Seatrium shares lag STI despite recovery signs. What investors may want to watch

Stocks

By Goh Lay Peng • 11 Jun 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Seatrium shares have lagged the STI despite improving margins and a S$15.5b order book. We look at what investors may want to watch next.

What happened?

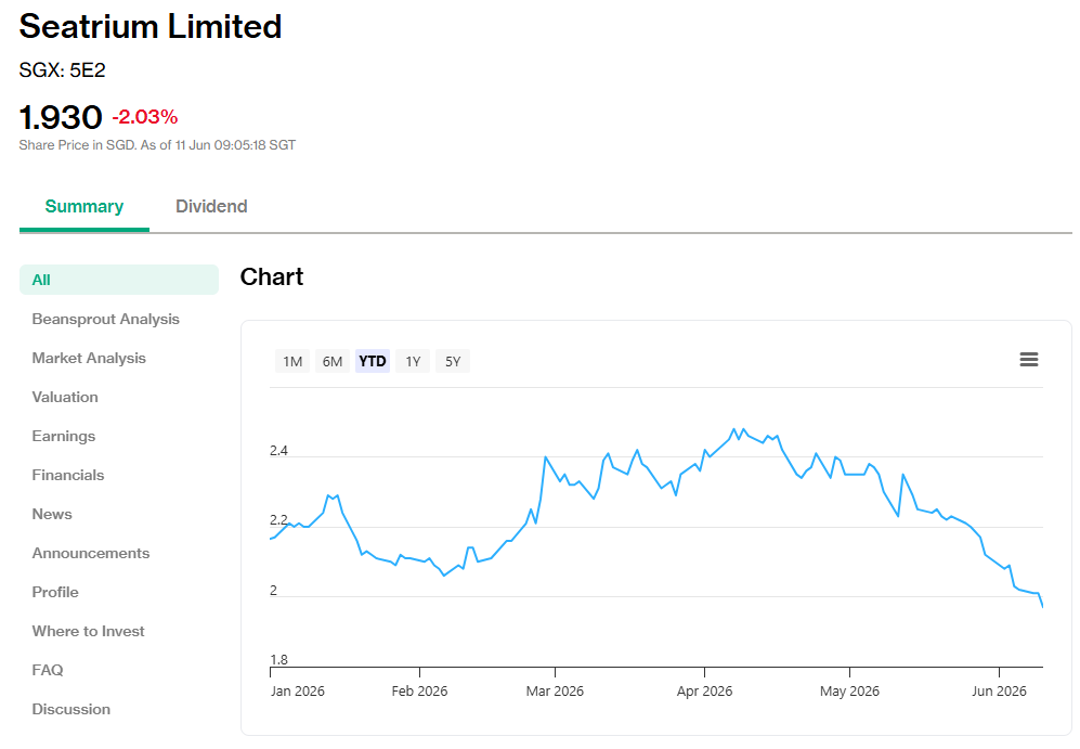

Seatrium has shown clearer signs of recovery this year.

Earlier this year, we highlighted Seatrium as one of the best-performing Singapore blue chip stocks in February 2026, after its share price rallied on the back of stronger financial year 2025 (FY2025) results and improving order visibility.

Even so, its share price has still lagged the Straits Times Index (STI) year-to-date. As of 9 June 2026, the STI was up about 7.9% year-to-date, while Seatrium’s share price had fallen by about 6.9%.

The weakness came even as Seatrium’s 1Q2026 business update on 29 May 2026 pointed to further progress in its turnaround.

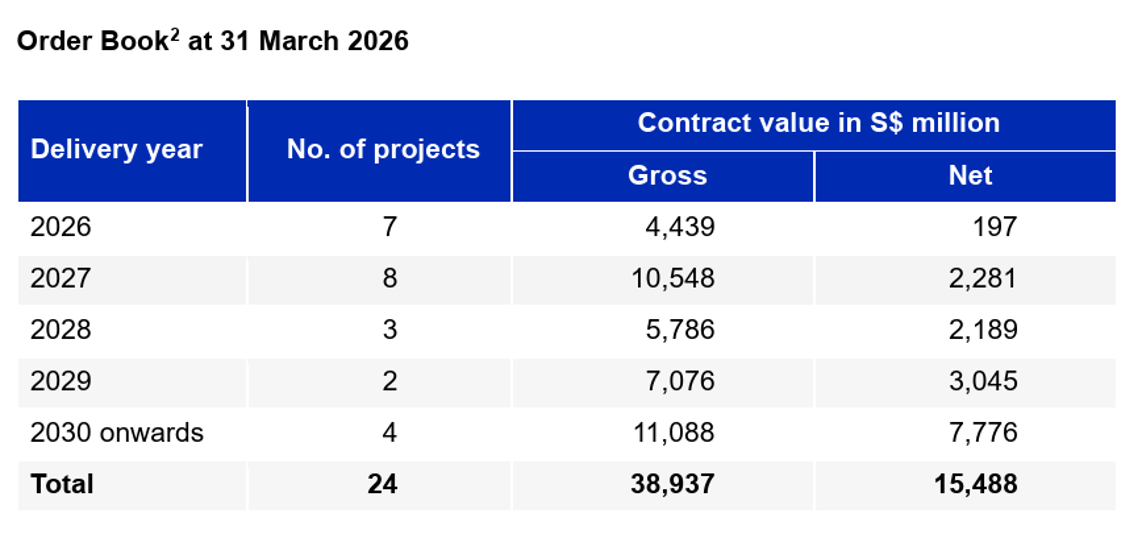

The company reported a net order book of S$15.5 billion across 24 projects, with deliveries stretching through to 2033, while gross margins continued to improve from a better project mix, lower overheads and cost discipline.

This raises a key question: is the market overlooking Seatrium’s recovery, or waiting for clearer evidence that the turnaround is sustainable?

In this article, I take a closer look at why Seatrium’s share price has lagged, what stood out from its latest update, and what investors may want to watch before deciding if the stock deserves a closer look.

Why has Seatrium’s share price lagged despite recovery signs?

Seatrium’s recovery story has improved.

However, investors may still be looking for clearer evidence that the recovery can translate into stronger earnings and returns.

#1 - Seatrium’s order book has declined from its previous level

Seatrium’s net order book stood at S$15.5 billion as of 31 March 2026.

This is still a sizeable order book, with deliveries stretching through to 2033.

However, it was lower than the S$17.8 billion net order book at the end of 2025.

This means investors may be watching whether Seatrium can replenish its order book quickly enough.

This is important because new order wins are needed to support future revenue growth once current projects are delivered.

#2 - FY2026 revenue may dip before recovering

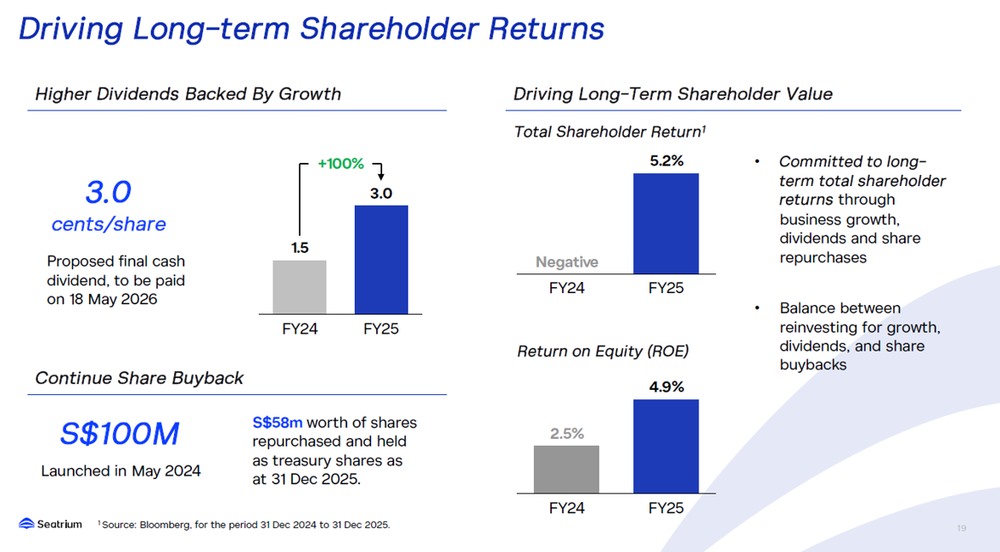

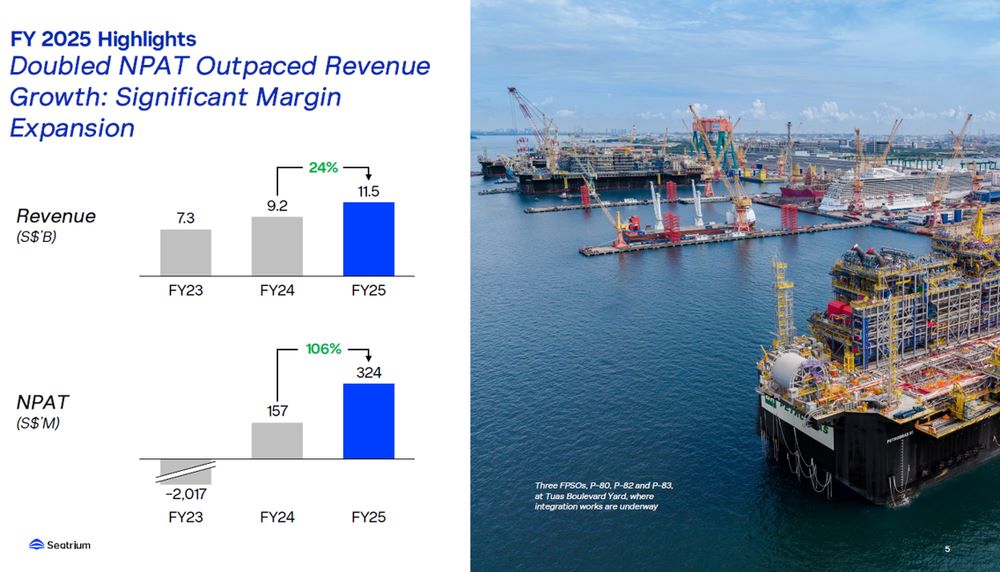

Seatrium’s FY2025 results showed strong improvement.

Revenue rose 24% year-on-year to S$11.5 billion, while net profit doubled to S$324 million.

Gross profit margin improved to 7.4% from 3.1% in FY2024. EBITDA also rose 34% to S$837 million.

However, FY2026 revenue may dip slightly before recovering from 2027 onwards, as 2025 order wins were softer than Seatrium’s revenue run-rate.

This may explain why investors have not fully priced in the recovery yet.

#3 - Return on equity is still low

Seatrium’s return on equity (ROE) remains below what investors may usually look for in a stronger recovery stock.

Trailing ROE is currently around 4.8%.

This is still below the 10% level that I would usually use as a baseline for companies generating meaningful returns on shareholders’ capital.

Part of this reflects Seatrium’s early stage of recovery following the Keppel Offshore & Marine merger.

It also reflects the drag from older lower-margin projects that are still working their way through the order book.

The direction is improving, but the recovery has not fully shown up in shareholder returns yet.

#4 - Some legacy risks remain

Seatrium has made progress in resolving legacy issues.

However, some residual legal and arbitration risks remain.

Operation Car Wash required a total settlement outflow of around S$172 million in FY2025, while a Keppel arbitration claim of about S$68 million remains outstanding.

These may not change the long-term recovery story, but they could still affect investor sentiment in the near term.

What stood out from Seatrium’s 1Q2026 update?

Despite the share price weakness, Seatrium’s latest update had several encouraging points.

The key question is whether these positives are enough to support a more sustainable earnings recovery.

#1 - Seatrium delivered projects and maintained a sizeable order book

Seatrium delivered two projects during the quarter.

These were the the trailing suction hopper dredger (TSHD) Frederick Paup, the largest Jones Act-compliant trailing suction hopper dredger built in the United States, and the wind turbine installation vessel (WTIV) Maersk Viridis, a next-generation wind turbine installation vessel.

The group also completed 46 vessel repairs and upgrades. These included one floating storage and regasification unit (FSRU) conversion, five liquefied natural gas (LNG) carriers and seven cruise vessels.

Seatrium also secured its eighth FSRU conversion project, the LNGT Karadeniz, for Karpowership. This suggests that project execution remains on track.

#2 - Seatrium’s margins continued to improve

The improvement in margins may be the more important signal.

Seatrium’s gross profit margin improved to 7.4% in FY2025, compared with 3.1% in FY2024.

In 1Q2026, gross margins continued to improve, supported by a better project mix, lower overheads and continued cost discipline.

This matters because Seatrium’s investment case is not just about winning more projects. It is also about whether the company can execute these projects at better margins.

If legacy lower-margin projects continue to roll off, Seatrium may have room to improve earnings quality over time.

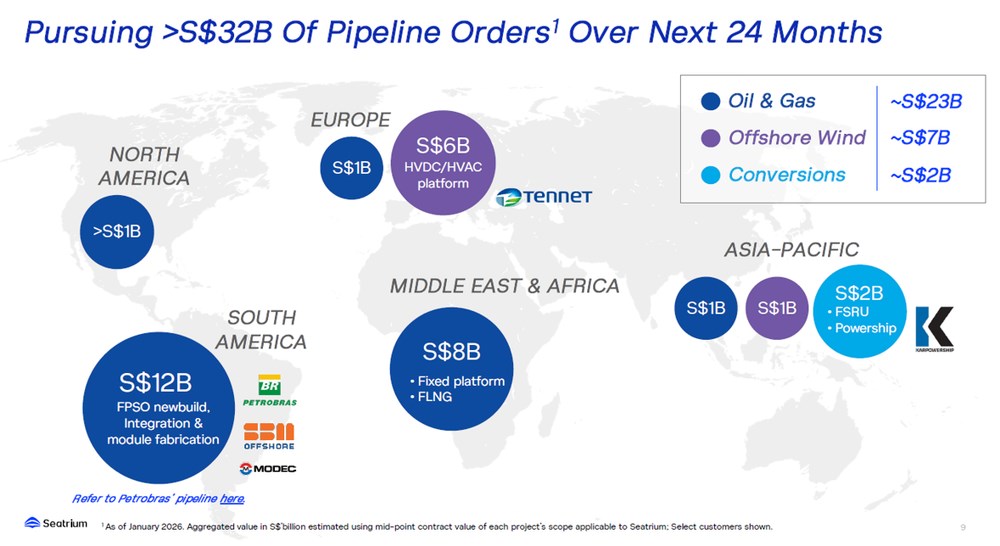

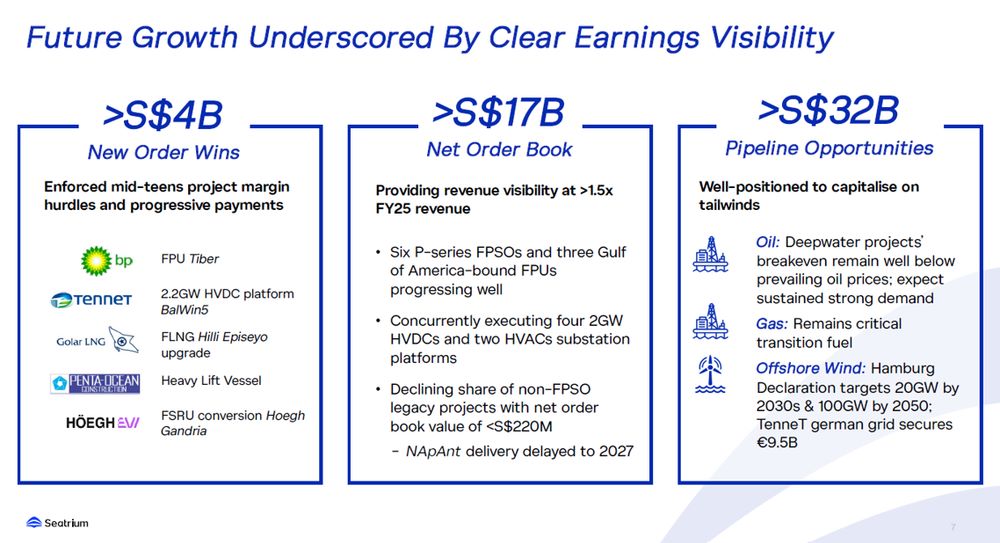

#3 - Seatrium has more than S$28 billion in pipeline opportunities

Seatrium also highlighted more than S$28 billion in pipeline opportunities over the next 24 months.

These opportunities are diversified across oil and gas, offshore wind and conversion projects.

This provides some visibility that demand for offshore energy infrastructure remains active.

However, a pipeline is not the same as confirmed orders.

Customers remain disciplined in their capital allocation, with continued focus on project economics, capital efficiency and risk-sharing structures.

As a result, new order wins may still come through unevenly.

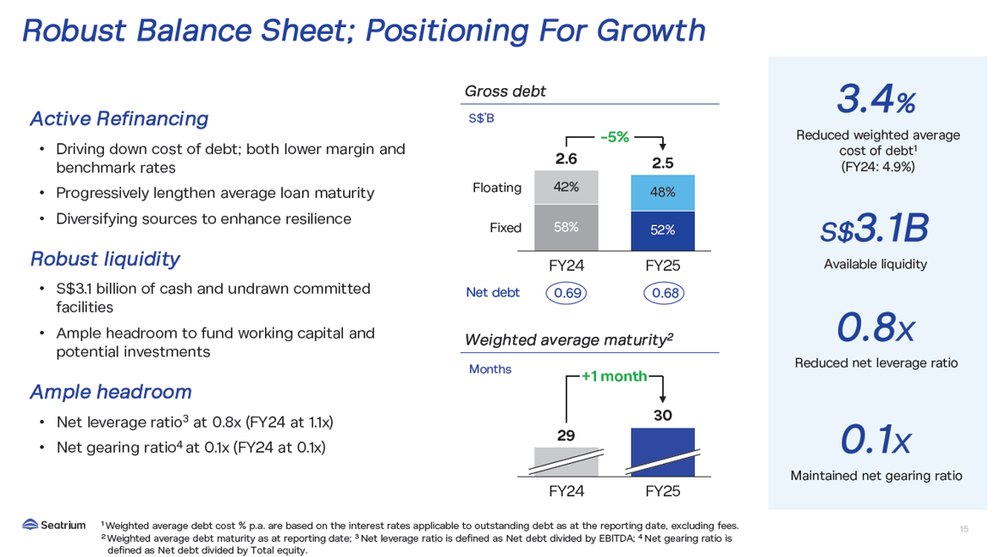

#4 - Seatrium has improved its financial flexibility

Seatrium’s balance sheet has also improved.

Net leverage declined to 0.8 times in FY2025, from 1.1 times in FY2024. Net gearing stood at 0.1 times.

Gross debt was reduced to S$2.5 billion, while refinancing efforts brought the cost of debt down to 3.4%.

Seatrium also launched a S$3 billion Multicurrency Debt Issuance Programme, with its inaugural S$400 million bond issuance attracting strong institutional demand.

This gives the group more financial flexibility to support future project wins and manage working capital needs.

Is Seatrium attractive after its share price decline?

Seatrium’s recovery appears to be moving in the right direction.

The company has a sizeable order book, improving margins, better cash flow generation and a cleaner balance sheet.

At around S$2.01, the stock trades at about 16 times FY2026 estimated earnings and around 13 times FY2027 estimated earnings.

This may look reasonable if management can continue to improve margins and convert pipeline opportunities into actual orders.

However, investors may still want to see clearer proof of three things.

First, Seatrium needs to replenish its order book after the decline in 1Q2026.

Second, gross margin improvement needs to translate into stronger net profit and cash flow.

Third, ROE needs to improve from current levels to show that the business is generating better returns on shareholders’ capital.

Until then, Seatrium may remain a recovery story that requires patience.

Key risks to watch for Seatrium

#1 - Legacy legal exposure

Seatrium has made progress in resolving legacy legal issues, but the overhang has not been fully removed.

Operation Car Wash required a total settlement outflow of around S$172 million in FY2025. Separately, a Keppel arbitration claim of approximately S$68 million remains outstanding.

While the bulk of this overhang has been resolved, residual legal risk is not fully eliminated.

Any unexpected development could affect investor sentiment or cash flow.

#2 - Order book replenishment

Seatrium’s order book remains sizeable, but replenishment will be important to watch.

Its net order book moderated from S$23 billion to S$17.8 billion in 2025, as order wins of about S$4 billion fell short of the company’s revenue run-rate.

By the end of 1Q2026, its net order book had declined further to S$15.5 billion.

This still provides revenue visibility through to 2033, but investors may want to see stronger order wins in the coming quarters.

While Seatrium has a large project pipeline, order conversion can be lumpy.

It also depends on oil prices, customer final investment decisions, project economics and financing conditions.

Source: Seatrium Limited 1Q2026 Announcements & Media Releases

#3 - Oil price sensitivity

Seatrium remains exposed to the offshore energy cycle.

Seatrium's order wins have historically had a correlation of around 0.74 with oil prices.

This means that a sustained decline in oil prices could delay project sanctions and slow order book replenishment.

Even if long-term demand for offshore energy infrastructure remains intact, weaker oil prices could make customers more cautious about committing to new projects.

This may affect the timing of new contract awards.

#4 - Cost and foreign exchange risks

Seatrium's large engineering, procurement, construction and installation (EPCI)-style contracts

These contracts can be exposed to steel cost inflation, labour cost pressures and foreign exchange movements.

Maybank estimates that a 5% rise in steel costs could reduce Earnings before interest, taxes, depreciation and amortisation (EBITDA) by approximately S$57 million to S$86 million.

A weaker US dollar against the Singapore dollar could also affect earnings, given the currency exposure in offshore and marine projects.

This makes cost control, hedging and project execution discipline important for Seatrium’s margin recovery.

What would Beansprout do?

In my view, Seatrium is a recovery stock worth watching, but I would not view it as a simple turnaround story yet.

The positives are clearer now.

Seatrium has a S$15.5 billion order book, improving margins, better cash flow generation and more than S$28 billion in pipeline opportunities.

The balance sheet also looks healthier after several years of restructuring.

However, I would still want to see clearer progress in new order wins, ROE improvement and sustained cash flow generation.

The stock may be a potential candidate for the Opportunity Pot within Beansprout's four pots of wealth, but only for investors who are comfortable with a multi-year recovery story and the risks that come with it. Learn more about how I invest with clarity with Beansprout's four pots of wealth here.

In the meantime, I would continue to monitor Seatrium progress and before initiating exposure as Seatrium passes three of our four screening factors, with ROE as the one area still in recovery mode. Size and liquidity, revenue and earnings momentum, and balance sheet strength all look acceptable.

For now, I would keep Seatrium on the watchlist rather than rush to increase exposure.

The next key update to watch would be whether Seatrium can show stronger order replenishment and further margin improvement in its upcoming results.

The pace of new order wins will be critical to watch, and FY2026 revenue may dip slightly before recovering from 2027 onwards. The residual Keppel arbitration claim and ongoing exposure to oil price movements are also worth keeping in mind.

Learn more about Seatrium here.

If you are looking for more Singapore stock ideas linked to long-term growth themes, you can explore our high-conviction curated stock opportunities here.

You can also screen for stocks that meet Beansprout’s 4-factor Opportunity framework here.

If you prefer broad exposure to blue chips without picking individual names, you can learn more about the Straits Times Index (STI).

Would you consider Seatrium as an opportunity stock at current prices, or would you wait for more clarity from the August results? Share with us in the comments below or in our Telegram group!

Planning to invest in Seatrium? Compare the best Singapore brokers to find the right trading platform, and see the latest promotions and sign-up rewards available.

Follow Beansprout on YouTube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments