OCBC has outpaced DBS and UOB in 2026. Is its 4.3% dividend yield still attractive?

Stocks

By Gerald Wong, CFA • 14 Apr 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

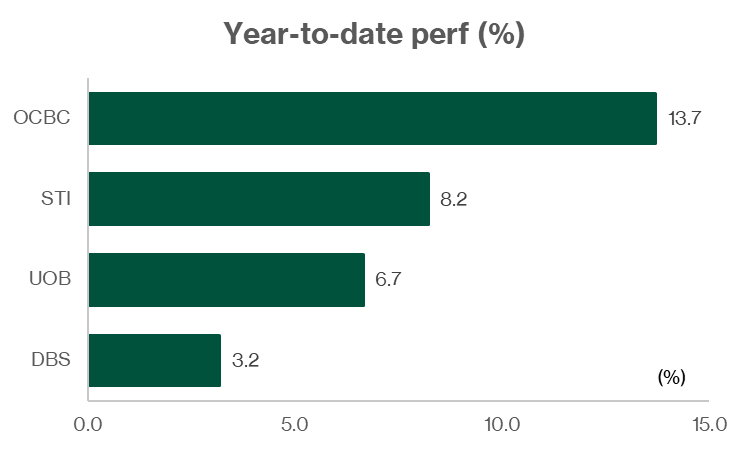

The share price of OCBC has hit an all-time high in April 2026. With a forward dividend yield of 4.3%, we find out if OCBC is more attractive than DBS and UOB.

What happened?

OCBC has quietly become the standout among Singapore’s three local banks.

While DBS was the market favourite for much of 2025, it is OCBC that has recently been making new highs in 2026.

OCBC’s share price rose above S$22 at the end of March and touched a fresh record high of S$22.83 on April 2, 2026, taking its market capitalisation above S$100 billion for the first time.

By comparison, DBS was still trading below its own recent peak, while UOB’s earlier rebound had been less sustained.

With the recent movement, I have seen questions in the Beansprout community on how OCBC has been hitting all-time highs and if this could continue.

In this article, I look at why OCBC has done well compared to DBS and UOB and if it could continue to play catch-up with DBS.

6 reasons why OCBC's share price has performed better than DBS and UOB

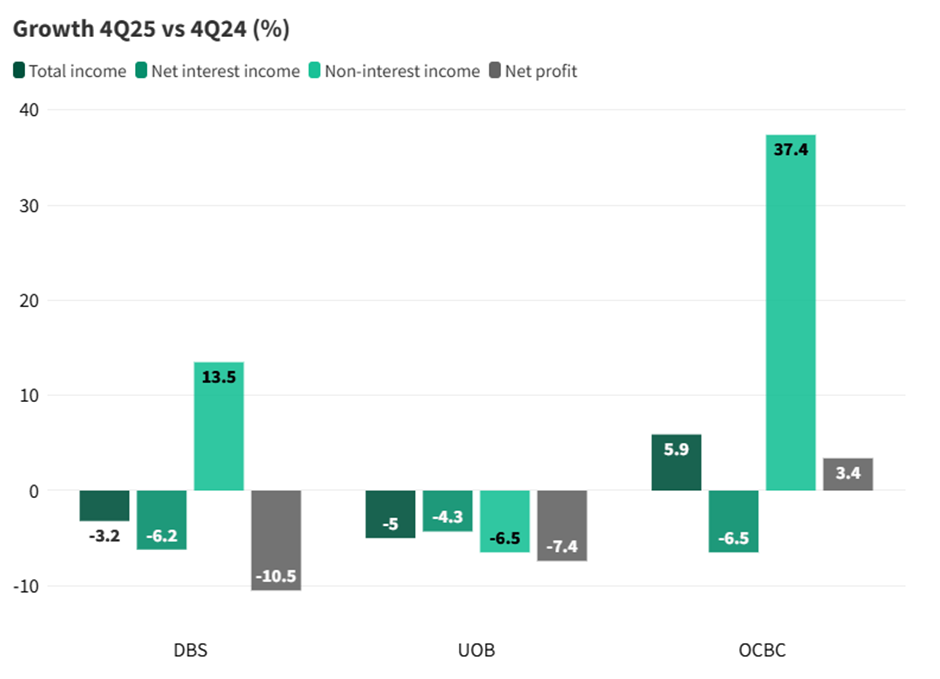

#1 - OCBC was the only bank to post a year-on-year net profit increase in 4Q25

OCBC delivered the strongest fourth-quarter result among the three banks.

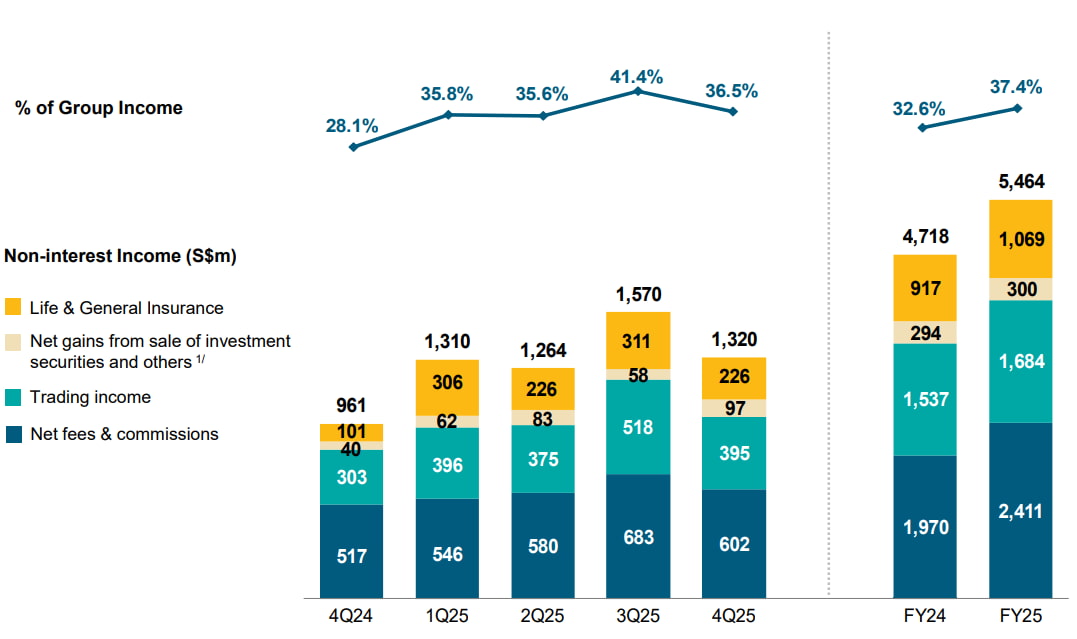

For 4Q2025, OCBC’s net profit rose 3% year on year to S$1.74 billion, beating analyst expectations, helped by a 37% jump in non-interest income.

For the full year, it reported record total income of S$14.6 billion and profit before tax of S$9.12 billion, even as lower interest rates weighed on net interest income.

That stood in contrast to DBS and UOB.

DBS reported a 10% drop in 4Q2025 net profit and guided that 2026 net profit would likely come in slightly below 2025 levels as rate headwinds persist.

UOB’s 4Q2025 net profit fell 7% year on year, while management kept guidance for net interest margin at 1.75% to 1.80% for 2026 and trimmed its fee-growth outlook.

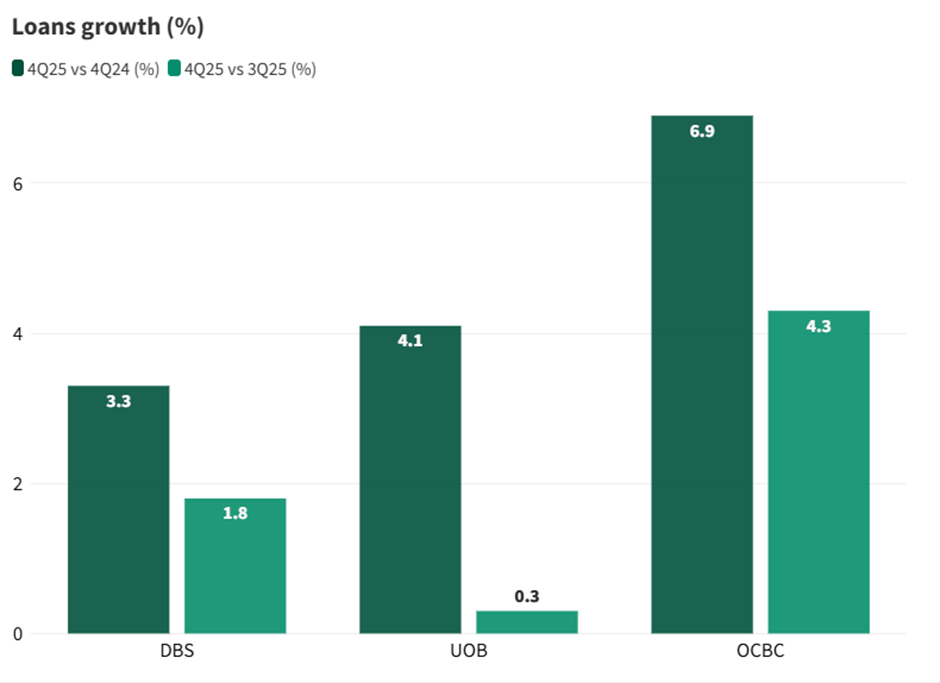

#2 - OCBC led loan growth in 4Q25, while all three banks showed steady expansion

OCBC continued to lead on loan growth in 4Q25, with its loan book rising 6.9% year-on-year and 4.3% quarter-on-quarter, supported by Singapore mortgages and ASEAN corporate lending.

UOB reported 4.1% year-on-year loan growth, backed by steady demand from its corporate and regional client base.

DBS saw more moderate growth of 3.3% year-on-year, but still delivered broad-based expansion across corporate and wealth management loans, bringing gross loans to S$451bn.

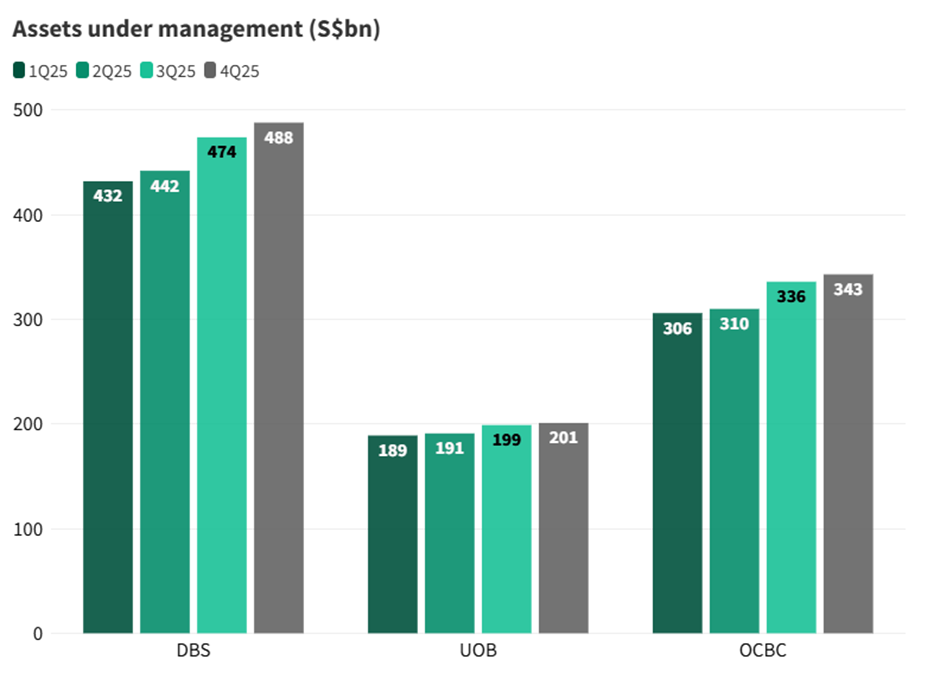

#3 - OCBC delivered fastest growing wealth management fees

For FY2025, OCBC’s total non-interest income rose 16% to S$5.46 billion, driven by a 33% jump in wealth management fees, the fastest growth among the three local banks, as well as a 17% increase in insurance income from Great Eastern.

Its broader wealth management income reached a record S$5.6 billion and made up 38% of total income, up from 34% a year earlier. That gave OCBC a much bigger buffer against lower lending margins.

DBS also saw strong wealth growth, with wealth management fees up 29% to a record S$2.81 billion and assets under management at a new high.

But its fourth-quarter earnings still missed expectations because margin pressure was stronger and other non-interest income was weaker.

UOB is improving its fee base too, but it still looks more exposed to margin compression than OCBC, and its recent earnings have been weighed down by both lower NIM and earlier heavy provisioning.

#4 - Great Eastern gives OCBC an advantage that DBS and UOB do not have

This is probably one of the most underappreciated parts of the story.

OCBC’s majority stake in Great Eastern gives it a second earnings engine that DBS and UOB simply do not have.

In 4Q2025, OCBC’s insurance income more than doubled year on year to S$226 million, while full-year insurance income rose 17 per cent to S$1.07 billion.

That matters even more in a lower rate environment, because it helps cushion pressure on traditional banking profits.

This is one reason investors are now willing to pay more for OCBC than before. It is no longer seen as just the slower Singapore bank.

Increasingly, it is being valued as a bank with a stronger mix of wealth and insurance earnings.

#5 - OCBC had more room to surprise because expectations were lower

DBS has long been the market favourite among Singapore banks, supported by its strong management execution, digital leadership and consistently high valuation. But that also means expectations are very demanding.

When a stock is already widely owned and priced for near-flawless delivery, even strong results may not drive as much further upside.

OCBC, on the other hand, is less well-owned by investors compared to DBS and it’s less priced to perfection.

That left more room for investors to re-rate the stock as earnings held up, capital returns improved and management execution remained steady.

#6 - OCBC may have the most balanced outlook of the three

What matters now is not just who did best last quarter, but which bank looks best positioned for the next 12 months.

OCBC’s outlook appears increasingly balanced across net interest income, wealth management and insurance and it reduces reliance on any single earnings engine.

DBS remains the quality leader, but expectations are already high and its profit outlook is moderating as margins ease.

UOB still offers leverage to regional growth, but its story looks more tied to loan momentum, margin stability and credit normalisation.

How does OCBC's current valuation compare to DBS and UOB?

OCBC has a lower forward dividend yield compared to DBS and UOB.

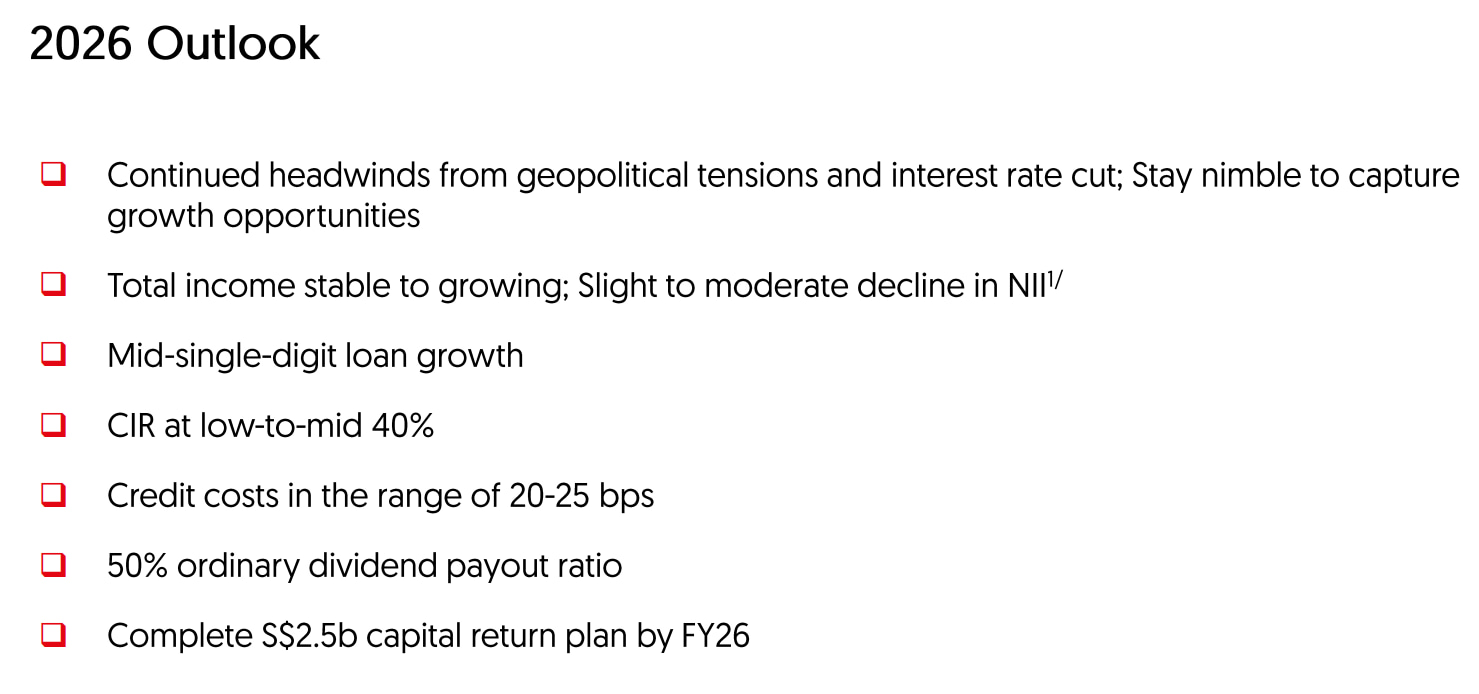

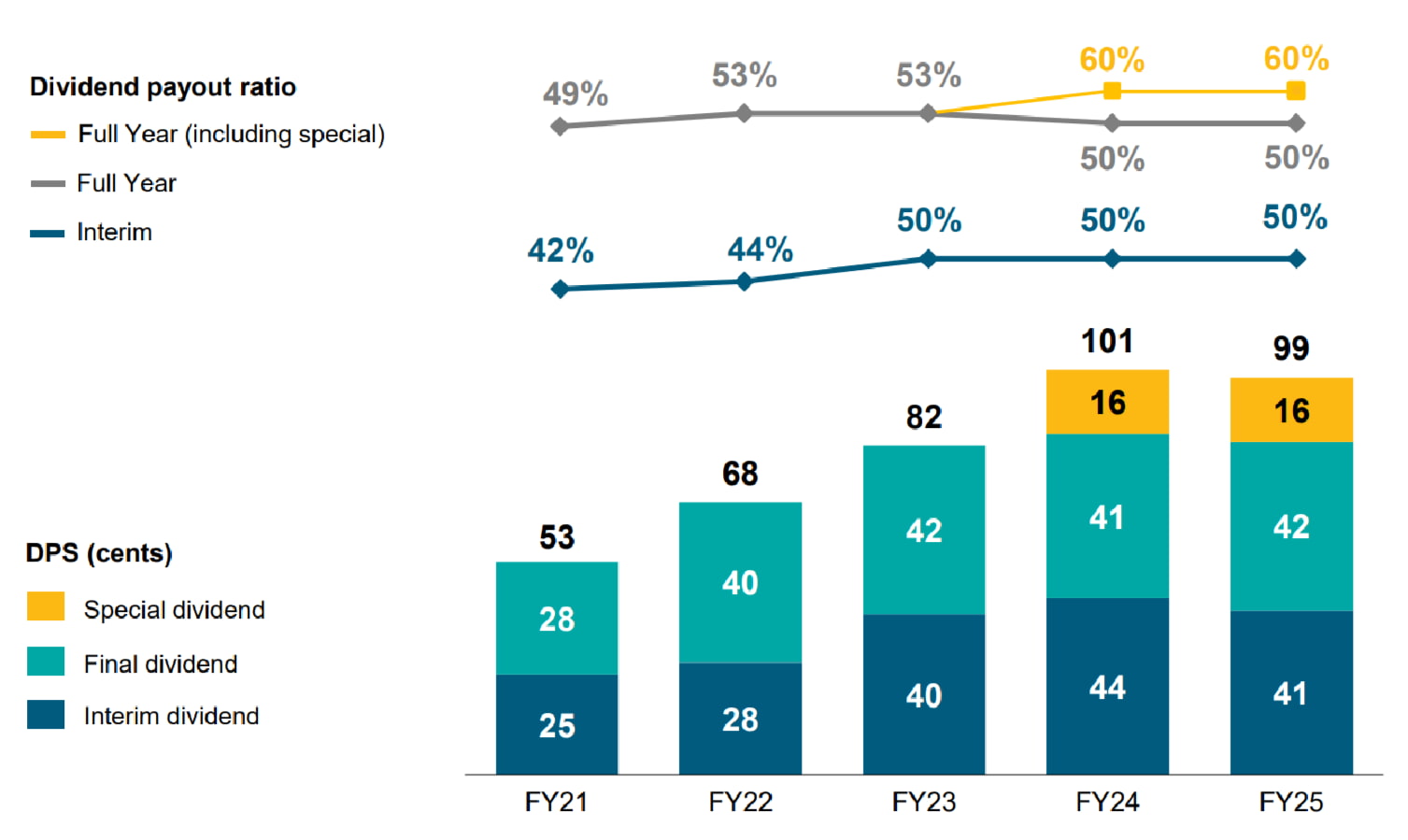

OCBC proposed total FY2025 dividends of 99 cents per share, including a special dividend, implying a 60 per cent payout ratio. Management has also reiterated that its S$2.5 billion capital return plan is targeted to be completed by FY2026.

While OCBC’s formal guidance still points to a 50 per cent ordinary payout ratio, comments from its new CEO suggesting a preference for special dividends have helped reassure investors that capital returns could remain supportive.

Currently, OCBC offers a forward dividend of 4.3%, below DBS forward dividend yield at about 5.8 per cent, and UOB 's forward divdiend yield of 4.6 per cent.

OCBC price to book at 1.66x, lower than DBS’ 2.36x

OCBC is still cheaper than DBS on price-to-book, trading at about 1.66 times book value versus 2.36 times for DBS.

Its current valuation is already well above its historical average of around 1.13 times book, which suggests much of the recent improvement is now being reflected in the share price.

What would Beansprout do?

OCBC has been the standout among the three local banks because it delivered stronger earnings, faster loan growth, better wealth fee momentum and a more diversified earnings base through Great Eastern.

However, after its strong share price performance, its valuation is no longer as attractive as before.

Its price-to-book valuation has moved up to about 1.66x, well above its historical average.

OCBC’s forward dividend yield of about 4.3 per cent is also lower than DBS at around 5.8 per cent.

Hence for income investors, DBS still offers a higher forward dividend yield, stronger franchise quality and market leadership.

If I am looking to diversify my portfolio beyond DBS by adding another Singapore bank, then I may consider OCBC through its exposure to banking, wealth management and insurance in one name, albeit with a lower yield.

More broadly, this fits with our view that Singapore should remain a core part of a portfolio, supported by the market’s relative resilience, dividend support, and safe haven appeal.

It also reflects our focus on looking beyond Singapore REITs for income, by building a more diversified portfolio with quality dividend names such as the local banks.

Looking for more stock ideas to capture market opportunities? Explore our high conviction ideas here.

Do you own DBS or OCBC or both? Share with us in the comments below or in our Telegram group!

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win S$150 CapitaVoucher weekly, with S$600 in total up for grabs. Promo ends on 30 April 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Planning to invest in OCBC, UOB or DBS? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments