CapitaLand Integrated Commercial Trust buys Paragon and sells Asia Square Tower 2

REITs

By Ng Hui Min • 20 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

CapitaLand Integrated Commercial Trust (CICT), Asia’s largest REIT, has announced the acquisition of the freehold Paragon for $3.9 billion, and divestment of Asia Square Tower 2.

What happened?

CapitaLand Integrated Commercial Trust (CICT) has been active managing its portfolio.

We saw its acquisition of the remaining 55% interest in CapitaSpring in August last year, as well as the purchase of ION Orchard earlier.

This would make it one of the Singapore REITs that has been active buying assets over the past 18 months.

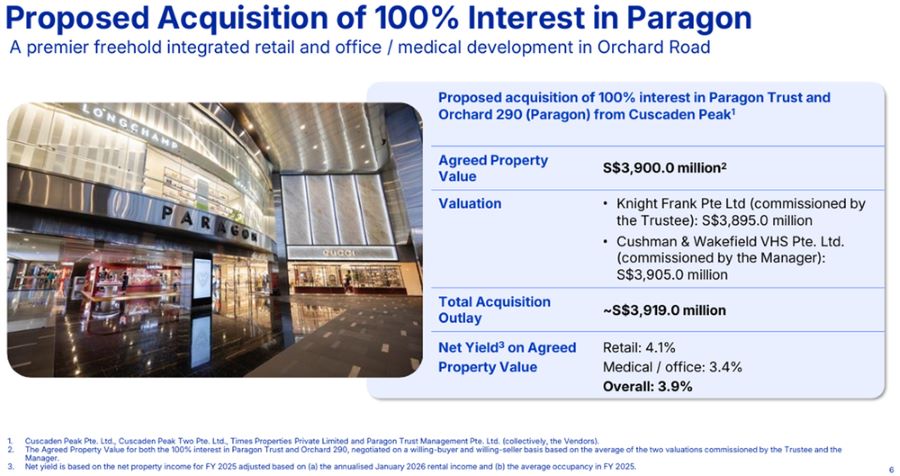

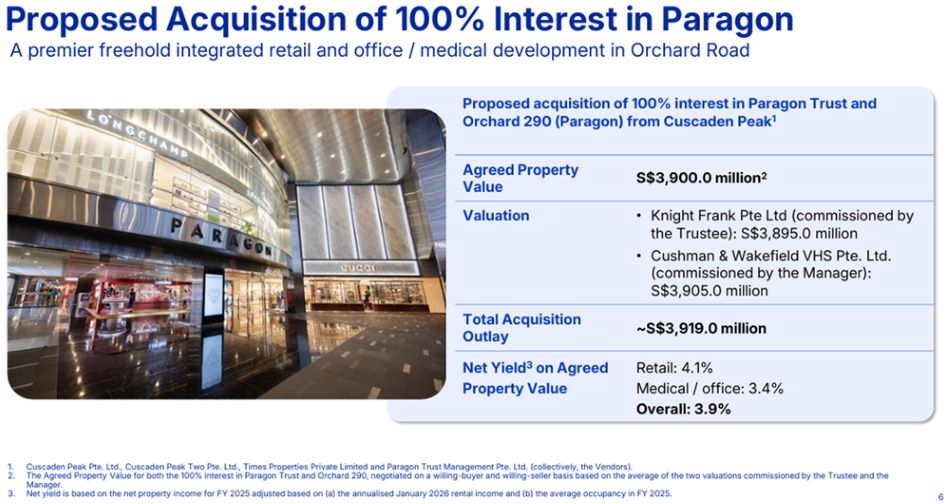

On 20 April 2026, CapitaLand Integrated Commercial Trust (CICT) announced the acquisition of Paragon, a premier freehold integrated development on Orchard Road, for S$3.9 billion, and the divestment of Asia Square Tower 2 for S$2.476 billion simultaneously.

To fund the shortfall, CapitaLand Integrated Commercial Trust (CICT) has also launched a private placement to raise at least S$600 million in new equity.

In this article, we will dive deeper into the transactions and understand what it means for CapitaLand Integrated Commercial Trust (CICT) unitholders.

6 things you need to know about CapitaLand Integrated Commercial Trust’s latest deals

#1 — Selling Asia Square Tower 2 and buying Paragon

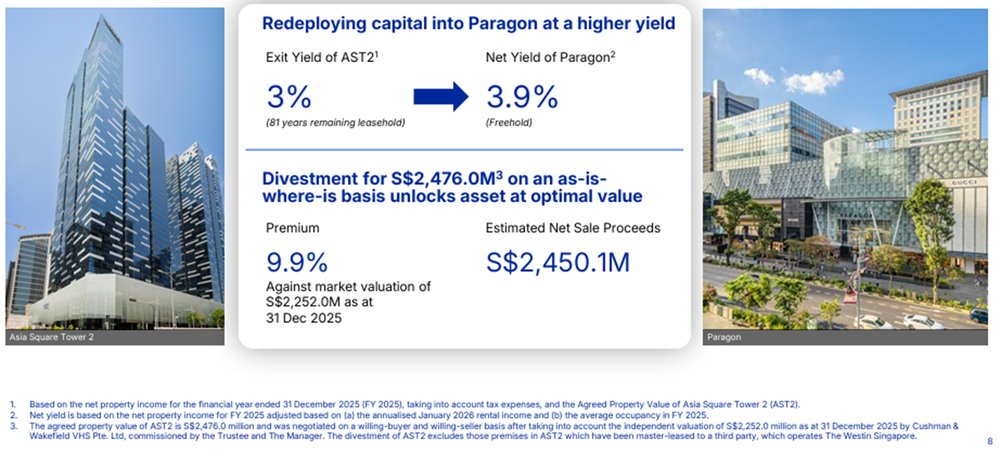

CapitaLand Integrated Commercial Trust is selling Asia Square Tower 2 and using the proceeds to invest in Paragon.

Asia Square Tower 2 is an office property with 81 years left on its lease, while Paragon is a freehold integrated development with a higher property yield of 3.9 per cent, compared with 3.0 per cent for Asia Square Tower 2.

This means CapitaLand Integrated Commercial Trust is selling one property and reinvesting the money into another property with a longer tenure and higher income yield.

At its core, this is a capital recycling transaction, where the REIT sells an asset and redeploys the proceeds into another one.

The 0.9 percentage point difference in yield may help support income over time, although this will also depend on how the transaction is carried out.

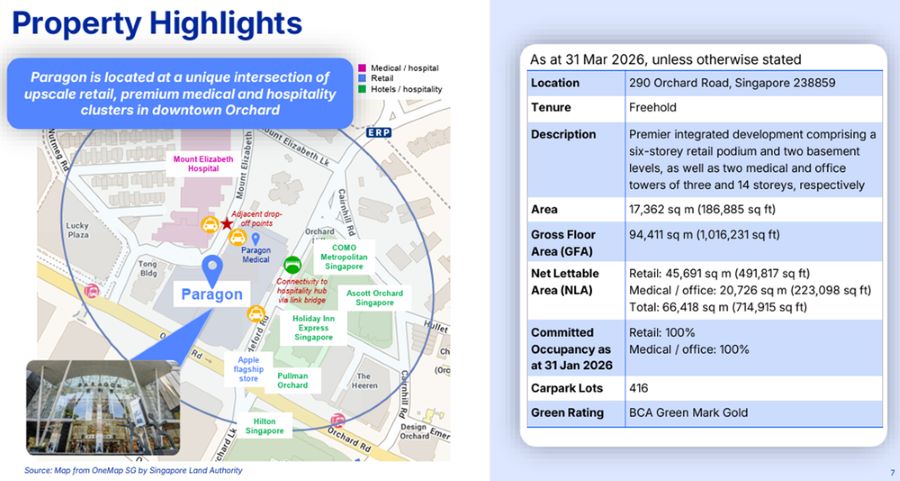

#2 — Paragon is a rare freehold Orchard Road asset

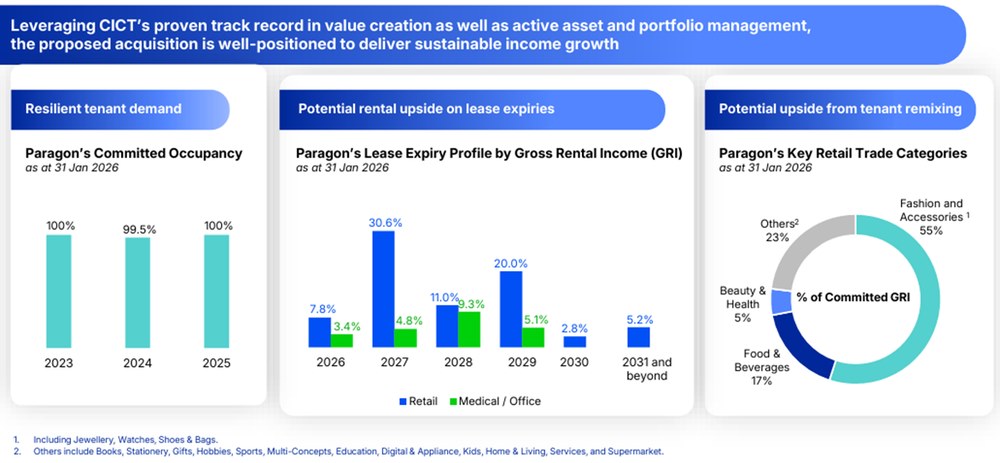

Paragon is a well-known Orchard Road property that combines luxury retail with medical suites and office space, giving CapitaLand Integrated Commercial Trust (CICT) exposure to more than one source of rental income.

What stands out is that the property was fully occupied as of January 2026, with both its retail space and medical or office space fully leased.

Paragon is also a freehold property, which is uncommon for a prime Orchard Road asset.

Unlike a leasehold property, it does not have a lease that runs down over time. This may help support its value over the longer term.

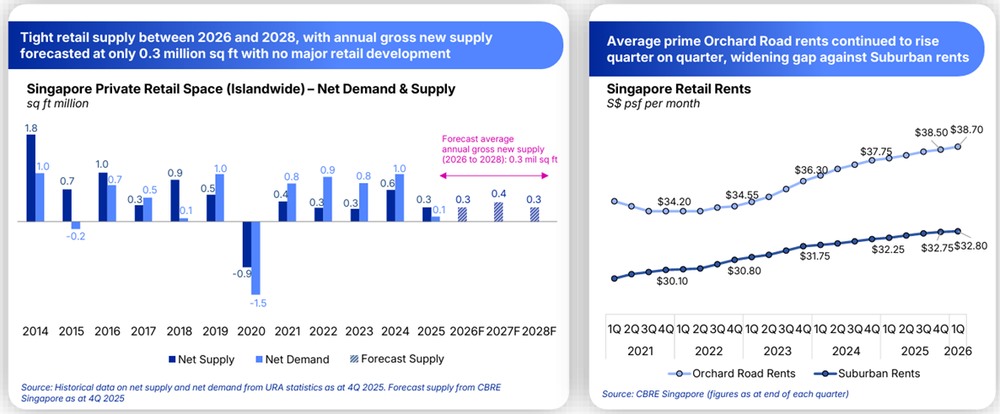

The broader backdrop also appears supportive.

There is not expected to be much new retail space added along Orchard Road over the next few years, which could help support rents if demand stays healthy.

At the same time, Orchard Road rents have been rising, growing by about 3.0% a year since 2021.

On top of that, CapitaLand Integrated Commercial Trust (CICT) sees room to further enhance the asset.

The last major upgrading works at Paragon were done in 2009, and management has said a future asset enhancement initiative could involve S$300 million or more in capital expenditure.

If executed well, this could create additional long term value on top of the current rental income.

#3 — Asia Square Tower 2 is being sold at a 9.9% premium

CapitaLand Integrated Commercial Trust (CICT) has agreed to sell Asia Square Tower 2 to IOI Marina View for S$2.476 billion.

This is 9.9 per cent above its latest independent valuation of S$2.252 billion as at 31 December 2025.

The estimated net sale proceeds are about S$2.450 billion, after taking into account transaction-related adjustments.

CapitaLand Integrated Commercial Trust (CICT) has owned Asia Square Tower 2 through CapitaLand Commercial Trust since 2017.

The sale is expected to complete in the second half of 2026, subject to the buyer obtaining shareholder approval at an EGM and receiving the relevant tax confirmation from IRAS.

#4 — The combined deal is expected to raise DPU

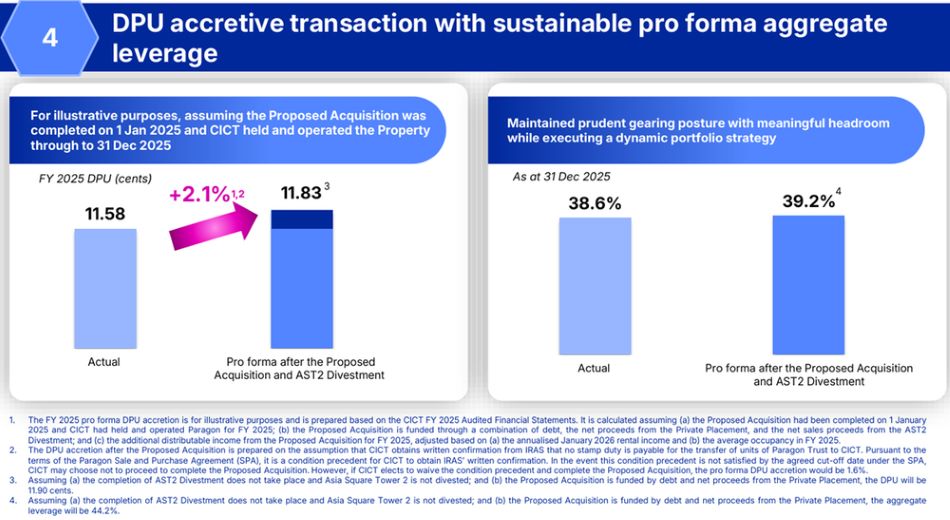

CapitaLand Integrated Commercial Trust (CICT) said the combined deal should be accretive to its distribution per unit (DPU).

On a pro forma basis, if both the Paragon acquisition and the Asia Square Tower 2 divestment had been completed on 1 January 2025, FY2025 DPU would have increased from 11.58 cents to 11.83 cents, implying a 2.1 per cent uplift.

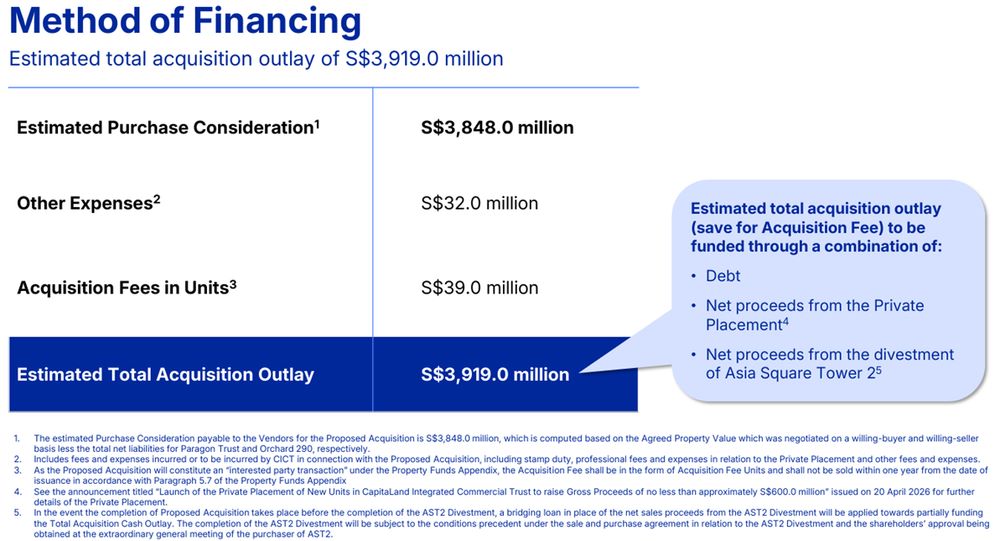

The deal will be funded using a mix of debt, net proceeds from the private placement of at least S$600 million, and the net sale proceeds from the AST2 divestment.

Even after the acquisition, CapitaLand Integrated Commercial Trust’s (CICT) pro forma aggregate leverage is expected to be 39.2 per cent, which remains comfortably below the 50 per cent regulatory limit.

#5 — CICT becomes larger and less focused on office assets

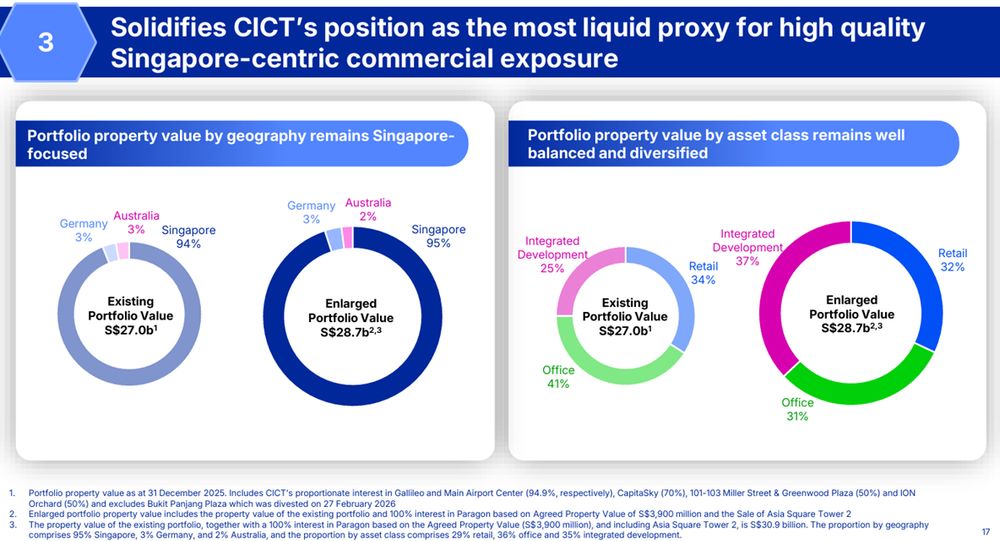

After the deal, CapitaLand Integrated Commercial Trust’s (CICT) portfolio will grow to S$28.7 billion across 25 properties.

The portfolio mix will also change after the transaction.

Retail properties are expected to make up 32 per cent of the portfolio, office properties 31 per cent, and integrated developments 37 per cent, up from 25 per cent previously.

This means CapitaLand Integrated Commercial Trust will become less dependent on office assets, with a larger share of the portfolio coming from retail and integrated developments.

The enlarged portfolio is also expected to remain well occupied, with occupancy at 97.2 per cent. Singapore will continue to account for 95 per cent of the portfolio by value.

In Singapore’s retail market, CapitaLand Integrated Commercial Trust is also expected to strengthen its position as the largest private retail landlord. With the addition of Paragon, its presence along Orchard Road will increase, and its share of Singapore’s private retail stock will rise to about 10 per cent.

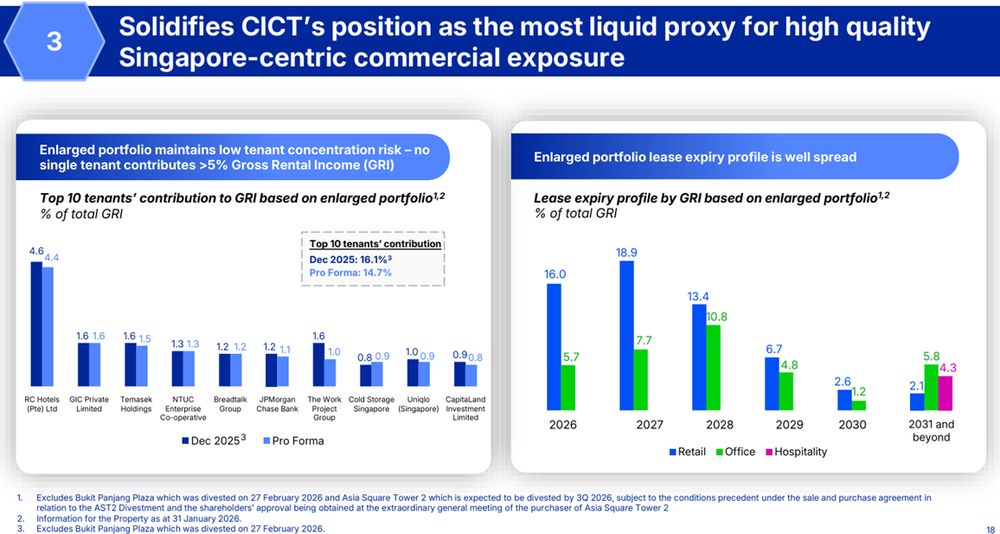

Tenant concentration is also expected to improve slightly. No single tenant is expected to contribute more than 5 per cent of gross rental income, while the share contributed by the top 10 tenants is expected to fall from 16.1 per cent to 14.7 per cent.

#6 — Unitholder approval is still needed

One important point is that the Paragon acquisition cannot go through yet without unitholder approval.

This is because the deal is classified as an interested person transaction, as the sellers, Cuscaden Peak, are indirect subsidiaries of Temasek.

Under SGX listing rules and the property funds rules, CapitaLand Integrated Commercial Trust (CICT) must seek specific approval from unitholders before it can complete the acquisition.

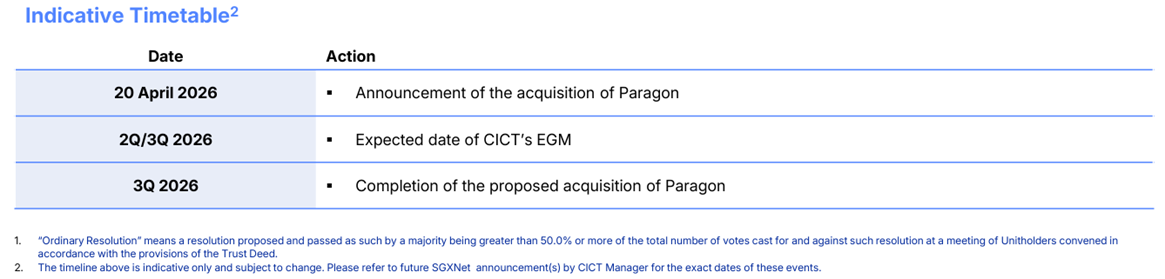

An extraordinary general meeting is expected to be held in the second or third quarter of 2026.

If unitholders approve the deal and the remaining conditions in the sale and purchase agreement are met, completion is expected in the third quarter of 2026.

Private placement of approximately S$750 million

Asia Square Tower 2 is being sold for S$2.476 billion, which is 9.9 per cent above its December 2025 valuation of S$2.252 billion.

Paragon is being acquired for S$3.9 billion, which is broadly in line with its March 2026 valuation range of S$3.895 billion to S$3.905 billion.

Based on these two transactions, CapitaLand Integrated Commercial Trust will need about S$1.47 billion in additional funding. This is based on Paragon’s total acquisition cost of S$3.919 billion, less the estimated net sale proceeds of S$2.450 billion from the divestment of Asia Square Tower 2.

To fund this amount, CapitaLand Integrated Commercial Trust plans to raise around S$600 million through a private placement, with the remaining amount to be funded by debt.

The placement drew strong demand from institutional and accredited investors and was upsized to approximately S$750 million, with the book approximately 4.8 times covered based on the upsized size.

The issue price was fixed at S$2.30 per new unit, a discount of approximately 4.0 per cent to the volume weighted average price of S$2.3955 on 17 April 2026.

A total of 326,087,000 new units will be issued, with trading expected to commence on the SGX on 29 April 2026.

CapitaLand Integrated Commercial Trust will also pay an advanced distribution of between 3.93 and 4.03 cents per unit for the period from 1 January 2026 up to the day before the new units are issued.

For existing unitholders, one point to watch is the increase in the number of units.

The 326,087,000 new units represent approximately 4.28 per cent of the total unit base.

Overall, the acquisition of Paragon and the sale of Asia Square Tower 2 are expected to increase distribution per unit by 2.1 per cent on a pro forma basis.

In the long term, the transaction could look more favourable if Paragon is able to contribute stronger rental growth and if there are opportunities to improve the property further.

What would Beansprout do?

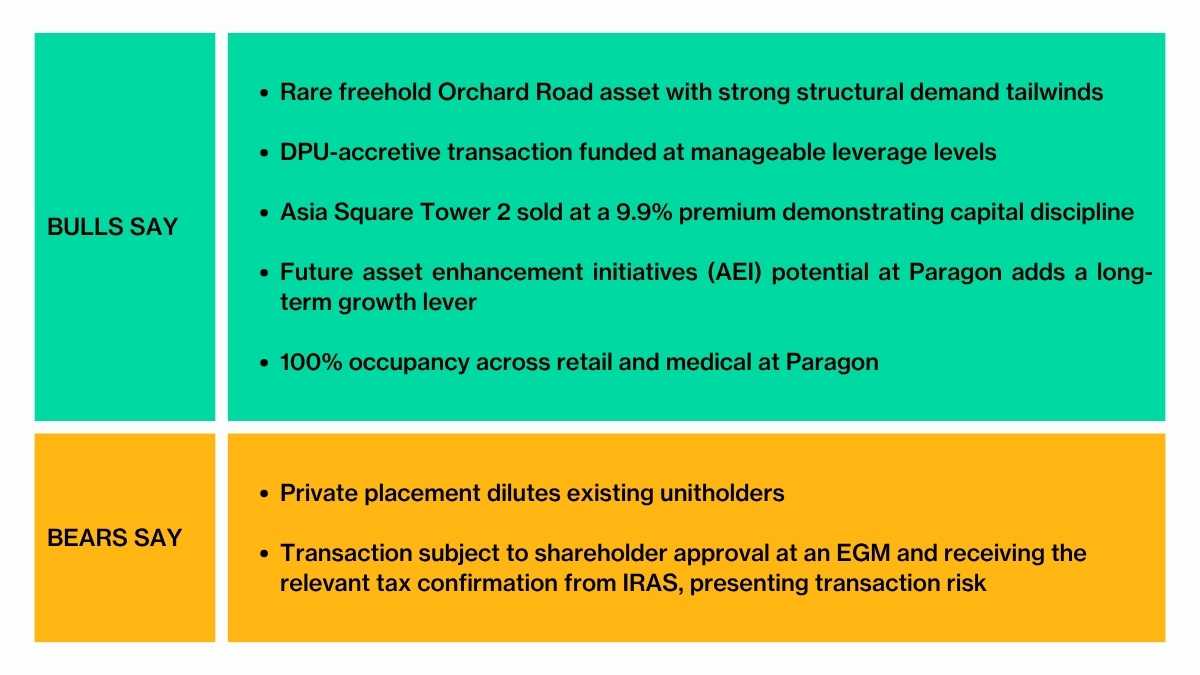

To me, CapitaLand Integrated Commercial Trust’s latest move appears to be a reasonable transaction.

The REIT is selling Asia Square Tower 2, an older office property with a lease, at a price that is 9.9% above its valuation, and using the proceeds to acquire Paragon, a freehold Orchard Road property with a higher property yield and full occupancy.

This suggests the transaction is not only increasing the size of the portfolio, but may also improve its quality over time.

The deal also appears supportive for income. Based on management’s guidance, pro forma distribution per unit is expected to increase by 2.1%, while aggregate leverage is expected to increase to 39.2%.

Overall, CapitaLand Integrated Commercial Trust (CICT) continues to offer relatively steady distributions through its portfolio of assets largely in Singapore, making it one of the names I would consider if I am looking for income ideas.

However, I would be mindful that the REIT's valuation does not look as attractive as before.

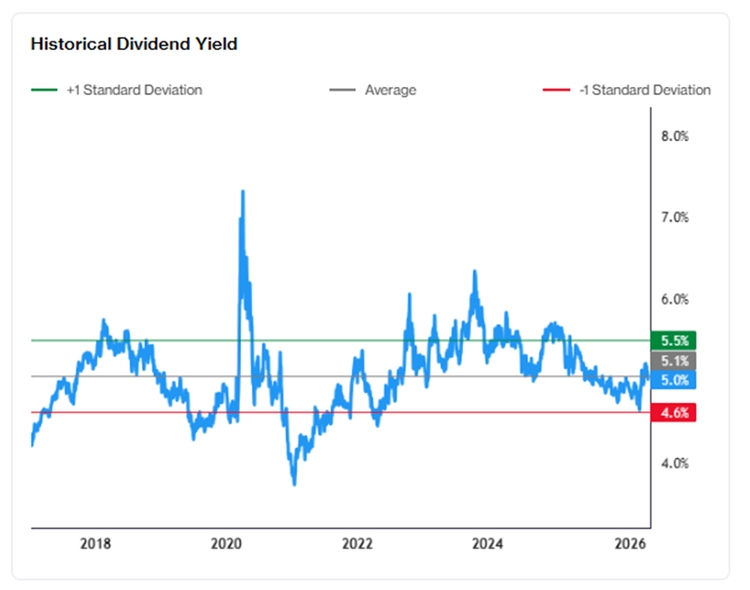

Based on the pro forma distribution per unit of 11.83 cents and the 17 April closing price of S$2.39, CapitaLand Integrated Commercial Trust would offer a dividend yield of about 4.9%. This is lower than its long-term average of 5.1% dividend yield.

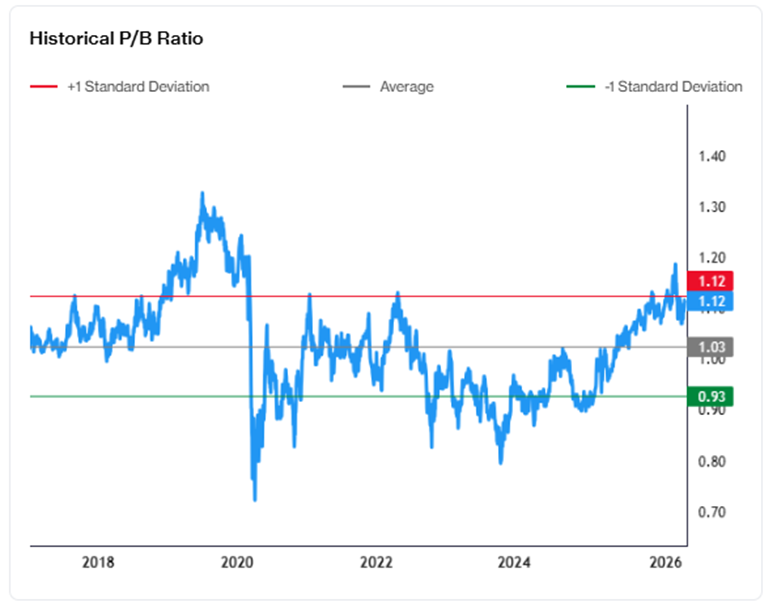

Its pro forma NAV per unit is expected to rise to S$2.11, implying a price-to-book ratio of 1.13x, above its long-term average P/B of 1.03x.

I will also be thinking about how I can build a diversified income portfolio beyond Singapore REITs to grow my income pot. Explore other income ideas here.

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

What do you think of CapitaLand Integrated Commercial Trust (CICT)'s proposed acquisition of Paragon? Share with us in the comments below or in our Telegram group!

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments