Fed warns inflation may rise. What it means for Singapore blue chip stocks

Stocks

By Gerald Wong, CFA • 19 Mar 2026

Why trust Beansprout? We’ve been awarded Best Investment Website at the SIAS Investors’ Choice Awards 2025

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M17.64%209.20455C17.64%208.56637%2017.5827%207.95273%2017.4764%207.36364H9V10.845H13.8436C13.635%2011.97%2013.0009%2012.9232%2012.0477%2013.5614V15.8195H14.9564C16.6582%2014.2527%2017.64%2011.9455%2017.64%209.20455V9.20455Z'%20fill='%234285F4'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%2018C11.43%2018%2013.4673%2017.1941%2014.9564%2015.8195L12.0477%2013.5614C11.2418%2014.1014%2010.2109%2014.4205%209%2014.4205C6.65591%2014.4205%204.67182%2012.8373%203.96409%2010.71H0.957275V13.0418C2.43818%2015.9832%205.48182%2018%209%2018V18Z'%20fill='%2334A853'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M3.96409%2010.71C3.78409%2010.17%203.68182%209.59318%203.68182%209C3.68182%208.40682%203.78409%207.83%203.96409%207.29V4.95818H0.957273C0.347727%206.17318%200%207.54773%200%209C0%2010.4523%200.347727%2011.8268%200.957273%2013.0418L3.96409%2010.71V10.71Z'%20fill='%23FBBC05'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9%203.57955C10.3214%203.57955%2011.5077%204.03364%2012.4405%204.92545L15.0218%202.34409C13.4632%200.891818%2011.4259%200%209%200C5.48182%200%202.43818%202.01682%200.957275%204.95818L3.96409%207.29C4.67182%205.16273%206.65591%203.57955%209%203.57955V3.57955Z'%20fill='%23EA4335'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_0_2849'%3e%3crect%20width='18'%20height='18'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Make Beansprout your preferred source on Google

Add us on Google to see more of our insights in your search results

With the Fed warning that inflation may climb, we look at how slower pace of rate cuts may impact Singapore blue chips, including banks, REITs and dividend stocks.

What happened?

Markets have been more volatile in the past few weeks.

With the escalation in the Middle East conflict, we have seen more uncertainty on the interest rate direction too.

For example, we have seen the latest T-bill yields edging up, and fixed deposit rates moving up, after declining for most of 2025.

This comes as higher oil prices lead investors to expect inflation to pick up again.

In this article, we look at the key takeaways from the US Federal Reserve’s latest meeting and what they could mean for the Singapore stock market.

What we learnt from the latest US Federal Reserve Meeting

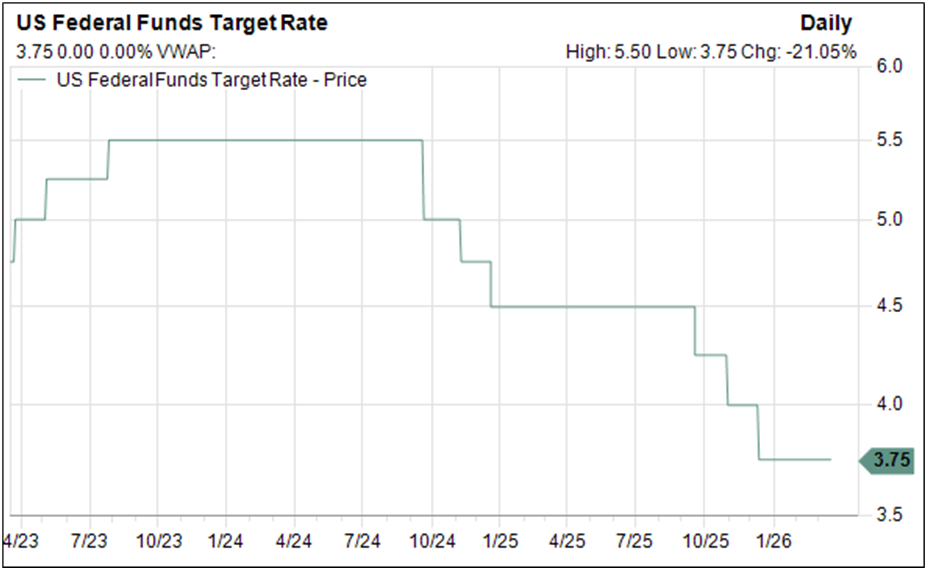

At its meeting on 18 March, the US Federal Reserve kept rates unchanged at 3.5 to 3.75%, as widely expected by investors.

This follows its stance of maintaining rates unchanged in the January meeting, after cutting interest rates by three times in 2025.

However, the bigger surprise was the more cautious tone from Fed Chairman Jerome Powell.

The Fed now expects personal consumption expenditures (PCE) inflation to be 2.7% in 2026, higher than the earlier estimate of 2.4%.

Core inflation, which excludes food and energy, is also expected to be 2.7%, up from 2.5%.

Inflation is now expected to come down more slowly, with projections for it to reach 2.2% in 2027 and return to the Fed’s 2% target by 2028.

The conflict in the Middle East has added another layer of uncertainty. Higher oil prices could keep inflation elevated for longer, even if the Fed still expects the impact to be temporary for now.

Markets had already gone into 2026 expecting only one to two rate cuts, and that outlook is now looking even less certain.

The Federal Reserve has signalled a more cautious path for rate cuts in 2026.

The dot plot, which shows the projections of Fed officials, indicates that most officials expect rates in 2026 to be between 3.25% and 3.50%, implying potentially one rate cut this year.

While the median has not changed, some officials are now expecting fewer numbers of cuts. Four or five officials went from expecting two rates cuts in 2026 to expecting just one rate cut.

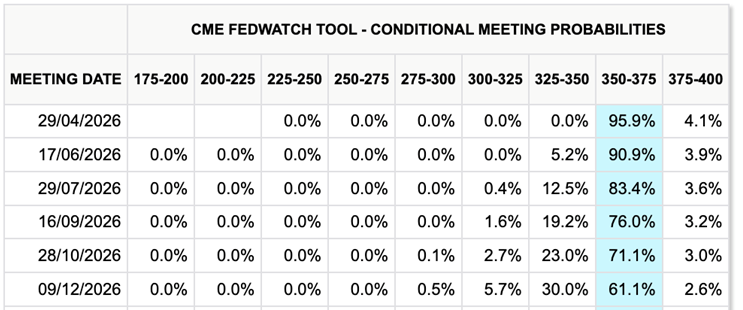

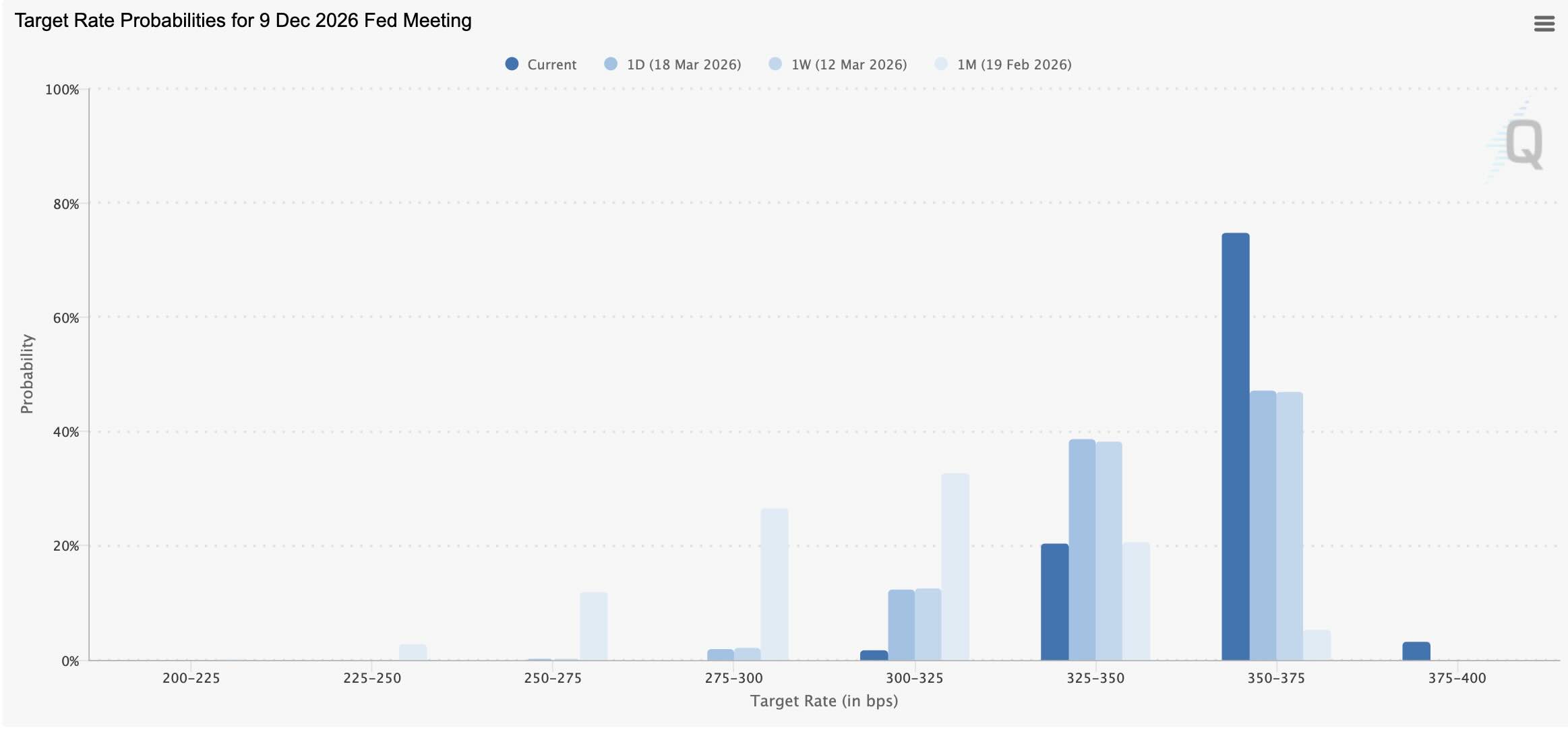

In fact, investors are now expecting rates to be maintained through 2026. According to the CME Fedwatch Tool, traders are pricing in a 60% probability that rates will stay at current level for the rest of the year.

Just one month ago, traders were assigning more than a 50% probability that there will be at least one rate cut this year.

To keep track of the latest rate cut probabilities, you can refer to the latest US Fed interest rate expectations here.

What the US interest rate outlook means for Singapore blue chip stocks

For Singapore stocks, a slower pace of US rate cuts does not necessarily mean the market will see an immediate sharp pullback.

However, it could mean the next phase of the market may be less driven by a broad rally, and more by differences across sectors.

In a higher for longer interest rate environment, returns are likely to depend more on which companies can continue to deliver resilient earnings.

For example, higher rates tend to support bank earnings because of stronger net interest margins, but they may be less favourable for rate sensitive sectors such as S-REITs, where borrowing costs are higher.

Here is how we would think about the different parts of the Singapore market.

#1 – Singapore stocks - Gains may be more selective

The STI is still trading near recent highs of around 5,000 points, supported by a relatively stable domestic backdrop.

Singapore’s economy is expected to continue growing in 2026, although likely at a slower pace than in 2025. Resilient domestic demand should still provide support for corporate earnings.

However, if the US Federal Reserve cuts rates more gradually, the market may not receive the same valuation boost that typically comes from sharply lower interest rates.

This means the next phase of the market may be less about a broad rally, and more about which sectors and companies can continue to deliver steady earnings.

In this environment, performance is likely to be driven more by sector rotation and stock selection rather than liquidity lifting the entire market.

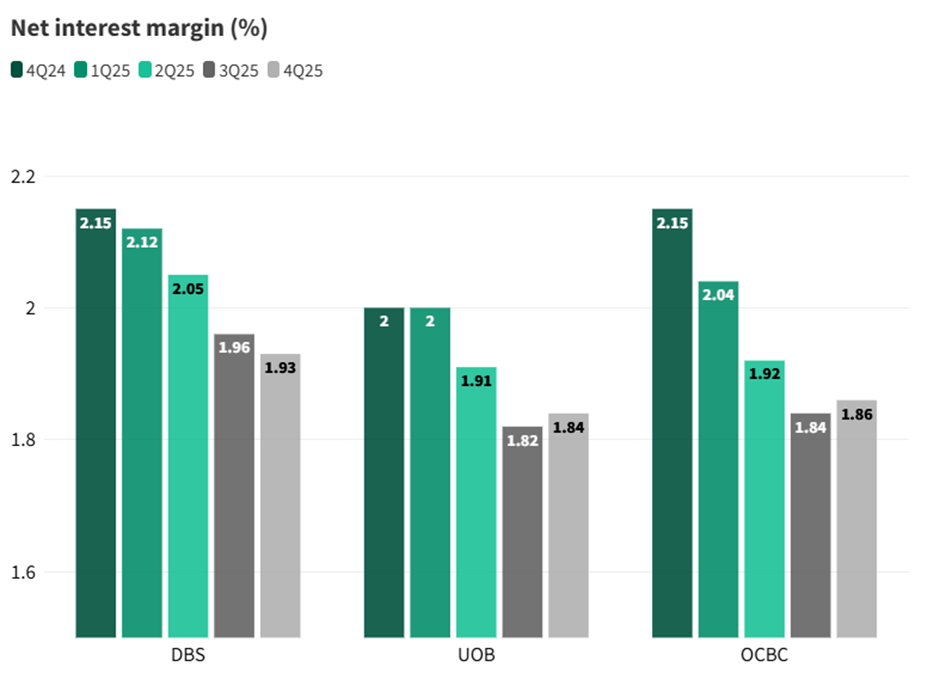

#1 - Singapore banks — Stable earnings and dividend support

Banks remain one of the most interest rate sensitive sectors in the Singapore market, and a higher for longer rate environment could help slow the pace of decline in net interest margins.

Margins have already started to ease in 2025, which has been a drag on bank earnings, so a more gradual path of rate cuts would be supportive.

Even if the US Federal Reserve begins cutting rates in the second half of 2026, the impact on margins is likely to be gradual rather than sharp. This should help cushion the pressure on earnings compared to a scenario where rates fall quickly.

At the same time, underlying business conditions remain stable. Loan growth has been steady, fee income remains healthy, and Singapore continues to attract wealth inflows during periods of global uncertainty, supporting wealth related fee income.

While net interest margins may continue to edge lower, earnings should be supported by diversified income streams, strong capital positions, and attractive dividend payouts.

All three local banks are currently guiding for broadly stable income in 2026.

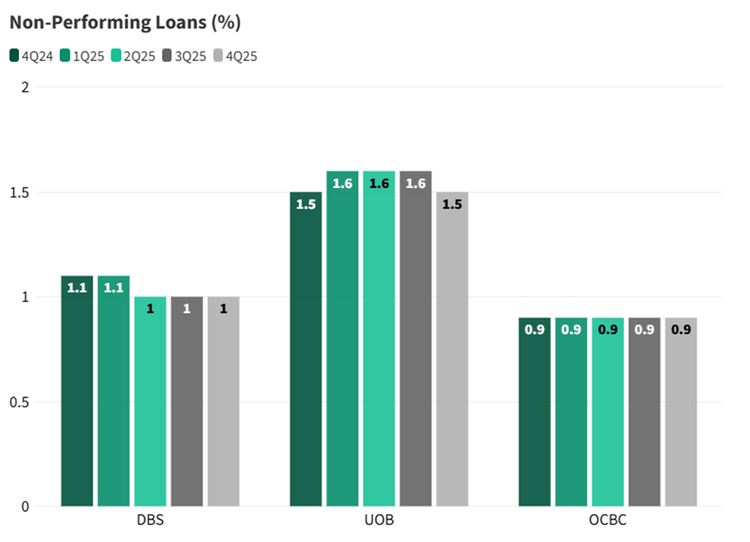

One risk to watch would be a sharper than expected slowdown in the global economy, especially if oil prices remain elevated for an extended period. This could lead to higher non performing loans and credit costs, which may weigh on bank earnings.

To learn more about how the Middle East conflict may impact DBS, UOB and OCBC, read our recent analysis on Singapore banks here.

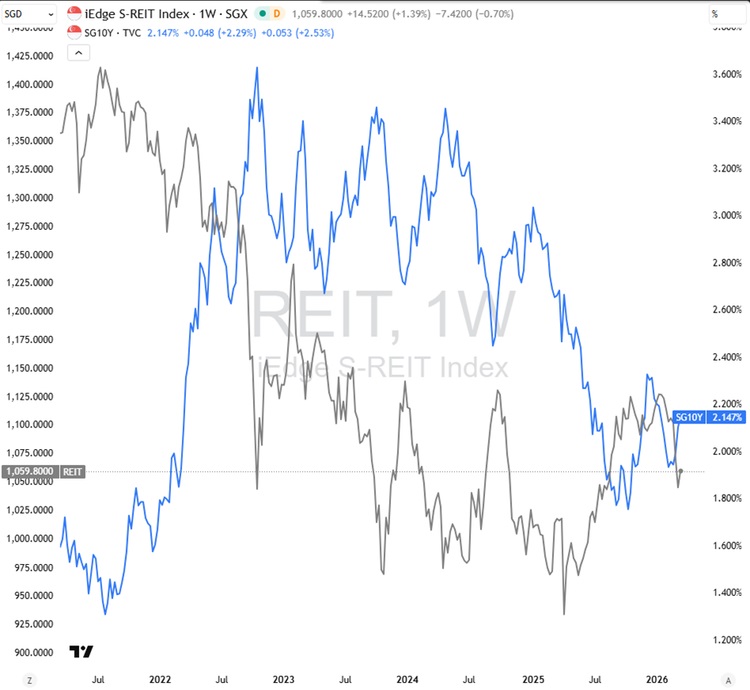

#2 - S-REITs and Property — Share price declines reflecting slower pace of rate cut expectations

Singapore REITs and property developers are among the most interest rate sensitive sectors in the Singapore market. Both sectors saw a recovery in share prices in 2025, supported by expectations that interest rates would fall more quickly.

However, the recent shift towards a slower pace of US rate cuts has started to weigh on sentiment. Over the past month, Singapore REITs and property stocks have pulled back as investors reassess how long borrowing costs may stay elevated. If inflation remains sticky, especially with higher energy prices, rate cuts could be delayed further.

Higher for longer interest rates mean refinancing costs may stay elevated for REITs, which could slow the recovery in distributions. For property developers, higher mortgage rates and financing costs may also dampen demand and limit earnings growth.

That said, companies with stronger bottom up drivers may be better cushioned if rates stay higher for longer. Some developers have been accelerating capital recycling through asset disposals and monetisation to improve returns, while REITs have stepped up acquisitions to drive inorganic growth.

Recent examples include Keppel REIT raised its stake in MBFC Tower 3, Keppel DC REIT acquired a Japan data centre, CapitaLand Ascendas REIT expanded its Singapore portfolio, and CapitaLand Integrated Commercial Trust (CICT) acquired CapitaSpring.

At the same time, REITs with exposure to structural growth areas such as data centres and healthcare may continue to see resilient rental demand, even in a more uncertain interest rate environment.

#3 - Structural growth themes may still stand out

In a slower rate cut environment, sectors supported by structural growth themes could still stand out, even if overall market gains become more selective. These are areas where earnings are driven more by long term demand trends rather than short term changes in interest rates.

Infrastructure is one example. While these assets are sensitive to interest rates, they are also supported by multi year investment cycles across Southeast Asia, including data centre expansion, the energy transition, transport networks, and utilities development.

Because of these structural drivers, companies with visible cash flows and exposure to long term spending pipelines may continue to perform relatively better, even if the pace of rate cuts is slower than previously expected.

What is the key risk to watch? What if the Fed does not cut at all?

The main risk to this outlook is that inflation starts to rise again, for example if geopolitical tensions keep oil prices elevated for longer. In that scenario, the US Federal Reserve may delay rate cuts, or keep interest rates unchanged for an extended period.

If rates stay higher for longer, the sectors that had benefited from expectations of lower interest rates, such as S-REITs and property developers, could remain under pressure. Banks may hold up relatively better at first, as higher rates continue to support margins, while sectors driven by structural growth themes may also be more resilient.

However, we would also be watchful for whether a slower pace of rate cuts comes together with a more significant slowdown in the economy. If growth weakens meaningfully, cyclical sectors could be affected more broadly, including the banks, as loan growth slows and credit costs start to rise.

To assess whether these risks are building, we would watch a few key indicators closely, including US core PCE inflation, the trend in oil prices, signs of slowing economic data, and the tone of the Fed’s communication after each FOMC meeting.

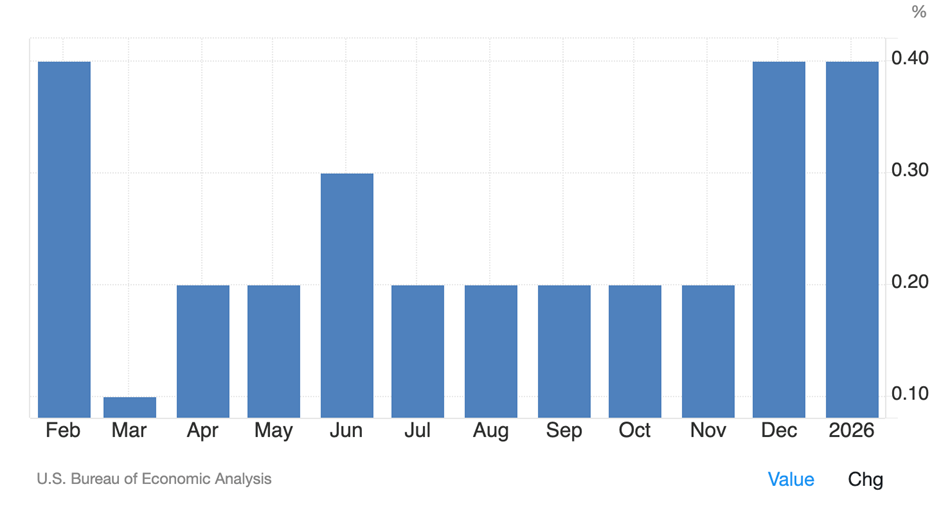

For example, the core PCE price index in the US, which is the Federal Reserve's preferred gauge of underlying inflation in the US economy, rose by 0.4% from the previous month in January of 2026, the same pace as the 10-month high from the previous month.

What would Beansprout do?

With the recent geopolitical tensions and uncertainty around the interest rate outlook, I have been reviewing my own financial plan to make sure it still provides enough security and peace of mind. Rather than trying to predict every market move, the focus is on making sure each part of the portfolio is positioned for different scenarios.

First, I would make sure I have sufficient cash put aside for emergency uses, held in instruments such as savings accounts, fixed deposits, T-bills, Singapore Savings Bonds and money market funds. The goal here is not to maximise returns, but to ensure stability and flexibility, while earning a reasonable yield on idle cash. Find out the best place to park your cash to earn a higher yield here.

Second, I would look for income opportunities, especially during periods of market pullback. When prices fall, yields on income assets can become more attractive. For example, the recent decline in Singapore REIT prices has pushed up dividend yields, which may offer opportunities for investors looking for steady income. Read about Singapore REITs with dividend yields above 6%, Singapore blue chip stocks with dividend yields of above 5%, and ETFs with dividend yields of above 6%.

Third, for long term growth, I would continue to invest gradually rather than wait for the perfect entry point. Using a dollar cost averaging approach helps reduce the risk of mistiming the market, and allows investors to stay invested through different interest rate and market cycles. Read about best S&P 500 ETF, best STI ETF, and how to buy gold in Singapore here.

Finally, I would continue to look for opportunities in structural growth themes. Even in a slower rate cut environment, sectors supported by long term trends such as infrastructure, data centres, energy transition and regional development could still deliver earnings growth over time. Read about Beansprout’s stock ideas here.

Overall, the key is not to move entirely to cash or try to time every shift in interest rates, but to stay diversified across liquidity, income, and growth, so the portfolio can remain resilient through different market conditions.

[Beansprout Exclusive Longbridge Promotion] Get bonus S$50 FairPrice voucher within 5 working days, plus 5% p.a. interest boost coupon (worth ~S$100) when you sign up for a Longbridge account via Beansprout. Plus, stand a chance to win 1g of gold bar. Promo ends on 31 March 2026. T&Cs apply. Learn more about the Longbridge promotion here.

Found this insight helpful? Follow Beansprout on Telegram, Youtube, Facebook and Instagram, and add Beansprout as your preferred source on Google so you never miss an update.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Most Popular

Comments

0 comments