How much CPF savings do you need to get $5,000 a month from CPF LIFE

Retirement

By Gerald Wong, CFA • 28 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Find out how much CPF savings may be needed for $5,000 monthly retirement income from CPF LIFE, and how CPF top-ups and payout deferment may help.

What happened?

I came across an interesting discussion on CPF LIFE retirement payouts recently.

After we shared about how you can find out if your CPF savings are enough for retirement, there was a news report of a retiree receiving about S$4,600 a month from CPF LIFE,

For those who are not familiar, CPF LIFE is the foundation of our retirement income as it provides monthly payouts for as long as we live.

Then, I saw a question in the Beansprout community about “How much CPF savings would we need to receive S$5,000 a month from CPF LIFE?”

In this article, I’ll look at how CPF LIFE payouts work, how much may be needed in the CPF Retirement Account, and the other key considerations before aiming for a S$5,000 monthly payout.

CPF LIFE for retirement income

CPF LIFE stands for CPF Lifelong Income for the Elderly.

It is Singapore’s national longevity insurance annuity scheme that provides monthly payouts for as long as we live.

This is why CPF LIFE can play an important role in retirement planning.

Unlike a fixed pool of savings that can be drawn down over time, CPF LIFE is designed to provide income for life.

However, the monthly payout is not the same for everyone.

It depends on factors such as how much CPF savings we have, when we start our payouts, and which CPF LIFE plan we choose.

For most Singaporeans, the key starting point is the CPF Retirement Account.

CPF Retirement Account savings determine your CPF LIFE payout

When we turn 55, savings from our Special Account (SA), followed by our Ordinary Account (OA), are transferred to a newly opened CPF Retirement Account (RA).

The amount transferred is capped at the Full Retirement Sum (FRS), unless we choose to top up further to the Enhanced Retirement Sum (ERS) for higher payouts.

The amount in the Retirement Account will then help determine our future monthly payouts.

Learn more about the CPF retirement sums here and CPF LIFE payout here.

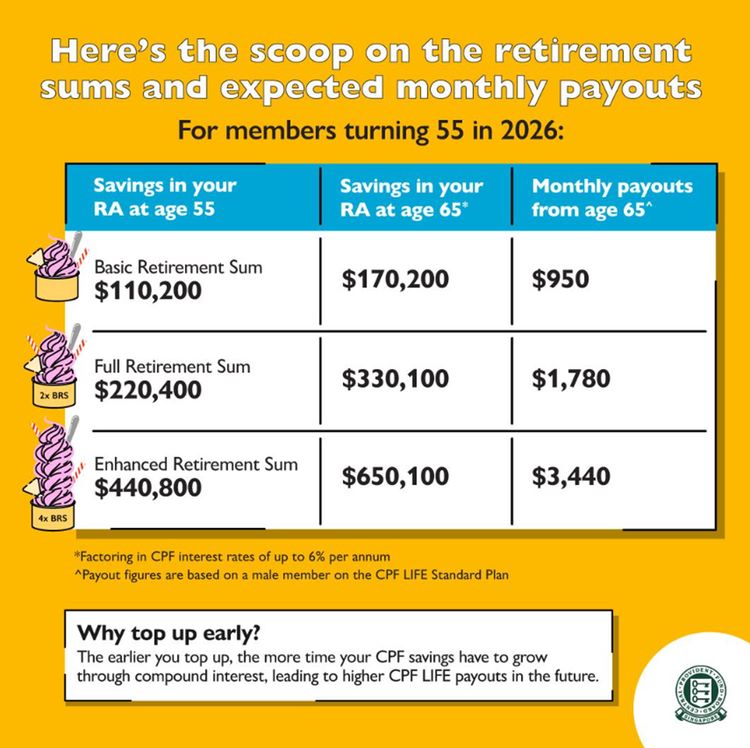

For members who turn 55 in 2026, CPF provides the following payout estimates. This gives us a useful starting point.

For someone turning 55 in 2026, setting aside or topping up to the Full Retirement Sum of S$220,400 may provide about S$1,780 a month from age 65 under the CPF LIFE Standard Plan.

For someone turning 55 in 2026, setting aside or topping up to the Enhanced Retirement Sum of S$440,800 may provide about S$3,440 a month from age 65 under the CPF LIFE Standard Plan.

| CPF retirement sum in 2026 | Amount in Retirement Account (RA) at age 55 | Estimated monthly payout from age 65 |

| Basic Retirement Sum (BRS) | S$110,200 | S$950 |

| Full Retirement Sum (FRS) | S$220,400 | S$1,780 |

| Enhanced Retirement Sum (ERS) | S$440,800 | S$3,440 |

| Source: CPF Board. Estimates are for members who turn 55 in 2026 and set aside or top up the respective amounts, based on the CPF LIFE Standard Plan and CPF interest rate of 4%. | ||

How much do we need to generate S$5,000 in CPF LIFE payouts per month?

As we saw earlier, CPF estimates that setting aside the Enhanced Retirement Sum of S$440,800 may provide about S$3,440 a month from age 65 for members turning 55 in 2026, under the CPF LIFE Standard Plan.

If we assume the Retirement Account balance grows at CPF’s 4% interest rate over 10 years, S$440,800 would grow to about S$653,000 by age 65 before CPF LIFE payouts begin.

To get to a CPF LIFE payout of S$5,000 per month at the age of 65, we would need about S$640,000 of CPF Retirement Account balance at the age of 55, which may then grow to about S$950,000 of savings at the age of 65, factoring in CPF interest rates of up to 6% per annum.

How to get higher CPF Life payouts

For those who are looking to grow their CPF Life payouts, there are two main ways to do so - CPF Retirement Account top-ups and payout deferment.

| Lever | How it works | What to note |

| Top up CPF Retirement Account | Add more savings up to the prevailing Enhanced Retirement Sum | Top-ups are irreversible and reserved for retirement payouts |

| Defer CPF LIFE payouts | Start CPF LIFE payouts later, up to age 70 | Monthly payouts may be higher, but there is no CPF LIFE income during the deferment period |

#1 - Top up the CPF Retirement Account

According to CPF, Members aged 55 and above can top up their Retirement Account up to the current year’s Enhanced Retirement Sum.

As the Enhanced Retirement Sum increases every January, members may be able to make further top-ups each year.

However, it is worth noting that CPF Retirement Account top-ups are irreversible and cannot be withdrawn for other purposes.

Learn more about how you can grow your CPF savings here.

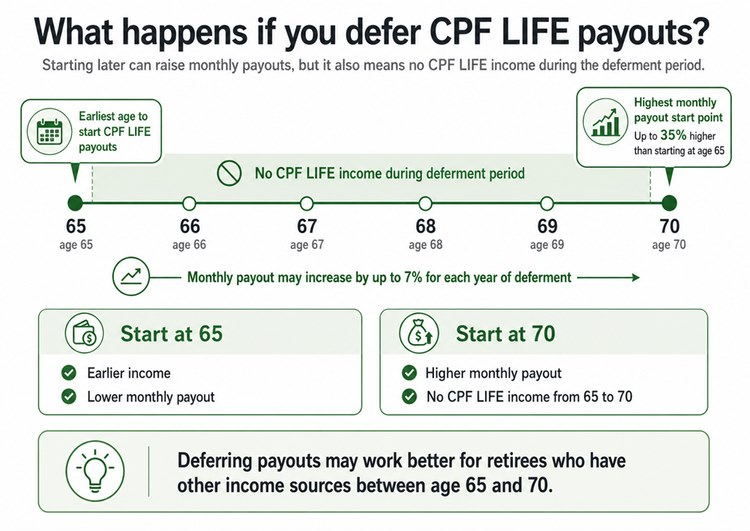

#2 - Delay CPF LIFE payouts

CPF LIFE payouts can start from age 65. However, members can choose to defer receiving payouts up to age 70.

According to CPF, the monthly payouts can increase by up to 7% for each year of deferment, or up to 35% if payouts are deferred to age 70.

The amount needed may be lower if CPF LIFE payouts are deferred.

According to CPF, payouts can increase by up to 35% if they are deferred to age 70.

Taking this deferment effect into account, a CPF member may need closer to S$700,000 in the CPF Retirement Account by age 65 to approach a S$5,000 monthly payout from age 70.

| Scenario | Beansprout estimate |

| Estimated monthly payout from 2026 Enhanced Retirement Sum | About S$3,440/month from age 65 |

| Estimated CPF Retirement Account balance needed for about S$5,000/month from age 65 | Around S$950,000 by age 65 |

| Estimated CPF Retirement Account balance needed for about S$5,000/month from age 70 | Around S$700,000 by age 65 |

| Target payout | S$5,000/month |

Once again, this is not meant to be a precise CPF LIFE calculation.

The actual payout will depend on factors such as the CPF LIFE plan selected, payout start age, gender, age and CPF Board’s prevailing assumptions at the time.

Still, it gives us a useful guide.

Delaying CPF LIFE payouts may also work better for retirees who have other income sources between age 65 and 70.

This could include employment income, rental income, dividends, Singapore Savings Bonds, T-bills or fixed deposits.

What else to consider when deciding your CPF Life payouts?

The amount in the CPF Retirement Account is not the only factor that affects CPF LIFE payouts.

The CPF LIFE plan also matters.

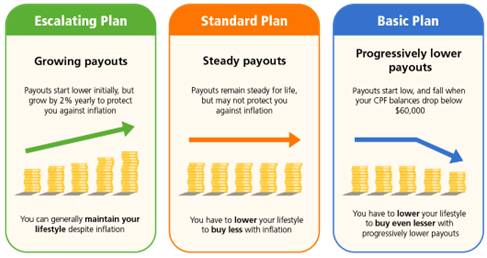

CPF LIFE currently offers three plans: Standard Plan, Escalating Plan and Basic Plan. Each plan structures retirement income differently.

The Standard Plan is the most relevant plan if the goal is to maximise the starting monthly payout.

However, the Standard Plan payouts do not grow, which means they do not protect against inflation.

This makes the Standard Plan more useful for someone who wants a higher starting payout. However, the monthly income does not increase.

The Escalating Plan works differently.

Monthly payouts start lower, but grow by 2% each year for life. This helps protect purchasing power against inflation over time.

This means the Escalating Plan may be less useful for someone trying to hit S$5,000 a month at the start of retirement.

However, it may be worth comparing for retirees who are more worried about rising living costs over a long retirement.

The Basic Plan provides progressively lower payouts.

The monthly payouts under the Basic Plan start lower and fall when CPF balances fall below S$60,000.

This makes the Basic Plan less relevant if the main goal is to maximise monthly retirement income from CPF LIFE.

The key point is that a S$5,000 CPF LIFE payout is not just about the amount in CPF.

It also depends on whether we want a higher starting income, income that rises over time, or a lower payout structure.

| Retirement income goal | CPF LIFE plan to compare |

| Higher starting monthly income | Standard Plan |

| Income that rises over time | Escalating Plan |

| Lower payout structure | Basic Plan |

For someone targeting S$5,000 a month, the Standard Plan may show the highest starting payout.

But for someone expecting a long retirement, the Escalating Plan may deserve a closer look because inflation can gradually reduce the value of a fixed monthly payout.

Read more about how the CPF LIFE Plan works.

What would Beansprout do?

CPF LIFE can be a useful foundation for retirement income, but I would not start by asking whether I can get S$5,000 a month from CPF LIFE.

I would start with a more practical question: what kind of retirement lifestyle do I want, and how much monthly income would I need to support it?

Based on our estimates, receiving about S$5,000 a month from CPF LIFE may require around S$950,000 in CPF LIFE savings by age 65, if payouts start at 65.

If payouts are deferred to age 70, the amount needed by age 65 may be closer to S$700,000.

That is a meaningful amount, and may be more than what many members will have in their CPF Retirement Account.

For context, members turning 55 in 2026 who set aside the Enhanced Retirement Sum of S$440,800 may receive about S$3,440 a month from age 65 under the CPF LIFE Standard Plan. Those who set aside the Full Retirement Sum of S$220,400 may receive about S$1,780 a month.

This is why I would see CPF LIFE as one part of my retirement income plan, rather than the whole plan. If my CPF LIFE payouts can cover my basic needs, that already provides a strong safety net.

If I want a higher CPF LIFE payout, CPF top-ups may be worth considering, especially if I have strong cash flow and do not need the money before retirement. However, Retirement Account top-ups are irreversible and cannot be withdrawn for other purposes.

Deferring CPF LIFE payouts can also increase monthly payouts, but it means starting them later.

Ultimately, the goal is not just to maximise CPF LIFE payouts. It is to understand the retirement lifestyle I want, how much CPF LIFE can support, and what gap I need to fill with savings or investments outside CPF.

To understand the latest payout estimates, you can start with our guide to CPF LIFE payouts in 2026 and our explainer on the CPF Retirement Sum.

You can also learn more about how to grow your CPF savings here.

Would you aim for a S$5,000 monthly CPF LIFE payout, or keep more flexibility outside CPF for your retirement years? Share with us in the comments below or in our Telegram group!

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

2 comments

- Sam Ow • 09 May 2026 12:42 AM

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20160.45%20160.45'%20style='enable-background:new%200%200%20160.45%20160.45;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%2300DBA4;}%20%3c/style%3e%3cg%3e%3cg%3e%3cpath%20class='st0'%20d='M80.23,0C35.99,0,0,35.99,0,80.23s35.99,80.23,80.23,80.23c44.24,0,80.23-35.99,80.23-80.23S124.46,0,80.23,0%20z%20M80.23,149.37c-1.73,0-3.45-0.09-5.15-0.21l0-38.76c-1.44-31.08,14.86-34.75,32.13-38.65c5.66-1.28,11.08-2.5,15.76-4.7%20c1.78,15.32-1.66,28.48-9.68,37.18c-0.11,0.11-10.83,10.24-23.27,10.24c-1.12,0-2.26-0.08-3.4-0.26l-1.72,10.94%20c1.73,0.27,3.44,0.4,5.11,0.4c16.97,0,30.39-12.77,31.2-13.57c11.35-12.3,15.63-30.42,12.07-51.01l-2.17-12.46l-10.42,7.15%20c-3.7,2.54-9.63,3.87-15.93,5.29c-16.97,3.82-42.62,9.6-40.75,49.71v36.77c-30.32-7.32-52.92-34.67-52.92-67.21%20c0-38.13,31.02-69.15,69.15-69.15c38.13,0,69.15,31.02,69.15,69.15S118.36,149.37,80.23,149.37z'/%3e%3cpath%20class='st0'%20d='M56.13,44.13c-3.86-0.87-7.5-1.69-9.57-3.11l-9.25-6.35l-1.92,11.06c-2.41,13.89,0.52,26.16,8.48,34.77%20c0.37,0.36,7.58,7.23,17.36,8.83c0.43-1.57,0.92-3.09,1.48-4.54c0.85-2.19,1.85-4.26,3-6.21c-7.3,0.3-13.91-5.81-13.92-5.81%20c0,0,0,0,0,0c-4.44-4.81-6.53-11.78-6.09-19.96c2.57,0.91,5.31,1.52,8.01,2.13c8.98,2.02,16.94,3.83,18.8,15.11%20c0.56-0.52,1.13-1.04,1.72-1.53c2.54-2.12,5.24-3.84,8-5.27C77.55,48.96,64.62,46.04,56.13,44.13z'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Beansprout • 15 May 2026 10:37 AM

Beansprout • 15 May 2026 10:37 AM

- TAN CHI WEI • 29 Apr 2026 04:14 AM