In some of these areas, companies are starting to see practical benefits. Tasks can be completed faster, costs can be reduced, and teams can handle a higher volume of work.

That said, the impact is still uneven.

Some business processes are already being meaningfully improved by AI, while others remain at the testing or pilot stage. This explains why the benefits may not yet be fully visible in broader economic productivity numbers.

This is not unusual for major technologies.

Electricity, computers, and the internet also took time to spread across the economy. The productivity gains did not appear overnight. They emerged gradually as companies changed the way they worked.

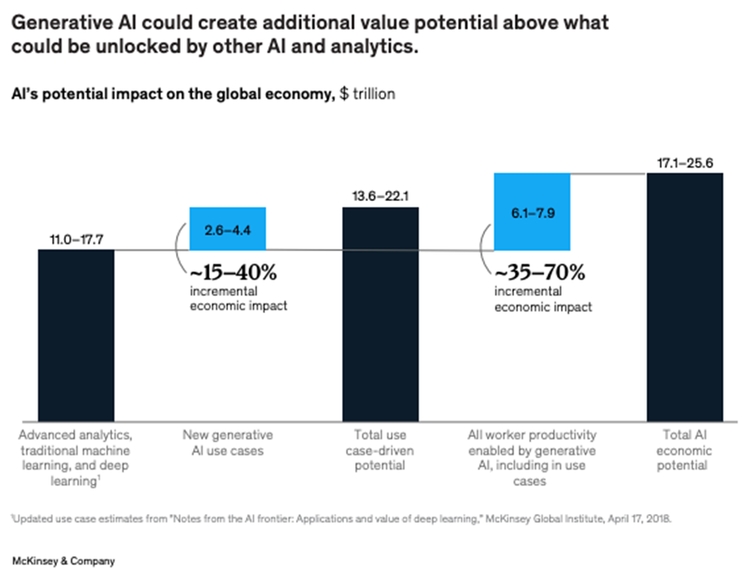

The adoption curve below helps put this into perspective. Compared with past technologies such as computers and the internet, AI still appears to be in the early stages of adoption, which suggests there may be significant room for further growth.

The chart below draws from McKinsey & Company's research on AI's potential impact on the global economy.

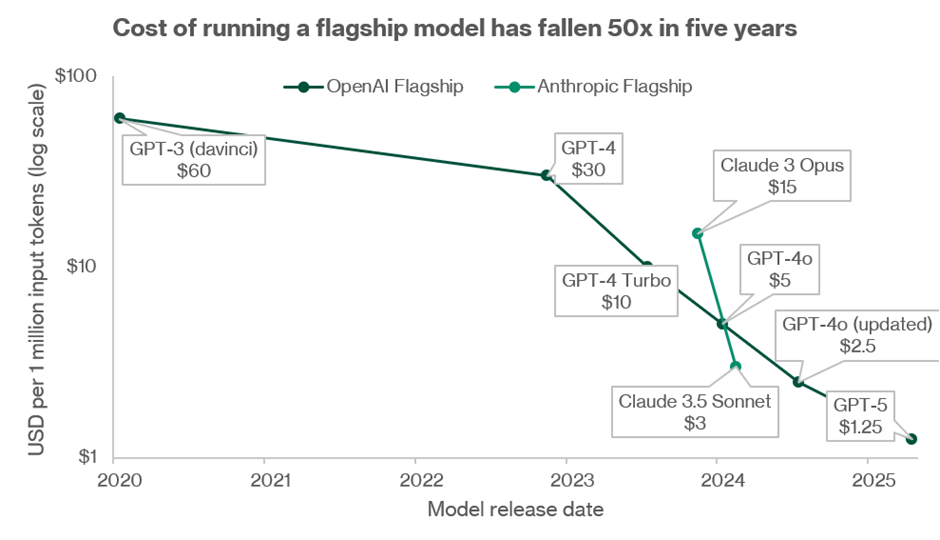

#4 - The cost of AI is falling quickly

The economics are improving quickly.

The cost of using AI models has been falling sharply, helped by better models, more efficient chips, and improvements in how these systems are deployed.

This matters because AI becomes more useful when it becomes cheaper to use.

In the early stages, only large companies may be able to afford advanced AI tools. But as the cost of “intelligence” falls, more businesses can start using AI in everyday workflows, from customer service and coding to marketing, data analysis and operations.

The decline in model pricing has been significant. The cost of running flagship AI models from OpenAI and Anthropic has fallen with each new generation, making advanced AI capabilities more accessible over time.

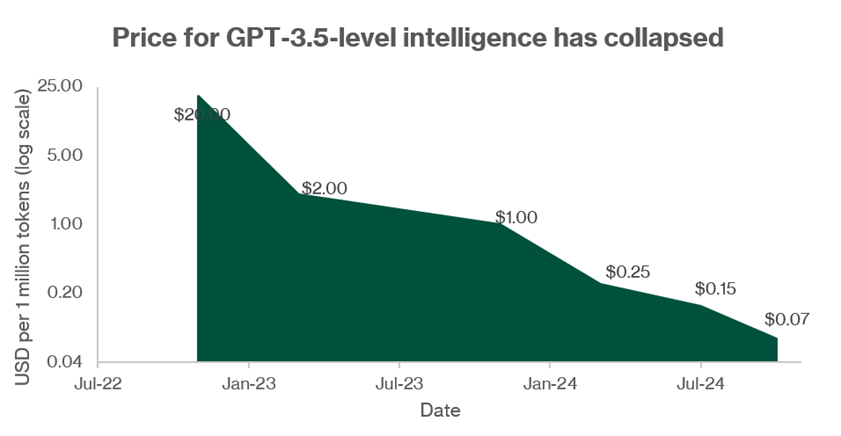

The trend becomes even clearer when we compare the cost of achieving a similar level of capability. The cost of querying a model with GPT-3.5 level performance reportedly fell from around US$20 per million tokens in late 2022 to less than US$0.10 by late 2024.

Lower costs could unlock more use cases that were previously too expensive to justify. For example, a company may not use AI for customer support if each query is costly. But if the cost falls sharply, the same use case may suddenly become economically viable.

This is different from many speculative bubbles.

In a bubble, prices often rise because investors expect someone else to pay more later. The underlying asset does not necessarily become more useful or cheaper to produce.

With AI, the opposite may be happening. The technology is becoming more capable, while the cost of using it is falling.

#5 - Even if the boom cools, the infrastructure remains

Even if enthusiasm around AI fades at some point, the infrastructure being built today may still have long-term value.

History offers some useful lessons.

During past investment booms, many investors lost money when valuations fell and weaker companies collapsed. But the physical assets built during those periods often continued to support economic growth for many years.

Railway companies went bankrupt after the railway boom in the 1800s, but the tracks still helped move goods across economies. The telecom crash in the early 2000s wiped out many companies, but the fibre networks built during that period later became part of the backbone of the modern internet.

The same could apply to AI infrastructure.

Data centres, power capacity, fibre networks and GPUs do not disappear just because share prices fall. These assets can continue supporting cloud computing, AI applications, video streaming, enterprise software, and future digital services.

This is why the AI boom should not be viewed only through the lens of short-term stock market performance.

Some AI-related companies may still be overvalued. Some investments may not generate the returns investors expect. But the infrastructure itself could remain valuable, especially if demand for computing power continues to grow over time.

Five reasons the AI rally looks bubble-like

The AI rally has been supported by real revenue, strong cash flows, and rising adoption.

But that does not mean investors should ignore the risks.

Even if AI is not a repeat of the dot-com bubble, parts of the market are starting to show bubble-like behaviour. The main concern is not that companies have no earnings. It is that share prices may already be assuming a very optimistic path for future earnings.

Here are five reasons why some investors remain cautious.

#1 - Valuations may look reasonable, but earnings forecasts are demanding

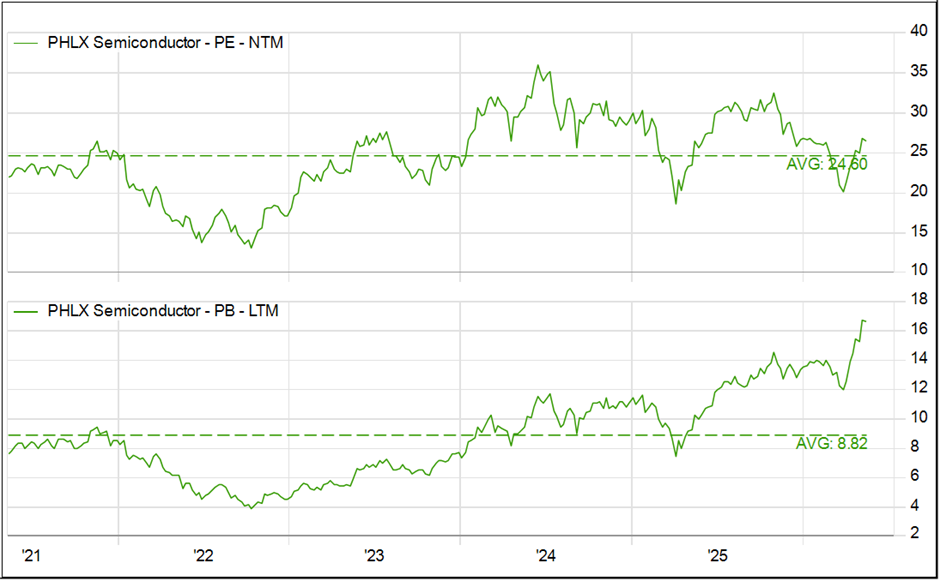

At first glance, valuations for some AI-related stocks do not look as extreme as past bubbles.

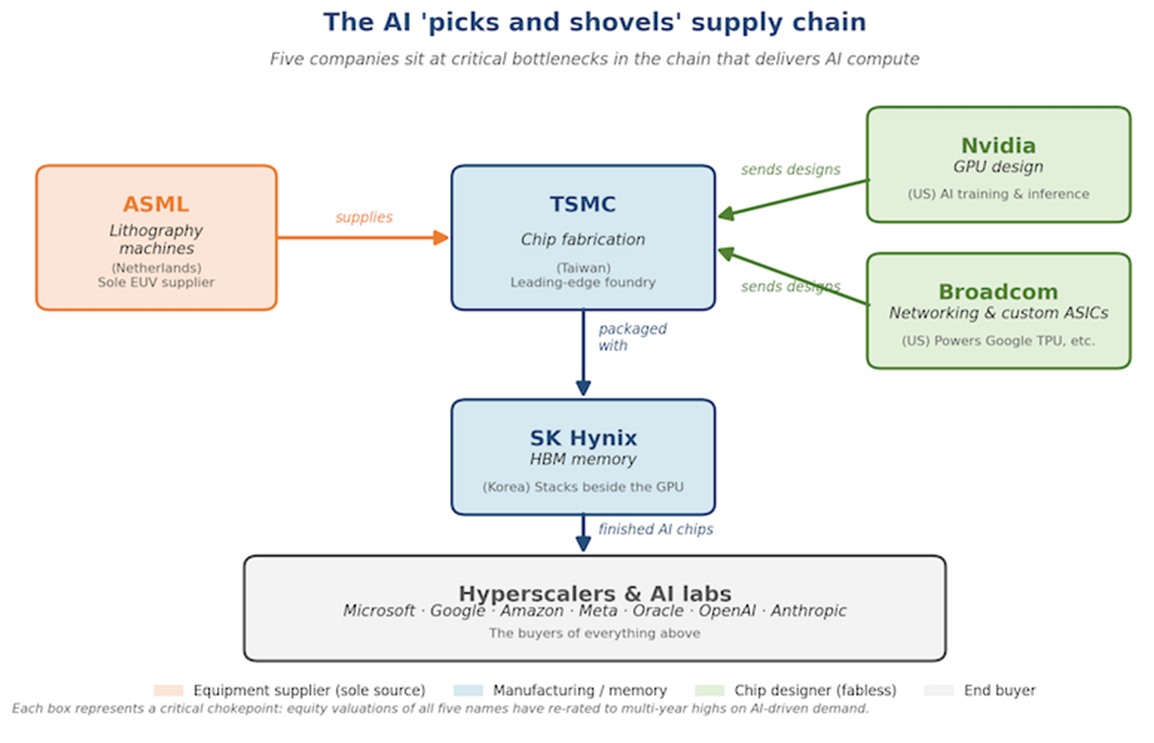

Many of the key “picks and shovels” companies, such as Nvidia, Broadcom, TSMC, SK Hynix and ASML, have delivered strong earnings growth. This has helped their profits catch up with their rising share prices.

As a result, headline valuation multiples such as forward price-to-earnings ratios no longer look as stretched as they did earlier in the rally.

For example, the Philadelphia Semiconductor Index was trading at a forward P/E ratio of 26.6 times as of 13 May 2026. This is above its historical average of 24.6 times, but not at the kind of extreme level that would immediately suggest a bubble.

The bigger issue is what those valuations are assuming.

If earnings forecasts already reflect years of strong AI demand, rising margins, and continued spending by the major cloud companies, then there is less room for disappointment.

A slowdown in AI chip orders, a change in model architecture, or a pause in hyperscaler capital expenditure could lead analysts to cut their earnings forecasts.

In that scenario, a stock that looks fairly valued based on today’s earnings expectations could suddenly look expensive based on lower future earnings.

#2 - Valuations depend heavily on future expectations

Another warning sign is that some AI valuations depend heavily on what investors expect to happen in the future.

In simple terms, many AI stocks are not being priced only on what these companies are earning today. They are also being priced on the belief that AI could eventually transform large parts of the economy, automate many office tasks, and create trillions of dollars in new value.

That may happen. But it has not fully shown up in earnings yet.

A simple way to think about this is like buying a property at a very high price because you expect a new MRT station to be built nearby in 10 years. If the station is completed on time and brings more demand, the price may be justified. But if the project is delayed, scaled down, or does not lift demand as much as expected, the price paid earlier may start to look too high.

The same applies to AI stocks.

When share prices already assume a very strong future, even small disappointments can lead to sharp corrections. This could happen if AI adoption takes longer than expected, if companies struggle to monetise AI tools, or if the expected productivity gains do not translate into profits quickly enough.

History gives us a useful reminder.

The internet did change the world, and many of the long-term predictions from the late 1990s eventually came true. But share prices had moved too far ahead of business reality.

Many investors who were right about the technology still lost money because they paid too much, too early, during the boom.

*Actual (LTM) P/E and EV/Sales data from 02/01/1973 for Nifty 50.

** LTM P/E data and EV/sales from 27/12/1989 for Japan Financial Bubble.

***24m Fwd P/E and EV/Sales data from 24/03/2000 for tech bubble.

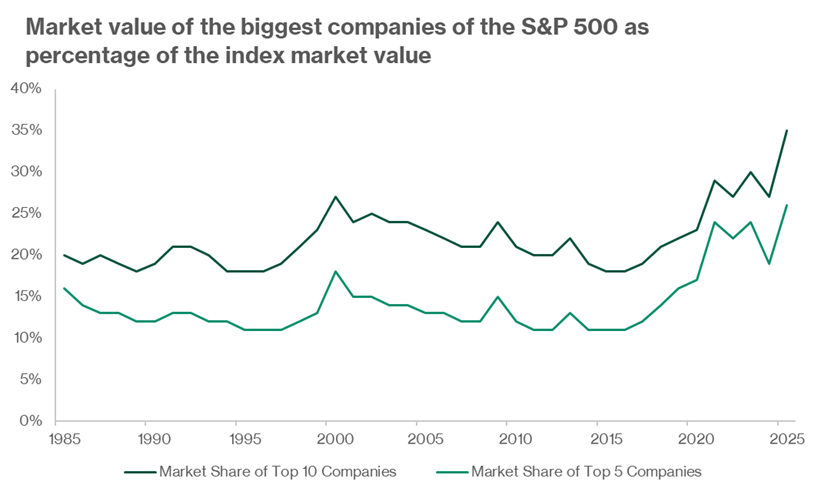

#3 - Passive flows and index concentration amplify the rally

Another bubble-like feature is how concentrated the market has become.

The biggest AI winners now make up a large share of major equity indices such as the S&P 500 and NASDAQ. This matters because many investors gain exposure to markets through passive funds and ETFs.

When money flows into these funds, the largest index constituents receive more buying automatically. This can provide strong support for AI-related stocks on the way up, even if valuations are already stretched.

But the same mechanism can work in reverse.

If sentiment turns and investors start pulling money out of equity funds, the largest index names may also face the most selling pressure. This could make the decline sharper, especially if many investors are crowded into the same AI beneficiaries.

#4 - Circular financing may be making AI demand look stronger

A clearer risk is that some AI revenue may not be coming from independent end customers yet.

In parts of the AI ecosystem, money is moving in a loop.

For example, a chipmaker may invest in an AI start-up. That start-up then uses the funding to buy chips from the same chipmaker. A cloud provider may give capital, credits or favourable terms to an AI model company, which then commits to spending heavily on that same cloud platform.

This is known as circular financing.

The revenue is still real. Chips are being bought, data centres are being used, and cloud contracts are being signed.

But the important question is whether the demand is sustainable.

If AI companies are using cash generated from their own customers to pay for chips and cloud computing, that would be a healthier sign. But if a meaningful part of the spending is being funded by the same companies that benefit from the orders, then headline demand may look stronger than underlying end-user demand.

This is why some investors are becoming more cautious.

During the telecom boom in the late 1990s, some equipment suppliers helped finance customers that bought their products. This kept sales growing for a while, but became painful when actual demand failed to catch up.

The AI cycle today is not identical. The largest technology companies have much stronger balance sheets and are still generating strong cash flows from their existing businesses.

Still, circular financing is a risk worth watching.

#5 - Demand is concentrated in a small group of buyers and suppliers

One concern is that AI demand has not yet spread widely across the broader economy.

A large share of GPU and data centre orders is coming from a small number of buyers. These include the major cloud companies, a few leading AI labs, and sovereign-backed AI projects.

This has helped the AI build-out move quickly. These buyers have deep pockets, strong access to capital, and the ability to commit to large multi-year spending plans.

But concentration also creates risk.

If one major cloud provider slows its AI spending, the impact could be felt across the entire supply chain. The same could happen if a leading AI lab cuts back on compute demand, or if governments become more cautious about funding large AI infrastructure projects.

The supply side is also narrow.

Much of the AI supply chain depends on a small number of key players, such as a dominant GPU provider, a leading advanced chip foundry, and a key supplier of advanced chipmaking equipment.

This makes the AI ecosystem efficient, but also fragile.

A change in strategy by one large customer, a delay in chip production, an in-house chip programme, or a regulatory restriction could affect many AI-linked companies at the same time.

Four signals to tell if the AI rally is sustainable

The AI debate is not as simple as “bubble or not”.

There are real reasons to stay constructive. AI revenue is already showing up, the biggest companies are funding their investments with cash flow, and the technology is being used in more business workflows.

But there are also real risks. The rally is concentrated in a small group of stocks, some demand may be supported by circular financing, and valuations still depend on strong earnings growth continuing for many years.

That means a correction is still possible, even if the long-term AI story remains intact.

For investors, the more useful question is not whether AI is a bubble. It is whether the fundamentals can keep improving fast enough to justify the prices being paid today.

If AI revenue keeps broadening, data centres remain well used, and large companies continue spending because they see returns, the rally may still have room to run.

But if revenue growth slows while capital spending keeps rising, investors may start to question whether expectations have run too far ahead.

That is why I would watch four key signals to see whether the AI boom is strengthening or starting to lose momentum.

#1 - Demand: is the AI revenue real?

The most important question is whether AI revenue can grow beyond today’s narrow base.

For now, much of the visible AI demand still comes from a few areas. These include cloud spending at Microsoft, Google, and Amazon, large enterprise trials, and consumer subscriptions such as ChatGPT and Copilot.

For the AI bull case to remain intact, demand needs to broaden. More mid-sized companies need to adopt AI. More industries need to use AI in daily operations. AI use cases also need to move beyond coding, customer support and productivity tools.

The risk is that companies continue spending heavily on AI infrastructure, but the revenue generated from AI does not grow fast enough to justify the investment.

That is often when markets start to turn.

| What to track | Healthy signs | Warning signs |

| Quarterly earnings updates from Microsoft, Google, Oracle, Salesforce and ServiceNow after the January, April, July and October earnings seasons | AI growth accelerating, Copilot adoption beating expectations, demand outpacing supply, or share prices rising after results | AI returns under scrutiny, customers cutting AI spending, pilots failing to scale, or sharp share-price falls despite otherwise reasonable results |

#2 - Utilisation: Are the chips actually being used?

Data centres only create value if they are being used for real workloads.

That is why Nvidia remains one of the clearest signals for the AI cycle. Its chips are used in many major AI build-outs, so its quarterly results give investors a useful read on whether demand is still stronger than supply.

Strong chip demand would suggest that AI infrastructure is still being absorbed by the market.

Weakening demand, on the other hand, could suggest that companies have overbuilt capacity or that AI adoption is not growing quickly enough.

| What to track | Healthy signs | Warning signs |

| Nvidia’s quarterly earnings and next-day share-price reaction, with CoreWeave as a secondary indicator for GPU rental demand | Nvidia “beat-and-raise” quarters, reports of GPU shortages or chip waitlists, utilities building new power capacity for AI data centres, or CoreWeave rental prices rising | Nvidia missing estimates, its share price falling sharply after results, headlines shifting to GPU oversupply or data centre right-sizing, or delayed and cancelled data centre projects |

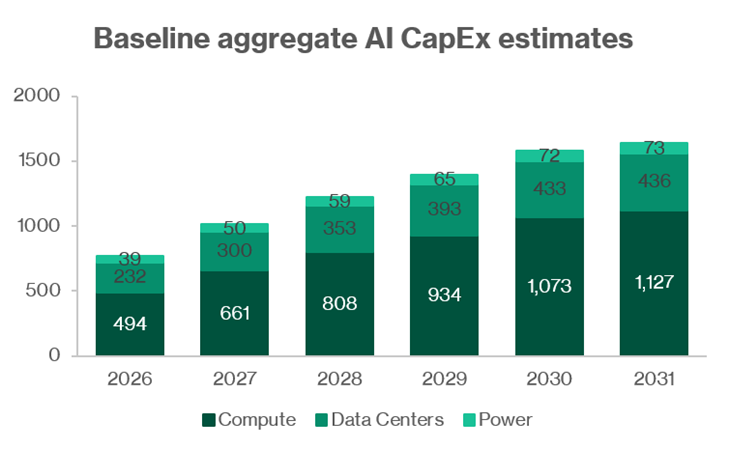

#3 - Forward orders: Are the big buyers still spending?

The AI boom is heavily dependent on a small group of very large buyers.

Microsoft, Google, Amazon, Meta and Oracle account for a large part of AI infrastructure spending. Every quarter, investors watch how much these companies plan to spend on data centres, chips and related infrastructure.

This spending is known as capital expenditure, or capex.

For now, rising capex is seen as a sign of confidence. It suggests that large technology companies still believe AI demand will be strong enough to justify the investment.

But if one major buyer starts cutting back, investors should pay close attention to whether others follow.

| What to track | Healthy signs | Warning signs |

| Capex headlines from the big five: Microsoft, Google, Amazon, Meta and Oracle | Microsoft raising capex to a record level, Google increasing AI infrastructure spending, or major new data centre and power-deal announcements | Meta pacing AI investment, Amazon scaling back data centre plans, executives questioning AI returns, or cancelled and delayed project |

#4 - Quality of demand: is the money real or just circulating?

This is harder to track, but it may be one of the most important signals.

Some AI demand is supported by a web of strategic investments and partnerships. For example, chipmakers may invest in AI companies that then buy their chips. Cloud providers may fund AI start-ups that commit to using their platforms.

Each deal may make sense on its own. But taken together, they can make headline demand look stronger than it really is.

This does not mean the AI boom is fake. But investors should be cautious if more demand starts to depend on financing from the same group of companies.

The risk is highest when companies continue announcing higher AI spending, but the market starts questioning whether the returns are real.

That gap between spending and returns is often where late-cycle risks start to build.

| What to track | Healthy signs | Warning signs |

| Tone of business-news coverage around major AI deals | New enterprise customers signing on without strategic equity attached, or AI start-ups raising at higher valuations from financial rather than strategic investors | Reports questioning whether AI revenue is real or circular, write-downs on strategic stakes, cancelled or renegotiated AI partnerships, layoffs in AI divisions, or AI start-ups raising at lower valuations or struggling to raise funds |

How to read the signals together

No single indicator will tell us whether the AI rally is ending.

What matters is whether the signals move together.

If AI revenue continues to broaden, Nvidia demand remains strong, big technology companies keep raising capex, and AI deals become less dependent on circular funding, the rally could still have further to run.

But if several signals turn at the same time, investors should become more cautious.

For example, if AI revenue slows, chip demand weakens, capex guidance is cut, and more deals rely on strategic financing, it may suggest that expectations have run too far ahead.

For long-term investors, the goal is not to call the exact peak.

It is to recognise when the risk-reward has changed, manage position sizes, and avoid becoming too concentrated in the most expensive AI-related stocks.

What would Beansprout do?

I would not describe the entire AI boom as just a bubble.

The technology is real, revenue is already being generated, and the infrastructure being built may support economic activity for many years.

At the same time, I would not assume that every AI-linked stock is attractive at today's price.

The more a stock depends on years of strong growth, high margins and uninterrupted AI spending, the less room there is for disappointment.

That is why I would keep three principles in mind.

First, separate the technology from the trade. Believing in AI does not mean every AI-linked stock is attractive at any price. I would always ask what growth expectations are already priced in.

Second, diversify across the AI value chain. Today’s obvious winner may not always remain the winner in the next phase of the cycle. Instead of concentrating everything in one stock, I would look at exposure across chips, cloud platforms, software, infrastructure and broader index funds.

Third, expect volatility. Even if the long-term AI story remains intact, sharp drawdowns of 30% to 50% are possible when expectations are high. For patient investors, market weakness may be a chance to add selectively, rather than a reason to panic.

In other words, I would not avoid AI completely.

But I would avoid chasing the rally blindly. The goal is to participate in the long-term growth of AI, while making sure the portfolio can still withstand a correction if the hype cools.

If I already have broad exposure through the S&P 500, Nasdaq 100 or global equity ETFs, I would first check how much AI exposure I already own before adding more.

If my exposure has become too large because a few AI stocks have run up sharply, I would consider rebalancing rather than letting one theme dominate the portfolio.

For new money, I would prefer a gradual approach.

Broad equity exposure can sit within the Growth Pot, while higher-conviction AI names can be sized within the Opportunity Pot so that I can participate without taking excessive concentration risk.

The honest answer is that AI may be both a real revolution and a market cycle with pockets of excess.

For investors, the goal is not to win the debate on whether AI is a bubble. It is to build a portfolio that can benefit if AI keeps compounding, while still surviving if the excitement cools.

For a broader framework, you can read more about how we build a portfolio across the four pots of wealth through different market cycles here.

Are you increasing your exposure to AI stocks, or trimming after the rally? Share your thoughts in the comments below or join the discussion in our Beansprout Telegram community.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments