3 CPF updates from Budget 2026 that may affect your retirement savings

Retirement

By Gerald Wong, CFA • 26 Feb 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Learn more about three CPF updates in Budget 2026, including a one-off top-up, higher senior contribution rates and a new voluntary investment scheme.

What happened?

Several CPF updates were announced in Budget 2026.

These are part of the key measures announced in Budget 2026, including more CDC vouchers and support for AI upskilling.

This comes on top of CPF changes that have already come into effect in 2026, such as CPF contribution changes, higher retirement sums, and matching grant schemes.

These CPF changes are intended to boost the retirement savings of Singaporeans.

In this article, I will go through three CPF announcements from Budget 2026 and what they could mean for our retirement savings.

3 CPF announcements from Budget 2026 that may affect your retirement savings

#1 - Budget 2026 CPF Top-Up of up to S$1,500 in December 2026

The Government will provide a one-off, means-tested CPF top-up of up to S$1,500 to eligible Singaporeans aged 50 and above in 2026, which refers to those born in 1976 or earlier.

The top-up will be credited in December 2026 to your CPF Retirement Account (RA), or to your Special Account (SA) if your Retirement Account has not been created yet.

The amount is tiered based on CPF retirement savings as at 31 December 2025 and the Annual Value (AV) of your residential property, and you must own not more than one property to qualify.

Eligible seniors with CPF retirement savings below S$60,000 will receive S$1,500 if their home Annual Value is not more than S$21,000, or S$500 if the Annual Value is more than S$21,000 but not exceeding S$31,000.

Eligible seniors with CPF retirement savings of at least S$60,000 but less than S$110,200 (the 2026 Basic Retirement Sum) will receive S$1,000 if their home Annual Value is not more than S$21,000, or S$500 if the Annual Value is more than S$21,000 but not exceeding S$31,000.

CPF Board has stated that more details will be available later in 2026, and eligible recipients will be notified in December 2026, with eligibility checks available via GovBenefits.

| CPF Retirement Savings1 (as at 31 Dec 2025) | Singaporeans born in 1976 or earlier | |

| Own not more than 1 property | ||

| Less than S$60,000 | S$1,500 | S$500 |

| At least S$60,000 but less than S$110,200 (2026’s Basic Retirement Sum) | S$1,000 | S$500 |

| 1 Computed based on the sum of Retirement Account and CPF LIFE balances, or the sum of Ordinary Account and Special Account balances if the Retirement Account has not yet been created. Source: CPF | ||

#2 - CPF contribution rates will rise for senior workers from 1 January 2027

CPF contribution rates for senior workers will increase from 1 January 2027, in line with recommendations by the Tripartite Workgroup on Older Workers.

Employees aged above 55 to 65 will see changes to their contribution rates, regardless of their salary level, provided they earn more than S$750 per month.

Total contribution rates will rise by 1.5 percentage points for employees aged above 55 to 60, and by 1 percentage point for employees aged above 60 to 65.

The increase includes a 0.5 percentage point rise in employer contributions, while employee contributions rise by 1 percentage point (for above 55 to 60) and 0.5 percentage point (for above 60 to 65).

Here are the new contribution rates for senior workers aged above 55 to 65 from 1 January 2027:

| Employee’s age (years) | CPF Contribution Rates in 2026 | CPF Contribution Rates from 1 Jan 2027 | ||

| Total (% of wage) | Total (% of wage) | By employer (% of wage) | By employer (% of wage) | |

| 55 and below | 37 | 37 | 17 | 20 |

| Above 55 to 60 | 34 | 35.5 (+1.5) | 16.5 (+0.5) | 19.0 (+1) |

| Above 60 to 65 | 25 | 26 (+1) | 13.0 (+0.5) | 13.0 (+0.5) |

| Above 65 to 70 | 16.5 | 16.5 | 9 | 7.5 |

| Above 70 | 12.5 | 12.5 | 7.5 | 5 |

| Note: Figures in brackets () denote increase in rates. *For employees earning monthly wages exceeding $750 Source: CPF | ||||

These additional contributions will be fully allocated to the Retirement Account (RA) up to the Full Retirement Sum (FRS), to help senior workers save more for retirement.

If a working senior has already set aside the Full Retirement Sum (FRS) in the Retirement Account, the increased contributions will be channelled to the Ordinary Account (OA) instead.

To cushion the impact on business costs, employers will receive a CPF Transition Offset equivalent to half of the 2027 increase in employer CPF contributions, and CPF Board stated that the offset will be provided automatically without application.

Read here to know the CPF contribution changes from 1 Jan 2026.

#3 - A new CPF investment scheme will be introduced in the first half of 2028

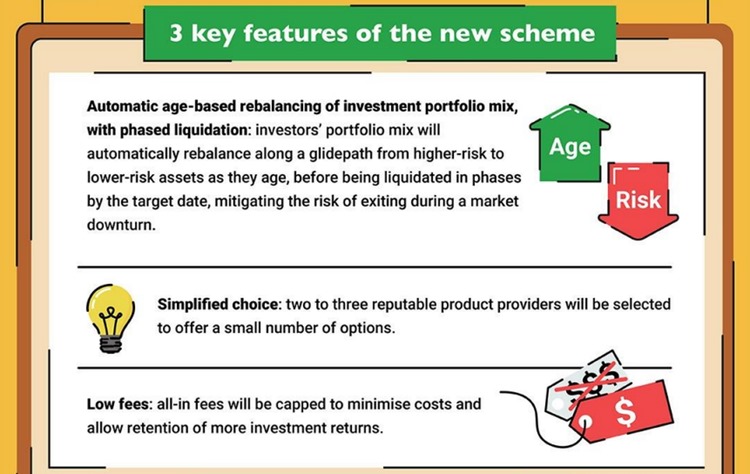

CPF Board will introduce a new, voluntary investment scheme in the first half of 2028, following the CPF Advisory Panel’s recommendation for a Lifetime Retirement Investment Scheme.

The stated aim is to offer simplified, low-cost and diversified life-cycle investment products for members who want to stay invested for the long term, but may have less expertise navigating CPF Investment Scheme (CPFIS) options or may prefer not to actively manage their investments.

CPF Board said these life-cycle products are designed to automatically rebalance portfolios from higher-risk assets towards lower-risk assets as members approach a target date, and the products may be liquidated in phases before that target date.

The phased liquidation is intended to reduce the risk of exiting during a market downturn, because withdrawals are not concentrated at a single point in time.

After phased liquidation, sale proceeds will be transferred to the member’s Retirement Account (RA) up to the Full Retirement Sum (FRS), with any remaining proceeds transferred to the Ordinary Account (OA).

The RA balances can then be used for CPF LIFE, when the member chooses to start monthly payouts any time from age 65.

The product line-up is intended to be more curated than CPFIS, with two to three product providers and a simplified set of choices, and that all-in fees for the scheme will be capped.

CPF Board said it will engage the industry from March 2026, expects selected providers to be announced in the first half of 2027, and targets launch in the first half of 2028.

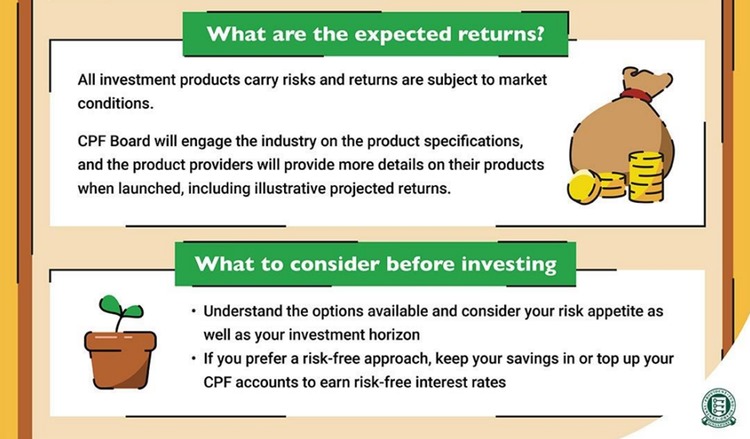

That said, members who prefer a risk-free approach can continue to keep savings in CPF to earn CPF interest rates, and members can also consider cash top-ups or transferring OA savings to the Special Account to boost CPF LIFE payouts.

For members who want to take investment risk for the possibility of higher returns, CPF Board said the new scheme will be an additional option alongside CPFIS, and CPFIS eligibility criteria will apply to members who want to invest CPF savings under the new scheme.

As with any market-based product, CPF Board cautioned that investment risk remains, and returns will depend on market conditions.

What would Beansprout do?

Budget 2026 introduced three CPF measures intended to help Singaporeans with their retirement planning: a one-off CPF top-up for eligible older Singaporeans, higher CPF contribution rates for senior workers from 2027, and a new voluntary life-cycle investment scheme planned for 2028.

Across the three measures, I believe the new CPF investment scheme has the most scope fo impact how much savings I have for my retirement, as the potential investment returns can make a significant impact when compounded over time.

However, I will look out for more details on product providers, fee caps, and how the glidepath is implemented to determine if it is something I will take up.

I will also compare it against CPF’s risk-free interest and existing CPFIS choices to understand what are the trade-offs.

In the meantime, I will consider exploring different ways to grow my CPF retirement savings.

One of the options is to transfer funds from your CPF Ordinary Account (OA) to your CPF Special Account (SA) to earn a higher interest rate. I discuss the pros and cons of transferring to your SA here.

Alternatively, I may also choose to invest your CPF funds. I look at the different investment options eligible for the CPF Investment Scheme here.

Outside of the CPF, I will also be looking at other ways to generate passive income to strengthen my retirement nest egg. Learn more about the different ways to generate passive income.

If you want the wider context of Budget measures beyond CPF, you can refer to our Budget 2026 overview here.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments