ASEAN's gig economy: More than a side hustle

Stocks

Powered by

By Gerald Wong, CFA • 25 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

ASEAN's gig economy is changing how millions work and how goods move across the region. Discover the labour, logistics and infrastructure trends, and the investment opportunities they create.

When most people think about ASEAN’s gig economy, they think of ride-hailing drivers or food delivery riders.

That is part of the picture, but not the full story.

Across Southeast Asia, gig work has become a structural part of the economy, supporting millions of workers and helping cities function more efficiently.

In many markets, informal or platform-based work is not just a side hustle, but a main source of income.

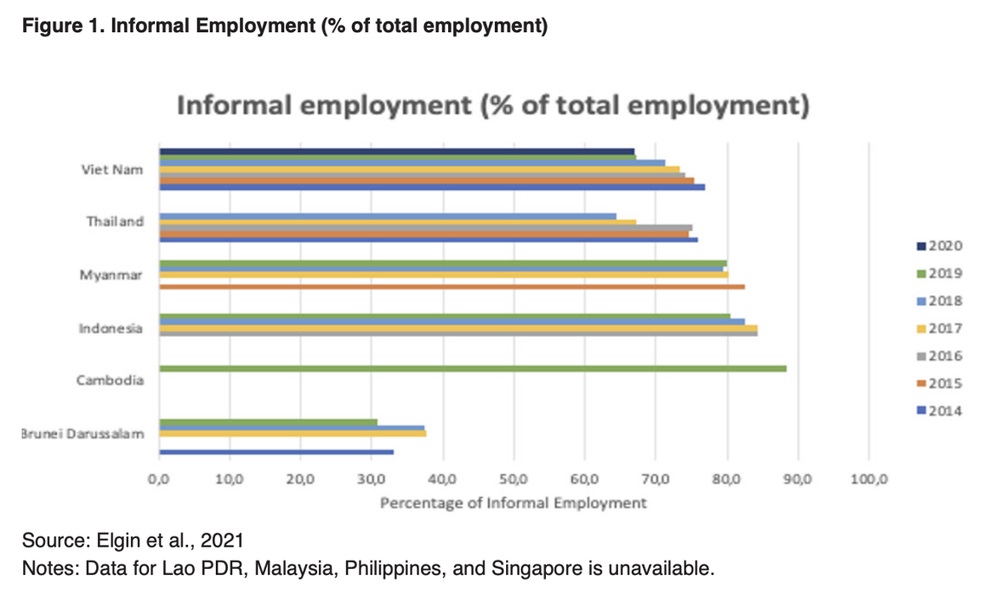

With the share of informal employment being one of the highest in Asia-Pacific1, the gig economy is no longer an investment story about which platform wins.

It is a broader long-term theme tied to urbanisation, improving digital infrastructure, and the gradual formalisation of these platforms in the region.

In this article, we look at what is driving ASEAN’s gig economy, how the landscape is evolving, and where investors can gain exposure to this theme.

Why is ASEAN built for gig economy growth?

ASEAN has a unique mix of demographics, economic structure, and infrastructure that makes platform-based work increasingly necessary.

1. A young, mobile-first population

Nearly half of ASEAN’s population was under 30 in 2024 (ASEAN Statistical Highlights 2025), creating a large pool of digitally savvy workers.

In key markets such as Vietnam, the Philippines and Indonesia, young people make up a meaningful share of the population, and many have grown up using smartphones as their main gateway to work, payments and services.

This has made younger workers more open to gig work, more comfortable managing multiple income streams, and more reliant on digital platforms to find jobs.

With internet penetration across Southeast Asia already above 80% (Kearney for Asia Tech x Singapore, 2022), the infrastructure to support this shift is largely in place.

The result is a large, young, and mobile-first workforce that is increasingly seeking flexible ways to earn, and that gig platforms can reach at scale.

2. High levels of informal employment

Despite ASEAN’s large and growing workforce, formal job creation has not kept pace. This has made gig work less a matter of choice, and more a necessity for many workers.

According to the International Labour Organization, more than 16 percent of youth across Southeast Asia were not in education, employment, or training in 2024.

For many of them, gig platforms help fill this gap by offering a flexible and accessible way to earn income without requiring formal qualifications, prior work experience, or even a bank account.

This matters in a region where informal employment remains deeply entrenched.

In countries such as Cambodia, Indonesia and Thailand, informal work accounts for more than 80 per cent of total employment. (ASEAN Socio-Cultural Community Trend Report No. 19, 2025).

In Indonesia alone, 59 per cent of the country’s 144 million workers are engaged in informal activities (United Nations Development Programme).

Against this backdrop, gig platforms have become more than just job-matching apps.

They are increasingly acting as organisers of informal work, offering workers greater structure, better income visibility, and in some cases access to financial services that were previously out of reach.

3. Congested cities and underdeveloped infrastructure

Urbanisation is also changing where people live and how they earn.

More than half of ASEAN's population lived in cities in 2024, and as more young workers move into urban centres, they enter places where platform-based work is both easier to access and more in demand. (ASEAN Statistical Highlights, 2025).

At the same time, many of these cities face severe traffic congestion.

In places like Jakarta and Manila, this has made fast and flexible delivery services more essential.

When short trips can take a long time by car, on-demand motorcycle delivery becomes a practical solution for both consumers and businesses.

This has helped platforms such as GoTo play a bigger role in solving last-mile logistics challenges that existing infrastructure could not fully address.

As urbanisation continues across the region, demand for platform-based delivery and on-demand services is likely to keep rising.

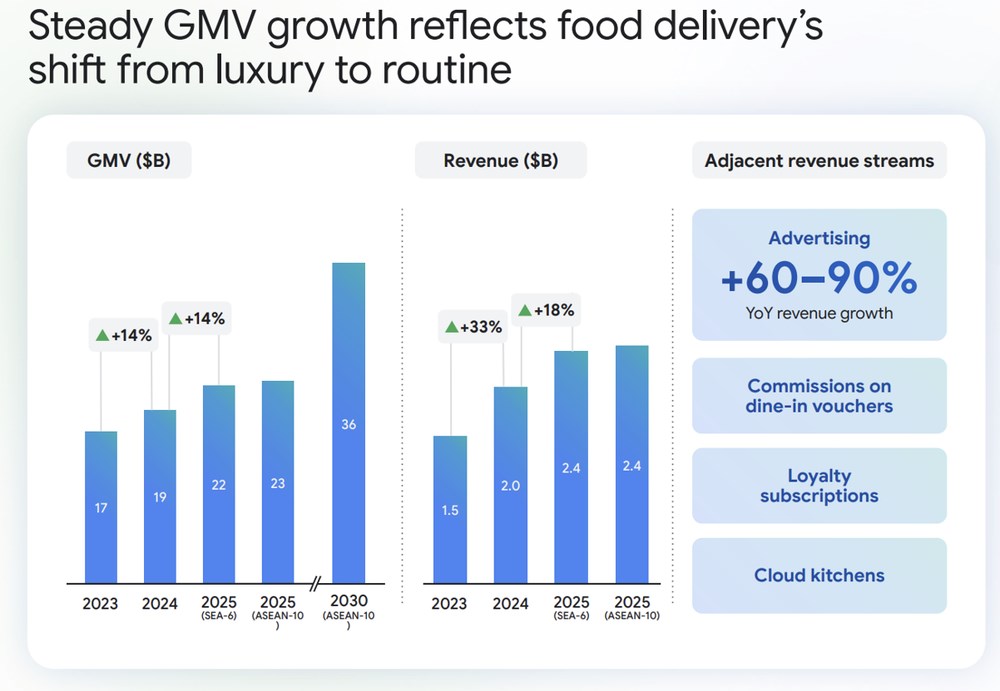

Southeast Asia's food delivery gross merchandise value (GMV) grew from US$17 billion in 2023 to US$23 billion in 2025, with the broader ASEAN-10 market projected to reach US$36 billion by 2030, as platforms move beyond delivery volumes into adjacent revenue streams.

As urbanisation continues, with countries like Indonesia projected to be 70 percent urbanised by 2045 (World Bank), the structural demand for platform-mediated logistics and on-demand services is likely to deepen.

4. A fast-growing digital economy

The digital economy that supports gig work has also expanded rapidly.

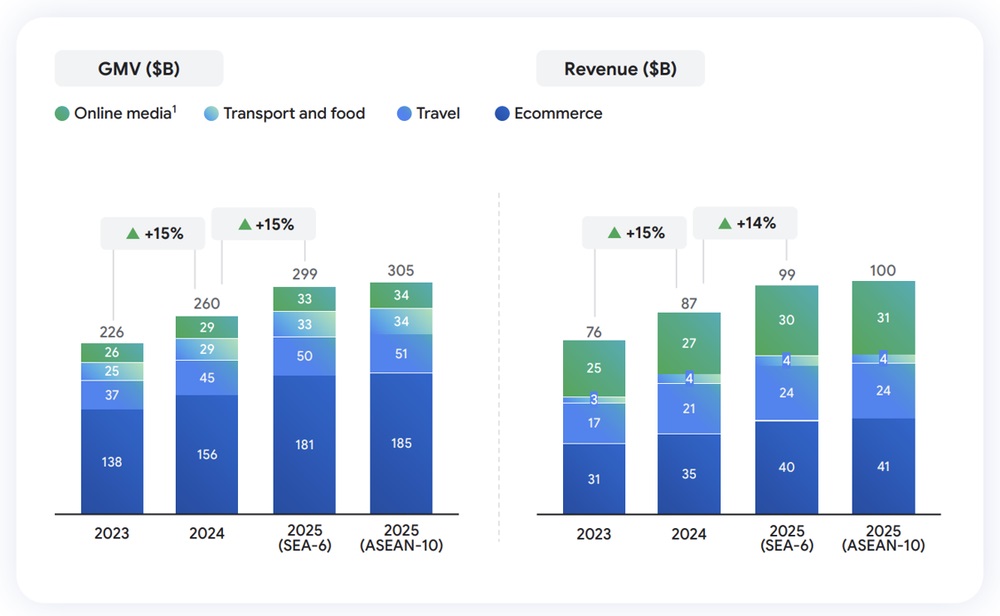

Across Southeast Asia, digital economy GMV exceeded US$300 billion in 2025, up sharply from about US$40 billion a decade earlier. (Google, Temasek, and Bain & Company, e-Conomy SEA 2025).

That growth rate, 17 percent annually, outpaces that of the United States, Europe, and China.

This reflects not just stronger online consumption, but also the buildout of the digital infrastructure that gig platforms rely on, including payments systems, logistics networks, cloud services and mobile connectivity.

This is a reminder that the gig economy does not operate in isolation. It sits on top of a broader digital ecosystem that is still growing and, in many areas, is still at an early stage of monetisation.

Source: Google, Temasek, and Bain & Company e-Conomy SEA 2025

What role does the gig economy play in ASEAN?

To understand the investment case, it helps to look beyond the platforms themselves.

In ASEAN, the gig economy plays three important roles in the broader economy, and each creates a different set of opportunities for investors.

1. Logistics backbone

In many parts of Southeast Asia, logistics infrastructure is still catching up with the needs of a fast growing digital economy.

Warehousing networks remain uneven, last mile delivery can be unreliable, and traditional courier services are often not built for the speed and flexibility that e-commerce requires.

As a result, ride-hailing and delivery platforms powered by millions of gig workers have become an important part of the region’s logistics backbone.

This means the opportunity is not limited to platform companies.

The fulfilment centres, cold chain networks and cross-border logistics hubs that support this ecosystem are also becoming increasingly important and investable.

2. Labour absorption mechanism

ASEAN’s formal labour market has not expanded fast enough to absorb its young and growing workforce, and gig work has helped fill that gap by providing income opportunities to millions who might otherwise be unemployed or underemployed.

At the same time, the gig economy is no longer limited to ride hailing and food delivery.

In markets such as the Philippines, more workers are using digital platforms to offer services like graphic design, software development, virtual assistance and data work to clients around the world.

As the platform economy expands into higher value segments such as freelance services, digital advertising and skilled remote work, the investment opportunity becomes broader than just transport and delivery.

3. Financial inclusion engine

The gig economy is also helping to bring more workers into the formal financial system.

Each time a gig worker completes a delivery, drives a passenger or finishes a freelance job through a platform, they leave behind a digital record of income.

That matters because many informal workers have traditionally lacked the documents or credit history that banks require.

Platforms such as GoTo have used this transaction data to offer services like micro loans, insurance and savings tools to workers who may not have had access to conventional banking products before.

In a region where nearly 70 percent of Southeast Asia's adult population remain unbanked or underbanked (Bain & Company), gig platforms are becoming an important channel for expanding financial inclusion.

A turning point for platform regulation

For much of the past decade, gig platforms in ASEAN operated in a regulatory grey zone. Workers were generally treated as independent contractors rather than employees, allowing platforms to scale quickly but with limited protections for workers.

That is now starting to change.

As gig work becomes a more established part of the economy, governments across the region have begun putting clearer rules in place.

Singapore has taken the lead with the Platform Workers Act, which requires CPF contributions and work injury compensation.

Malaysia has also moved in a similar direction with the Gig Workers Act 2025, mandating contributions to the Social Security Organisation (Socso) and the Employees Provident Fund (EPF) for platform workers.

The Act also broadens the legal definition of gig work beyond ride-hailing and delivery, bringing a wider range of platform-based occupations under its scope.

Other markets such as Indonesia, the Philippines, Vietnam and Thailand are still at earlier stages, although momentum is building and Indonesia could be the next key market to watch.

For platforms, tighter regulation is likely to raise costs in the near term.

But over time, it could also strengthen larger incumbents. Higher compliance costs may make it harder for smaller players to compete, which could support consolidation and benefit scaled platforms such as GoTo.

For long-term investors, the regulatory shift is worth monitoring closely, as it may increasingly separate the companies that can adapt and endure from those that cannot.

Where are the investment opportunities?

Each ASEAN market differs in platform development, regulatory maturity, and workforce composition. The opportunity for investors lies in understanding where value accrues across platforms, infrastructure, and digital services.

Singapore: regional command centre

Singapore hosts the region’s key platforms and the most developed regulatory framework.

ComfortDelGro (SGX: C52) offers some gig economy exposure in Singapore through its Zig ride-hailing platform, which operates within the country’s formal platform-worker framework.

Mapletree Logistics Trust (SGX: M44U) offers exposure to the physical infrastructure behind ASEAN’s gig economy through its portfolio of warehouses and fulfilment centres across the region.

Indonesia: the scale story

Indonesia is the largest gig economy market in Southeast Asia, supported by its large population and sizeable informal workforce.

GoTo Group (IDX: GOTO) is the clearest listed proxy for this theme in Indonesia. Through Gojek, it has a leading position in ride-hailing and food delivery across the country’s major cities, while Tokopedia gives it meaningful exposure to e-commerce as well.

Malaysia: regulation and consolidation

Malaysia stands out for its mix of clearer regulation and rising demand for logistics.

TIME dotCom (KLSE:TIMECOM) specialises in domestic and international connectivity, data centre, cloud and managed services solutions for retail, enterprise and wholesale markets.

It operates a fully-fiberised nationwide network anchored by the Cross Peninsular Cable System (CPCS™).

The company also has stakes in international submarine cable systems, including UNITY, Asia Pacific Gateway (APG), Asia-Africa-Europe-1 (AAE-1) and FASTER, enabling connectivity between Asia and global markets, while offering borderless cloud services through its carrier-neutral data centres to support regional connectivity needs.

TIME dotcom is a member of Bursa Malaysia Quality 50 Index.

Philippines: the freelance and knowledge-gig hub

The Philippines stands out within ASEAN’s gig economy for its strong role in freelance and digital work, adding a different dimension to the investment case.

Globe Telecom (PSE: GLO) offers exposure through GCash, which sits at the intersection of connectivity and financial inclusion in the Philippines. With more than 94 million registered users, GCash has become an important digital wallet and payments platform, while also expanding into lending and insurance for workers who have traditionally been underserved by formal banking.

Vietnam: a consolidating market

Vietnam's gig economy has undergone significant consolidation over the past two years.

For investors, this consolidation reduces the subsidy-driven competition that depressed margins across the sector and creates a clearer landscape of investable names.

GrabFood and ShopeeFood now dominate food delivery, while Ahamove has emerged as a significant player in last-mile logistics for businesses.

FPT Corporation (HOSE: FPT) offers a different angle on Vietnam’s gig economy. As the country’s largest technology and IT services company, it provides the digital backbone through software development, IT outsourcing and AI services that supports Vietnam’s growing role in the global tech supply chain.

FPT gives investors exposure not just to platform work, but to the higher-value freelance and contract-based digital work that is becoming a bigger part of the region’s gig economy.

Thailand: tourism, logistics, and a market to watch

While ride-hailing and food delivery are present and growing, Thailand's platform economy is more closely intertwined with its tourism industry than any other market in ASEAN.

CP All (SET: CPALL) offers indirect but meaningful exposure. Its network of nearly 16,000 7-Eleven stores increasingly serves as a logistics and fulfilment infrastructure layer, which is a physical last-mile network that platform-based commerce depends on for cash payments, parcel collection, and order fulfilment.

Singapore-based investors can access CP All through its Singapore Depository Receipt (SGX: TCPD).

What risks should investors consider?

While the long term case for ASEAN’s gig economy is compelling, there are still several risks investors should keep in mind.

1. Profitability remains uncertain

Many of the region’s major platform companies have improved their adjusted EBITDA, but consistent net profitability remains less certain.

Much of the industry’s early growth was supported by subsidies, discounts and aggressive pricing.

The key question now is whether platforms can keep growing as they reduce these incentives.

2. Regulation could raise costs

Singapore and Malaysia have already introduced clearer rules for platform workers, and other ASEAN markets may eventually follow.

While this could strengthen the industry over time, it may also increase labour and compliance costs in the near term.

Indonesia is likely the most important market to watch given the size of its gig workforce.

3. Not every platform will survive

The recent consolidation seen in markets such as Vietnam is a reminder that platform exits can still happen.

Competitive pressure, weaker funding conditions or strategic shifts by parent companies could force smaller or less well-capitalised players to scale back or leave the market.

4. Currency movements can affect returns

Investing across ASEAN also means taking on exposure to multiple regional currencies. Even if a company performs well operationally, returns for Singapore based investors can be affected if local currencies weaken against the Singapore dollar or US dollar.

Putting the ASEAN gig economy in perspective

For investors looking at ASEAN’s gig economy, we would avoid treating it as a narrow bet on ride-hailing or food delivery alone.

Instead, we would view it as a broader structural theme tied to three long-term trends: the digitalisation of work, the buildout of logistics and fulfilment infrastructure, and the expansion of financial services to underserved workers and merchants.

That means taking a diversified approach to exposure.

ComfortDelGro can offer one angle through its Zig ride-hailing platform and point-to-point transport business, while infrastructure names such as Mapletree Logistics Trust, and digital finance or services players such as Globe Telecom and FPT, offer other ways to gain exposure to the same broader theme.

We would also look across markets rather than focus on just one country. Singapore offers access to listed transport and infrastructure names, Indonesia provides scale, the Philippines adds exposure to freelance and financial inclusion trends, while Vietnam and Malaysia offer more specialised angles through technology and logistics.

Overall, we think the most resilient way to invest in ASEAN’s gig economy is to spread exposure across platforms, infrastructure and digital services, rather than try to pick a single winner.

1Source: International Labour Organization (ILO), 2023. “Women and men in the informal economy: A statistical update”.

About ASEAN Exchanges

ASEAN Exchanges is a collaboration among the exchanges in the ASEAN countries with the objectives of promoting greater integration of the ASEAN capital markets, enhancing the visibility of ASEAN as an asset class, and strengthening ASEAN as an attractive investment destination for both ASEAN and global investors.

Current participating ASEAN exchanges (“Member Exchanges”) are Bursa Malaysia Berhad, Indonesia Stock Exchange, The Philippine Stock Exchange, Singapore Exchange, The Stock Exchange of Thailand, and Vietnam Exchange.

More information about ASEAN Exchanges can be found here.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments