3 best-performing Singapore blue chip stocks in February. Can the rally continue?

Stocks

By Gerald Wong, CFA • 11 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

We look at the top three Singapore blue chip stocks in February 2026. With gains of 13% or more in February, we find out if their rally can be sustained.

What happened?

Singapore stocks remained firm in February 2026.

More recently, however, market sentiment has become less straightforward.

We highlighted in our latest review of DBS, UOB and OCBC that Singapore bank shares have pulled back from earlier highs amid renewed market volatility linked to the escalation in the Middle East conflict.

Against this backdrop, the February blue chip outperformers were also different from the 3 best-performing Singapore blue chip stocks in January 2026.

In this article, we examine the 3 best-performing Singapore blue chip stocks in February 2026, and whether their earnings momentum, order visibility and dividend outlook are strong enough to support the rally.

3 best-performing Singapore blue chip stocks in February 2026

#1 – Yangzijiang Shipbuilding (Holdings) Ltd (SGX: BS6)

Yangzijiang Shipbuilding is one of Asia’s leading shipbuilders, with a core focus on containerships and tankers, while also earning a smaller stream of charter income from its shipping segment.

The stock has also been one of the strongest performing blue chips since February 2026. As of 28 February 2026, Yangzijiang Shipbuilding’s share price was S$4.34, representing a month-to-date gain of 29.9 percent.

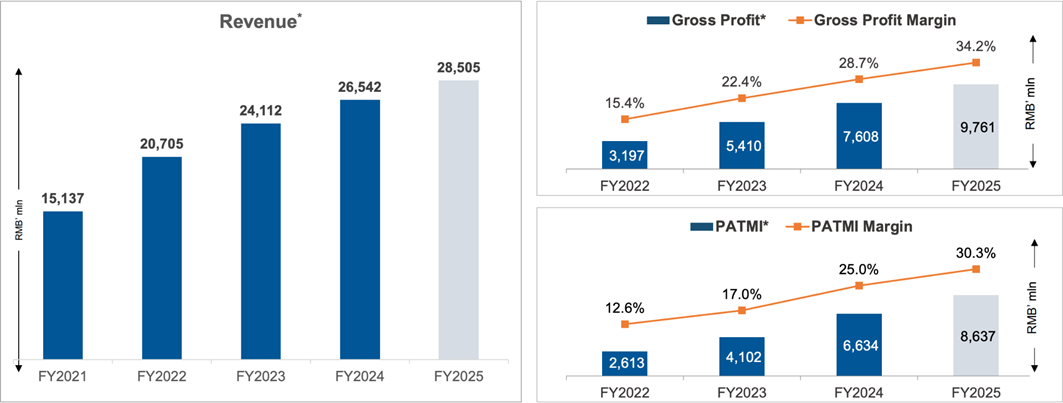

The rally was sparked by Yangzijiang’s record FY2025 results.

For the year, revenue rose 7.4 percent year on year to RMB28.5 billion, while profit attributable to shareholders jumped 30.3 percent to RMB8.6 billion.

Operationally, the group met its delivery target of 56 vessels in FY2025. It also secured US$2.5 billion of new orders during the year, ending with an outstanding order book of US$22.4 billion. This provides strong earnings visibility for the next few years.

Profitability also improved meaningfully.

Management said gross margin expanded on the back of lower steel costs and better pricing for newbuild contracts. Gross margins of around 35 percent are exceptionally high by historical standards, and management described this as a rare upcycle.

For now, it expects margins at this level to be sustained through 2026 and 2027, barring any major swings in steel prices or the US dollar against the renminbi.

The sharp share price move in February was not just about headline earnings.

Yangzijiang also hit a record intraday high and became the most actively traded stock after its results, reflecting strong investor interest in the shipbuilding cycle and the group’s earnings visibility.

Beyond the near term, the company is also pressing ahead with capacity expansion.

Construction of the Hongyuan Yard remains on track, with preliminary shipbuilding work starting in 1Q 2026. This is expected to add about 5 percent capacity in the near term, with the full yard potentially lifting capacity by around 20 percent from 2027.

At the same time, management appears to be taking a more measured approach to new orders.

Its FY2026 order win target of 4.5 billion yuan suggests that profitability and execution are being prioritised over chasing volume.

Yangzijiang is also positioning itself for the shift towards greener vessels. Green vessels now make up 71 percent of its outstanding order book by value, with containerships still the dominant vessel type. This suggests demand is increasingly moving towards more fuel efficient, next generation ships.

That said, investors are still watching policy and geopolitical risks closely.

Proposed US port fees on Chinese built or Chinese operated ships have caused sharp swings in Yangzijiang’s share price, showing that sentiment can remain volatile even when the company’s fundamentals stay strong.

On dividends, Yangzijiang raised its dividend payout ratio to 50% and proposed a dividend of 20 Singapore cents per share for FY2025, up from 12 cents in FY2024.

Based on the share price of S$4.34, the consensus dividend of 21.4 cents implies a dividend yield of about 4.9%.

Find out how much dividends you would have received as a shareholder of Yangzijiang Shipbuilding (Holdings) Ltd in the past 12 months with the calculator below.

Related Links:

- Yangzijiang Shipbuilding (Holdings) Ltd share price history and share price target

- Yangzijiang Shipbuilding (Holdings) Ltd dividend forecast and dividend yield

#2 – Keppel Ltd (SGX: BN4)

Keppel is a global asset manager and operator with businesses across Infrastructure, Connectivity and Real Estate. Over the past few years, it has been shifting towards a more asset-light model by growing funds under management and recycling capital from mature assets into new opportunities.

The stock was also one of the strongest performing blue chips in February 2026. As of 28 February 2026, Keppel’s share price stood at S$13.08, representing a month-to-date gain of 19.7 percent from S$10.93.

The rally followed a strong set of FY2025 results. Excluding its non-core assets held for divestment and discontinued operations, Keppel said net profit rose 39 percent year on year to S$1.1 billion, with all three business segments contributing to the improvement.

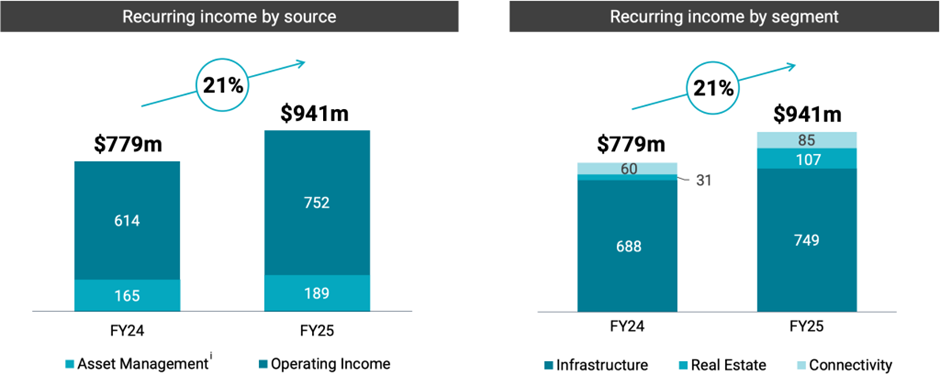

Recurring income also continued to grow, rising 21 percent year on year to S$941 million in FY2025. This reflects Keppel’s ongoing shift towards more stable fee-based and operating income.

Its asset management platform remains an important growth driver. Funds under management increased to S$95 billion at the end of 2025, up from S$88 billion a year earlier, and management said it remains on track to reach S$100 billion by end-2026.

Beyond earnings, capital recycling remains a key part of the investment story. Keppel announced about S$2.9 billion of divestments in 2025, taking cumulative monetisation proceeds higher since the programme began in 2020.

Its non-core portfolio earmarked for divestment stood at about S$13.5 billion, with management targeting substantial monetisation by 2030. The proceeds are expected to support debt reduction, fund growth investments, and underpin shareholder returns.

Keppel has also continued returning capital through buybacks. Since launching its S$500 million share buyback programme in July 2025, the group had repurchased about S$116 million worth of shares as of end-2025.

On the governance front, Keppel announced that Piyush Gupta will be appointed non-executive chairman after the AGM on 17 April 2026, replacing Danny Teoh, who will retire. Management said Piyush has already been actively involved with the board since joining in July 2025 and has helped sharpen the group’s strategic direction.

On dividends, Keppel proposed a total FY2025 dividend of about 47 cents per share, up from 34 cents in FY2024. This comprises ordinary cash dividends of 34 cents per share, and a special dividend of about 13 cents per share, funded by asset monetisation proceeds.

Based on the share price of S$13.08, the consensus dividend of 45.7 cents implies a dividend yield of about 3.5%.

Find out how much dividends you would have received as a shareholder of Keppel Ltd in the past 12 months with the calculator below.

Related Links:

- Keppel Ltd share price history and share price target

- Keppel Ltd dividend history and dividend forecast

#3 – Seatrium Limited (SGX: 5E2)

Seatrium is a Singapore-based offshore, marine and energy engineering group. It builds offshore production platforms, floating production storage and offloading (FPSOs) and offshore wind vessels, while also providing repair and upgrade services.

The stock was also one of the strongest performing blue chips in February 2026. As of 28 February 2026, Seatrium’s share price stood at S$2.40, representing a month-to-date gain of about 13.7 percent from S$2.11.

The rally came after Seatrium reported a sharp improvement in FY2025 results. Revenue rose 24 percent year on year to S$11.5 billion, while net profit more than doubled to S$324 million, helped by margin expansion and lower net finance costs.

Management said the stronger performance was supported by higher revenue recognition from both the Oil and Gas and Offshore Wind segments. Oil and Gas revenue increased to S$8.1 billion in FY2025, while Offshore Wind continued to contribute to overall growth.

Seatrium also entered 2026 with a strong order book. Its net order book stood at more than S$17 billion, equivalent to over 1.5 times FY2025 revenue, which provides earnings visibility over the next few years.

Importantly, management highlighted that 95 percent of the order book now comprises series-build projects, which carry lower execution risk. Non-FPSO legacy projects now make up just over 1 percent of the order book, while remaining US exposure has been reduced to less than S$10 million.

The group has also been working to improve its cost base. Divestments of non-core assets, including the Amfels yard, GNL vessels, Karimun yards, tugboats and floating docks, are expected to deliver more than S$50 million in annualised cost savings, with most of this flowing through cost of sales.

These divestments are also expected to unlock more than S$230 million in gross gains and over S$330 million in cash proceeds. Around S$70 million in gains was recognised in FY2025, with another S$150 million expected to be recognised in FY2026 as the remaining transactions are completed.

Looking further ahead, management has identified more than S$200 million of additional non-core assets for divestment by 2028, and expects cumulative cost savings to exceed S$100 million by FY2028.

Seatrium has also removed a key overhang on sentiment after resolving its dispute with Maersk over a terminated offshore wind vessel contract. Under the settlement, Maersk agreed to pay the remaining contract value, including a portion structured as a long term credit arrangement, and both sides withdrew legal action.

Looking ahead, management said project margins are trending towards the mid teens. However, reported gross margins may move closer to, but not fully reach, 15 percent because of production overheads from some underutilised capacity.

On dividends, Seatrium proposed a final cash dividend of 3.0 cents per share for FY2025, up from 1.5 cents in the previous year. Based on the share price of S$2.40, the consensus dividend of 4.2 cents implies a dividend yield of about 1.8%.

Find out how much dividends you would have received as a shareholder of Seatrium Limited in the past 12 months with the calculator below.

Related Links:

- Seatrium Limited share price history and share price target

- Seatrium Limited dividend history and dividend forecast

What would Beansprout do?

The best-performing Singapore blue chips in February 2026 were no longer the property names.

Instead, Yangzijiang Shipbuilding, Keppel Ltd., and Seatrium led the market higher, reflecting improving sentiment towards the shipbuilding and offshore marine cycle.

In different ways, all three are benefiting from similar themes, including better order visibility, stronger execution, and a recovery in offshore and marine activity after several volatile years.

The rally has also been supported by company-specific drivers such as capacity expansion, capital recycling, and improving margins.

| Stock | The good | Key risks |

| Yangzijiang Shipbuilding | • Forward dividend yield about 4.9% • Strong order book and higher margins lifted earnings • Increasing exposure to green vessels supports longer-term demand | • Earnings may remain cyclical • Sensitive to global economic growth and trade activity |

| Seatrium | • Earnings improved with stronger margins • Higher order book compared to previous year • Earnings base becoming more recurring as asset management grows | • Earnings depend on offshore and marine cycle • Execution risks on order book delivery |

| Keppel Ltd. | • Dividends and share buybacks support shareholder returns • Decent dividend yield about 3.5% | • Share price prone to profit taking with strong performance in past year |

For investors seeking income, Yangzijiang Shipbuilding stands out among the three, with a consensus forward dividend yield of about 4.9%.

The higher dividend payout is supported by its strong order book, while earnings have grown over the past year on the back of improved margins.

However, investors should note that Yangzijiang's future earnings may remain cyclical, as shipbuilding demand tends to be sensitive to global economic growth and trade activity.

Similarly, Seatrium’s earnings are also cyclical as they depend on conditions in the offshore and marine sector, and the company continues to face execution risks relating to the delivery of its order book. Seatrium also offers the lowest dividend yield of the 3 names.

For investors looking at longer-term opportunities, Keppel may stand out as its earnings base is becoming more recurring as its asset management platform grows.

Capital recycling remains central to the story, and recent dividends and share buybacks highlight management’s focus on shareholder returns.

Following the recent pullback in its share price amid market volatility linked to the Iran conflict, Keppel could be worth watching for investors who believe in its longer-term transformation. Its dividend yield is about 3.5% based on FY2026 consensus estimates.

You can also learn more about how shifting economic drivers are broadening opportunities beyond Singapore blue chips here.

If you’d like to screen for other Singapore stocks with attractive dividend yields and potential upside, you can explore our Singapore dividend stocks screener.

If you prefer broad exposure to blue chips without picking individual names, you can also learn more about the Straits Times Index (STI).

Check out the best stock trading platforms in Singapore with the latest promotions to invest in Singapore blue chip stocks.

Enjoyed this insight? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments