4 SGX SDRs with exposure to energy security

Stocks, Singapore Depository Receipts

Powered by

By Ng Hui Min • 18 May 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Energy security is back in focus as oil price volatility, geopolitical risks and the global shift towards electrification drive renewed interest in EVs, batteries and clean energy exposure.

What happened?

Energy security is back in focus.

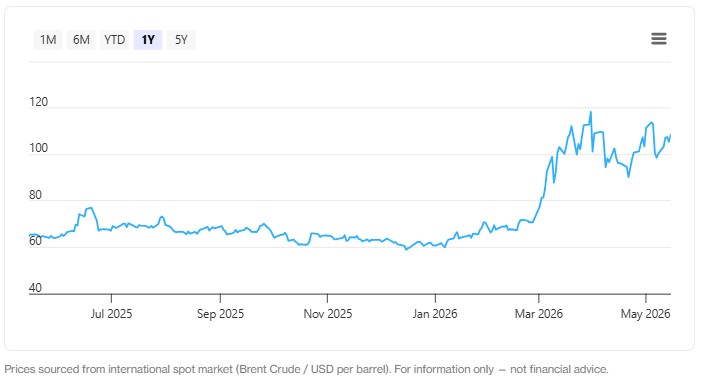

Oil prices have become more sensitive to geopolitical risks, especially with conflict in the Middle East and disruption risks around the Strait of Hormuz adding a risk premium to crude oil prices.

At the same time, trade tensions and tariffs are pushing governments to place greater emphasis on domestic clean energy, battery production and electrified transport.

This means EVs and clean energy are no longer just climate-related themes. They are increasingly part of each country’s industrial and national security strategy.

We recently highlighted energy security as one of the 3 growth themes to watch in Singapore, as electrification and energy transition may continue to remain relevant over the long term.

In this article, I look at why energy security is back in focus, the structural drivers supporting electrification, and how Singapore investors can gain exposure to the clean energy theme.

Why energy security is back in focus

The first half of 2026 has been a reminder that energy is not just an economic issue. It is also a geopolitical one.

#1 — A more volatile oil price environment

Oil prices have become more sensitive to geopolitical risks again.

Conflict in the Middle East and disruption risks around the Strait of Hormuz have added a risk premium to crude oil prices. This matters because many economies still depend heavily on imported fossil fuels.

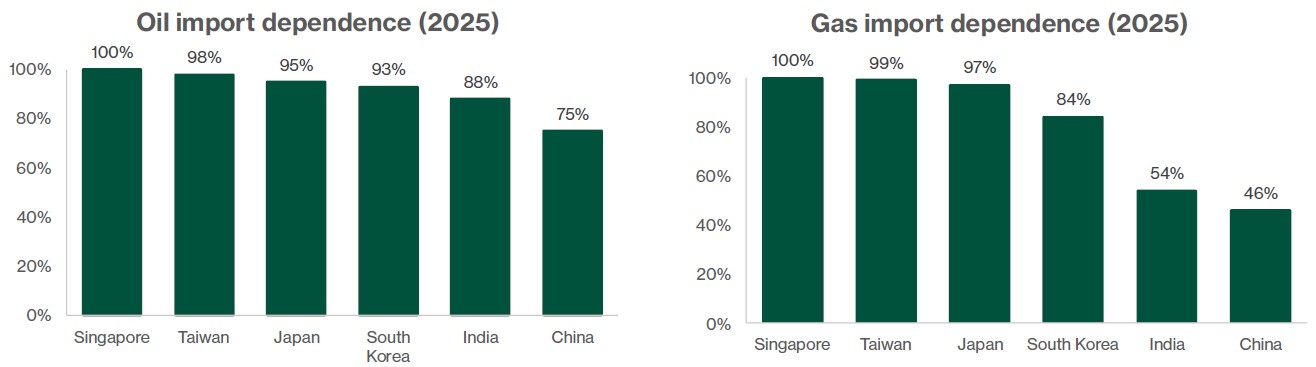

For Asian economies, the exposure is significant. China remains the world’s largest crude oil importer, while India, Japan, South Korea and much of Southeast Asia also rely heavily on imported energy.

When oil prices rise for a sustained period, the impact can show up in trade deficits, weaker currencies and higher consumer inflation.

This is different from oil-exporting economies, which may benefit from higher energy prices.

For oil-importing Asian countries, higher crude prices act more like a tax on households and businesses. This makes energy security an increasingly important policy priority.

#2 — A more protectionist trade and tariff backdrop

Trade policy is also pushing governments to think harder about energy security.

The US and Europe have imposed or maintained tariffs on Chinese EVs and batteries, while several countries are placing more restrictions on Chinese components in critical infrastructure.

The aim may differ across countries, but the effect is similar: governments want greater control over strategic supply chains.

This makes domestic clean energy, battery production and electrified transport more important from both an economic and political perspective.

This means the EV and clean-energy supply chain is no longer just about growth or climate policy. It is also becoming part of each country’s industrial and national security strategy.

#3 — Electrification is now technically and economically viable

In the past, energy security mainly meant diversifying oil suppliers or building strategic petroleum reserves.

Today, there is a more direct alternative: reduce oil demand by electrifying road transport and powering it with more renewable electricity.

This shift has become more practical because battery costs have fallen sharply. Lower battery costs have helped make EVs more affordable, especially in China, where many electric cars are now priced competitively against petrol cars.

According to International Energy Agency (20 March 2026), road transport accounts for around 45% of global oil demand and is one of the largest sources of oil demand.

Replacing petrol vehicles with EVs reduces reliance on imported oil and shifts energy consumption towards electricity that can be generated domestically through solar, wind, hydro or nuclear power.

Battery makers, automakers and electric-mobility suppliers are no longer just climate-related investments. They are increasingly part of a broader energy security and industrial strategy being adopted by many major economies.

Key tailwinds for EV and batteries

Behind the headlines, four structural drivers are working in favour of EV and battery manufacturers.

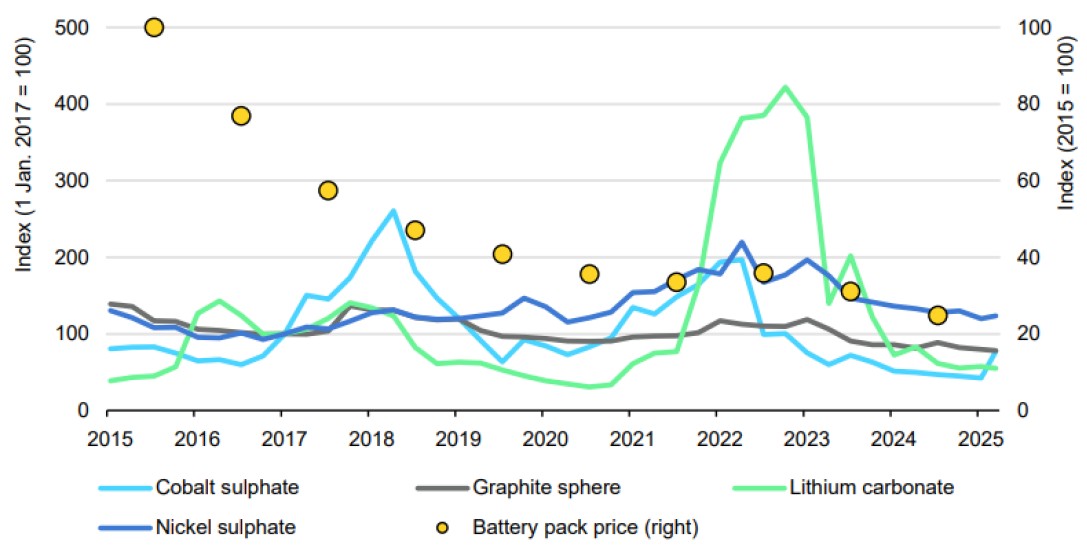

#1 — Falling battery costs are the master variable

Battery costs are one of the most important factors driving EV adoption.

Batteries are the largest cost component in an electric vehicle, so lower battery prices make EVs more affordable compared with petrol cars.

According to BloombergNEF’s 2025 survey, global lithium-ion battery pack prices fell 8% from 2024 to US$108 per kWh, while EV-specific packs stayed below US$100 per kWh for the second year. Chinese battery packs were even cheaper, at around US$84 per kWh.

Price of selected battery metals (left) and lithium-ion battery packs (right), 2015-2025

his has been helped by lower raw material prices, especially lithium carbonate, after the spike in 2022.

Manufacturing scale is another major factor. Large battery makers such as CATL have continued to expand production, helping to lower unit costs.

The shift towards lithium-iron-phosphate, or LFP, batteries has also reduced costs because they use cheaper and more widely available materials than nickel-cobalt-based batteries.

Looking ahead, sodium-ion batteries could become the next area to watch. They are still in early commercial use, but could further reduce costs for selected applications such as battery swapping, commercial vehicles and stationary energy storage.

#2 — More models mean more reasons to switch

EV adoption is not driven by price alone.

Consumers also need models that fit their needs, whether that means a low-cost city car, a family SUV, a luxury vehicle or a high-performance model.

That choice is expanding quickly. According to the IEA, there were 785 electric car models available globally in 2024, up 15% from the year before, with forecasts pointing to around 1,000 models by 2026.

This matters because EVs are no longer competing only in a narrow segment of the market. They are increasingly available across different price points and customer groups.

Chinese automakers are a good example of this.

BYD now sells models ranging from affordable city cars to premium vehicles under its Yangwang brand. Geely covers mass-market, hybrid, premium and luxury EV segments through brands such as Galaxy, Lynk & Co and Zeekr. Xiaomi has also expanded quickly from its first EV launch into performance sedans and SUVs.

Model proliferation is important because it broadens the addressable market. The more choices consumers have, the easier it becomes for EV adoption to move from early adopters to the mass market.

#3 — Emerging-market adoption is accelerating

EV growth is no longer just a China, Europe and US story.

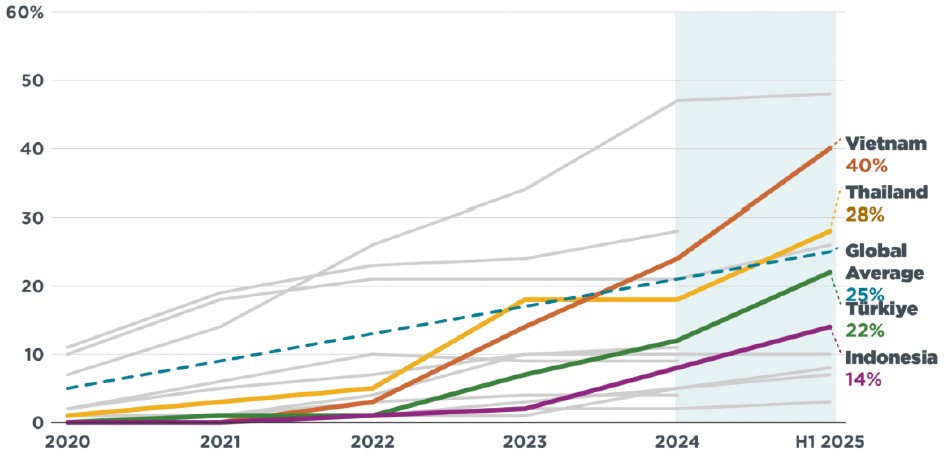

Adoption is now picking up quickly in emerging markets, including Southeast Asia and Latin America. Countries such as Vietnam, Thailand, Indonesia, Brazil and Uruguay are seeing EV penetration rise as more affordable models become available.

Emerging economies saw the fastest growth in EV sales share from 2024 to 2025, specifically Vietnam, Thailand, Turkiye, and Indonesia

Companies such as BYD, Geely and Great Wall Motor are offering lower-cost EVs while also building local manufacturing or assembly capacity in overseas markets. This helps them reduce import duties, qualify for local incentives and compete more effectively on price.

Battery makers are also following this trend, with companies such as CATL expanding production outside China.

The EV opportunity is becoming broader and more global. Emerging markets could provide the next leg of growth as affordability improves, charging infrastructure expands and governments support local EV supply chains.

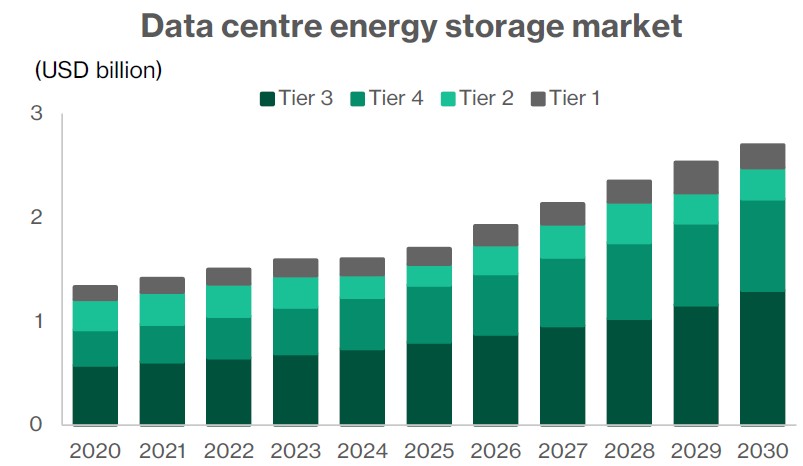

#4 — Energy storage is a parallel growth engine

EV batteries may get most of the attention, but stationary energy storage is becoming an important growth market too.

As countries add more solar and wind power, they also need batteries to store excess electricity and release it when needed. This helps make renewable energy more reliable.

This is why energy storage systems, or ESS, are growing quickly.

For battery makers, ESS can also be attractive because margins may be higher than in EV batteries, where automakers have strong bargaining power.

ESS demand is also being supported by data centres. As AI increases electricity demand, utilities and hyperscalers may need more battery storage to manage power loads and improve grid reliability.

For investors, this means battery companies are not only exposed to EV adoption. They can also benefit from the build-out of renewable energy, grid infrastructure and AI-related power demand.

Source: Grand View Research

Electrification as a long-term growth theme

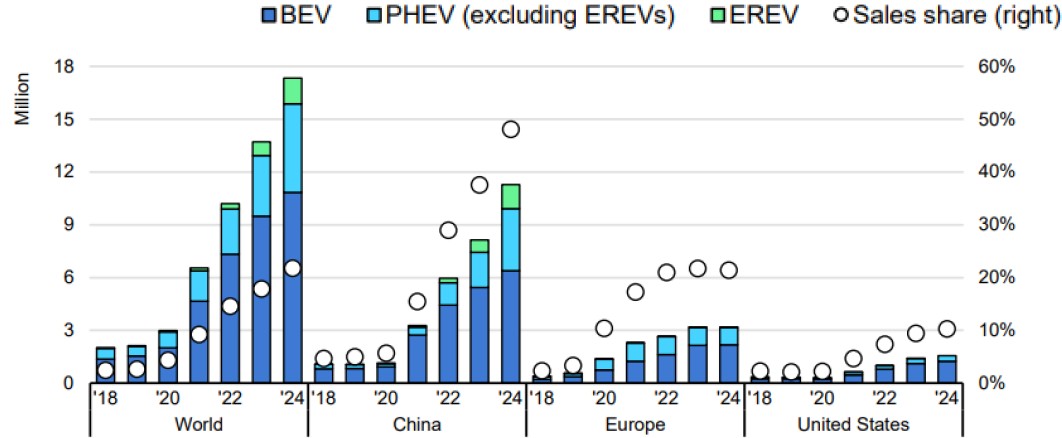

The IEA’s Global EV Outlook 2025 suggests that the EV adoption story still has room to run.

Under its Stated Policies Scenario, which reflects policies already announced rather than aspirational targets, global EV share of new car sales is expected to rise from around 25% in 2025 to more than 40% by 2030.

Electric car registrations and sales share in selected countries, 2018-2024

China is projected to remain the clear leader, with EVs reaching around 80% of new car sales by 2030. Europe is expected to reach close to 60%, supported by emissions regulation, while Southeast Asia could rise to about 25% as local manufacturing expands.

This has important implications for oil demand. Across all vehicle types, EVs could displace more than 5 million barrels of oil per day globally by 2030.

The charging ecosystem will also need to expand significantly. Public charging capacity may need to grow roughly ninefold by 2030 to support higher EV sales, creating opportunities across charging infrastructure, grid equipment and energy storage.

Importantly, the IEA estimates that EVs would still account for only around 2.5% of global electricity demand by 2030.

Share of electricity consumption from electric vehicles relative to final electricity consumption by region and scenario in the Stated Policies Scenario, 2024 and 2030

This suggests that, at least over this timeframe, grid capacity may not be the main constraint. Instead, the bigger questions are likely to be charging infrastructure, battery supply, affordability and policy support.

Long term: vehicle electrification as a wedge against fossil fuel dependence

Longer-term forecasts differ on timing, but the direction is clear.

Road transport is one of the easiest parts of fossil fuel demand to electrify, and China is likely to remain at the forefront of this shift. DNV projects that almost all new vehicles sold in China could be electric by the late 2030s, with nearly the entire vehicle fleet electrified by 2050.

This has two important implications for investors.

First, battery demand is likely to remain a multi-decade growth market, supported by both EV adoption and stationary energy storage.

Second, the companies that achieve scale this decade may build lasting advantages. These include lower manufacturing costs, stronger supply chains, vertical integration and better brand recognition in emerging markets.

In other words, electrification is not just a short-term EV sales story. It is part of a longer-term shift to reduce dependence on imported fossil fuels, with batteries and electric mobility sitting at the centre of that transition.

How Singapore investors can access the theme

Several Singapore Depositary Receipts (SDRs) listed on SGX now offer exposure to themes linked to EV adoption, batteries and energy security, including companies involved in battery manufacturing, electric vehicles and the broader clean energy supply chain.

For Singapore investors, this provides a more accessible way to participate in the global shift towards electrification and energy transition themes through the local market.

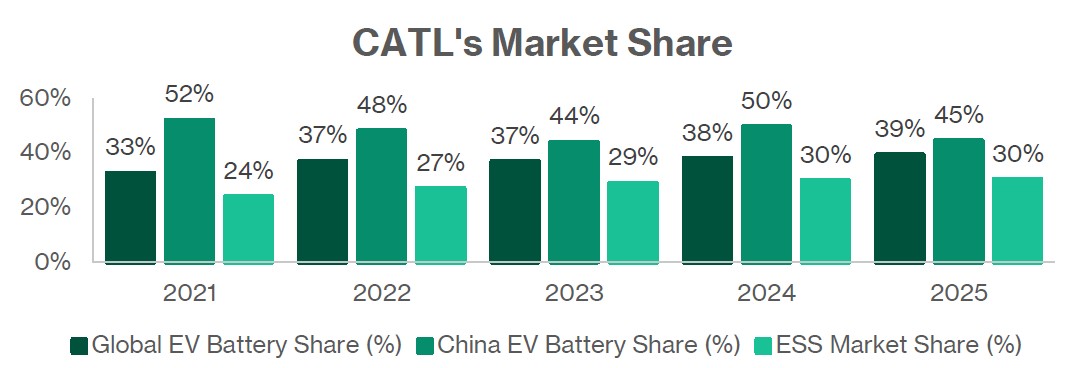

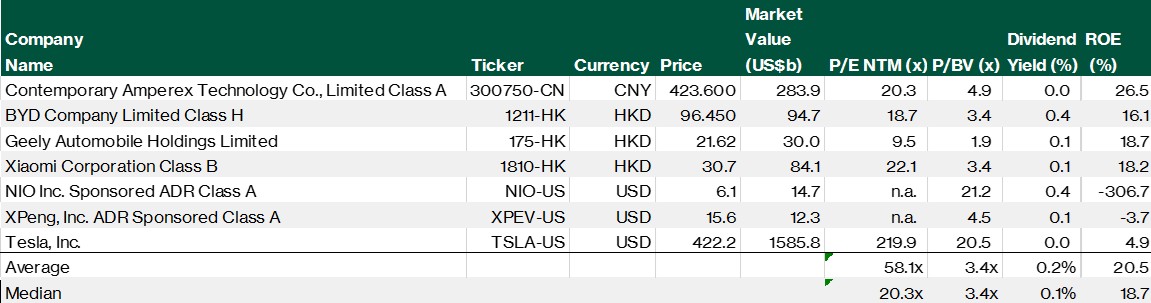

CATL (SGX: HCCD) — the supply-chain backbone

CATL is the world’s largest maker of lithium-ion batteries for electric vehicles and stationary energy storage.

It supplies many of the world’s leading automakers, including Tesla, BMW, Mercedes-Benz, Volkswagen, Stellantis, Hyundai and Honda, as well as Chinese EV makers such as Geely, Li Auto, Nio and XPeng.

FY2025 was a strong year for CATL. Revenue rose 17% to RMB 423.7 billion, while net profit increased 42% to RMB 72.2 billion. This was supported by better margins, scale efficiencies and a higher contribution from energy storage batteries.

Battery shipments reached 661 GWh, up 39% year-on-year. CATL also remained the global leader in both EV batteries and energy storage batteries, with market shares of 39.2% and 30.4% respectively.

The momentum continued into 2026, with 1Q26 revenue rising 52% to RMB 129.1 billion and net profit increasing 49% to RMB 20.7 billion.

Among the four SDRs, CATL offers the clearest exposure to the energy security theme. Its batteries support both EV adoption, which reduces oil demand, and energy storage, which helps renewables replace imported fossil fuels.

It is also less directly exposed to China’s EV price war than automakers, since it supplies batteries to many different car companies rather than relying on one brand.

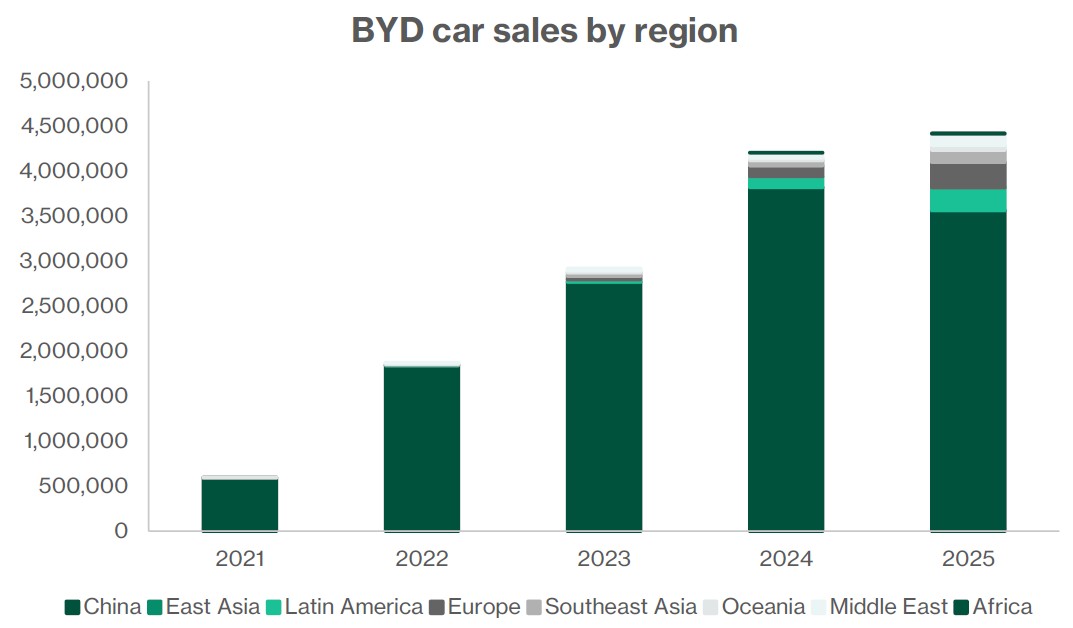

BYD (SGX: HYDD) — the global volume leader

BYD is the world’s largest producer of new energy vehicles, covering both battery-electric vehicles and plug-in hybrids.

It is also highly vertically integrated. Beyond making cars, BYD produces its own batteries, electric motors, motor controllers, automotive semiconductors and charging infrastructure.

FY2025 revenue rose 3.5% to a record RMB 804 billion, while new energy vehicle sales reached 4.60 million units. Pure EV deliveries of about 2.26 million units surpassed Tesla’s 1.64 million, making BYD the global leader in pure EV volume for the year.

However, profitability came under pressure. Net profit fell 19% to RMB 32.6 billion, as China’s intense EV price competition squeezed margins. Auto gross margin declined to 20.5% from 22.3%.

The bright spot was overseas growth. BYD’s exports surged 145% to more than 1.05 million units, with overseas margins meaningfully higher than domestic margins.

Management is targeting 1.3 million overseas units in 2026, supported by new local plants in markets such as Brazil, Hungary, Thailand, Indonesia, Uzbekistan and Mexico.

BYD is one of the clearest ways to gain exposure to Chinese EVs expanding globally, especially in emerging markets.

The key risk is margin pressure from China’s domestic price war, but its overseas growth, vertical integration and large R&D spending remain important competitive strengths.

Geely Automobile (SGX: HGMD) — the steady compounder

Geely Automobile is one of China’s largest privately controlled automakers.

The group operates across mass-market petrol cars, hybrids and electric vehicles through brands such as Geely Auto, Galaxy, Lynk & Co and Zeekr.

FY2025 was a record year for Geely. Revenue rose 25% to RMB 345.2 billion, while total vehicle sales crossed three million units for the first time.

New energy vehicle sales grew even faster, rising 90% year-on-year to 1.68 million units. This means NEVs now account for more than half of Geely’s total deliveries.

Geely Galaxy was a key growth driver, with sales up 150% to 1.24 million units.

Profitability was also resilient despite intense competition in China’s auto market. Core net profit rose 36% to RMB 14.41 billion, while gross margin improved to 16.6%.

Geely also has a broad international footprint, exporting 420,000 vehicles across 88 countries. Its 2026 target is 3.45 million units, including 2.22 million NEVs.

From an energy-security perspective, Geely offers exposure to the global adoption of Chinese EVs and hybrids, especially as the group expands overseas and builds local production in markets such as Egypt and Indonesia.

Xiaomi (SGX: HXXD) — the new entrant who is no longer new

Xiaomi is best known as a major global smartphone brand, but its EV business has quickly become one of its most important growth drivers.

The company launched its first EV, the SU7 sedan, in March 2024. It has since expanded its lineup with the SU7 Ultra, the YU7 SUV and a next-generation SU7 launched in March 2026.

FY2025 was a strong year for the group. Revenue rose 25% to RMB 457.3 billion, while adjusted net profit increased 44% to RMB 39.2 billion.

The standout was Xiaomi’s EV and new initiatives segment. Revenue from “Smart EV, AI and Other New Initiatives” rose 224% to RMB 106 billion, while the segment turned profitable for the first time with operating profit of RMB 900 million.

EV deliveries reached 411,082 vehicles, ahead of Xiaomi’s revised target of 350,000 units. The EV segment also delivered a gross margin of 24.3%, which compares well against several pure-play Chinese EV peers.

Unlike the other EV names, Xiaomi also has large and profitable non-EV businesses in smartphones and IoT products.

This gives the company cash flow to fund its EV expansion and reduces its reliance on the EV market alone.

The trade-off is that Xiaomi trades more like a broader technology platform, not just an EV company. Investors also need to watch risks such as smartphone competition and memory chip costs, which can affect earnings outside the EV business.

Valuations reflect different business models and growth profiles

Geely Automobile is the lowest-valued among the group, while BYD trades at a premium due to its scale and overseas growth, CATL commands a higher multiple for its battery leadership, and Xiaomi trades at the highest valuation due to its faster growth and broader technology ecosystem.

Key risks

Key risks include China’s EV price war, trade and tariff escalation, commodity price volatility, weaker Chinese consumer demand, and a possible easing of oil prices that could reduce near-term interest in the energy-security theme.

Download the full report here.

Check out Beansprout's guide to the best stock trading platforms in Singapore with the latest promotions to invest in Singapore Depositary Receipts.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Beansprout received monetary compensation from Singapore Exchange (SGX) to provide independent research on Singapore Depository Receipts (SDRs).

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments