Singapore REITs pull back as interest rates rise. Are they a buying opportunity?

REITs

By Gerald Wong, CFA • 28 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

Singapore REITs have pulled back as interest rates rise. We break down what is happening, what to watch next, and whether the pullback could create selective buying opportunities.

What happened?

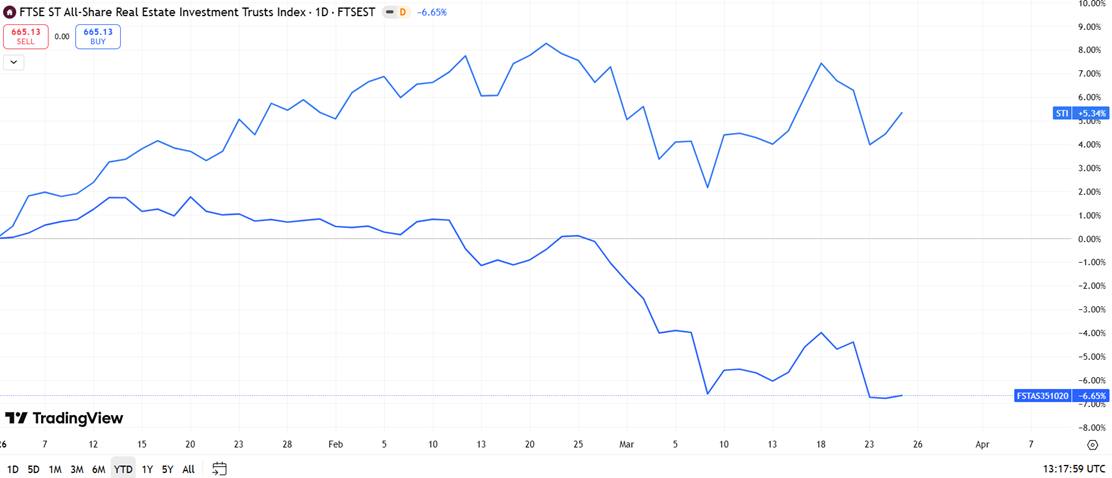

Singapore REITs have been under pressure in March 2026.

Recently, we have also seen a jump in the 6-month Singapore T-bill yield.

This has led to a 7% decline in an index of Singapore REITs has declined by 7% so far this month, compared to the 2% pullback in the Straits Times Index (STI) (as of 26 March).

With the fall in the share prices of Singapore REITs, I saw a question in the Beansprout Telegram group asking about my thoughts on Singapore REITs.

After all, the correction in the share price of Singapore REITs has also led to more attractive valuations, with some REITs offering a dividend yield of 6% and above.

In this article, we take a deeper look at what the rise in interest rates mean for Singapore REITs, what are the fundamentals of different sectors, and if they are worthwhile buying.

Why are S-REITs falling in March 2026?

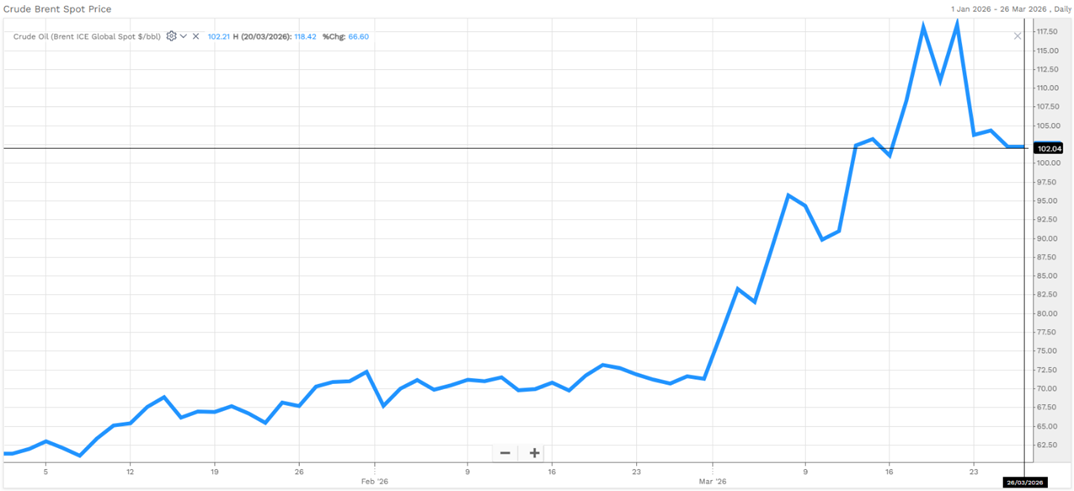

#1 - Oil prices surged above US$110/bbl amid structural supply disruption that could last till 2028.

The closure of Straits of Hormuz has increased concerns about tightening global supply. This is compounded by missile damage to critical LNG infrastructure in Qatar, which could deepen the disruption over a longer period of time.

As oil prices affect the price of goods and services on a broader scale, the fear of prolonged high oil prices drove up inflation expectation.

On 23 March 2026, brent crude soared 58% month-to-date to a high of US$114/bbl .

If oil prices remains elevated for a prolonged period, it will lead to higher inflation. Risk of rising inflation could drive Central Banks to hike interest rates in order to keep their targeted inflation rate.

#2 - Rising U.S. 10-year Treasury bond yield reflects moderation of rate cut expectations

In fact, that was the message from US Federal Reserve at the Fed meeting on 18 March 2026. The US Federal Reserve kept Fed Funds Rate unchanged at 3.5 to 3.75%, as widely expected by investors.

This follows its stance of maintaining rates unchanged in the January meeting, after cutting interest rates by three times in 2025.

More importantly, Fed Chairman Jerome Powell sent a caution message on inflation expectations. The Fed now expects personal consumption expenditures (PCE) inflation to be 2.7% in 2026, higher than the earlier estimate of 2.4%.

Core inflation, which excludes food and energy, is also expected to be 2.7%, up from 2.5%. Inflation is now expected to come down more slowly, with projections for it to reach 2.2% in 2027 and return to the Fed’s 2% target by 2028.

The Federal Reserve has signalled a more cautious path for rate cuts in 2026.

The dot plot, which shows the projections of Fed officials, indicates that most officials expect rates in 2026 to be between 3.25% and 3.50%, implying potentially one rate cut this year. While the median has not changed, some officials are now expecting fewer numbers of cuts. Four or five officials went from expecting two rates cuts in 2026 to expecting just one rate cut.

Similarly, Bank of England held interest rates unchanged at the meeting on 19 March 2026, compared to the earlier expectation of one rate cut. Policy makers also warned of rising inflation and slowdown in economic growth caused by the oil shock.

The Fed’s more cautious tone has pushed US government bond yields higher, with the 10-year yield rising above 4% and reaching about 4.34% by 23 March 2026.

When returns on safer investments like government bonds increase, S-REITs tend to look less attractive in comparison.

To stay competitive, REITs would need to offer higher yields, which usually happens when their prices fall.

In Singapore, the 10-year government bond yield has risen by about 33 bps month-to-date to 2.29%, as at 26 March 2026.

#3 - Funding cost may rise again

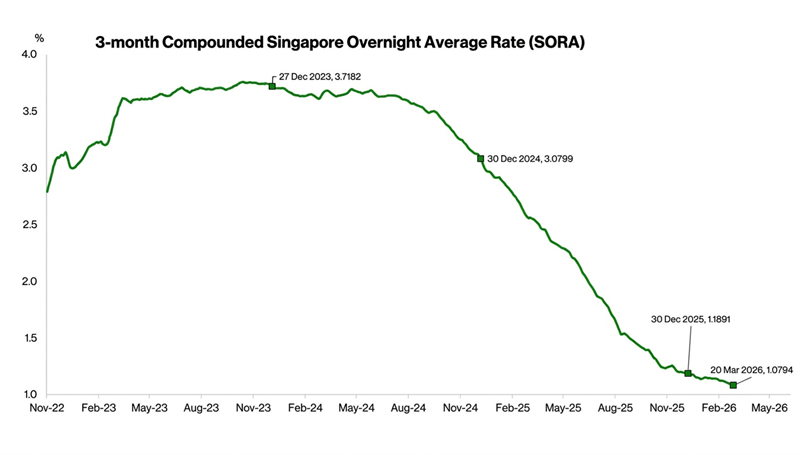

In 2025, S-REITs benefited from the sharp decline in 3-month SORA, the benchmark rate used for much of their borrowing.

As the Fed began cutting rates in late 2024, 3-month SORA fell to around 200 bps in 2025. This helped lower interest expenses, supporting higher distributable income and distributions.

Looking ahead, the outlook may become less favourable if interest rates move higher again. If inflation remains elevated, central banks may keep rates higher for longer or even raise them further.

In such a scenario, S-REITs could face higher refinancing costs over time.

Does the current pullback in REIT prices offer an attractive entry point?

With uncertainty around interest rates, the near-term outlook for S-REITs may be more challenging, and a broad recovery across the sector is less likely. Investors may need to be more selective.

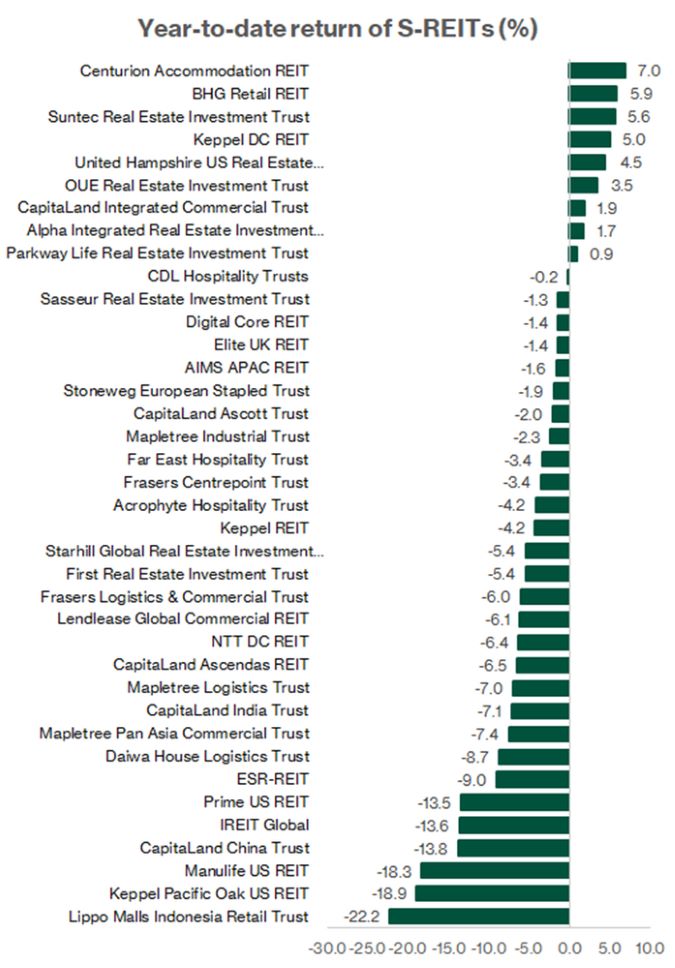

As shown in the chart below, there has been a significant divergence in the year-to-date performance of Singapore REITs.

In this environment, REITs with stronger assets and more stable demand may hold up better. This includes those focused on Singapore office, logistics, data centres and purpose-built accommodation.

Investors may also want to look for REITs that can maintain or grow their distributions through actions such as improving existing properties, making acquisitions or achieving higher rents.

Returns are likely to vary depending on the type of assets they own, where they operate, how their debt is structured and how well management executes.

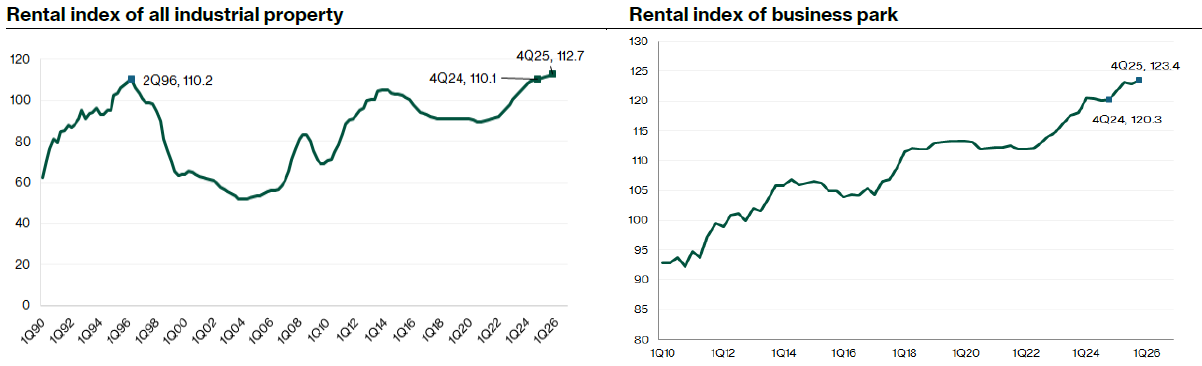

Fundamentals of selective sectors remain resilient as of 4Q25

Based on the key operating metrics as of end-4Q 2025, we believe the fundamentals of selective sectors remain resilient.

Singapore REITs reported 4Q25 results, extending the trend of higher year-on-year distribution per unit (DPU) led by lower interest costs.

Capitaland Integrated Commercial Trust issued long-tenor notes at 2.25%, well below its average cost of debt of 3.3% in 3Q2025. The interest savings flow directly into the distribution to unitholders. Capitaland Integrated Commercial Trust reported FY2025 distributable income increased by 14.4% year-on-year as cost of debt declined to 3.2%, from 3.6% in FY2024. Interest expense fell 8.9% year-on-year to S$314.7 million.

Keppel DC REIT's average cost of debt fell to 2.8% in 4Q2025, from 2.9% in 3Q25. CapitaLand Ascendas REIT maintained an average debt cost of 3.5% in FY2025, down from 3.7% in FY2024. These developments signalled that the debt market was strongly supportive of REIT refinancing and growth.

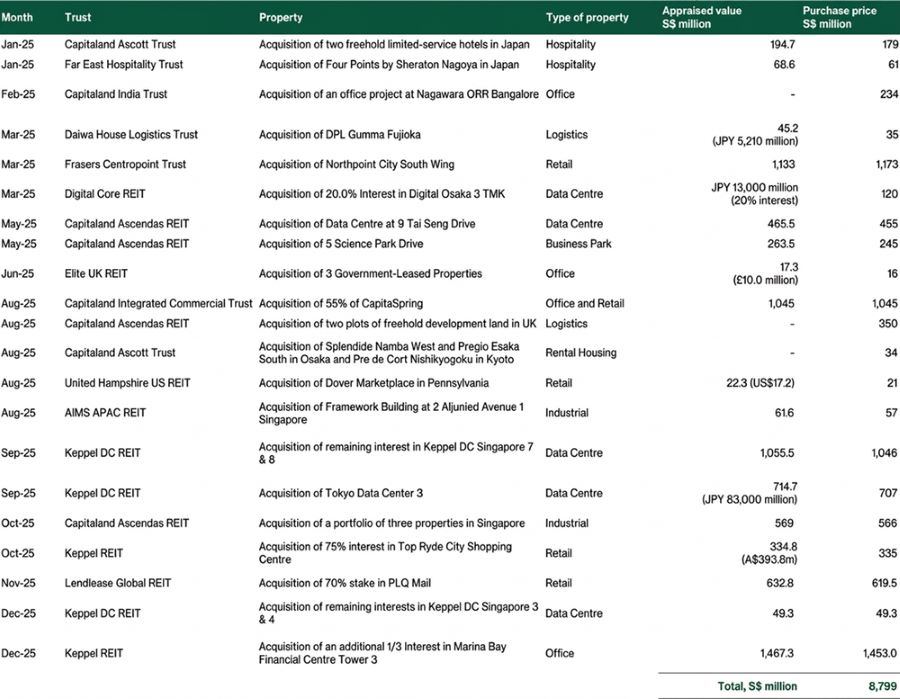

As capital market conditions improved significantly, the REITs took the opportunities to implement their acquisition plans in 4Q25. For the full year 2025, total value of acquisitions announced was about S$8.8 billion. Of which, S$3.0 billion were announced in 4Q25 with sizable acquisitions by Keppel DC REIT and Keppel REIT.

Data centre was the standout sector

The data centre sub-sector delivered the strongest results in FY2025, driven by structural demand from AI workloads and cloud computing.

Keppel DC REIT reported FY2025 gross revenue growth of 42.2% year-on-year and NPI growth of 47.2%, supported by acquisitions of Tokyo Data Centre 3 and full ownership of several Singapore data centre assets.

Full-year DPU rose 9.8% to 10.381 cents despite an enlarged unit base following a S$404.5 million preferential offering. Portfolio rental reversions for the year were approximately 45%, reflecting exceptional pricing power.

Portfolio occupancy remained healthy at 95.8% with a weighted average lease expiry of 6.7 years, and rental income from hyperscalers increased to 69.3% of total revenue. Management divested non-core assets in Germany and Malaysia as part of its hyperscale-focused repositioning strategy.

Digital Core REIT posted a 72% surge in revenue for FY2025. The REIT maintained near-full occupancy of 97% and assets under management of US$1.8 billion.

FY2025 DPU held steady at 3.60 US cents. Wholesale data centre pricing in Northern Virginia climbed to approximately US$225 per kilowatt per month, increase by 7% year-on-year. Shifting to an expansion strategy, it plans to double its US$1.8 billion asset base within the next three years.

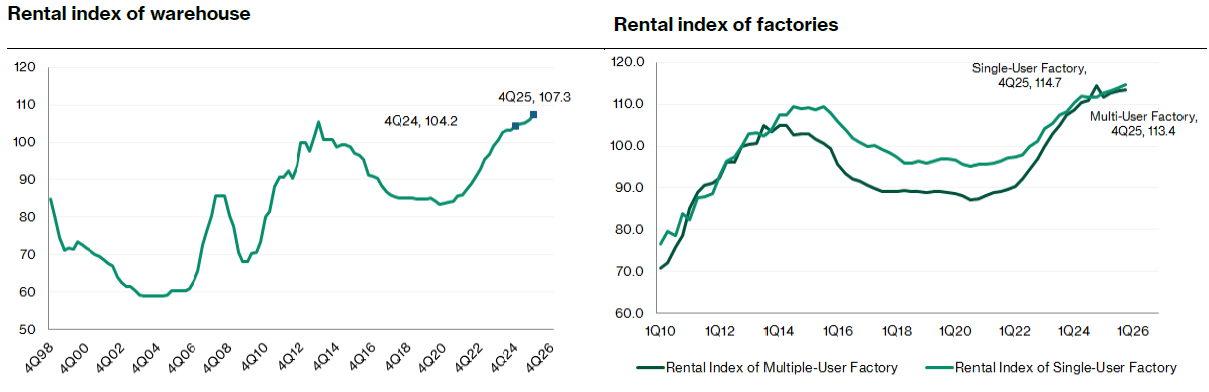

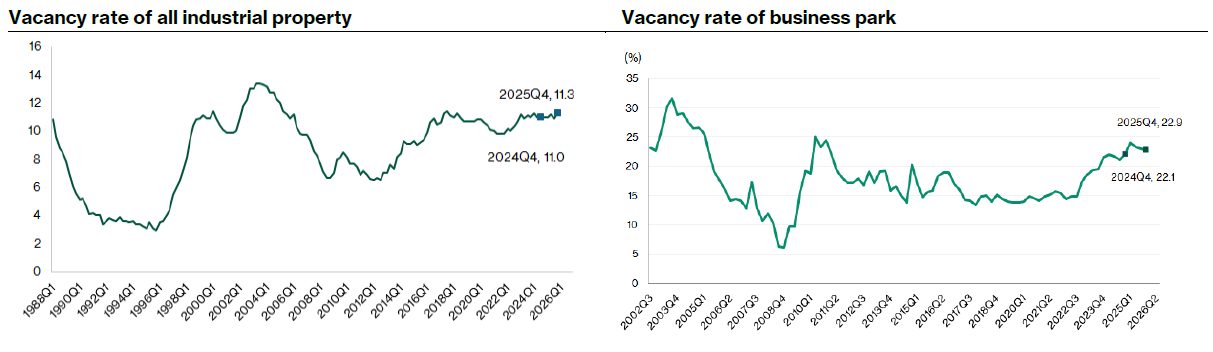

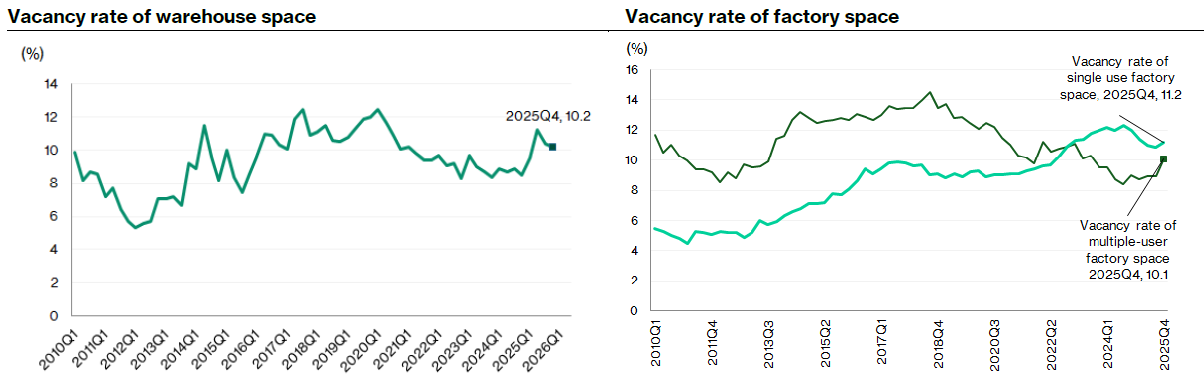

Industrial REITs delivered steady but mixed results

Industrial REITs maintained their resilience, particularly their Singapore industrial assets, though leasing activities in China remains subdued.

CapitaLand Ascendas REIT (CLAR), Singapore's largest industrial landlord, reported FY2025 DPU of 15.005 cents, down 1.3% year-on-year, primarily due to an enlarged unit base following a S$500 million equity fundraising. Portfolio occupancy stood at 90.9% as at end-December 2025.

Rental reversions were strong at 12.0% for FY2025, accelerating to 19.6% in 4Q2025. CLAR acquired S$1.47 billion in new assets across Singapore and the US at NPI yields of 6.1–7.6%, while divesting S$506.5 million at a 9% premium to valuation.

Mapletree Logistics Trust (MLT) reported less favourable rental reversion at 1.7% in 3QFY26 (3QFY25: 5.4%), excluding China. Potentially reflecting a gradual recovery, negative rental reversion from the Chinese market has moderated to 2.2% (3QFY25: -10.2%).

Portfolio occupancy improved to 96.4% as at 31 December 2025, from 96.1% as at 30 September 2025, driven by improvements in Singapore, Japan, and South Korea. In Singapore, Mapletree Joo Koon Logisitcs Hub continued to see strong leasing momentum.

Mapletree Industrial Trust (MINT) 3Q FY2025/26 DPU declined 7.0% year-on-year as North American lease non-renewals and FX headwinds took effect.

MINT outlined plans to divest up to S$600 million of North American properties for portfolio rebalancing. For the Singapore portfolio, MINT achieved healthy positive rental reversion of 7.1% in 3QFY26. Portfolio occupancy for Singapore was stable at 93%.

Together, these results reaffirmed the strong underlying demand that continues to support industrial and data centre assets.

Industrial REITs have delivered some of the most resilient operating data in 4Q25. The JTC All Industrial Rental Index rose 0.5% q/q, matching the pace in 3Q2025 and extending the upcycle to a 21st consecutive quarter of increases.

Singapore-focused REITs benefited from strong domestic conditions

The Singapore retail and office sub-sectors continued to benefit from resilient domestic consumption, strong mall traffic, and healthy leasing demand in the CBD.

CapitaLand Integrated Commercial Trust (CICT) delivered what may be the most impressive set of results among large-cap S-REITs. FY2025 gross revenue rose 2.1% to S$1,619.2 million, NPI rose 3.1% to S$1.18 billion, and DPU increased 6.4% to 11.58 cents.

The 2H2025 DPU surged 9.4% year-on-year to 5.96 cents. Growth was driven by the full-year consolidation of ION Orchard, the CapitaSpring step-up acquisition, and stronger existing property performance. Retail tenant sales surged 19.2% year-on-year in 3Q2025, and both retail and office portfolios maintained occupancy above 96–97%.

CICT took advantage of the debt market to issue long-tenor notes at just 2.25%. The REIT also divested Bukit Panjang Plaza for S$428 million at a 10% premium to valuation and a 165% premium over its original purchase price. Aggregate leverage remained comfortable at 38.6%.

Suntec REIT posted a strong set of full-year results, with gross revenue and NPI both rising approximately 1.7–1.9% year-on-year, while distributable income to unitholders jumped 14.6% to S$207.3 million. The improvement was driven by a stronger Singapore portfolio—with office occupancy at 98.5% and rent reversions of +8.5%—and meaningfully lower financing costs.

Full-year DPU climbed 12.5% year-on-year. However, the Australian office portfolio continued to weigh on results, and aggregate leverage edged up to 41.5% in 4Q2025.

Keppel REIT delivered an encouraging full year, with NPI rising 6.9% year-on-year, though DPU slipped due to a higher unit base.

The most significant development was its acquisition of a one-third interest in Marina Bay Financial Centre Tower 3 for S$1.45 billion, which significantly strengthens its CBD office footprint. Singapore CBD office demand remained robust.

Frasers Centrepoint Trust (FCT) reported strong results for its FY2025 (ended September 2025), with NPI rising 9.7% to S$277.9 million, driven by the acquisition of additional interest in Northpoint City South Wing and AEI-driven improvements at Tampines 1. Committed occupancy was 99.5%.

Office properties within Singapore also held up well, with Grade A CBD properties continuing to see healthy leasing demand and modest increase in passing rents.

CapitaLand Integrated Commercial Trust (CICT) delivered a stable set of results, with FY2025 net property income rising 1.6 per cent year-on-year and occupancy improving to more than 97 per cent. CICT took advantage of the improved debt market to issue a S$300 million in 7-year at fixed rate of 2.25 per cent, well below its historical cost of debt, underscoring its strong market access. The consolidation of CapitaSpring further strengthened its position in the Grade A CBD.

Keppel REIT delivered one of the more encouraging updates among the office-heavy REITs. Occupancy rose to 96.3 per cent, driven by strong demand for prime CBD space rents. Borrowing costs also improved to 3.41% for FY2025, from 3.45% for 9MFY25. The most significant development was its proposed acquisition of a 75 per cent stake in the Top Ryde City Shopping Centre in Sydney, a suburban retail asset with stable, essential-services anchors. The acquisition is expected to be DPU-accretive and adds income diversification, signalling Keppel REIT’s shift from defensive positioning to selective, growth-oriented capital deployment.

OUE REIT delivered a steady quarter with higher revenue and NPI from its Singapore assets, supported by stronger performance at Mandarin Orchard and its office properties. Financing costs fell meaningfully due to proactive refinancing, improving distributable income despite softer conditions in parts of the hospitality segment. OUE REIT reported 2H25 revenue and NPI increase of 2.9% and 5.2% year-on-year, on a like-for-like basis. Supported by firm office leasing and a recovery in hospitality performance. As at end-December 2025, office committed occupancy remained high at 95.4%, average passing rents increased to S$10.97 psf, and rental reversions stayed robust at 8.8% in 4Q25 (9.1% for FY25), reflecting sustained flight-to-quality demand for prime CBD offices. 2H25 DPU at 1.25 cents, an increase of 10.6% year-on-year. With astute capital management, the REIT successfully lowered its weighted average cost of debt to 3.9% in 4Q25, from 4.1% in 3Q25.

Overseas-focused S-REITs delivered a mixed set of results

Currency volatility and divergent market conditions drove wide performance differences among S-REITs with overseas assets.

CapitaLand China Trust (CLCT) faced a challenging year. Gross revenue fell 9.1% year-on-year to RMB 1,670 million, and NPI dropped 9.4%. Full-year DPU declined 14.7% to 4.82 cents, including a S$5.7 million distribution top-up from prior divestment gains.

Excluding this top-up, underlying DPU was down approximately 20.5%. The decline was attributed to the divestment of CapitaMall Yuhuating, asset enhancement initiatives downtime, and weaker occupancy and rents. On the positive side, CLCT increased its RMB-denominated debt from 35% to 60%, reducing interest costs by 8.1% and improving its natural currency hedge.

First REIT saw its FY2025 DPU fall around 8% year-on-tear, largely due to the continued depreciation of the IDR and JPY against the SGD. Core healthcare assets continued to perform in local currency terms, but FX translation losses and a larger unit base more than offset the gains.

Elite UK REIT stood out among overseas-focused S-REITs, growing FY2025 DPU by 5.6% year-on-year to 3.03 pence. Revenue rose 1.3% to GBP 38.0 million. The REIT significantly derisked its rental profile by extending leases with its primary tenant, the UK Department of Work and Pensions, resulting in portfolio WALE improving sharply to 7.2 years. Analysts noted that improved cashflow visibility could support tighter credit margins from lenders and potential valuation uplift. The repositioning of Lindsay House in Dundee into a 170-bed purpose-built student accommodation is targeted for the 2027 academic year, offering strategic upside.

Increase in acquisition and divestment activities in 4Q25

On the acquisition front, CLAR led with S$1.47 billion in new assets. Keppel DC REIT followed with approximately S$1.1 billion of data centre acquisitions.

Keppel REIT's S$1.45 billion acquisition of a stake in MBFC Tower 3 was the largest single commercial deal of the quarter. CICT completed the consolidation of CapitaSpring to strengthen its Grade A CBD positioning.

Lendlease REIT also moved decisively to consolidate full ownership of PLQ Mall, acquiring the remaining 30% stake for S$100.8 million at a 2.2% discount to independent valuation, implying an NPI yield of approximately 4.5%.

Divestments were equally prominent. CLAR divested S$506.5 million of assets at premiums. CICT sold Bukit Panjang Plaza for S$428 million. CapitaLand India Trust sold CyberVale and CyberPearl at a premium to valuation, freeing capital for higher-yielding projects.

MIT outlined plans to divest up to S$600 million of North American data-centre properties. Keppel DC REIT divested its Kelsterbach Data Centre in Germany as part of its hyperscale-focused repositioning.

These moves underscore a continued emphasis on capital recycling, with managers increasingly willing to exit non-core or mature assets and redeploy proceeds into higher-conviction segments.

What would Beansprout do?

The recent rise in Singapore government bond and T-bill yields has started to weigh on S-REITs. When safer investments like T-bills offer higher returns, REITs become less attractive in comparison, which has led to a pullback in their prices.

This suggests that the near-term outlook may be more challenging, and investors may need to be more selective rather than expecting a broad recovery across the sector.

In this environment, REITs with stronger underlying assets may hold up better. These include those focused on Singapore office, logistics, data centres and purpose-built accommodation, where demand has been relatively more stable. REITs with overseas assets that actively manage currency risks may also be better positioned.

At the same time, many REITs have taken steps in recent years to manage their debt, such as locking in borrowing costs earlier and spreading out their loan repayments. This provides some support, but it may not fully offset the pressure from higher interest rates if they persist.

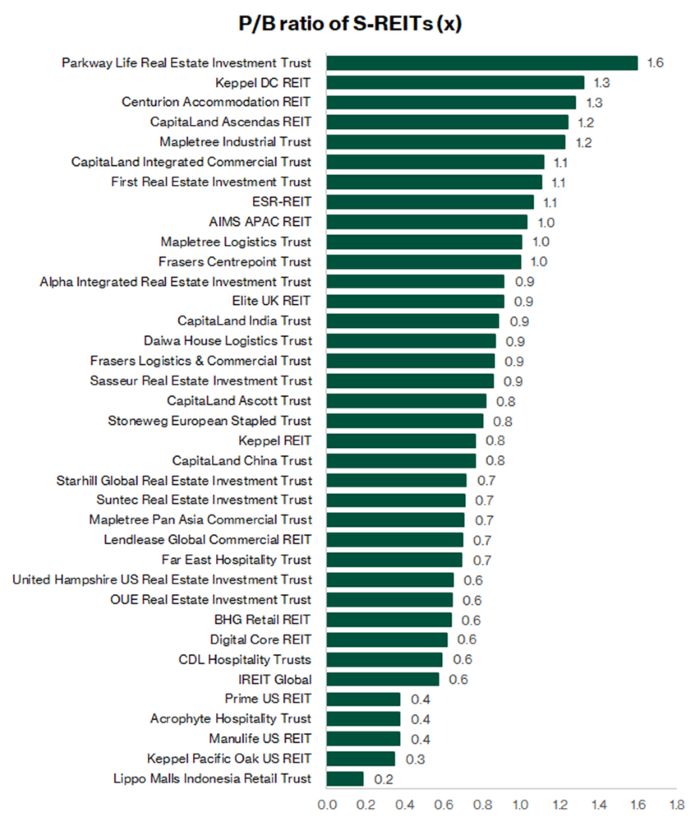

Valuations have also become more reasonable. The iEdge S-REIT index is trading at P/B 0.88x, lower than the 10-year historical average of 0.97x. Forward distribution yield has risen to 6.2%, in line with historical average.

In the current environment, investors may want to focus on REITs that can sustain and grow distributions through active portfolio management, such as asset enhancements, acquisitions and rental growth. Performance is likely to diverge based on sub-sector exposure, geographic mix, debt structure and execution capability.

For example, large-cap REITs like CapitaLand Integrated Commercial Trust stands out for their strong Singapore portfolio and acquisition track record, while Keppel DC REIT is positioned to benefit from structural demand in data centres.

Among mid-cap names, CapitaLand India Trust and Digital Core REIT offer exposure to growth markets, while AIMS APAC REIT and Parkway Life REIT have shown relatively resilient distribution growth.

Overall, Singapore REITs can still play a role in an income-focused portfolio, in our view. However, returns may be less consistent in the current environment, and investors may need to be more selective.

Which REIT is on your watchlist with the pullback in share prices? Share with us in the comments below or join the discussion in Beansprout telegram group.

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win 1g of gold bar. Promo ends on 31 March 2026. T&Cs apply. Learn more about the Longbridge promotion here.

To screen for Singapore REITs with lowest price-to-book valuation or highest dividend yield, check out our best Singapore REIT screener.

If you are new to investing in Singapore REITs, you can start to learn more about Singapore REITs here.

If you prefer diversification without picking individual REITs, you can also gain exposure through Singapore REIT ETFs.

Check out Beansprout guide to the best stock trading platforms in Singapore with the latest promotions to Singapore REITs Sector.

Download the full report here.

Enjoyed this insight? Follow Beansprout on Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Important Disclosures

Analyst Certification and Disclosures

The analyst(s) named in this report certifies that (i) all views expressed in this report accurately reflect the personal views of the analyst(s) with regard to any and all of the subject securities and companies mentioned in this report and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific views expressed by that analyst herein. The analyst(s) named in this report (or their associates) does not have a financial interest in the corporation(s) mentioned in this report.

An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Company Disclosure

Global Wealth Technology Pte Ltd (“Beansprout”) does not have any financial interest in the corporation(s) mentioned in this report.

Disclaimer

This report is provided by Beansprout for the use of intended recipients only and may not be reproduced, in whole or in part, or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set out herein.

You acknowledge that this document is provided for general information purposes only. Nothing in this document shall be construed as a recommendation to purchase, sell, or hold any security or other investment, or to pursue any investment style or strategy. Nothing in this document shall be construed as advice that purports to be tailored to your needs or the needs of any person or company receiving the advice. The information in this document is intended for general circulation only and does not constitute investment advice. Nothing in this document is published with regard to the specific investment objectives, financial situation and particular needs of any person who may receive the information.

Nothing in this document shall be construed as, or form part of, any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities. The data and information made available in this document are of a general nature and do not purport, and shall not in any way be deemed, to constitute an offer or provision of any professional or expert advice, including without limitation any financial, investment, legal, accounting or tax advice, and shall not be relied upon by you in that regard. You should at all times consult a qualified expert or professional adviser to obtain advice and independent verification of the information and data contained herein before acting on it. Any financial or investment information in this document are intended to be for your general information only. You should not rely upon such information in making any particular investment or other decision which should only be made after consulting with a fully qualified financial adviser. Such information do not nor are they intended to constitute any form of financial or investment advice, opinion or recommendation about any investment product, or any inducement or invitation relating to any of the products listed or referred to. Any arrangement made between you and a third party named on or linked to from these pages is at your sole risk and responsibility.

You acknowledge that Beansprout is under no obligation to exercise editorial control over, and to review, edit or amend any data, information, materials or contents of any content in this document. You agree that all statements, offers, information, opinions, materials, content in this document should be used, accepted and relied upon only with care and discretion and at your own risk, and Beansprout shall not be responsible for any loss, damage or liability incurred by you arising from such use or reliance.

This document (including all information and materials contained in this document) is provided “as is”. Although the material in this document is based upon information that Beansprout considers reliable and endeavours to keep current, Beansprout does not assure that this material is accurate, current or complete and is not providing any warranties or representations regarding the material contained in this document. All opinions contained herein constitute the views of the analyst(s) named in this report, they are subject to change without notice and are not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Any reference to past performance should not be taken as an indication of future performance. To the fullest extent permissible pursuant to applicable law, Beansprout disclaims all warranties and/or representations of any kind with regard to this document, including but not limited to any implied warranties of merchantability, non-infringement of third-party rights, or fitness for a particular purpose.

Beansprout does not warrant, either expressly or impliedly, the accuracy or completeness of the information, text, graphics, links or other items contained in this document. Neither Beansprout nor any of its affiliates, directors, employees or other representatives will be liable for any damages, losses or liabilities of any kind arising out of or in connection with the use of this document. To the best of Beansprout’s knowledge, this document does not contain and is not based on any non-public, material information. The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to law or regulation, or which would subject Beansprout to any registration requirement within such jurisdiction or country. Beansprout is not licensed or regulated by any authority in any jurisdiction or country to provide the information in this document.

As a condition of your use of this document, you agree to indemnify, defend and hold harmless Beansprout and its affiliates, and their respective officers, directors, employees, members, managing members, managers, agents, representatives, successors and assigns from and against any and all actions, causes of action, claims, charges, cost, demands, expenses and damages (including attorneys’ fees and expenses), losses and liabilities or other expenses of any kind that arise directly or indirectly out of or from, arising out of or in connection with violation of these terms, use of this document, violation of the rights of any third party, acts, omissions or negligence of third parties, their directors, employees or agents. To the extent permitted by law, Beansprout shall not be liable to you, any other person, or organization, for any direct, indirect, special, punitive, exemplary, incidental or consequential damages, whether in contract, tort (including negligence), or otherwise, arising in any way from, or in connection with, the use of this document and/or its content. This includes, without limitation, liability for any act or omission in reliance on the information in this document. Beansprout expressly disclaims and excludes all warranties, conditions, representations and terms not expressly set out in this User Agreement, whether express, implied or statutory, with regard to this document and its content, including any implied warranties or representations about the accuracy or completeness of this document and the content, suitability and general availability, or whether it is free from error.

If these terms or any part of them is understood to be illegal, invalid or otherwise unenforceable under the laws of any state or country in which these terms are intended to be effective, then to the extent that they are illegal, invalid or unenforceable, they shall in that state or country be treated as severed and deleted from these terms and the remaining terms shall survive and remain fully intact and in effect and will continue to be binding and enforceable in that state or country.

These terms, as well as any claims arising from or related thereto, are governed by the laws of Singapore without reference to the principles of conflicts of laws thereof. You agree to submit to the personal and exclusive jurisdiction of the courts of Singapore with respect to all disputes arising out of or related to this Agreement. Beansprout and you each hereby irrevocably consent to the jurisdiction of such courts, and each Party hereby waives any claim or defence that such forum is not convenient or proper.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments